Palantir a high-risk investment with ’a one-of-a-kind growth and margin model’

Introduction & Market Context

Intel Corporation (NASDAQ:INTC) presented its first-quarter 2025 earnings results on April 24, 2025, reporting revenue that exceeded January guidance despite ongoing challenges in the competitive landscape. The company’s stock reacted negatively to the results, dropping 6.75% in after-hours trading despite the earnings beat, as investors focused on the disappointing Q2 outlook.

Led by CEO Lip-Bu Tan and CFO David Zinsner, Intel highlighted its efforts to refocus on core products, refine its AI strategy, build trust with foundry customers, and strengthen its balance sheet amid continued transformation efforts.

Q1 Financial Performance Highlights

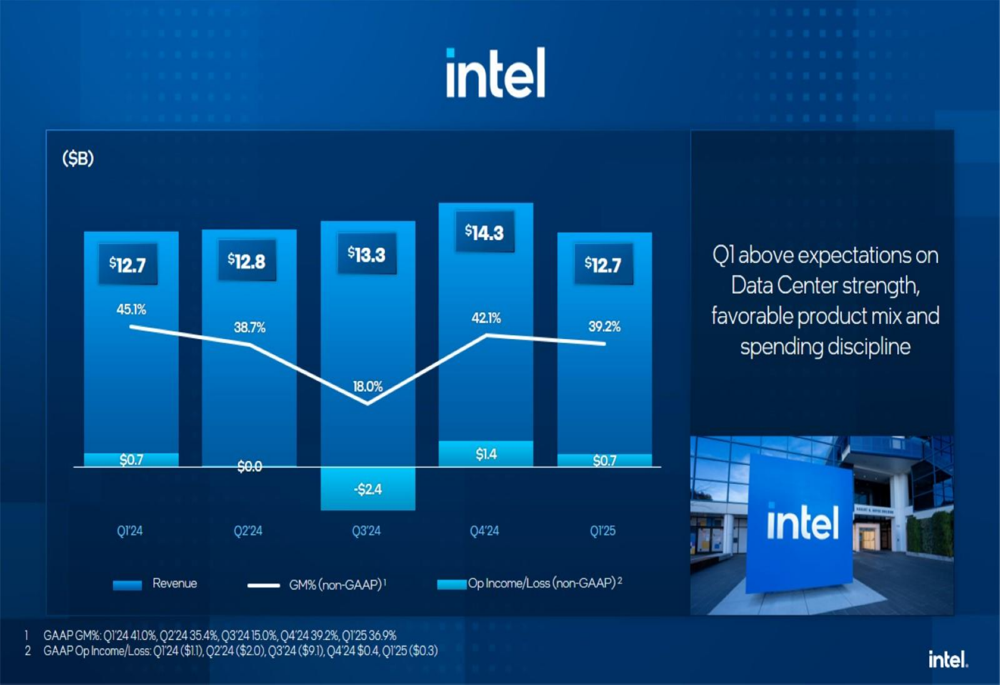

Intel reported Q1 2025 revenue of $12.7 billion, which was down 0.4% year-over-year but exceeded January guidance by $0.5 billion. The company’s non-GAAP gross margin came in at 39.2%, down 5.9 percentage points year-over-year but 3.2 percentage points above outlook. Earnings per share reached $0.13, down $0.05 year-over-year but significantly above the January outlook.

As shown in the following financial highlights chart:

The company attributed its better-than-expected Q1 performance to strength in the data center segment, favorable product mix, and disciplined spending. This represents a continuation of the sequential improvement seen in Q4 2024, when Intel also exceeded analyst expectations.

The following chart illustrates Intel’s revenue and profit trends over the past five quarters:

Segment Analysis

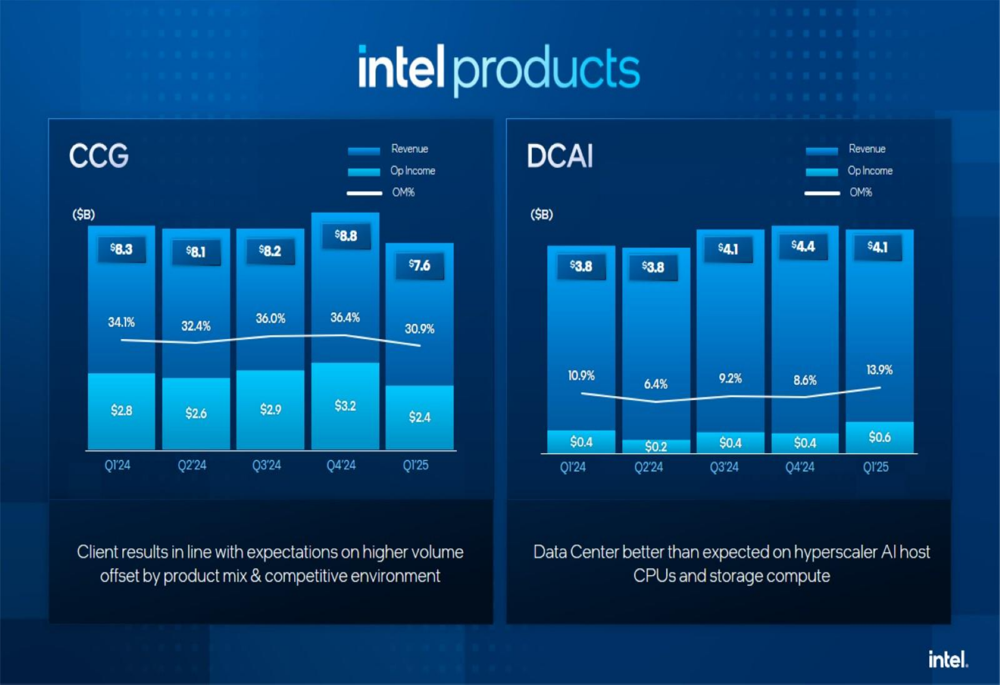

Intel’s performance varied significantly across its business segments, with data center showing strength while client computing faced challenges.

The Client Computing Group (CCG) posted revenue of $7.6 billion, down from $8.3 billion in Q1 2024, with operating margin declining to 30.9% from 34.1% a year earlier. Intel noted that client results were in line with expectations, with higher volume offset by product mix and competitive pressures.

In contrast, the Data Center and AI (DCAI) segment showed improvement, with revenue increasing to $4.1 billion from $3.8 billion in Q1 2024. Operating margin for this segment rose to 13.9% from 10.9% a year earlier. The company attributed this better-than-expected performance to hyperscaler AI host CPUs and storage compute solutions.

The following chart details the performance of these key segments:

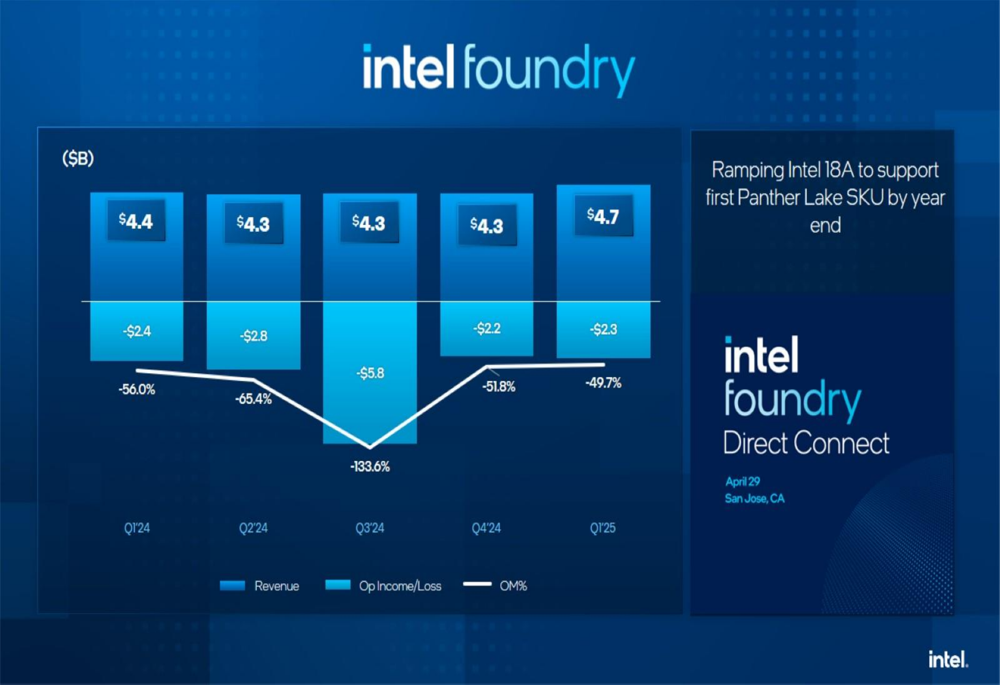

Intel Foundry continued to operate at a significant loss, though with slightly improving margins. The segment reported revenue of $4.7 billion, up from $4.4 billion in Q1 2024, with an operating loss of $2.3 billion, marginally better than the $2.4 billion loss a year earlier. The operating margin improved to -49.7% from -56.0%.

The company’s "All Other" segment, which includes Mobileye and Altera, showed positive momentum with revenue of $943 million and operating income of $103 million, representing an operating margin of 10.9%. This marks a significant improvement from the $170 million operating loss and -26.4% margin in Q1 2024.

Strategic Initiatives

Intel outlined several key strategic initiatives aimed at improving execution and driving innovation. The company is focusing on refining its core product franchise, particularly in client and data center computing ecosystems, while also refining its AI strategy to focus on emerging areas of disruption.

The presentation highlighted Intel’s efforts to build trust with foundry customers by delivering on time across power, performance, area, and cost metrics. The company is ramping up its 18A technology to support the first Panther Lake SKU by year-end, a critical milestone for its foundry business.

Intel also emphasized its commitment to strengthening its balance sheet through prudent capital management and monetization of non-core assets. This includes the planned majority stake sale of Altera to Silver Lake, which was mentioned in the presentation.

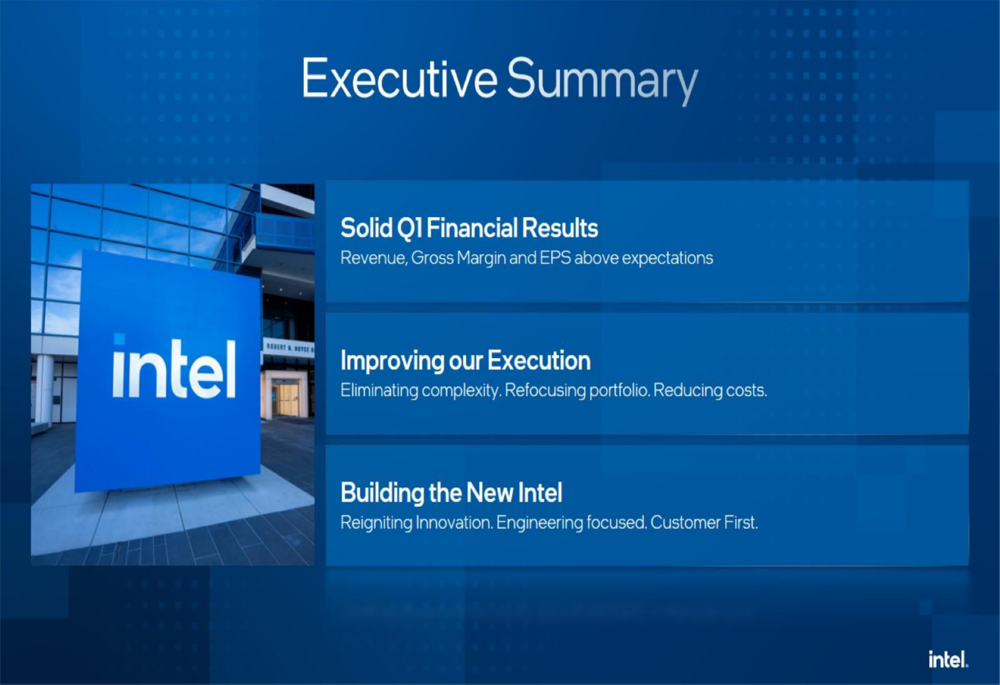

As shown in the executive summary slide:

Q2 2025 Outlook and Forward-Looking Statements

Intel’s outlook for Q2 2025 points to continued challenges, with projected revenue of $11.2-12.4 billion, representing a $1.0 billion decline year-over-year. The company expects a non-GAAP gross margin of 36.5%, down 2.2 percentage points year-over-year, and EPS of $0.00, down $0.02 from Q2 2024.

The following slide details the Q2 outlook:

This cautious guidance likely contributed to the negative stock reaction following the earnings release. While Intel exceeded expectations for Q1, investors appear concerned about the company’s ability to maintain momentum in an increasingly competitive environment.

Intel continues to face significant challenges in its foundry business, which remains unprofitable, and in the client computing segment, where competition is intensifying. However, the strength in the data center segment and the company’s strategic initiatives to refocus on core products and refine its AI strategy provide some positive indicators for the future.

As Intel works to execute its transformation strategy, investors will be closely watching whether the company can deliver on its commitments to improve execution, reignite innovation, and strengthen its financial position in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.