Palantir to report; Trump on Nvidia chip exports - what’s moving markets

Integer Holdings Corporation (NYSE:ITGR) presented its second quarter 2025 earnings results on July 24, showcasing double-digit growth in both sales and profitability. The medical device outsourcing manufacturer raised its adjusted operating income outlook while maintaining its sales guidance for the year. The stock is currently trading at $103.28, up 1.16% from its previous close.

Quarterly Performance Highlights

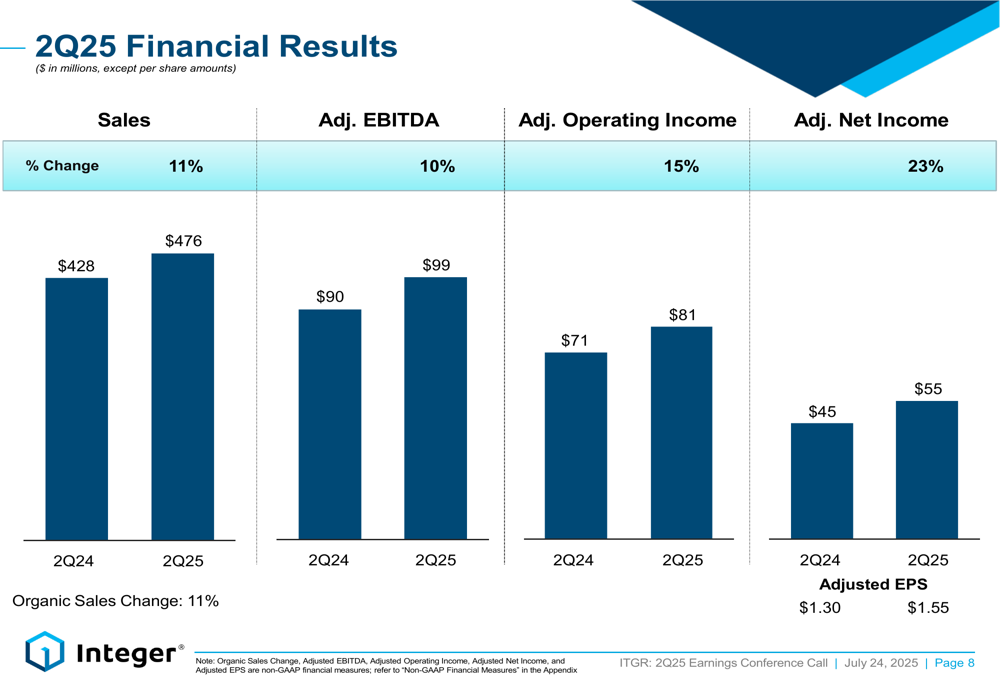

Integer delivered strong financial results in the second quarter, with sales reaching $476 million, representing an 11% increase compared to the same period last year. Both reported and organic sales growth were identical at 11%, demonstrating the company’s ability to grow its core business.

As shown in the following chart of quarterly financial performance, adjusted operating income grew even faster than sales, increasing 15% year-over-year to $81 million, while adjusted EPS rose 19% to $1.55 from $1.30 in Q2 2024:

The company’s adjusted EBITDA reached $99 million, up 10% compared to the prior year. Adjusted net income showed particularly strong growth, increasing 23% to $55 million.

Integer’s CEO Joe Dziedzic noted during the earnings call that the company "delivered strong growth in the first and second quarter with sales up 9% and EPS up 17% in the first half of 2025."

Segment Analysis

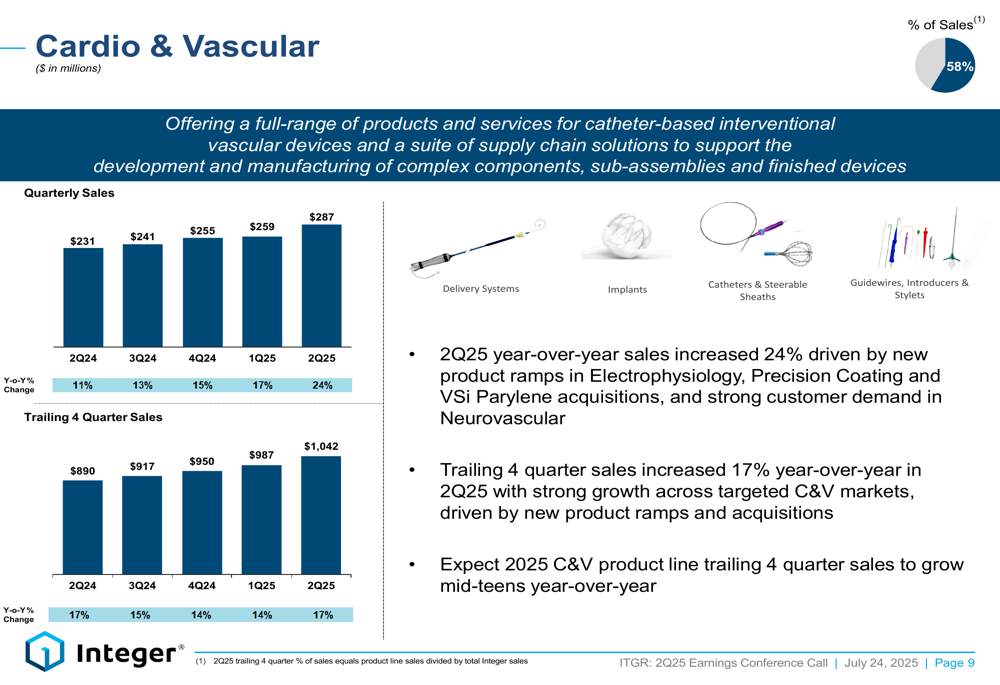

Integer’s performance was driven primarily by its Cardio & Vascular segment, which represented 58% of total sales. This segment grew 24% year-over-year to $287 million, significantly outpacing the company’s overall growth rate.

The following chart illustrates the strong performance in the Cardio & Vascular segment, which has shown consistent growth over the past several quarters:

Management attributed this robust growth to new product ramps in Electrophysiology, contributions from the Precision Coating and VSi Parylene acquisitions, and strong customer demand in the Neurovascular market. The company expects the Cardio & Vascular product line to maintain mid-teens growth for the full year 2025.

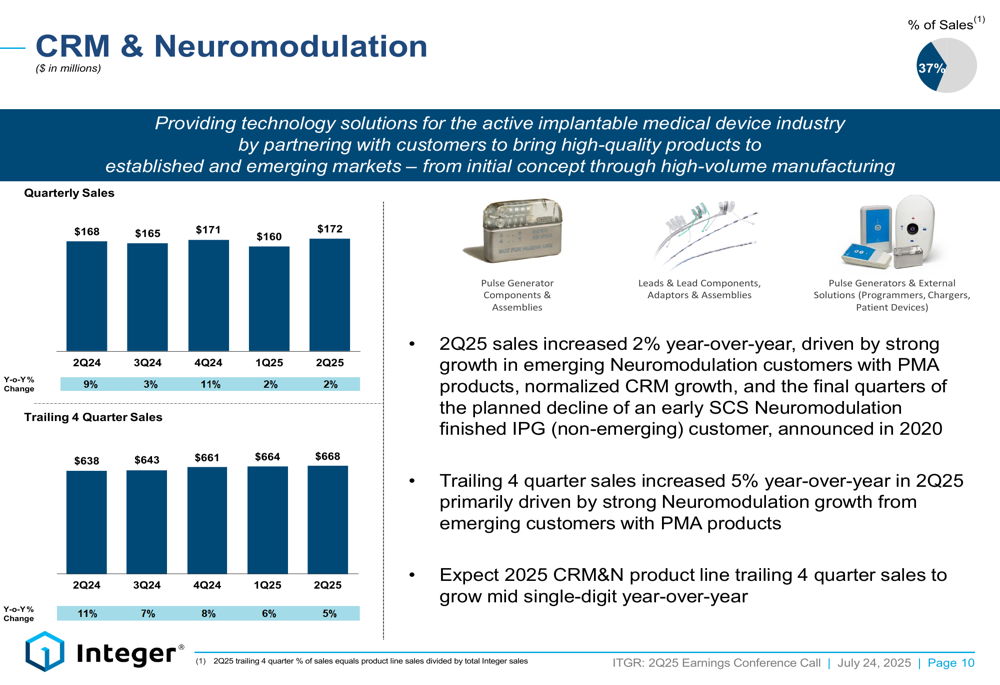

Meanwhile, the CRM & Neuromodulation segment, which accounts for 37% of sales, delivered more modest growth of 2% year-over-year, reaching $172 million in Q2:

The slower growth in this segment was partially due to the final quarters of a planned decline from an early SCS Neuromodulation finished IPG customer, as announced in 2020. However, the company highlighted strong growth from emerging Neuromodulation customers with PMA products. Integer expects this segment to achieve mid-single-digit growth for the full year.

Financial Health & Cash Flow

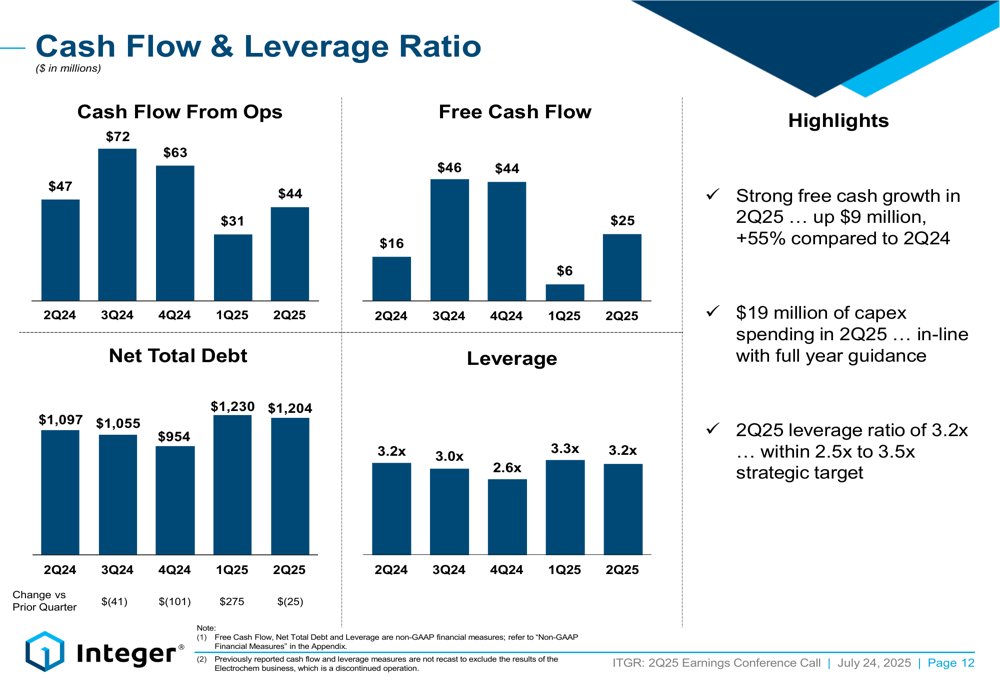

Integer demonstrated improved cash generation in the quarter, with free cash flow of $25 million representing a 55% increase compared to Q2 2024. The company maintained a healthy balance sheet with its leverage ratio at 3.2x, well within its strategic target range of 2.5x to 3.5x.

The following chart shows Integer’s cash flow and leverage trends over the past five quarters:

Capital expenditures for the quarter were $19 million, in line with full-year guidance. For the full year 2025, Integer expects capital expenditures of $110-120 million, compared to $105 million in 2024, supporting continued growth initiatives.

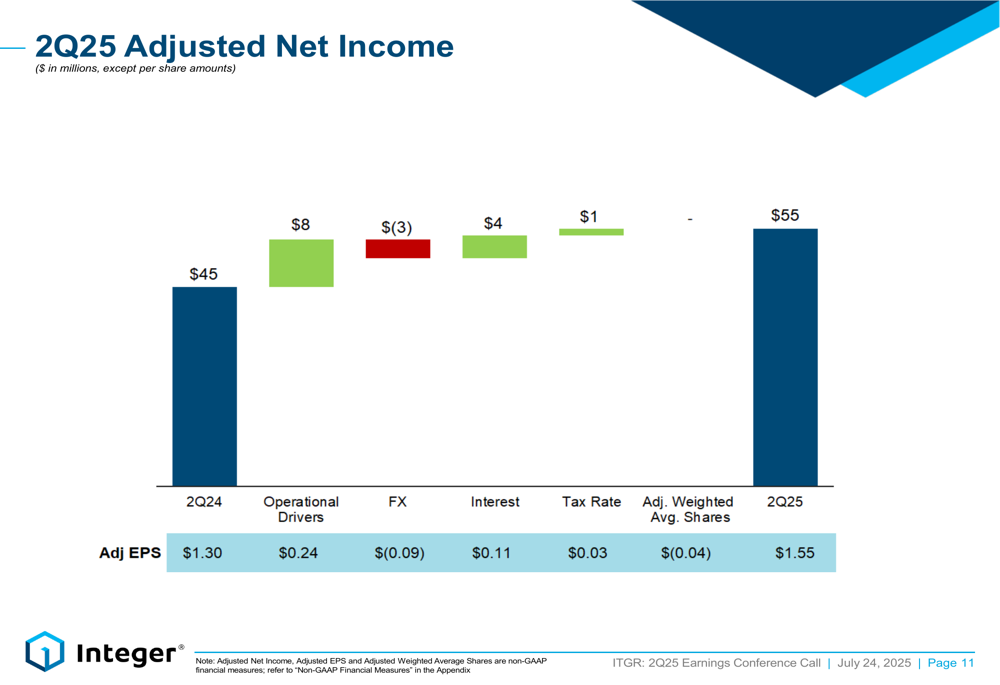

The company’s adjusted net income bridge provides insight into the key factors driving the 23% increase in profitability:

Operational improvements contributed $8 million to adjusted net income, while lower interest expenses added $4 million, demonstrating the benefits of the company’s debt management strategy. These gains were partially offset by a $3 million negative impact from foreign exchange.

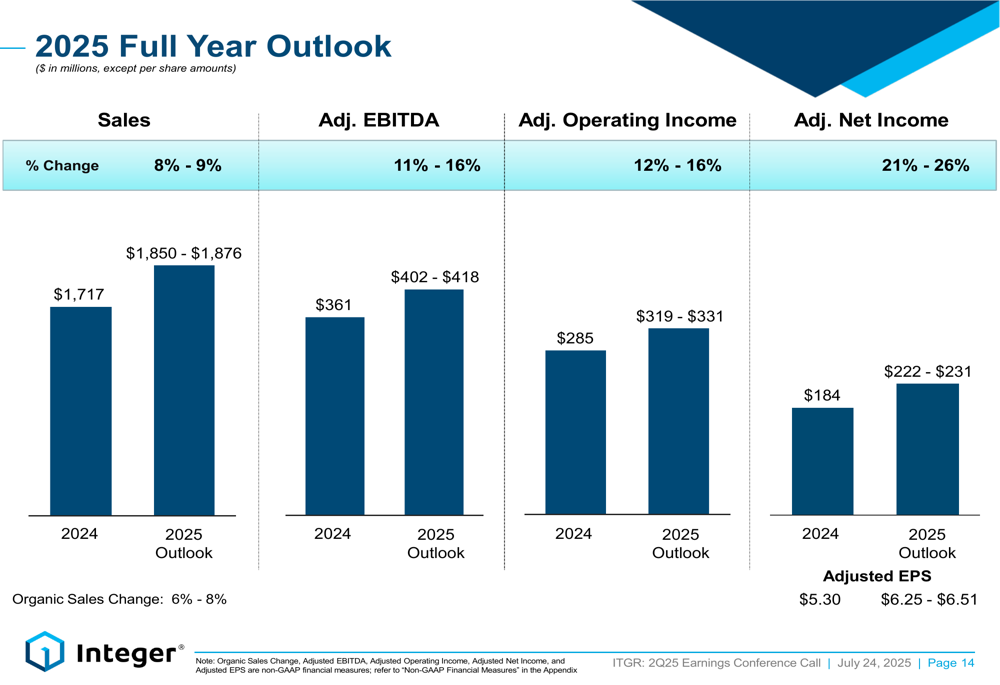

2025 Outlook & Guidance

Integer raised its adjusted operating income outlook by $2 million at the midpoint while maintaining its sales guidance. The company now projects full-year 2025 sales between $1,850 million and $1,876 million, representing 8-9% growth over 2024.

The following chart details Integer’s full-year 2025 outlook:

Adjusted operating income is now expected to be between $319 million and $331 million, reflecting 12-16% growth. Adjusted EPS guidance was raised to $6.25-$6.51, representing 18-23% growth compared to 2024.

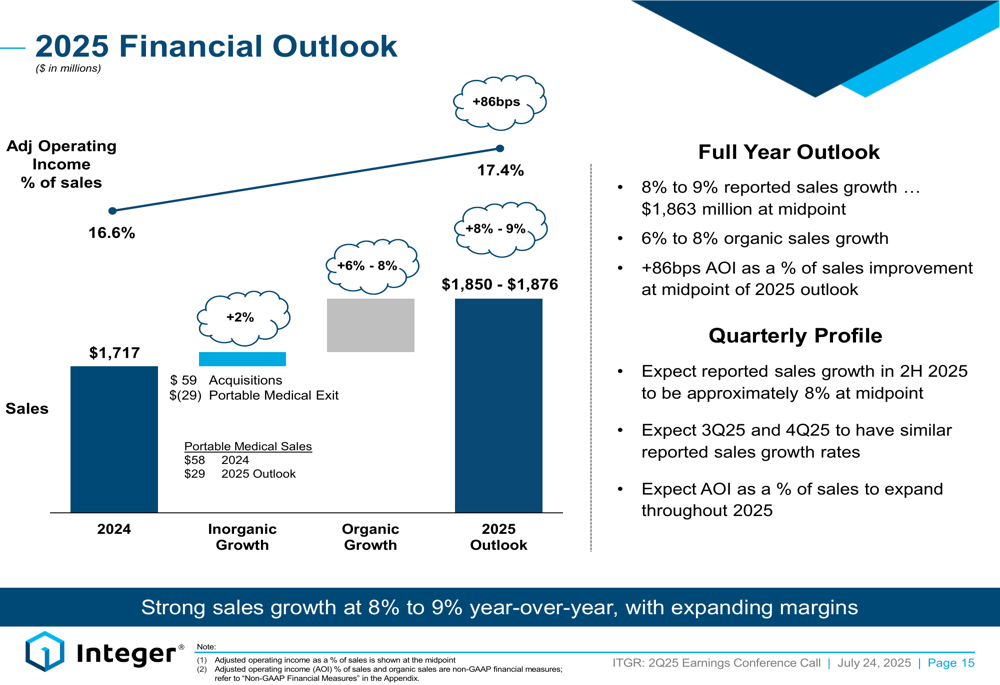

The company also provided a more detailed breakdown of its 2025 financial outlook:

Integer expects adjusted operating income as a percentage of sales to expand by 86 basis points at the midpoint of guidance, reaching 17.4% compared to 16.6% in 2024. Management indicated that they expect this margin expansion to continue throughout 2025, with similar reported sales growth rates in both Q3 and Q4.

Strategic Positioning

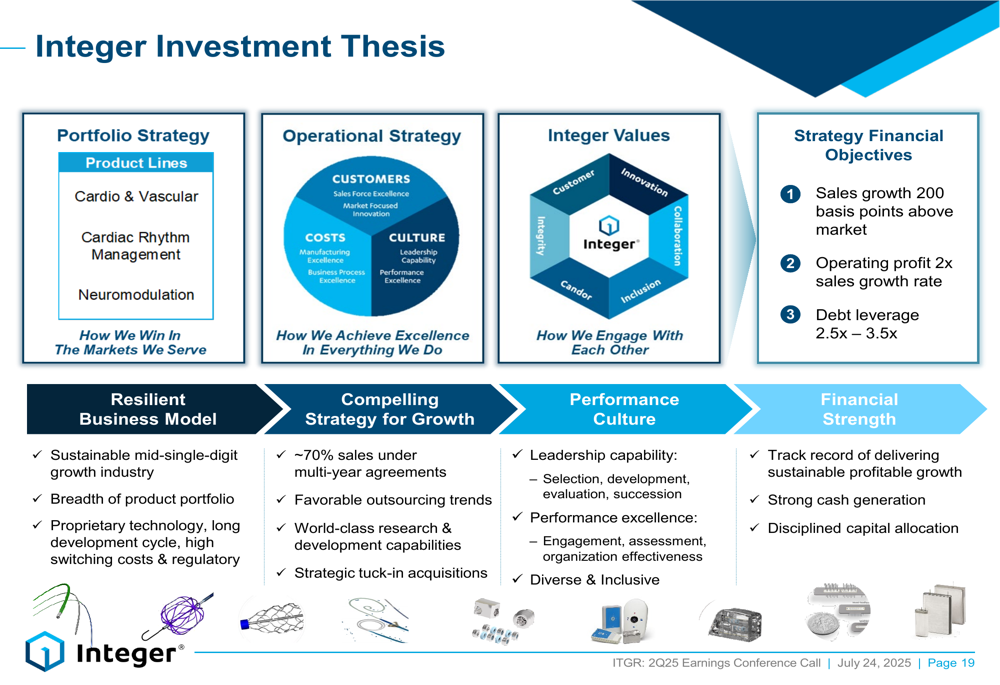

Integer’s investment thesis centers on delivering sustained above-market growth while expanding margins. The company aims to grow sales 200 basis points above market while increasing operating profit at twice the rate of sales growth.

The following illustration outlines Integer’s strategic positioning and investment thesis:

Management highlighted that approximately 70% of sales are under multi-year agreements, providing strong visibility into future demand. The company’s $700 million order backlog further supports this visibility.

Integer’s strategy leverages its broad product portfolio, proprietary technologies, and world-class R&D capabilities. The company operates in a favorable outsourcing environment within the medical device industry, which is experiencing sustainable mid-single-digit growth.

COO Payman Khales commented during the earnings call, "Our guidance midpoint has not changed. We just narrowed the range, given the good visibility that we have for the year."

With its strong Q2 results and raised profit outlook, Integer appears well-positioned to continue executing its strategy of above-market growth and margin expansion through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.