Japan PPI inflation slips to 11-mth low in July

Introduction & Market Context

Indosat Tbk (IDX:ISAT) released its first quarter 2025 results on April 30, showing improved profitability despite revenue challenges. The Indonesian telecommunications provider reported a sequential improvement in key financial metrics, with a particular focus on cost optimization and artificial intelligence initiatives to drive future growth.

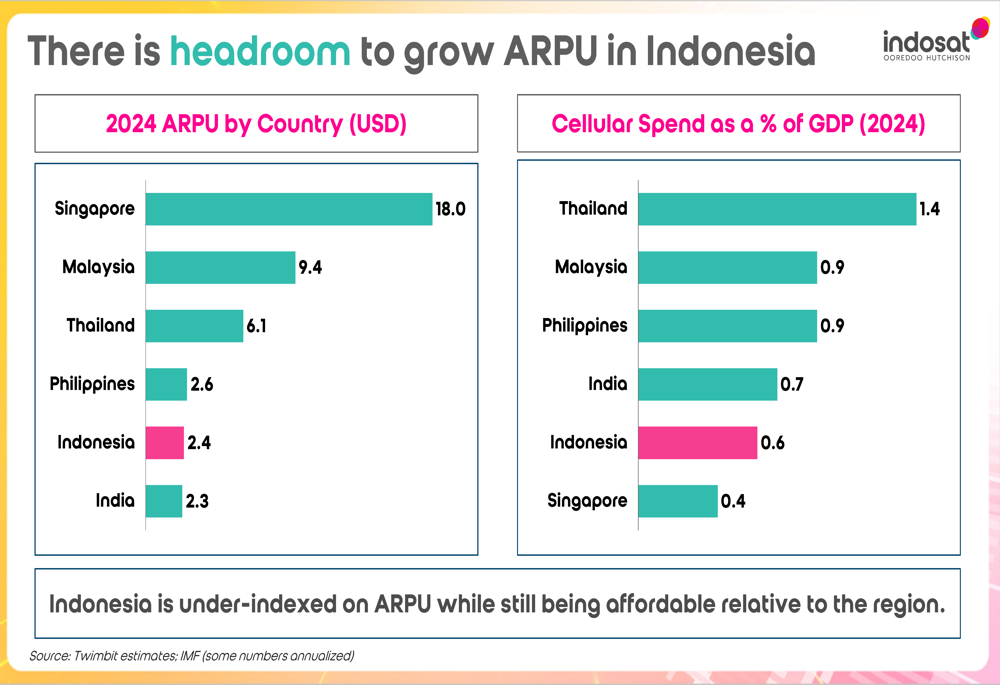

The company’s stock has faced pressure following the announcement, with fundamentals data showing a 9.56% decline. This comes despite Indosat’s strategic positioning in a market that appears to have significant ARPU (Average Revenue Per User) growth potential compared to regional peers.

As shown in the following chart comparing regional ARPU levels, Indonesia remains under-indexed at $2.4 USD, suggesting room for growth while maintaining affordability relative to neighboring countries:

Quarterly Performance Highlights

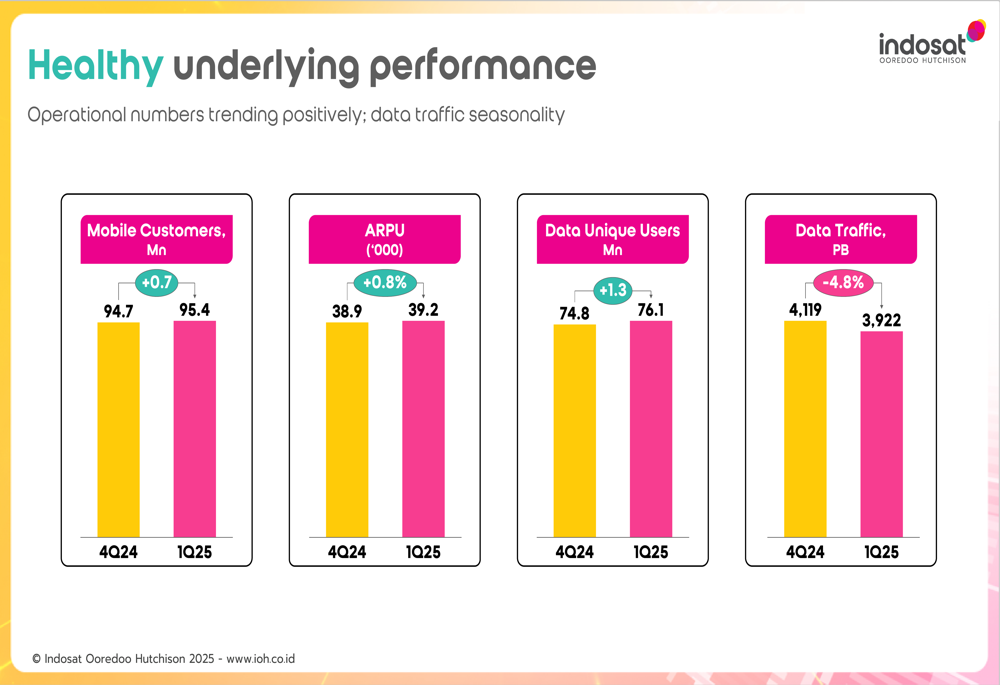

Indosat reported sequential improvement in profitability for Q1 2025, despite operating in what the company described as a "challenging environment." Key performance metrics showed mixed results, with customer growth and profitability improving while revenue declined.

The company’s sequential performance improvements include customer growth of 0.7 million, data unique users increase of 1.3 million, ARPU growth of 0.8%, EBITDA improvement of 0.6%, and normalized net profit growth of 6.0% quarter-over-quarter.

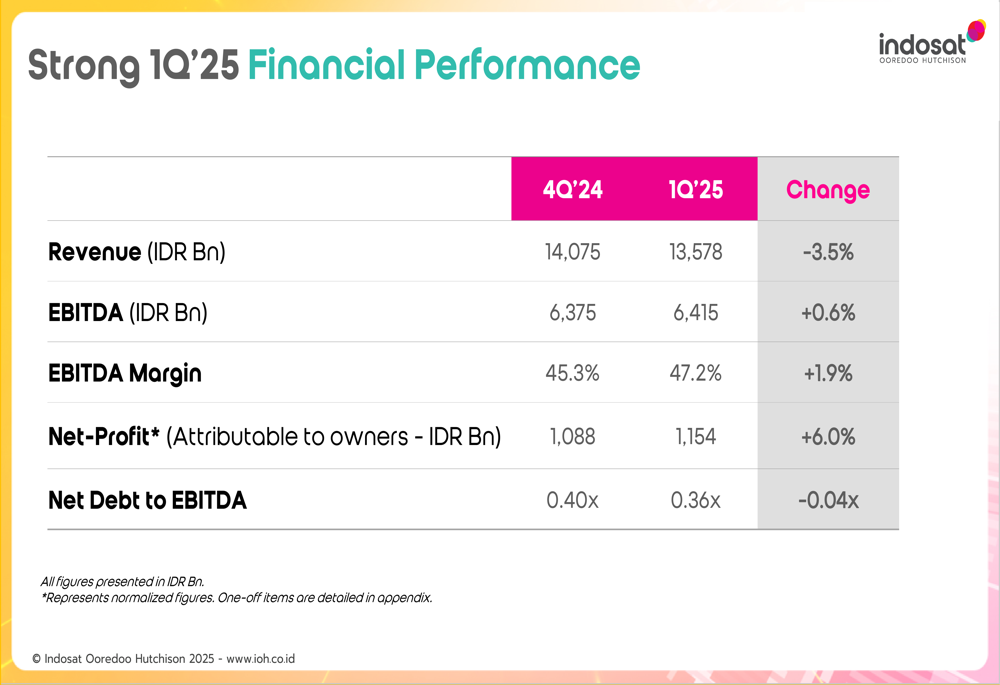

The following slide illustrates these key performance indicators:

In terms of financial performance, Indosat reported revenue of 13,578 IDR billion, representing a 3.5% decrease compared to the previous quarter and a 1.9% year-over-year decline. However, EBITDA reached 6,415 IDR billion with a margin of 47.2%, showing a 1.9 percentage point improvement quarter-over-quarter.

The company’s detailed financial performance is presented in the following slide:

Normalized net profit, which excludes one-off items, increased by 6.0% quarter-over-quarter to 1,154 IDR billion. The reported net profit was 1,311 IDR billion, representing a more substantial 27.0% increase from the previous quarter, largely due to one-off gains.

Cost Optimization Strategy

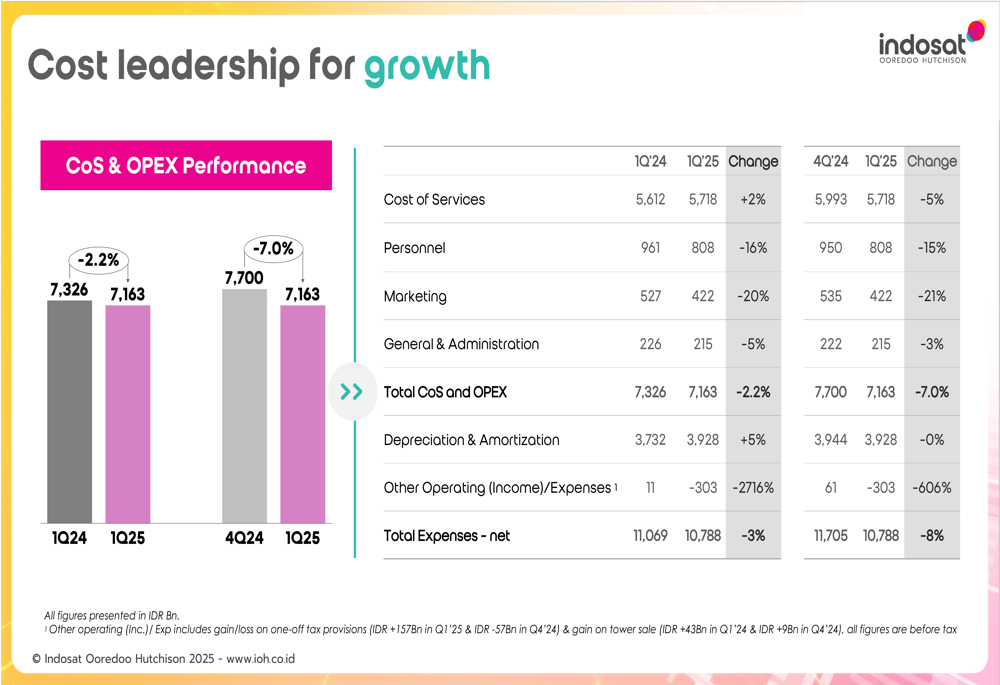

A key driver of Indosat’s improved profitability despite revenue challenges has been its aggressive cost optimization strategy. The company reported significant reductions across multiple expense categories compared to both the previous quarter and the same period last year.

Personnel costs decreased by 16% year-over-year and 15% quarter-over-quarter, while marketing expenses were reduced by 20% year-over-year and 21% quarter-over-quarter. General and administrative expenses also saw reductions of 5% year-over-year and 3% quarter-over-quarter.

The following slide details the company’s cost leadership initiatives:

These cost optimization efforts resulted in total cost of services and operating expenses decreasing by 7.0% quarter-over-quarter to 7,163 IDR billion. This disciplined approach to cost management has enabled Indosat to improve its EBITDA margin despite the revenue decline.

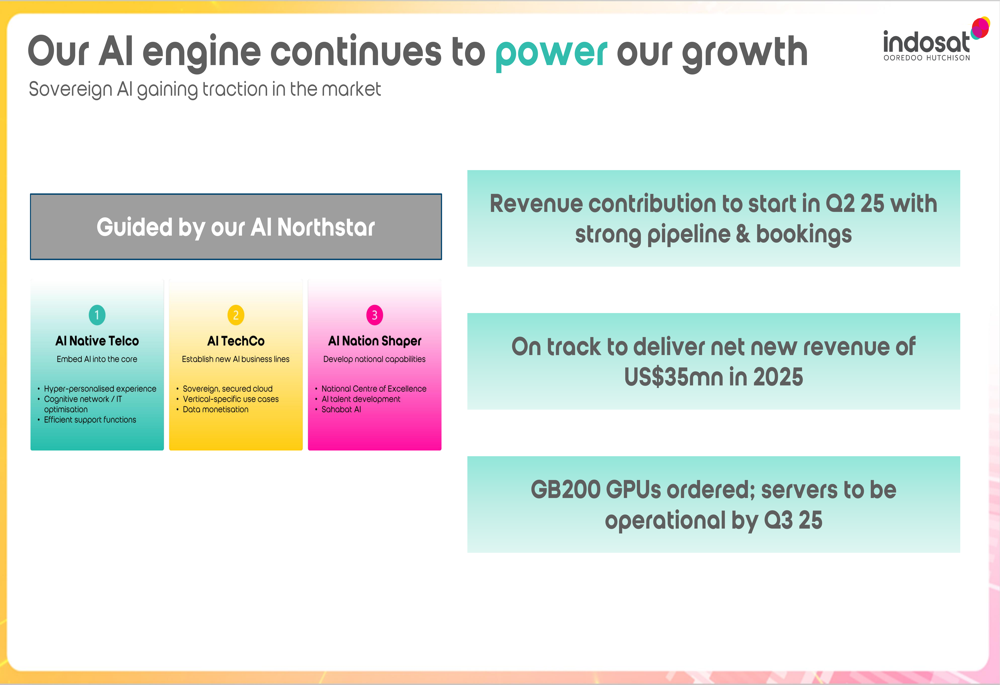

AI Initiatives and Future Growth

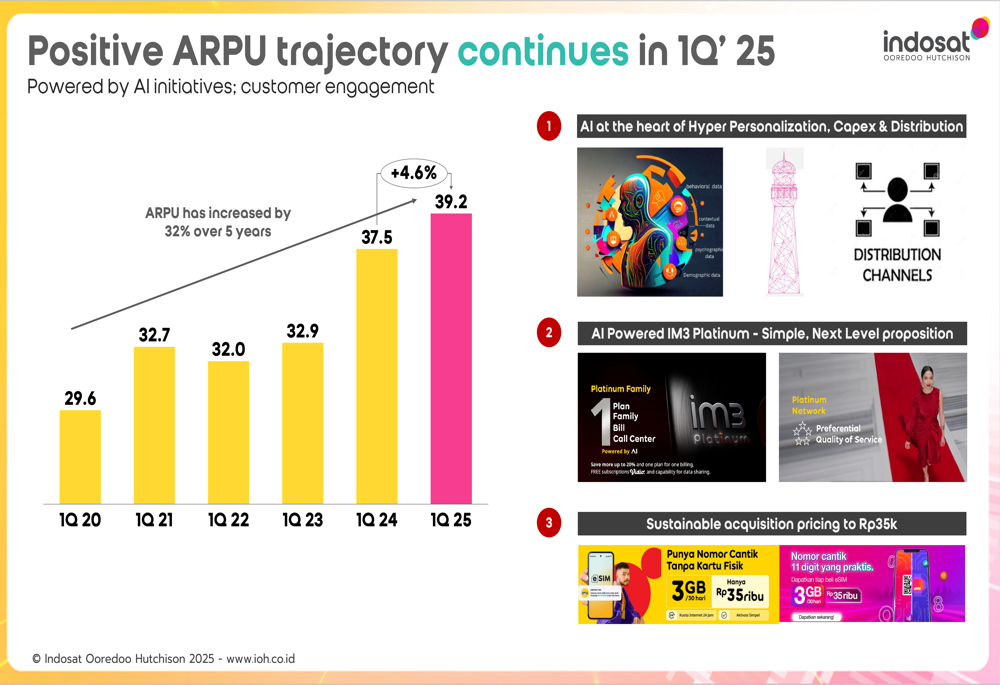

Indosat is placing significant emphasis on artificial intelligence as a key driver of future growth. The company’s ARPU has shown consistent improvement, increasing by 32% over the past five years from 29.6 in Q1 2020 to 39.2 in Q1 2025, with AI initiatives playing an increasingly important role in this growth.

The following slide illustrates this positive ARPU trajectory and the AI-driven initiatives supporting it:

The company’s AI strategy is built around three pillars: AI Native Telco (embedding AI into core operations), AI TechCo (establishing new AI business lines), and AI Nation Shaper (developing national capabilities). Indosat expects these initiatives to begin contributing to revenue in Q2 2025, with a target of delivering $35 million in new revenue in 2025.

As shown in the following slide detailing the company’s AI engine and growth strategy:

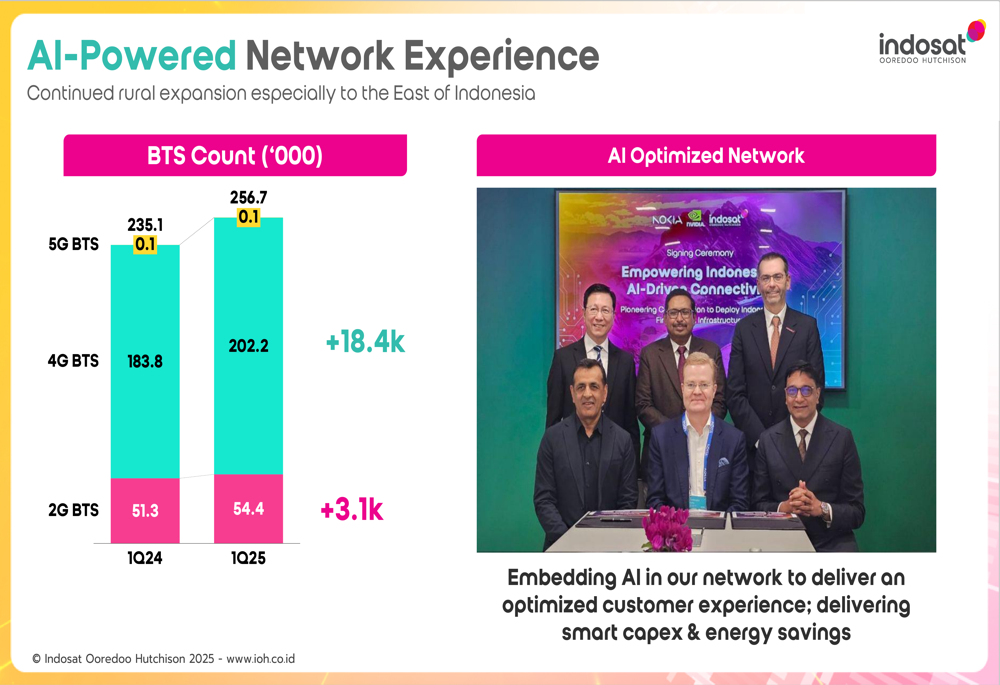

Network Expansion

Indosat continues to invest in network expansion, with a particular focus on rural areas in Eastern Indonesia. The company reported growth in its base transceiver station (BTS) counts across 2G, 4G, and 5G technologies.

The company’s AI-powered network experience and expansion efforts are illustrated in the following slide:

Operational metrics showed positive trends, with mobile customers reaching 95.4 million (an increase of 0.7 million quarter-over-quarter) and data unique users growing to 76.1 million (up 1.3 million quarter-over-quarter). However, data traffic decreased by 4.8% quarter-over-quarter to 3,922 PB.

The company’s operational performance is detailed in this slide:

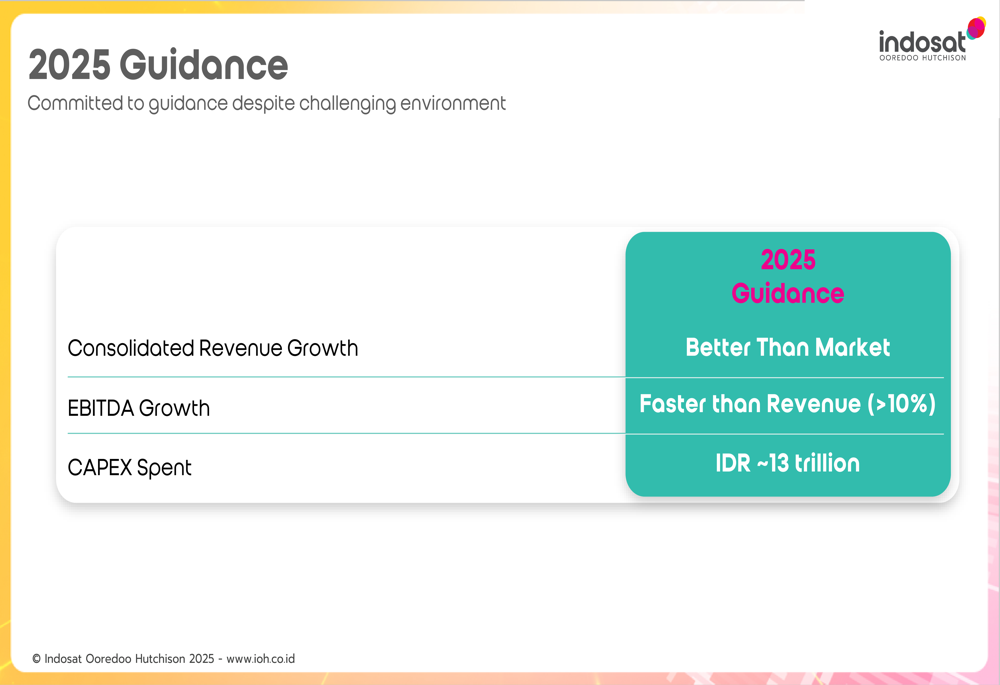

2025 Guidance and Outlook

Looking ahead, Indosat provided guidance for 2025, expecting consolidated revenue growth to outperform the market and EBITDA growth to exceed 10%, outpacing revenue growth. The company plans capital expenditure of approximately 13 trillion IDR for the year.

The following slide presents the company’s 2025 guidance:

Indosat’s balance sheet remains strong, with the net debt to EBITDA ratio improving to 0.36x, down from 0.40x in the previous quarter. This financial stability provides the company with flexibility to invest in strategic initiatives while maintaining profitability.

CEO Vikram Sinha emphasized the company’s focus on ensuring "EBITDA grows faster than revenue," highlighting Indosat’s strategic priorities of cost efficiency and profitability improvement. The company remains cautiously optimistic about ARPU growth potential in the Indonesian market, which continues to be under-indexed compared to regional peers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.