Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

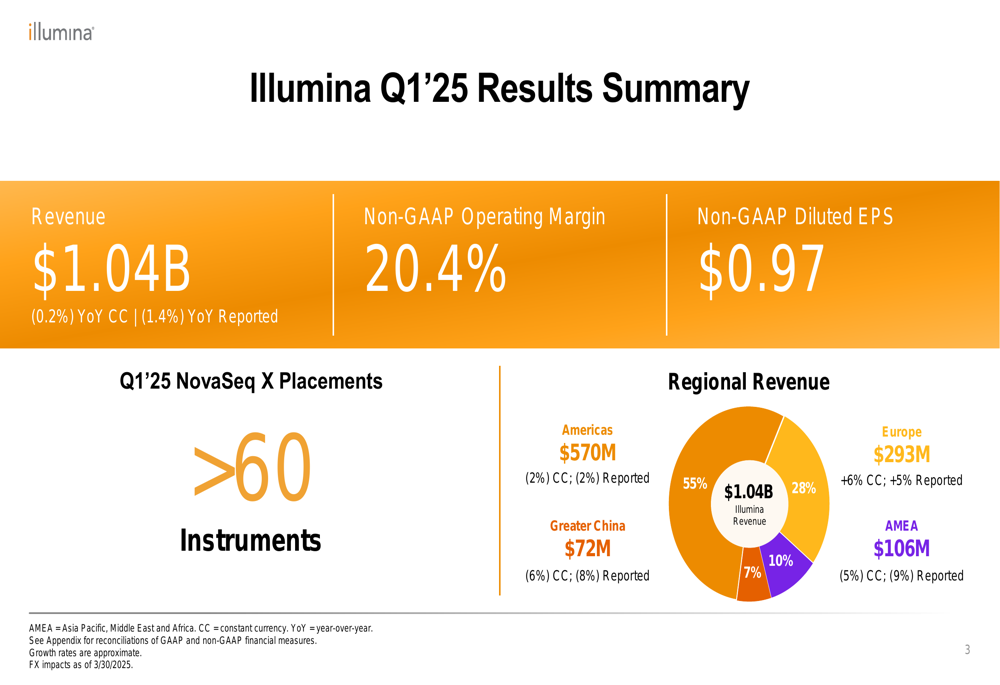

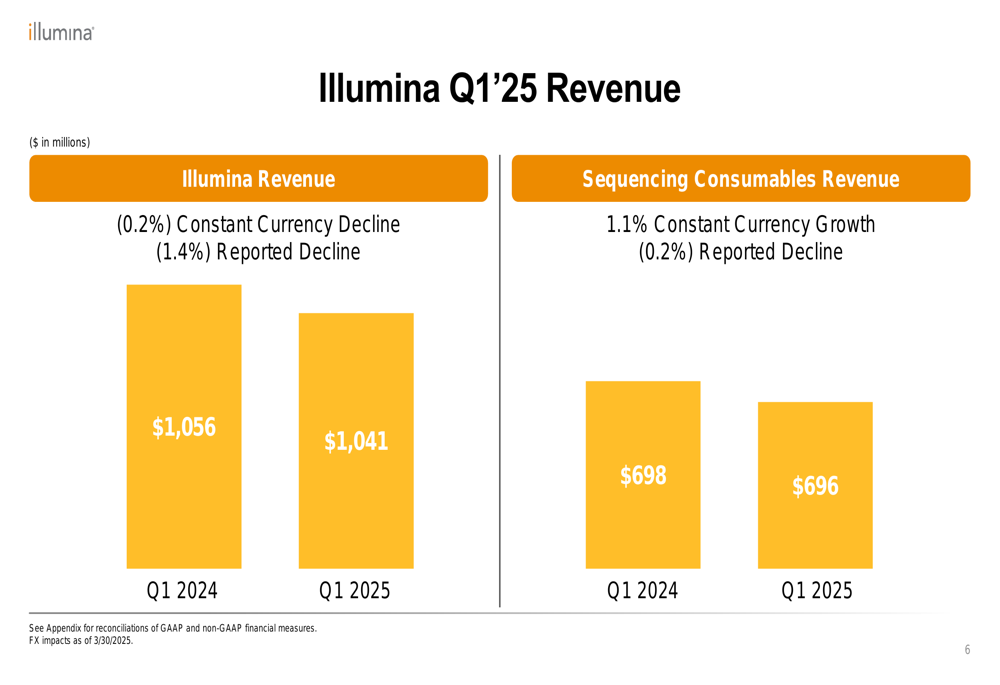

Illumina Inc. (NASDAQ:ILMN) released its Q1 2025 earnings presentation on May 8, 2025, reporting revenue of $1.04 billion, representing a slight year-over-year decline of 0.2% in constant currency (1.4% reported). The genomic sequencing leader faces multiple headwinds, including China export restrictions, U.S. research funding uncertainty, and global tariff implementation, prompting a downward revision of its full-year guidance despite implementing cost reduction measures.

The stock fell 3.05% to $77.15 in after-hours trading following the earnings release, reflecting investor concerns about the revised outlook. This decline continues a challenging period for Illumina, whose shares have traded closer to their 52-week low of $68.70 than their high of $156.66.

Quarterly Performance Highlights

Illumina reported Q1 2025 non-GAAP diluted earnings per share of $0.97, slightly below the $0.98 reported in Q1 2024. Non-GAAP operating margin came in at 20.4%, down 20 basis points from 20.6% in the prior-year period, while gross margin improved slightly to 67.4% from 67.1%.

The company’s regional performance showed mixed results, with Europe delivering 6% constant currency growth, while the Americas, Greater China, and Asia Pacific, Middle East and Africa (AMEA) regions experienced declines of 2%, 6%, and 5% respectively in constant currency terms.

As shown in the following quarterly results summary:

Sequencing consumables revenue, which represents the company’s recurring revenue stream, showed resilience with 1.1% constant currency growth despite a 0.2% reported decline to $696 million. Meanwhile, sequencing instruments revenue remained relatively flat with 0.2% constant currency growth but a 0.9% reported decline to $109 million.

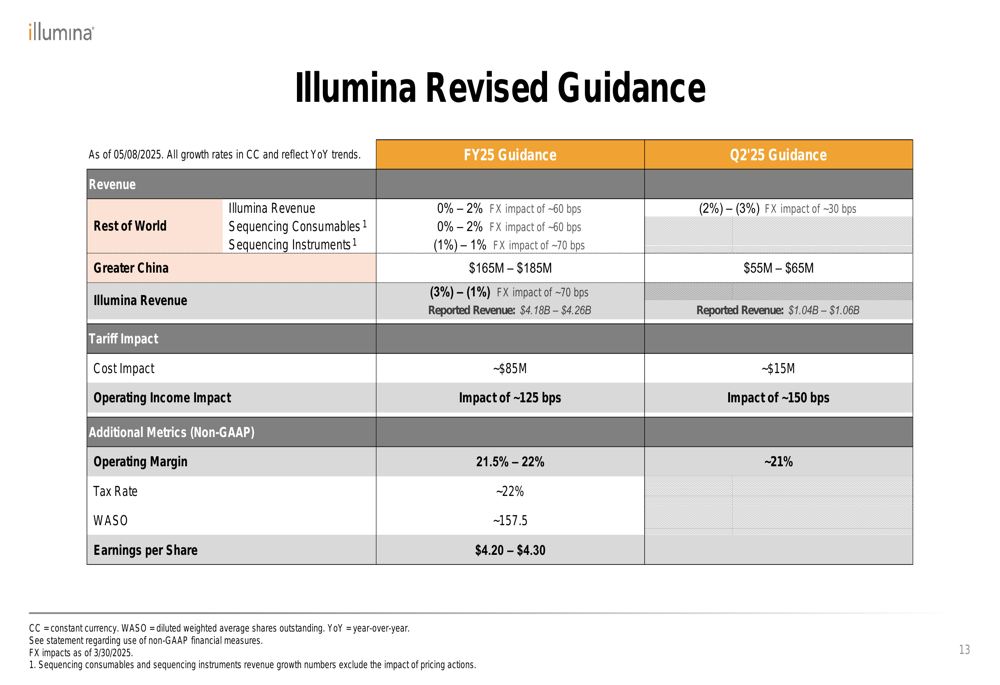

Revised Guidance & Challenges

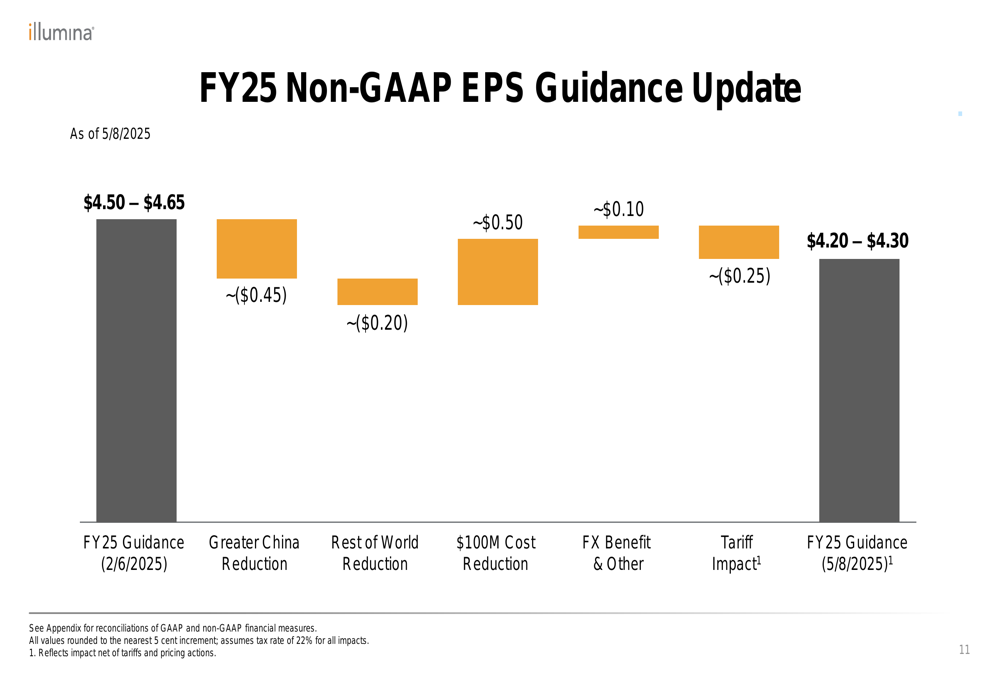

Illumina significantly revised its full-year 2025 guidance, reducing its non-GAAP EPS forecast from the previously announced range of $4.50-$4.65 to $4.20-$4.30. This adjustment reflects several challenges the company is facing, including an approximately $0.45 reduction from Greater China, $0.20 from Rest of World, and $0.25 from tariff impacts, partially offset by $0.50 benefit from cost reductions and $0.10 from foreign exchange and other factors.

The following waterfall chart illustrates these changes to the company’s guidance:

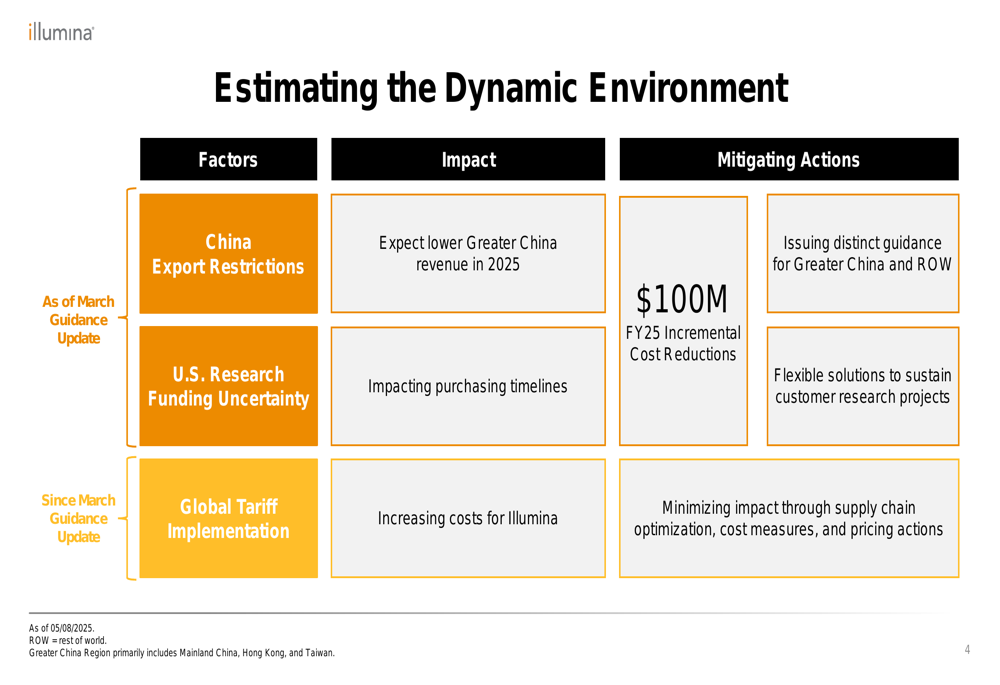

The company outlined three major factors impacting its business environment: China export restrictions, which are expected to lower Greater China revenue in 2025; U.S. research funding uncertainty affecting purchasing timelines; and global tariff implementation increasing costs. In response, Illumina is implementing a $100 million incremental cost reduction program for FY25.

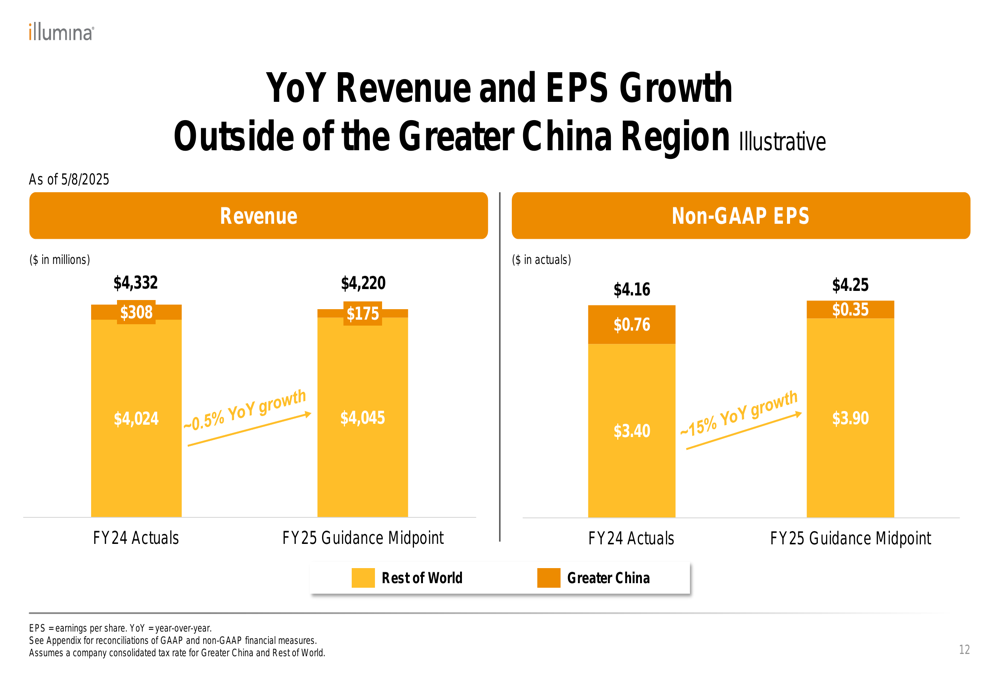

For the full year 2025, Illumina now expects revenue to decline 1-3% in constant currency terms, with sequencing consumables projected to range from a 1% decline to 1% growth. The company anticipates Greater China revenue of $165-185 million, significantly lower than the $308 million reported in FY24.

Strategic Initiatives

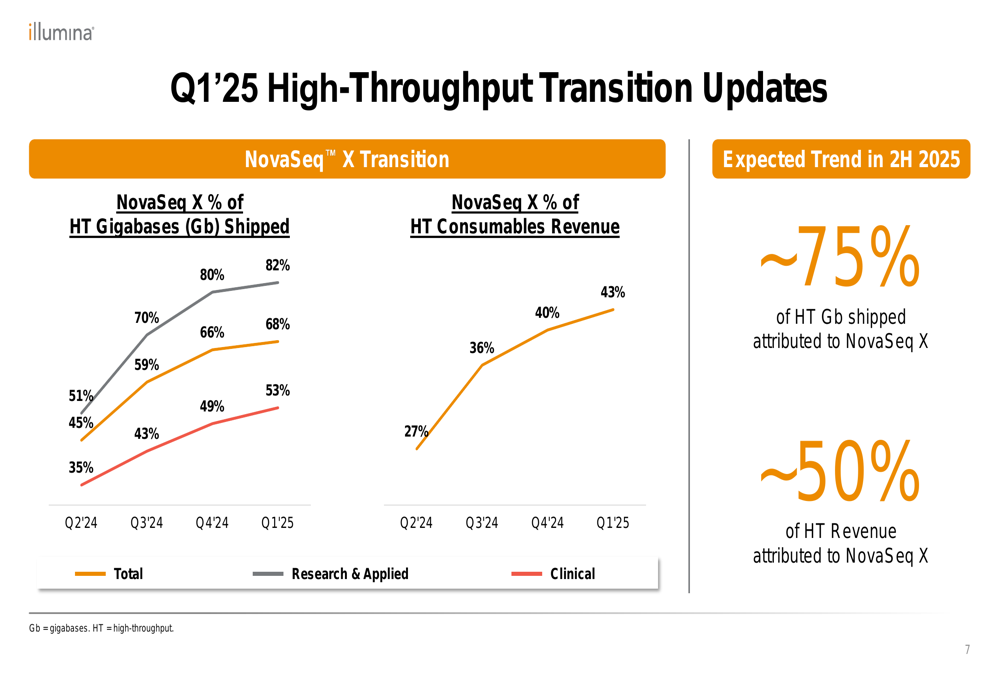

Despite the challenging environment, Illumina continues to make progress on its high-throughput transition to the NovaSeq X platform. The company placed over 60 NovaSeq X instruments in Q1 2025 and expects the platform to account for approximately 75% of high-throughput gigabases shipped and 50% of high-throughput revenue by the second half of 2025.

The following chart shows the NovaSeq X transition progress:

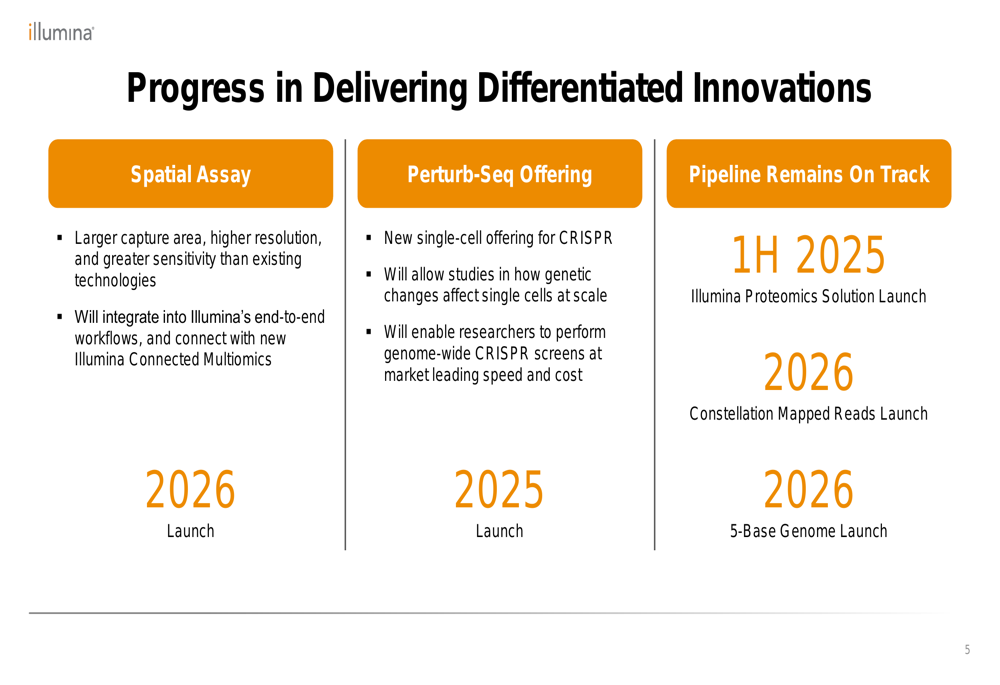

Illumina also highlighted its product innovation pipeline, which includes several planned launches over the next two years. The company expects to launch its Proteomics Solution in the first half of 2025 and its Perturb-Seq Offering later in 2025. Looking further ahead, Illumina plans to introduce its Spatial Assay, Constellation Mapped Reads, and 5-Base Genome technologies in 2026.

Financial Position

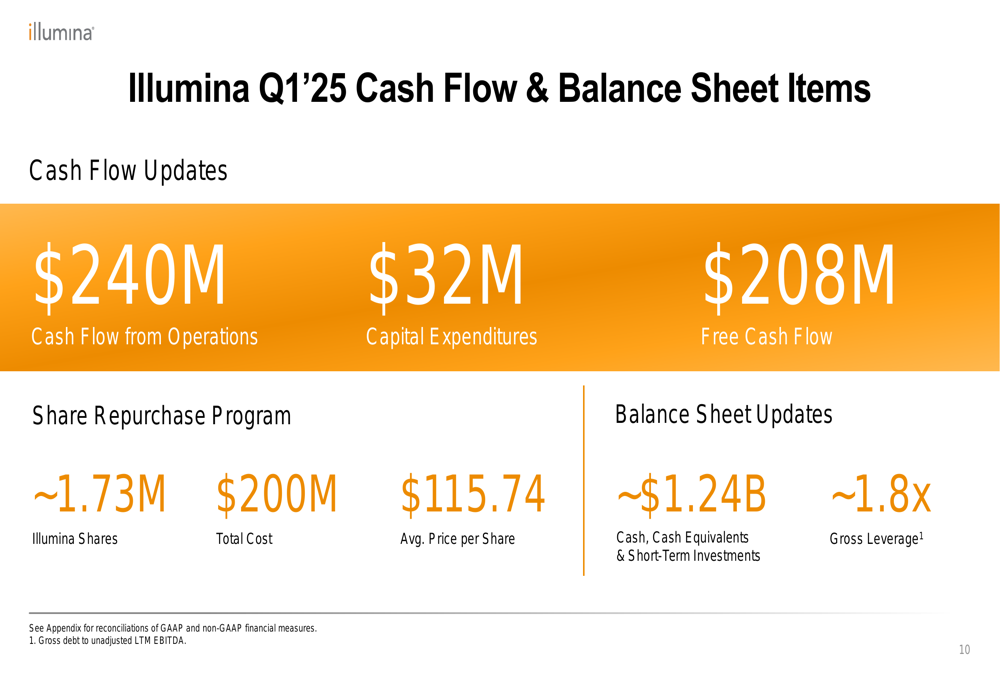

Illumina maintained a solid financial position in Q1 2025, generating $240 million in cash flow from operations and $208 million in free cash flow. The company continued its share repurchase program, buying back approximately 1.73 million shares at a total cost of $200 million, with an average price of $115.74 per share.

As of the end of Q1, Illumina reported approximately $1.24 billion in cash, cash equivalents, and short-term investments, with gross leverage of approximately 1.8x (gross debt to unadjusted LTM EBITDA).

While Illumina faces significant headwinds in Greater China, the company emphasized that its business outside this region is showing resilience. Excluding Greater China, Illumina projects approximately 15% year-over-year growth in non-GAAP EPS for FY25, despite an expected 0.5% revenue decline.

As Illumina navigates these challenges, the company’s focus on cost management, strategic product transitions, and continued innovation will be critical to maintaining its leadership position in the genomic sequencing market while addressing the current global economic and regulatory uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.