Gold prices hit 4-month high on Fed easing hopes, tariff uncertainty

Introduction & Market Context

Illumina Inc. (NASDAQ:ILMN) presented its second-quarter 2025 earnings results on July 31, revealing a mixed performance characterized by revenue challenges but improved profitability. The genomic sequencing leader reported a 3% year-over-year revenue decline while simultaneously expanding its operating margin and announcing a strategic acquisition to bolster its multiomics capabilities.

The company’s stock declined 0.62% in after-hours trading following the earnings release, adding to a 3.57% drop during regular trading hours. This reaction suggests investor concerns about Illumina’s ongoing revenue challenges, despite the company’s efforts to improve profitability and position itself for future growth.

Quarterly Performance Highlights

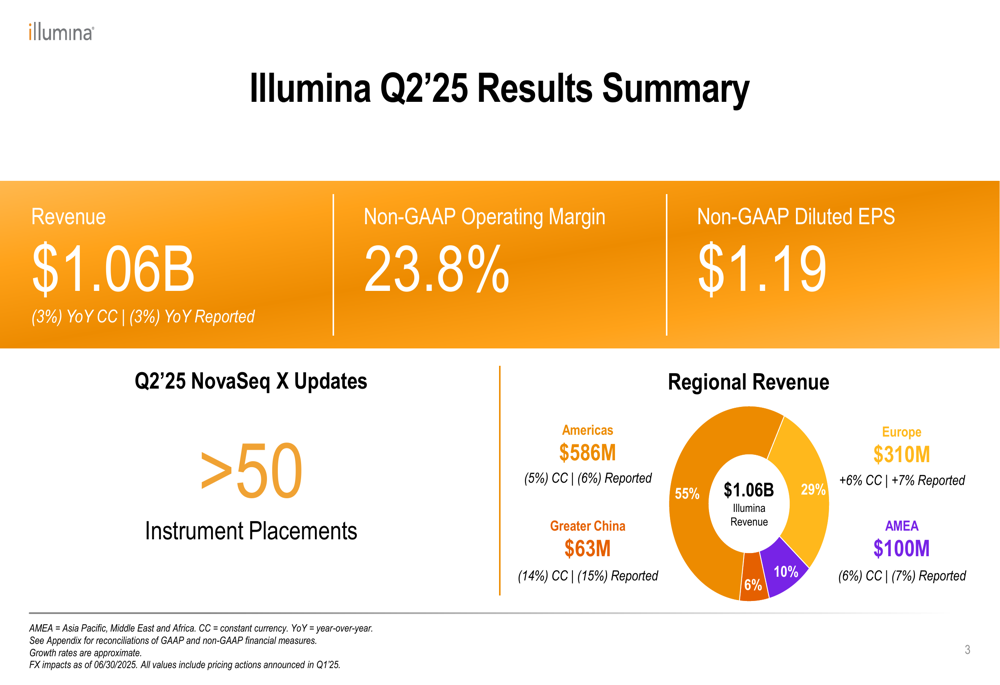

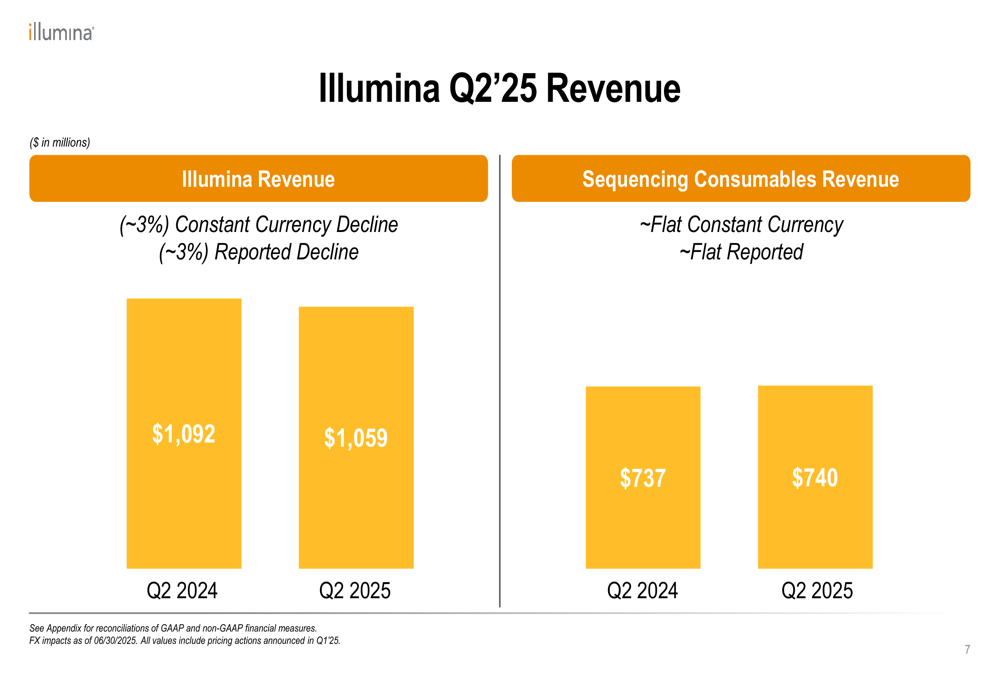

Illumina reported Q2 2025 revenue of $1.06 billion, representing a 3% year-over-year decline both on a constant currency and reported basis. Despite this revenue contraction, the company achieved a non-GAAP operating margin of 23.8% and non-GAAP diluted earnings per share of $1.19.

As shown in the following comprehensive results summary:

The company’s regional performance varied significantly, with Europe showing the strongest growth at 6% in constant currency, while Greater China experienced the steepest decline at 14%. The Americas, which accounts for 55% of total revenue, declined 5% in constant currency.

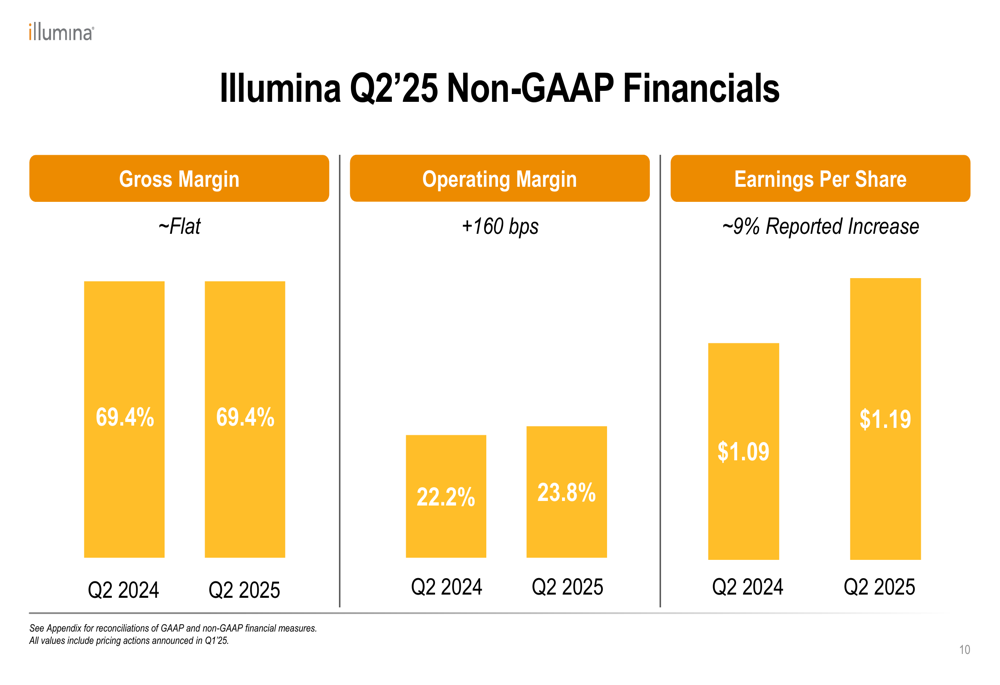

Illumina’s financial metrics demonstrated resilience in the face of revenue headwinds, with non-GAAP earnings per share increasing approximately 9% year-over-year from $1.09 to $1.19. This improvement was supported by expanded operating margins, which increased 160 basis points from 22.2% to 23.8%.

The following chart illustrates these key financial metrics:

Strategic Initiatives

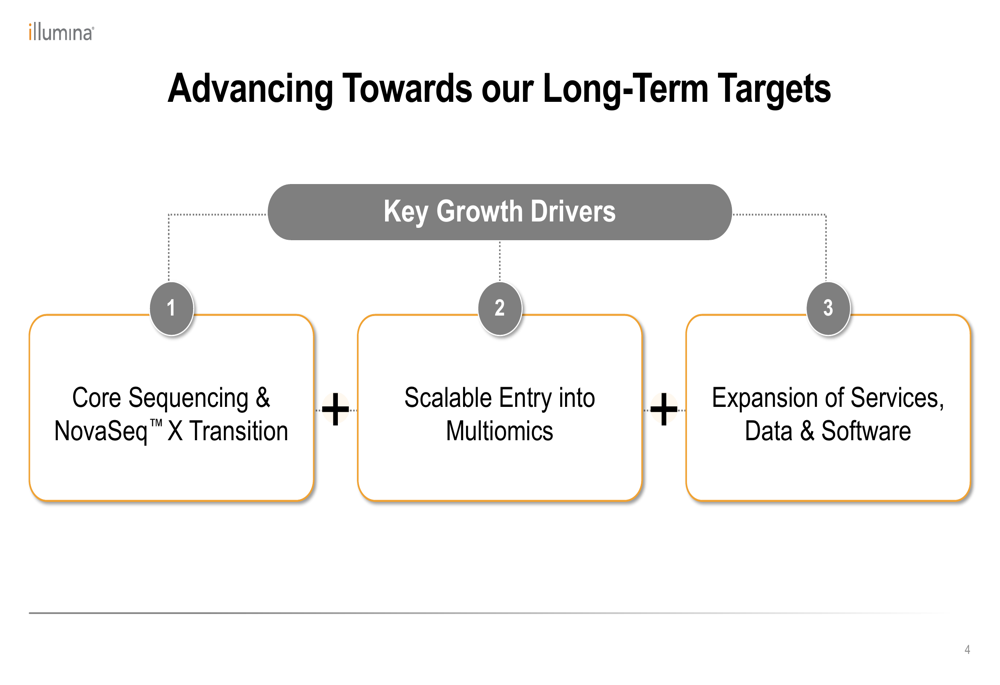

Illumina outlined three key pillars of its long-term growth strategy: Core Sequencing & NovaSeq X Transition, Scalable Entry into Multiomics, and Expansion of Services, Data & Software (ETR:SOWGn). These strategic initiatives are designed to position the company for sustainable growth despite current headwinds.

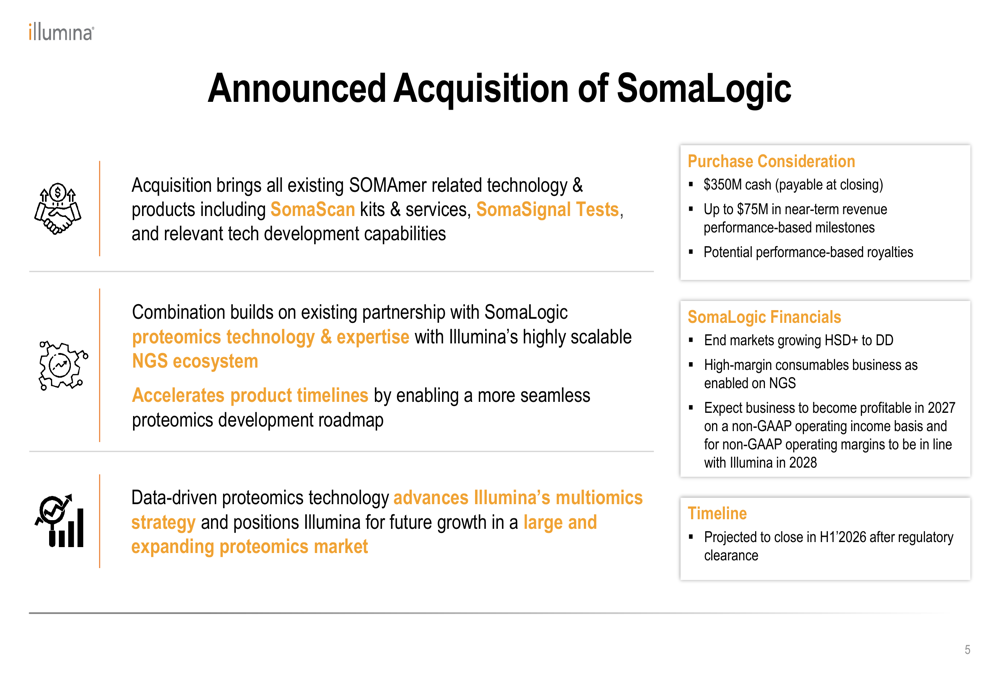

In a significant strategic move, Illumina announced the acquisition of SomaLogic, a leader in proteomics technology. The acquisition, valued at $350 million in cash with potential additional performance-based payments of up to $75 million, is expected to accelerate Illumina’s multiomics strategy and product development timelines.

The following details highlight the strategic rationale and financial terms of the SomaLogic acquisition:

The company also reported progress in its product portfolio expansion, with over 500 placements of its MiSeq i100 Plus instrument since launch and continued momentum in the NovaSeq X transition. Illumina placed over 50 NovaSeq X instruments in Q2 2025 and reported greater than 10% quarter-over-quarter growth in NovaSeq X consumables revenue.

Detailed Financial Analysis

Breaking down Illumina’s Q2 2025 revenue components reveals varying performance across product categories. Sequencing consumables revenue remained flat year-over-year at $740 million, while sequencing instruments revenue declined 18% to $96 million, reflecting challenges in instrument placements.

The following chart details these revenue components:

Sequencing service and other revenue also declined 5% year-over-year to $136 million. Despite these revenue challenges, Illumina maintained its gross margin at 69.4%, identical to the year-ago period, while improving operating efficiency to drive margin expansion.

The company’s cash flow remained strong, with $234 million in cash flow from operations and $204 million in free cash flow during the quarter. Illumina also continued its share repurchase program, buying back approximately 4.5 million shares at a total cost of $380 million, representing an average price of $84.66 per share.

Forward-Looking Statements

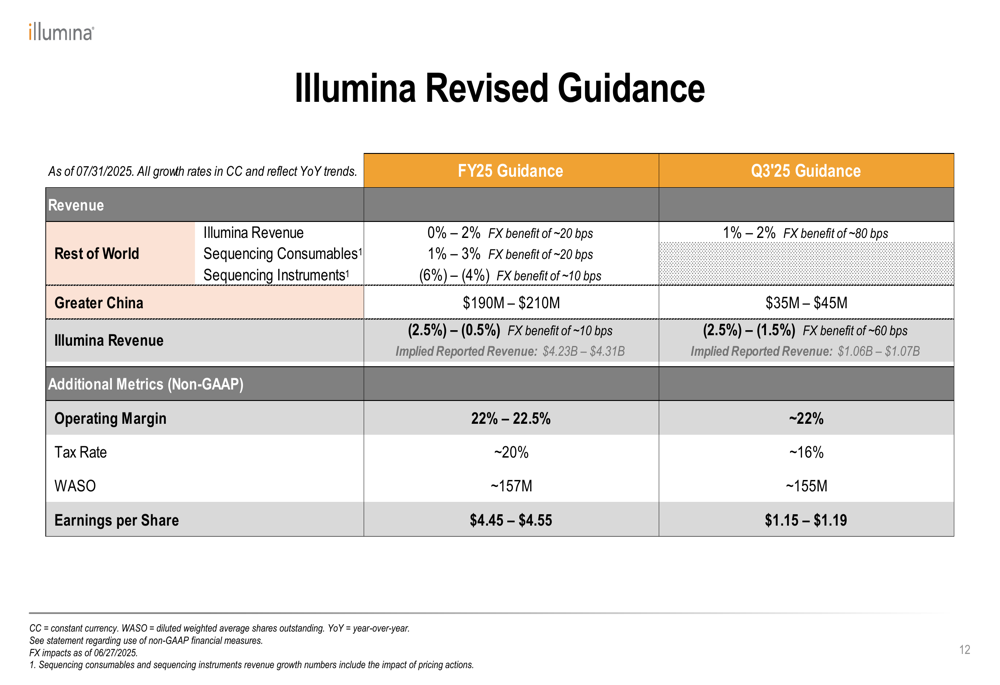

Illumina revised its full-year 2025 guidance, projecting revenue to decline between 2.5% and 0.5% on a constant currency basis, with an implied reported revenue range of $4.23 billion to $4.31 billion. For Q3 2025, the company expects revenue to decline between 2.5% and 1.5%.

The detailed guidance table below outlines Illumina’s expectations for the remainder of 2025:

Despite revenue challenges, Illumina projects full-year non-GAAP operating margins of 22% to 22.5% and earnings per share of $4.45 to $4.55. The company faces particular headwinds in Greater China, where it projects full-year revenue of $190 million to $210 million, with Q3 revenue expected to be just $35 million to $45 million.

The NovaSeq X transition remains a key focus, with Illumina targeting approximately 75% of high-throughput gigabases shipped and approximately 50% of high-throughput revenue to come from NovaSeq X by the end of 2025. This transition is crucial for the company’s long-term competitive positioning in the sequencing market.

While Illumina continues to face revenue challenges, its margin expansion, strategic acquisitions, and product transitions demonstrate management’s efforts to position the company for future growth in the evolving genomics and multiomics landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.