Palantir shares slip by 7% despite posting record revenue in third quarter

International Paper (NYSE:IP) shares plunged over 12% following its third-quarter 2025 earnings release on October 30, as the packaging giant reported mixed results that highlighted progress in its transformation strategy but fell significantly short of analyst expectations.

Financial Performance Highlights

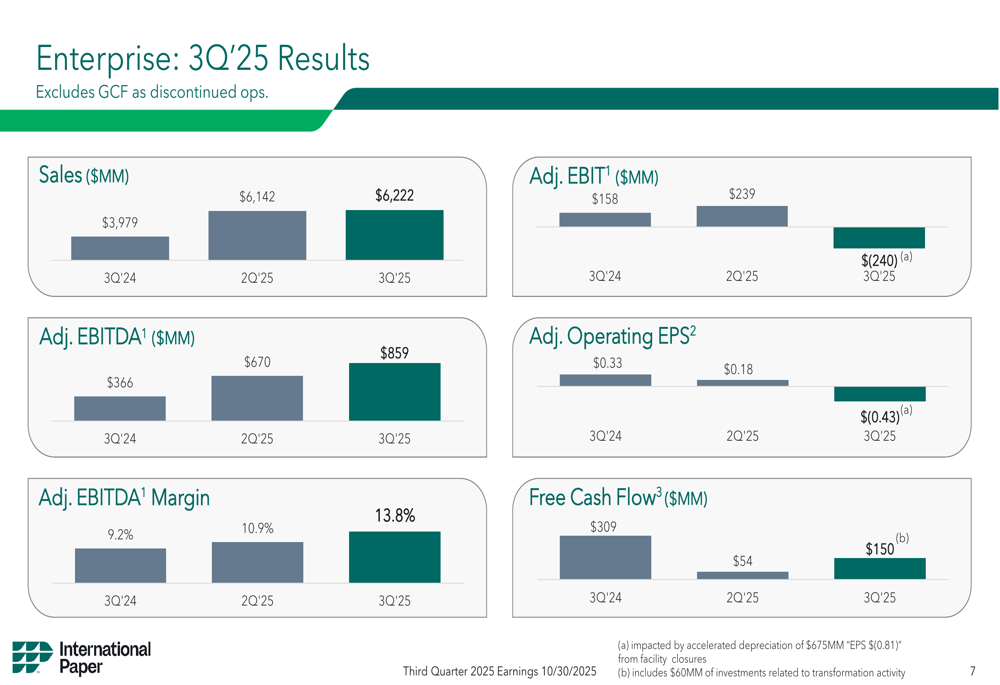

The company reported third-quarter sales of $6.22 billion, slightly up from $6.14 billion in the second quarter but missing analyst forecasts of $6.46 billion. While Adjusted EBITDA improved substantially to $859 million (up from $670 million in Q2 and $366 million in Q3 2024), the company posted a disappointing Adjusted Operating EPS loss of $0.43, compared to a profit of $0.18 in the previous quarter and well below analyst expectations of $0.55 profit.

The significant earnings miss triggered the steep stock decline, with shares falling to $42.50 in pre-market trading, approaching the 52-week low of $38.52.

As shown in the following enterprise results summary:

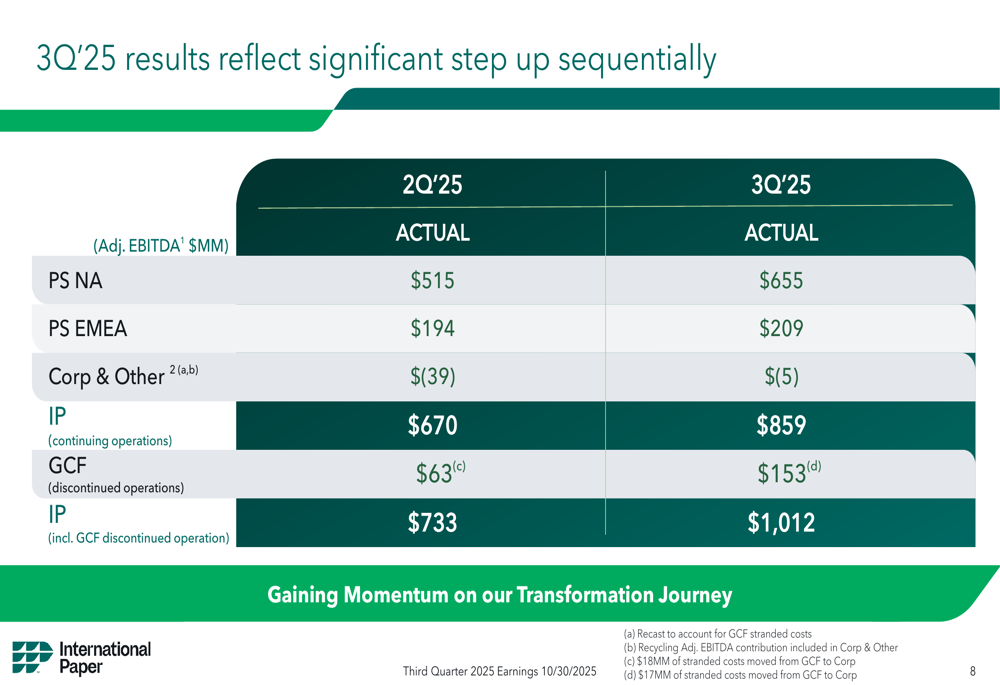

Despite the EPS disappointment, International Paper highlighted sequential improvements in its core packaging solutions businesses, with a 28% step-up in Adjusted EBITDA and improved margins. Free cash flow increased to $150 million from $54 million in the previous quarter.

The segment breakdown reveals the source of improvement came primarily from the North American packaging business:

Regional Performance Analysis

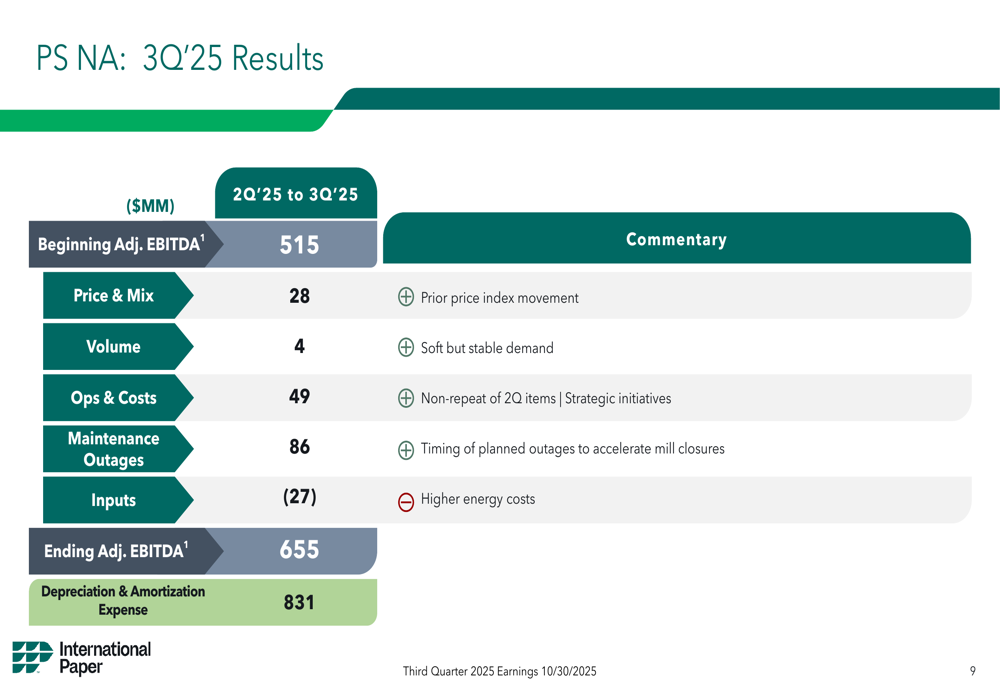

The North American packaging business delivered strong sequential improvement, with Adjusted EBITDA rising to $655 million from $515 million in Q2, driven by better pricing, operations, and cost management. The Adjusted EBITDA margin for this segment reached an impressive 17.5%.

The following bridge analysis illustrates the key drivers behind North America’s performance:

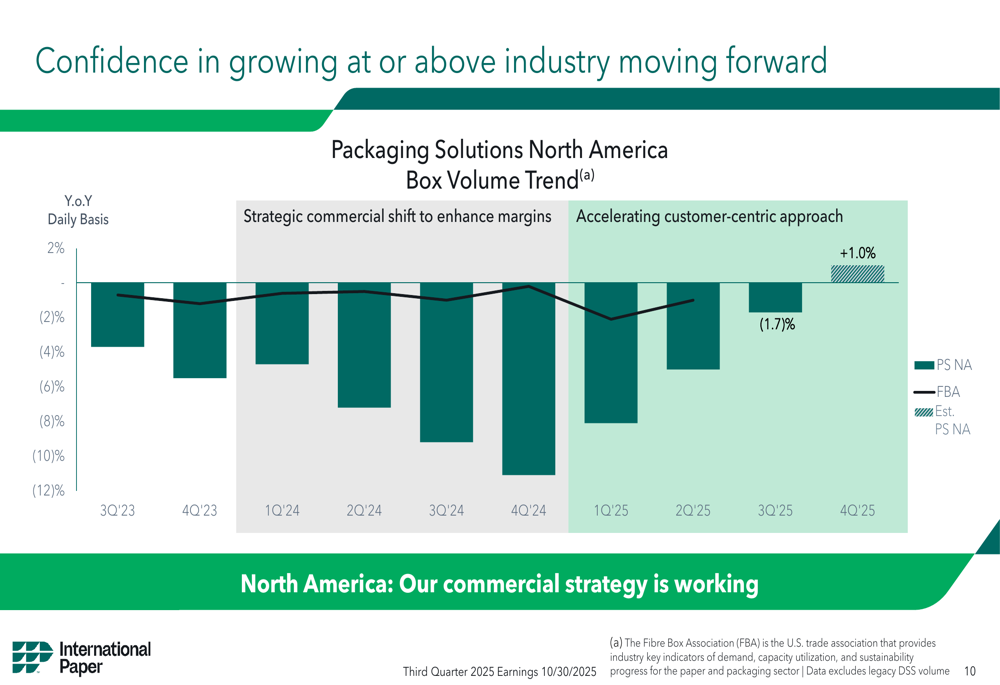

The company noted that its box volume trends in North America have shown improvement, with strategic customer wins resulting in year-over-year growth in September:

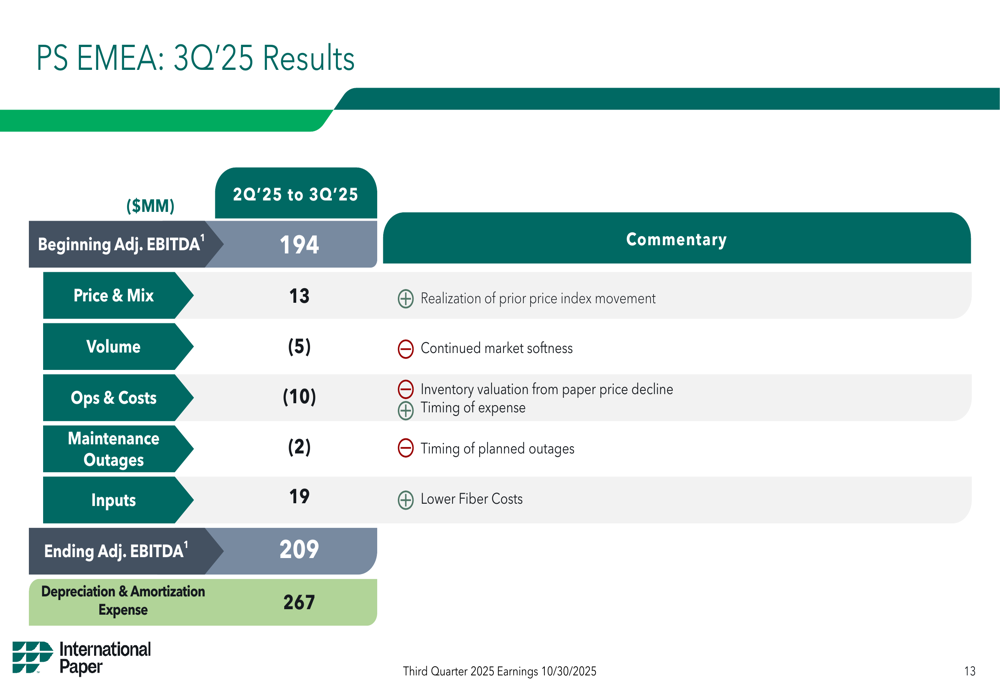

Meanwhile, the EMEA (Europe, Middle East, and Africa) region showed more modest improvement, with Adjusted EBITDA increasing to $209 million from $194 million in Q2. The company acknowledged persistent market softness and paper oversupply issues in Europe that are expected to continue until 2027.

As illustrated in the EMEA results bridge:

Strategic Transformation Progress

CEO Andy Silvernail emphasized the company’s transformation progress during the earnings call, stating, "We are making significant, measurable progress on our transformation." The company’s strategy centers around focusing on the right geographies, customers, and products while implementing a disciplined 80/20 approach to business segmentation.

The company’s strategic framework is outlined as follows:

International Paper reported meaningful progress against its planned strategic initiatives, particularly in commercial improvements and cost reduction:

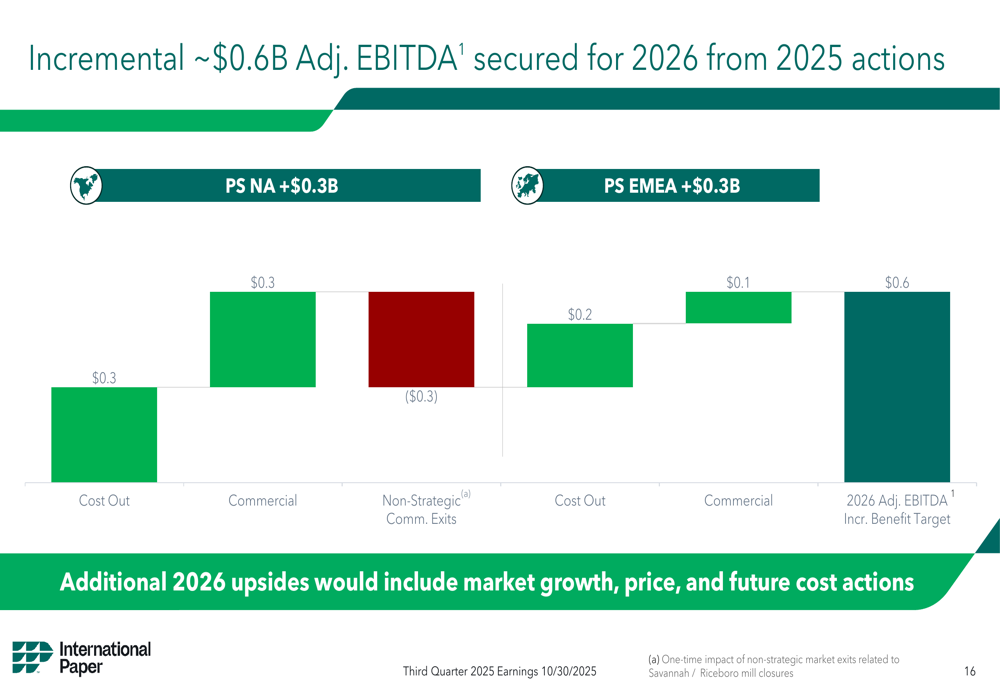

For 2026, the company has secured incremental EBITDA benefits from actions taken in 2025:

Forward Outlook

Despite the quarterly earnings miss, International Paper maintained a positive long-term outlook while adjusting near-term expectations. The company updated its 2025 targets to approximately $24 billion in net sales and $3 billion in Adjusted EBITDA, while projecting more substantial improvements by 2027.

The updated financial targets are summarized below:

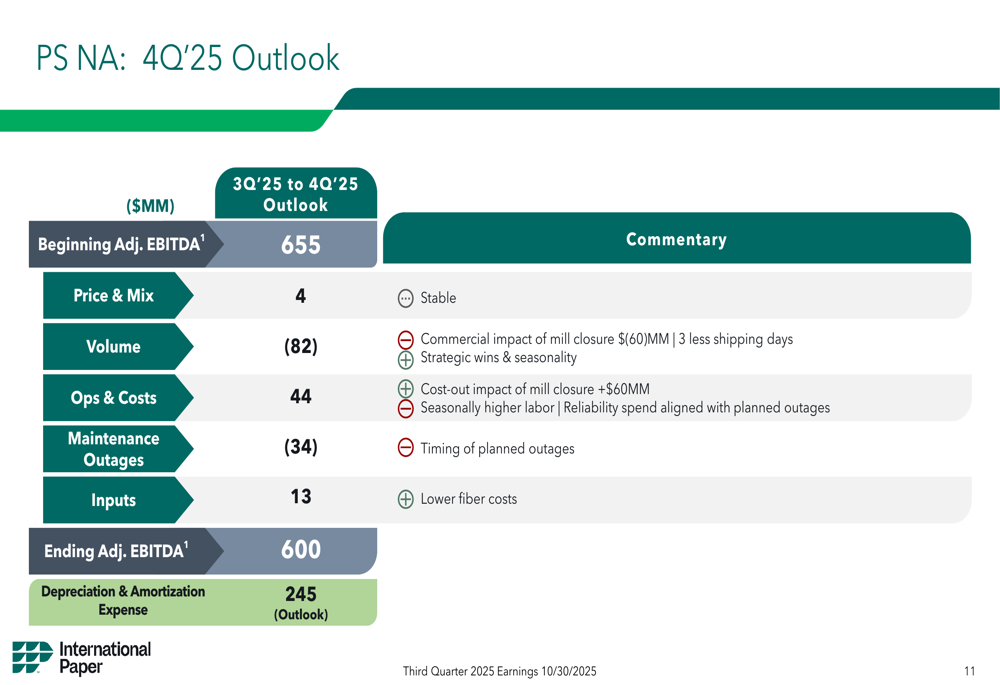

For the fourth quarter of 2025, the company expects North American Adjusted EBITDA to decrease to approximately $600 million, primarily due to volume declines:

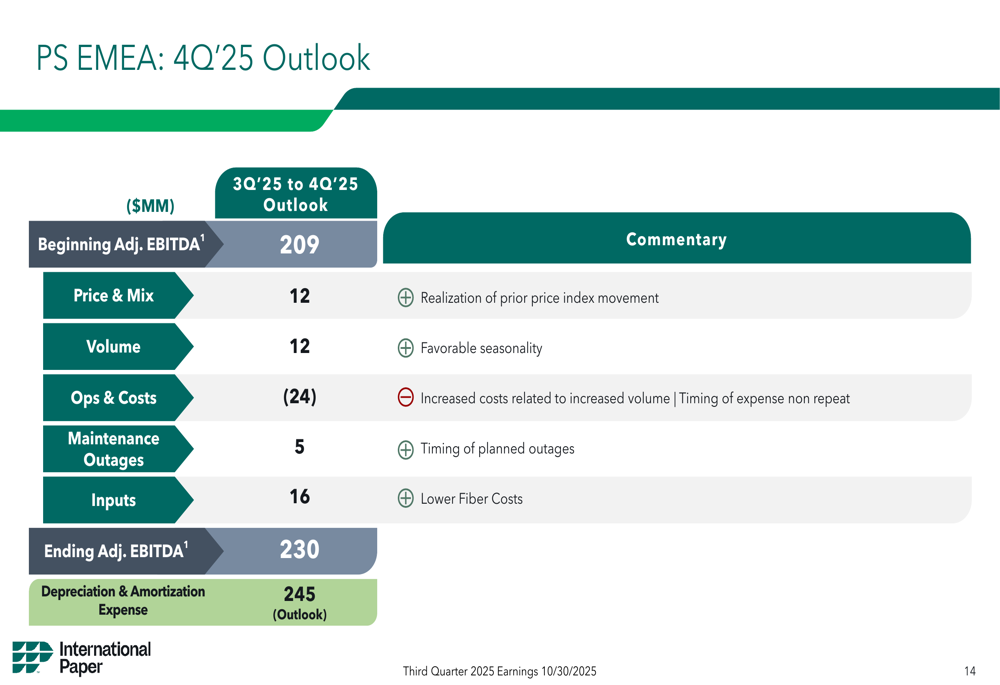

Meanwhile, EMEA is projected to see modest improvement to $230 million in Q4:

Balancing Transformation and Market Challenges

International Paper’s Q3 2025 results present a complex picture of a company making progress on its strategic transformation while facing significant market headwinds and struggling to meet investor expectations. The substantial improvement in EBITDA demonstrates operational progress, but the disappointing EPS figure raises questions about the company’s ability to translate operational improvements into bottom-line results.

The company’s focus on what it can control—including cost reduction, strategic customer targeting, and operational efficiency—appears to be yielding results at the EBITDA level. However, investors seem concerned about the pace and ultimate profitability of the transformation, as reflected in the sharp stock decline following the earnings release.

As International Paper continues its journey toward becoming a more focused packaging solutions provider—including the announced sale of its Global Cellulose Fibers and Bag businesses—investors will be watching closely to see if the company can overcome market softness and translate its strategic initiatives into consistent earnings growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.