TSX up after index logs fresh record high close

Iron Mountain Incorporated (NYSE:IRM) reported record second-quarter results on August 6, 2025, showcasing strong performance across all business segments and prompting management to raise full-year guidance. The data storage and information management company continues to execute its "Matterhorn Strategy," focusing on accelerating growth through strategic business segments.

Quarterly Performance Highlights

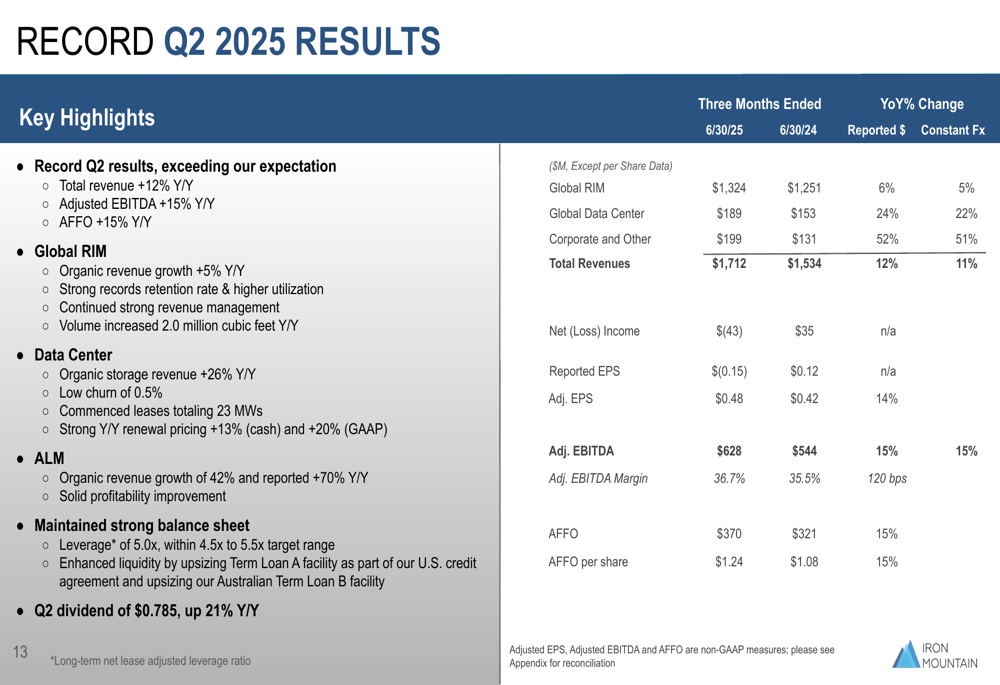

Iron Mountain delivered impressive financial results for Q2 2025, with total revenue reaching $1,712 million, a 12% increase year-over-year (11% in constant currency). Adjusted EBITDA rose 15% to $628 million, while Adjusted Funds From Operations (AFFO) grew 15% to $370 million compared to Q2 2024.

As shown in the following chart detailing the company’s Q2 2025 performance:

The company’s Global Records and Information Management (RIM) segment, which includes both physical records storage and digital solutions, grew 6% year-over-year with 5% organic revenue growth. Storage volume increased by 2.0 million cubic feet during the quarter, demonstrating continued demand for physical storage despite the digital transformation trend.

The Data Center business showed particularly strong momentum, with revenue growth of 24% year-over-year and organic storage revenue up 26%. The segment maintained an exceptionally low churn rate of 0.5% and commenced leases totaling 23 megawatts during the quarter.

Asset Lifecycle Management (ALM) emerged as the fastest-growing segment, with revenue surging 52% year-over-year and organic growth of 42%, reflecting strong demand for IT asset disposition services across both enterprise and data center markets.

Long-Term Growth Trajectory

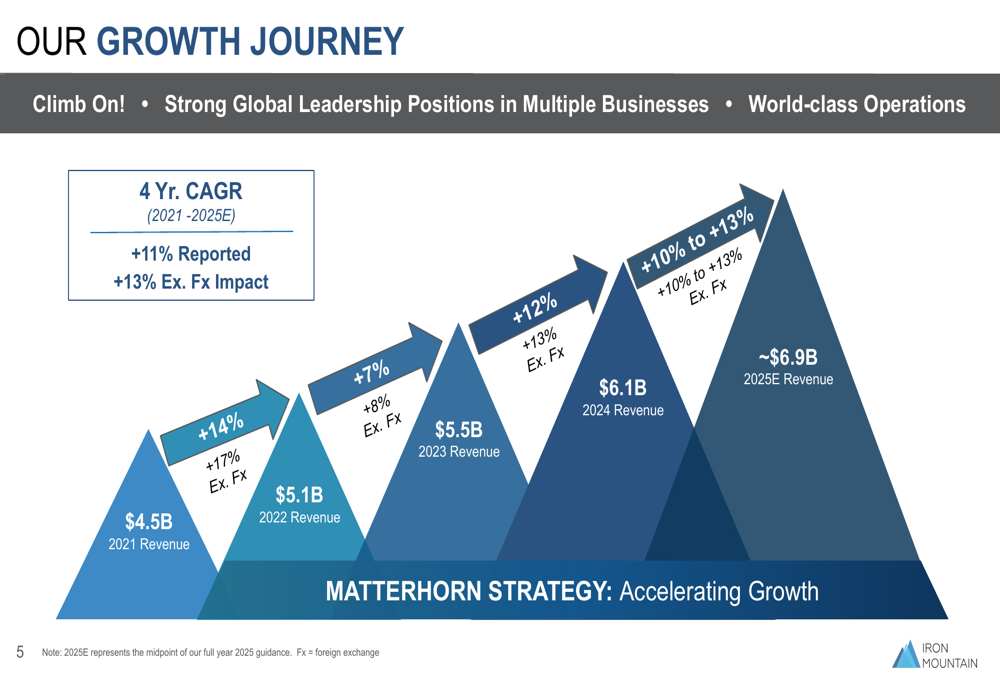

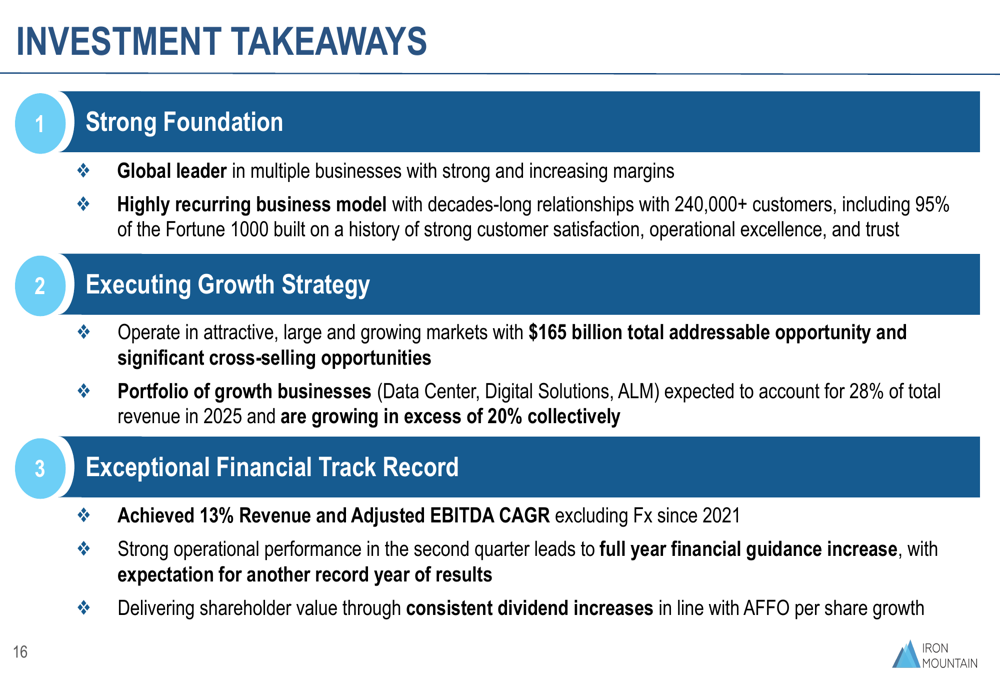

Iron Mountain has demonstrated consistent growth over recent years, with revenue expanding from $4.5 billion in 2021 to an expected $6.9 billion in 2025, representing an 11% compound annual growth rate (CAGR) or 13% excluding foreign exchange impacts.

The company’s growth journey is illustrated in this chart:

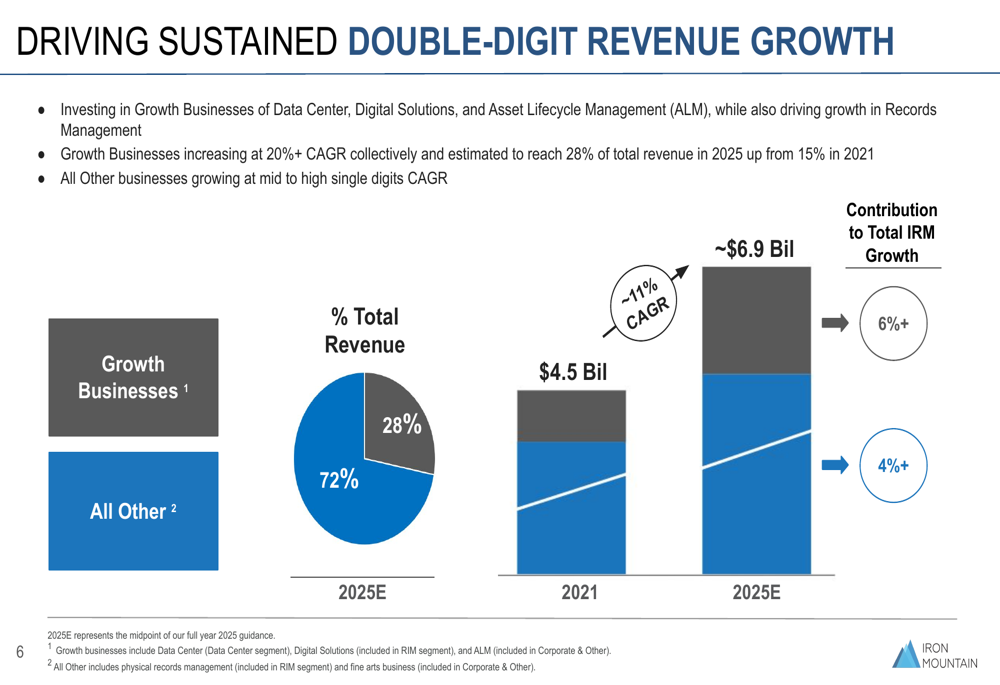

This sustained performance is driven by Iron Mountain’s strategic focus on high-growth business segments. The company’s growth businesses—Data Center, Digital Solutions, and Asset Lifecycle Management—are collectively growing at more than 20% annually and are expected to represent 28% of total revenue in 2025, up from 15% in 2021.

The following chart shows the contribution of these growth businesses to overall revenue:

Strategic Growth Initiatives

Iron Mountain’s Data Center business is positioned for continued expansion, with nearly 30% revenue growth expected in 2025 and at least 25% growth projected for 2026. The company operates 30 data centers globally and maintains a robust development pipeline.

The Data Center portfolio is expected to nearly triple in capacity to approximately 1.3 gigawatts, with 450 megawatts currently operating at 96% occupancy, 202 megawatts under construction (60% pre-leased), and 628 megawatts held for future development.

In the Asset Lifecycle Management segment, Iron Mountain has established itself as a global leader in a highly fragmented $30 billion market. The ALM business is expected to generate approximately $575 million in revenue in 2025, with the enterprise segment accounting for about 60% of ALM revenue and data center decommissioning representing the remaining 40%.

The company’s traditional Records and Information Management business continues to provide a stable foundation, with 35+ consecutive years of organic revenue growth and record storage volume of over 725 million cubic feet. This segment is expected to generate approximately $5.3 billion in revenue in 2025 with strong adjusted EBITDA margins of around 45%.

Revised 2025 Outlook

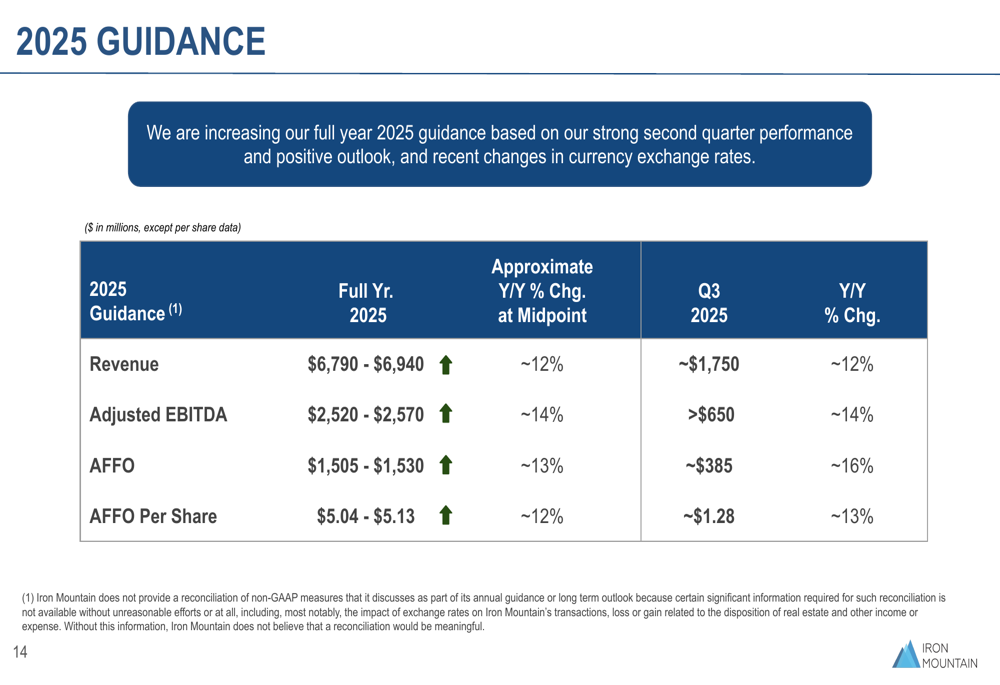

Based on strong first-half performance, Iron Mountain has raised its full-year 2025 guidance across all key metrics. The company now expects:

For the third quarter of 2025, Iron Mountain projects revenue of approximately $1,750 million (12% year-over-year growth), adjusted EBITDA exceeding $650 million (14% growth), and AFFO of around $385 million (16% growth).

The company maintains a target leverage ratio of 4.5x to 5.5x, currently at 5.0x, and remains committed to growing its dividend in line with AFFO per share growth. The Q2 2025 dividend was $0.785 per share, representing a 21% increase year-over-year.

Investment Perspective

Iron Mountain presents several compelling investment attributes, as highlighted in the company’s key takeaways:

The company’s capital allocation strategy focuses on high-return opportunities, with the business generating over $1 billion in annual operating cash flow. This covers both capital expenditures and the dividend, while adjusted EBITDA growth supports an incremental $1.5 billion of leverage-neutral growth capital financing.

Iron Mountain’s stock closed at $95.55 on August 5, 2025, up 0.82% for the day. The shares have traded between $72.33 and $130.24 over the past 52 weeks. Following the Q1 2025 earnings report in May, the stock had experienced a modest 0.7% increase, reflecting continued investor confidence in the company’s growth strategy.

With its diversified business model, expanding presence in high-growth markets, and consistent financial performance, Iron Mountain continues to execute its transformation from a traditional records management company to a comprehensive information management and digital solutions provider. The increased 2025 guidance suggests management’s confidence in sustaining this momentum through the remainder of the year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.