Can anything shut down the Gold rally?

Introduction & Market Context

Israel Discount Bank (TASE:DSCT) reported solid financial results for the second quarter of 2025, showcasing improved profitability and operational efficiency while advancing strategic initiatives. The bank’s stock traded down 0.72% to 3,167 shekels on August 14, 2025, following the release of its quarterly presentation, though it remains near its 52-week high of 3,485 shekels.

The Q2 results build upon the momentum established in the first quarter, with notable improvements in key performance metrics despite ongoing regional economic challenges. The bank continues to execute its strategic roadmap focused on growth, efficiency, and digital leadership.

Quarterly Performance Highlights

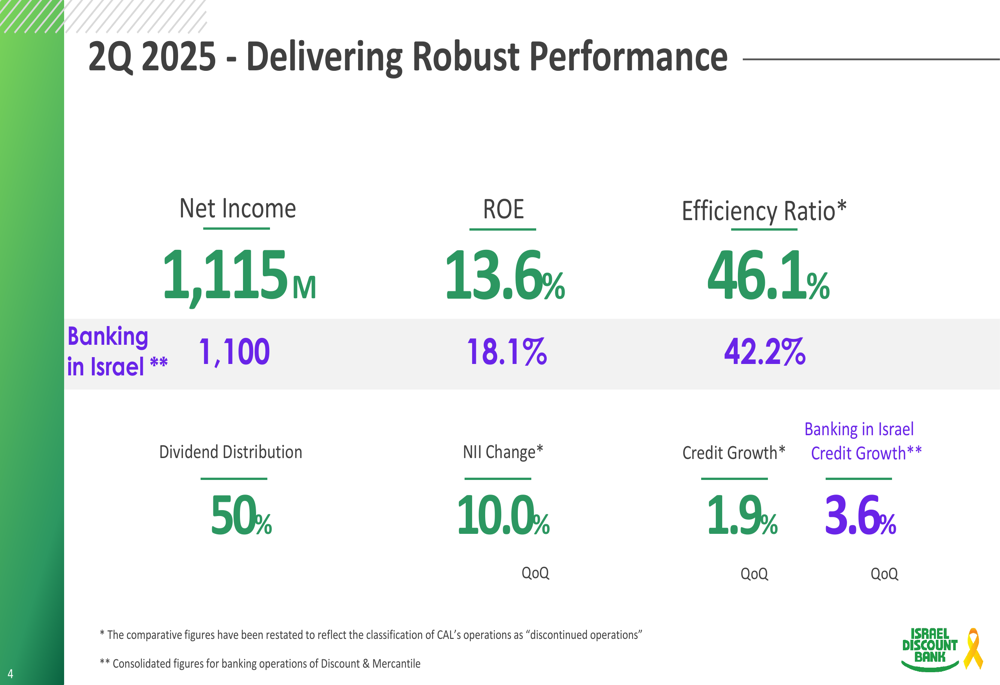

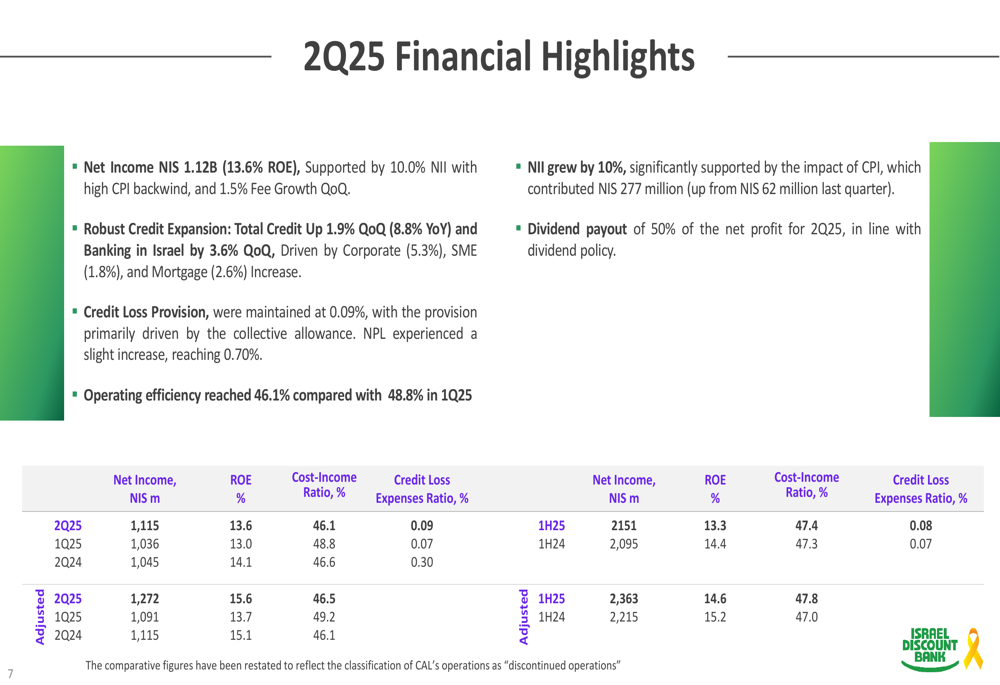

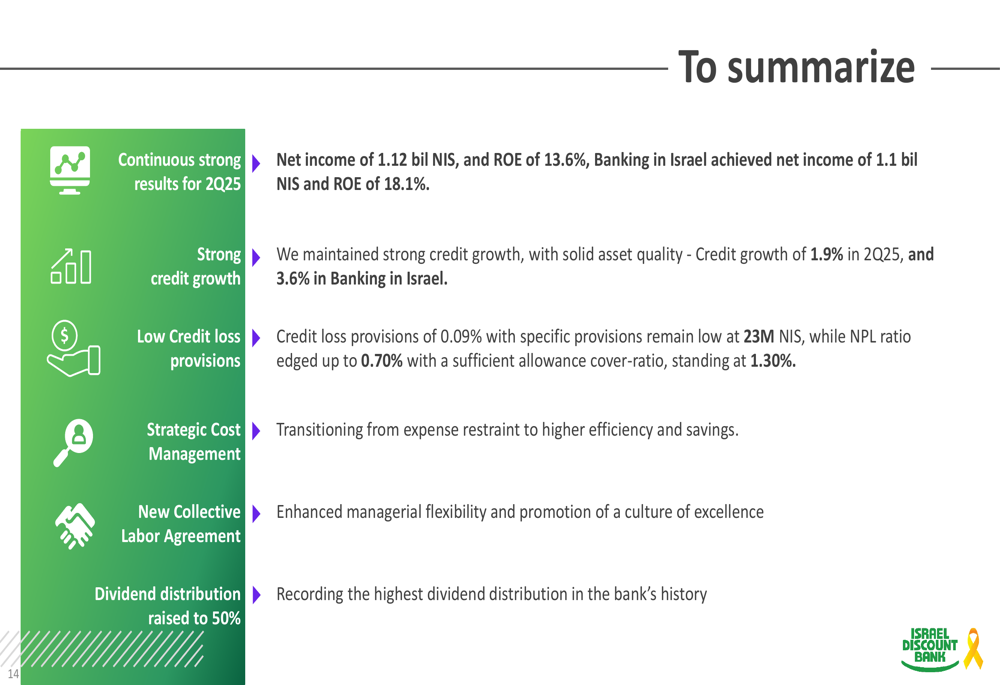

Israel Discount Bank delivered a net income of 1,115 million shekels in Q2 2025, representing a 7.6% increase from the 1,036 million shekels reported in Q1 2025. Return on equity improved to 13.6%, up from 13.0% in the previous quarter, while the efficiency ratio significantly improved to 46.1% from 48.8%.

As shown in the following comprehensive performance overview, the bank maintained strong results across key financial metrics:

The bank’s total revenues rose to 3,490 million shekels in Q2 2025, up from 3,249 million shekels in Q1, primarily driven by a 10% quarter-over-quarter increase in net interest income (NII). This growth was significantly supported by the impact of CPI, which contributed 277 million shekels compared to just 62 million shekels in the previous quarter.

A detailed breakdown of the financial highlights reveals consistent performance in the first half of 2025 compared to the same period in 2024:

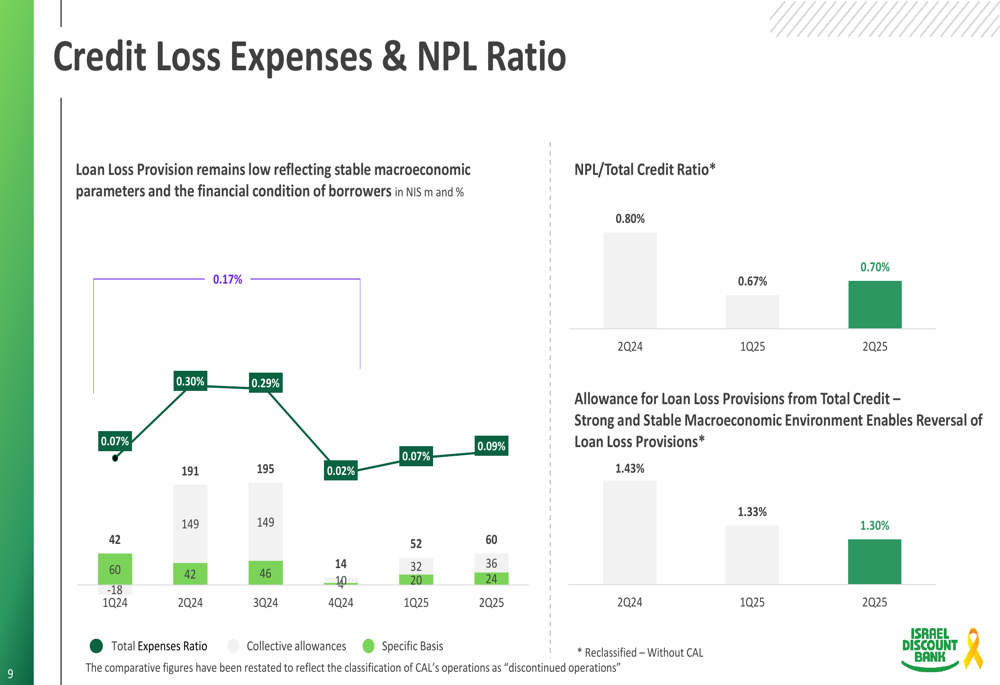

Credit loss provisions remained low at 0.09% of total credit, reflecting stable macroeconomic parameters and the sound financial condition of borrowers. The non-performing loan (NPL) ratio experienced a slight increase to 0.70% from 0.67% in the previous quarter, while the allowance for loan loss provisions decreased slightly to 1.30% of total credit.

The following chart illustrates the bank’s credit quality metrics:

Credit Growth and Portfolio Analysis

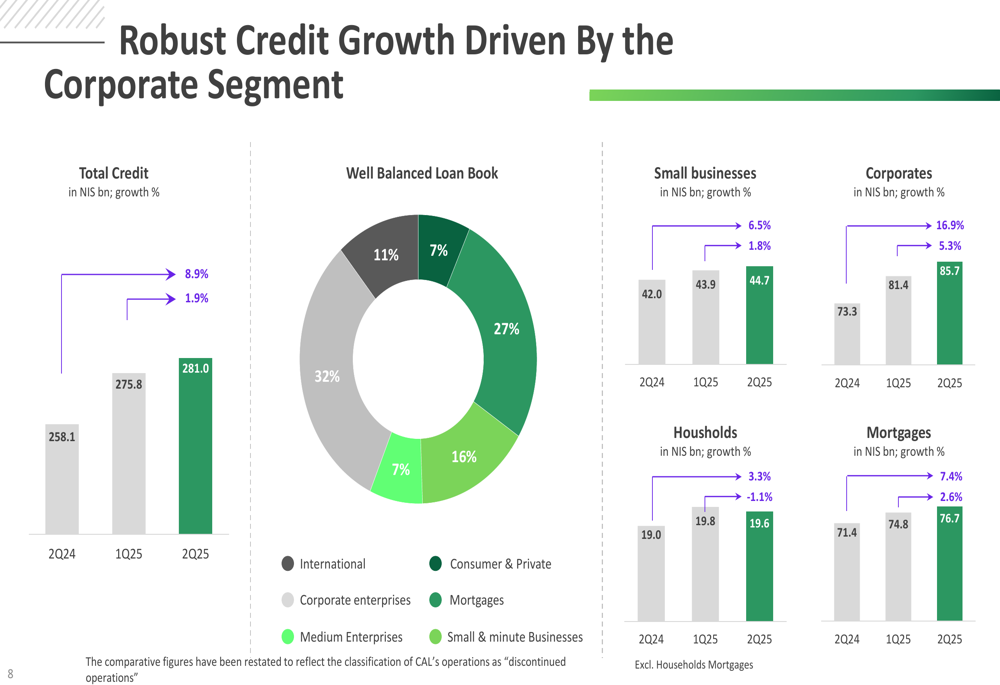

Israel Discount Bank reported robust credit expansion in Q2 2025, with total credit growing by 1.9% quarter-over-quarter and 8.9% year-over-year to reach 281.0 billion shekels. The growth was particularly strong in the corporate segment, which increased by 5.3% quarter-over-quarter and 16.9% year-over-year.

The bank’s loan portfolio remains well-balanced across different segments, as illustrated in the following breakdown:

Mortgage lending also showed healthy growth of 2.6% quarter-over-quarter and 7.4% year-over-year, reaching 76.7 billion shekels. Small business credit increased by 1.8% quarter-over-quarter to 44.7 billion shekels, while household credit slightly decreased by 1.1% to 19.6 billion shekels.

Strategic Initiatives

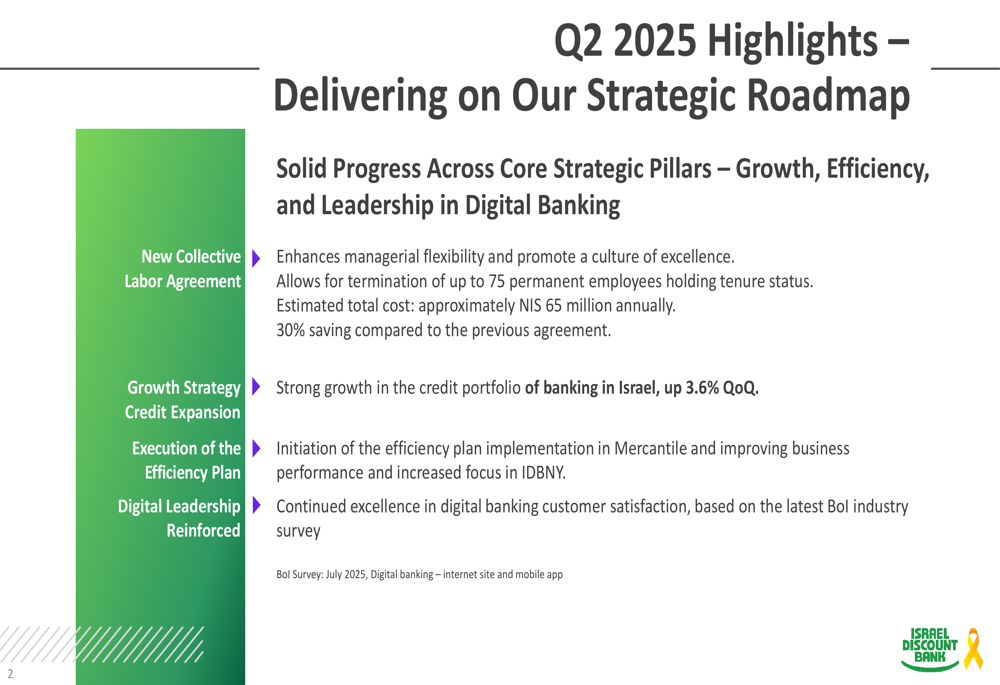

The bank continues to make progress on several strategic initiatives outlined in its roadmap. A key development in Q2 was the implementation of a new collective labor agreement, which enhances managerial flexibility and is expected to generate annual cost savings of approximately 65 million shekels, representing a 30% reduction compared to the previous agreement.

As shown in the strategic roadmap highlights, the bank is advancing on multiple fronts:

Another significant strategic move is the ongoing divestment of CAL (Israel Credit Cards). The bank has entered the second stage of negotiations with three bidding groups and has classified CAL as a "disposal group held for sale" and as a "discontinued operation" beginning with the Q2 2025 financial report. This aligns with the bank’s strategic focus on its core banking operations.

The bank also reported continued excellence in digital banking customer satisfaction, reinforcing its leadership position in this area according to the latest industry survey from July 2025.

Economic Outlook and Forward Guidance

Israel Discount Bank’s presentation included an economic outlook that projects a shift in GDP growth direction for 2025 and a rebound in 2026. According to Bank of Israel forecasts, GDP growth is expected to reach 3.3% in 2025 and accelerate to 4.6% in 2026, following a modest 0.9% growth in 2024 that was impacted by regional conflicts.

The following chart illustrates the economic projections and unemployment trends:

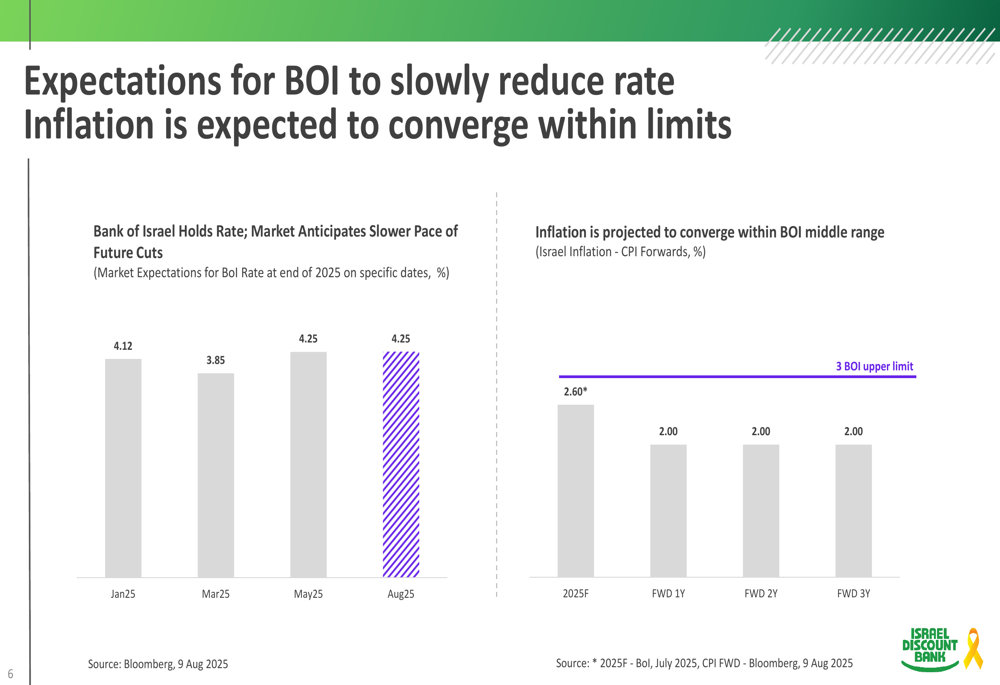

Inflation is expected to converge within the Bank of Israel’s target range, while interest rates are anticipated to decrease at a slower pace than previously expected. The Bank of Israel has maintained its policy rate at 4.25% as of August 2025, with market expectations pointing to gradual reductions in the future.

Capital Position and Dividend

Israel Discount Bank maintains a strong capital position with ratios well above regulatory requirements. The bank’s Tier I Capital Ratio stands at 10.53%, compared to the regulatory requirement of 9.61%, while the Total Capital Ratio is 13.47% against a requirement of 12.61%.

The bank has a robust and diversified funding base, with retail deposits accounting for 50% of total deposits. Liquidity coverage ratio (LCR) and net stable funding ratio (NSFR) remain well above the regulatory requirement of 100%.

In line with its dividend policy, the bank announced a dividend distribution of 50% of Q2 2025 net profit, representing an increase from previous quarters and reflecting confidence in its financial strength and future prospects.

The bank summarized its Q2 2025 achievements with the following highlights:

Overall, Israel Discount Bank’s Q2 2025 results demonstrate continued progress in executing its strategic roadmap while delivering solid financial performance. The bank’s focus on operational efficiency, credit growth, and strategic realignment positions it well for sustainable growth in the evolving economic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.