TSMC earnings; Oracle analyst meeting; Gold’s new high - what’s moving markets

Introduction & Market Context

Industrial Logistics Properties Trust (NASDAQ:ILPT) released its second quarter 2025 financial results on July 29, showing modest improvement in key metrics while taking strategic steps to address its debt structure. The company’s stock closed at $5.44 on the reporting day and gained 1.97% in after-hours trading, continuing a recovery trend after hitting a 52-week low of $2.45 earlier in the year.

The industrial REIT, which owns 411 properties spanning approximately 59.9 million rentable square feet across 39 states, has been working to stabilize its financial position while maintaining strong occupancy and tenant retention in a competitive industrial real estate market.

Quarterly Performance Highlights

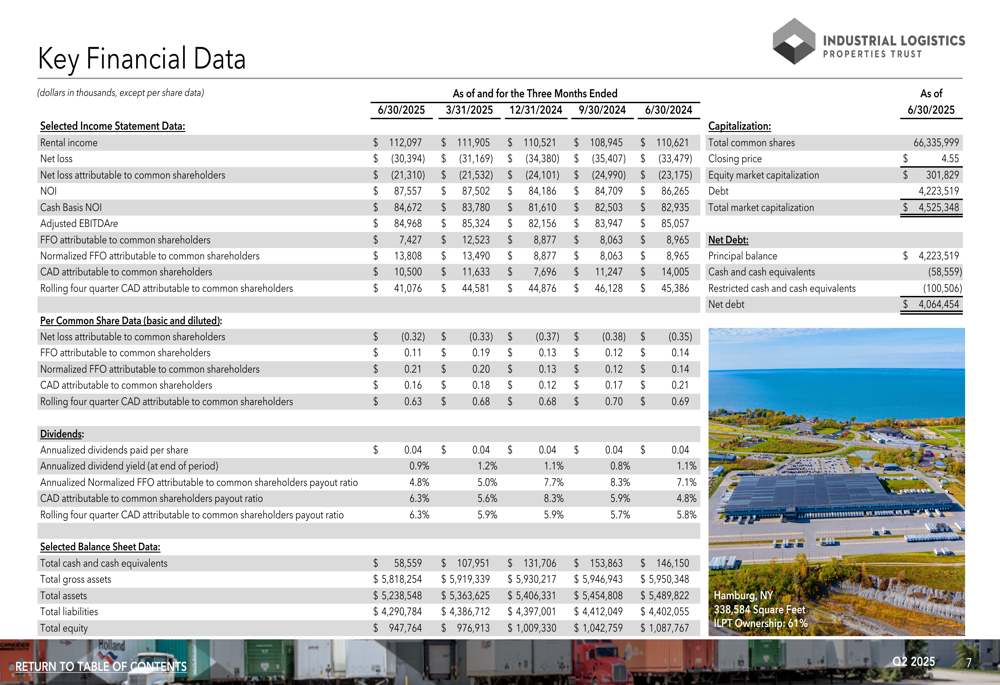

ILPT reported a net loss attributable to common shareholders of $21.3 million, or $0.32 per diluted share, for Q2 2025, representing a slight improvement from the $0.33 per share loss reported in the previous quarter. Normalized FFO attributable to common shareholders was $13.8 million, or $0.21 per diluted share, exceeding the company’s guidance of $0.19-$0.21 and showing sequential improvement from $0.20 per share in Q1.

As shown in the following comprehensive financial data table, the company’s net operating income (NOI) increased by 1.5% to $87.6 million, while Adjusted EBITDAre remained relatively stable at $85.0 million:

The company demonstrated strength in its leasing activities, executing 171,000 square feet of new and renewal leases at weighted average rental rates that were 21.1% higher than prior rental rates. This positive leasing spread highlights the continued demand for industrial properties despite broader economic uncertainties.

Debt Refinancing and Dividend Increase

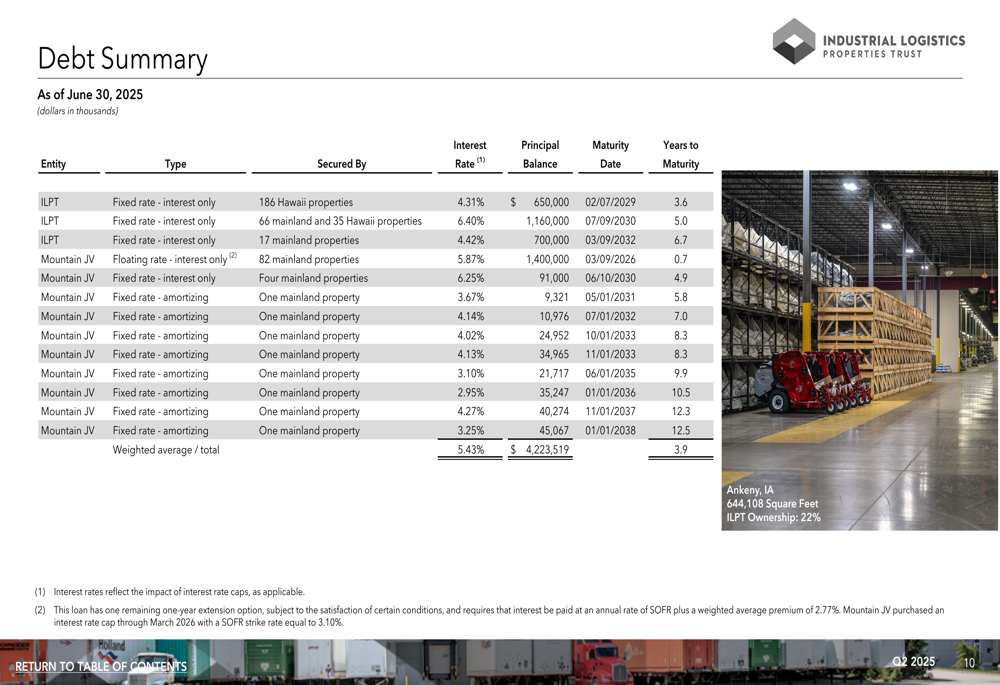

The most significant developments in the quarter were ILPT’s strategic refinancing of $1.235 billion of floating rate debt with $1.16 billion of fixed rate debt due July 2030, and the increase of its quarterly cash distribution to common shareholders from $0.01 per share to $0.05 per share.

The debt refinancing represents an important step in stabilizing the company’s capital structure by reducing exposure to interest rate fluctuations. As detailed in the following debt summary, ILPT now has a weighted average interest rate of 5.43% with a weighted average maturity of 3.9 years:

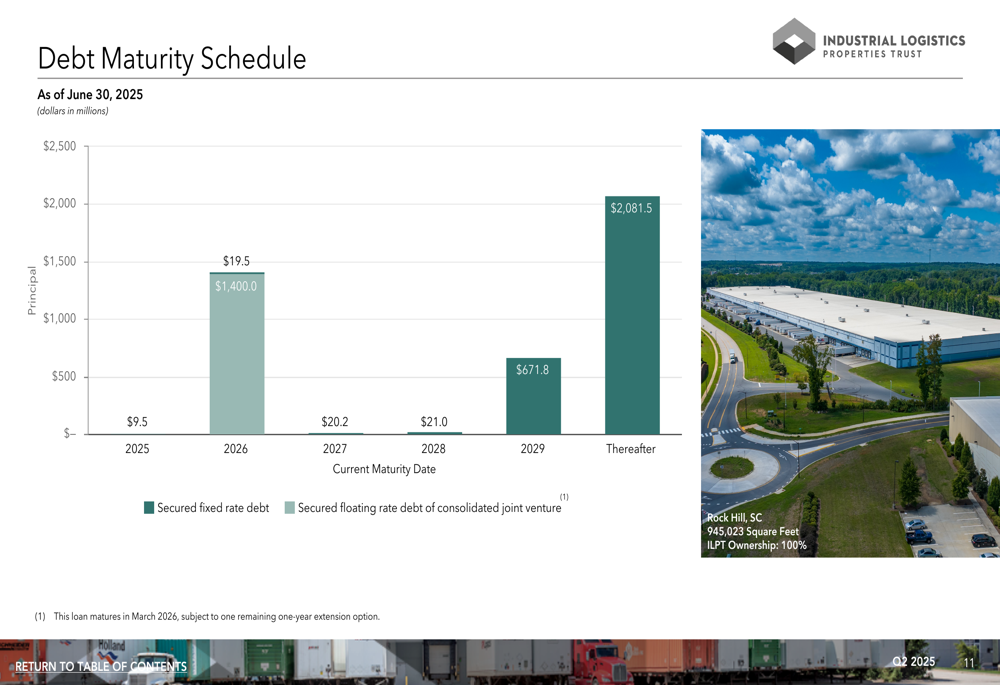

The company’s debt maturity schedule shows that the majority of its debt matures in 2026 and beyond, providing near-term stability:

The dividend increase, while modest in absolute terms, represents a significant 400% increase from the previous level and signals management’s growing confidence in the company’s financial stability and cash flow generation.

Portfolio Performance and Tenant Base

ILPT’s portfolio continues to demonstrate resilience with 94.3% of its space leased and only 2.1 million square feet (3.6% of leased area) set to expire in the next 12 months. This low near-term lease expiration exposure provides stability to the company’s revenue stream.

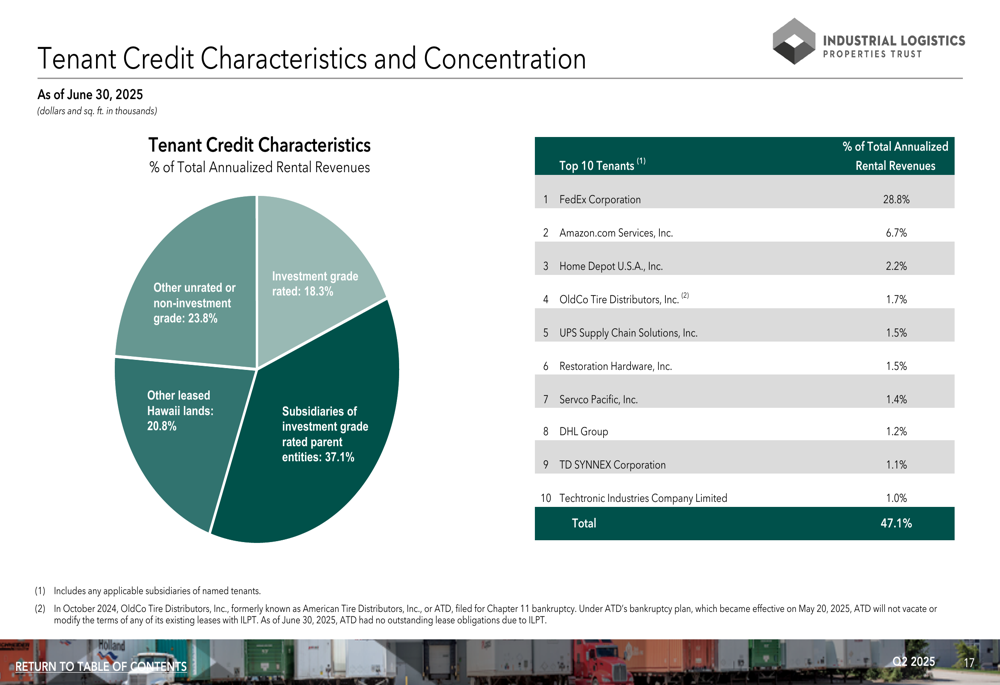

A key strength of ILPT’s portfolio is its high-quality tenant base. As illustrated in the following chart, approximately 76% of the company’s annualized rental revenues come from investment grade tenants or subsidiaries of investment grade rated parent entities:

The company’s tenant concentration is notable, with FedEx Corporation (NYSE:FDX) accounting for 28.8% of total annualized rental revenues, followed by Amazon.com (NASDAQ:AMZN) Services at 6.7%. While this concentration provides stability given the credit quality of these tenants, it also represents a potential risk should these major tenants reduce their space needs.

Financial Position and Leverage Concerns

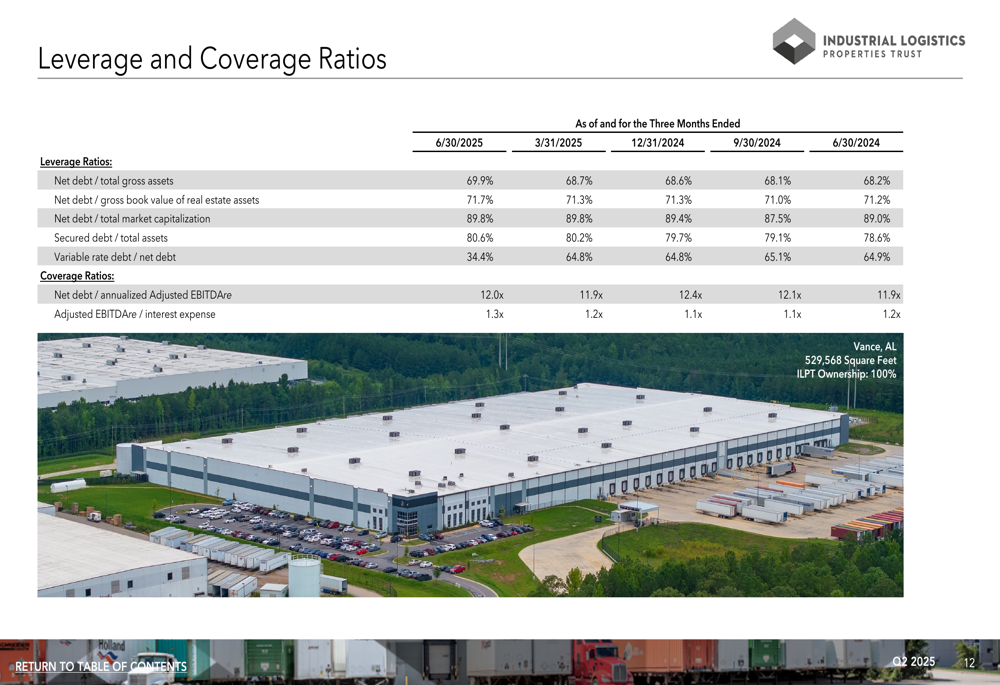

Despite operational improvements, ILPT’s leverage remains a significant concern. The company’s net debt to total gross assets ratio stands at 69.9%, while its net debt to total market capitalization is 89.8%. These high leverage metrics are well above industry averages and limit financial flexibility.

The following table illustrates the company’s leverage and coverage ratios:

Of particular concern is the interest coverage ratio (Adjusted EBITDAre / interest expense) of just 1.3x, which provides limited cushion for debt service. This thin coverage ratio underscores the importance of the company’s recent debt refinancing to stabilize interest costs.

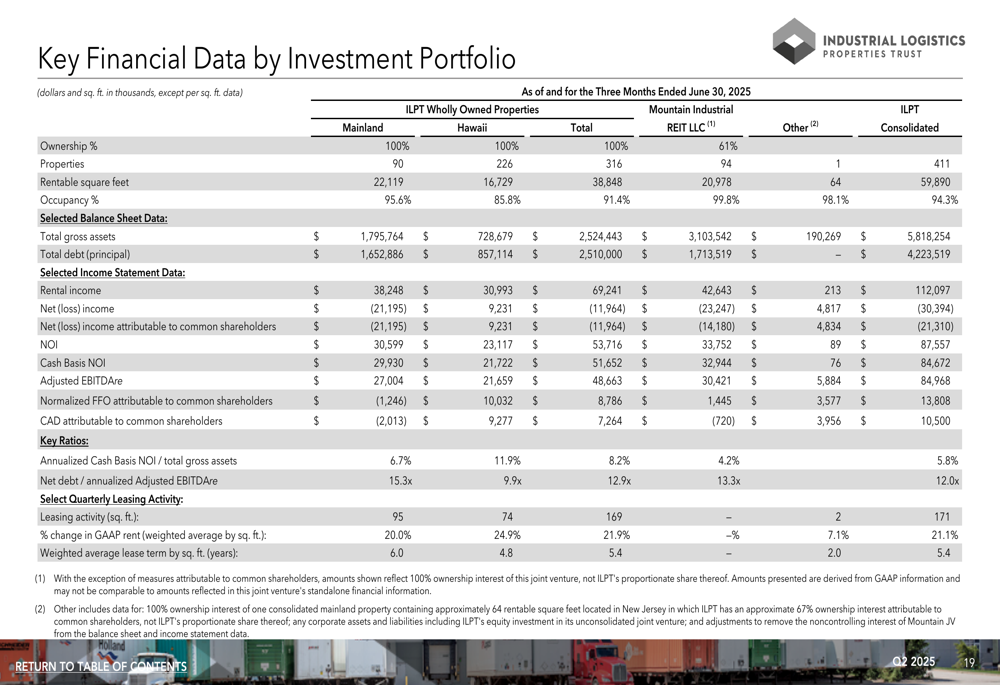

The company’s portfolio is split between wholly owned properties and joint ventures, as detailed in this breakdown of key financial data by investment portfolio:

Forward Outlook

While ILPT did not provide explicit forward guidance in its presentation, the company’s operational improvements and strategic financial moves suggest a continued focus on stabilizing its financial position while maximizing the value of its portfolio.

The increase in dividend, successful debt refinancing, and positive leasing spreads indicate management’s confidence in the company’s near-term prospects. However, the high leverage metrics and thin interest coverage ratio suggest that debt reduction should remain a priority.

In the previous quarter’s earnings call, management had indicated potential property dispositions to reduce leverage, though the current presentation does not explicitly mention completed sales. This strategy may still be under consideration as the company works to strengthen its balance sheet.

With no significant debt maturities until 2026, ILPT has time to execute its strategy, but investors will likely continue to monitor the company’s progress in addressing its leverage concerns while maintaining strong operational performance in an evolving industrial real estate market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.