e.l.f. Beauty stock plummets 20% as revenue and guidance fall short of expectations

Introduction & Market Context

ITAB Shop Concept AB (STO:ITAB) shares plunged 15.16% on Wednesday after the retail solutions provider revealed a significant profit decline in its Q2 2025 interim report presentation. The company reported a 40% drop in adjusted EBIT compared to what management described as a "historically strong" second quarter of 2024, as integration costs from its recent HMY acquisition weighed on performance.

The Swedish retail solutions specialist, which completed its acquisition of HMY in February 2025, is navigating a challenging integration period while facing headwinds in several key markets. The presentation highlighted both the short-term challenges and the company’s longer-term strategic vision through 2027.

Quarterly Performance Highlights

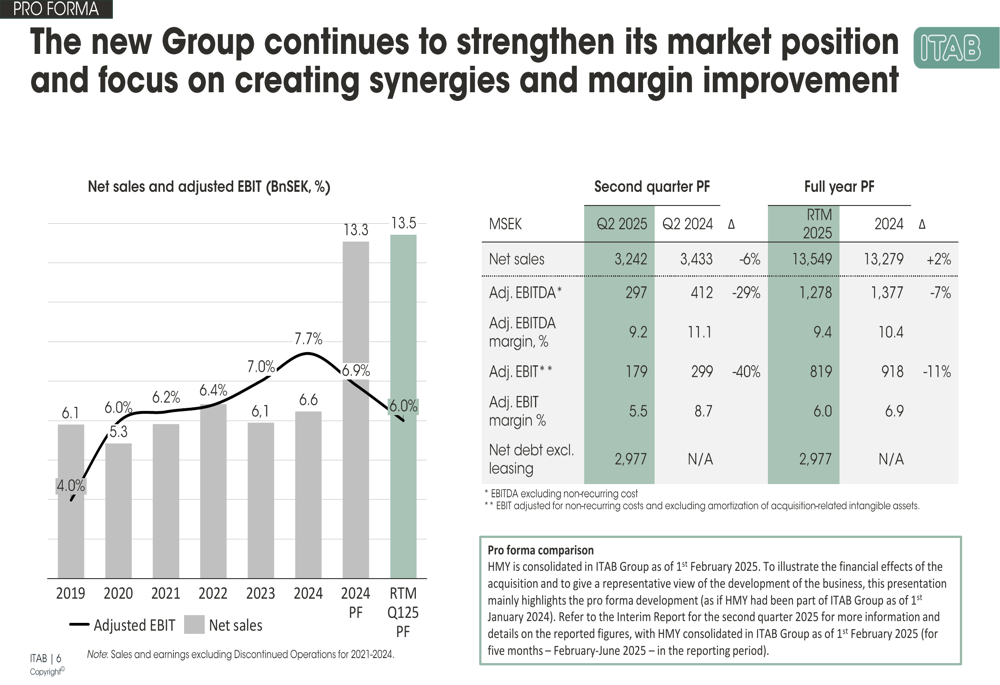

ITAB’s second quarter results showed notable deterioration from both the previous year and the first quarter of 2025. Net sales for Q2 2025 reached 3,242 MSEK, representing a 6% decline from the 3,433 MSEK reported in Q2 2024. More concerning for investors was the sharp drop in profitability, with adjusted EBIT falling to 179 MSEK from 299 MSEK in the comparable period, a 40% decrease.

The adjusted EBIT margin contracted significantly to 5.5% from 8.7% in Q2 2024, reflecting the integration challenges and changing business mix. This performance stands in stark contrast to the company’s Q1 2025 results, which had shown 16% sales growth and a healthier 6.8% adjusted EBIT margin.

As shown in the following financial performance chart:

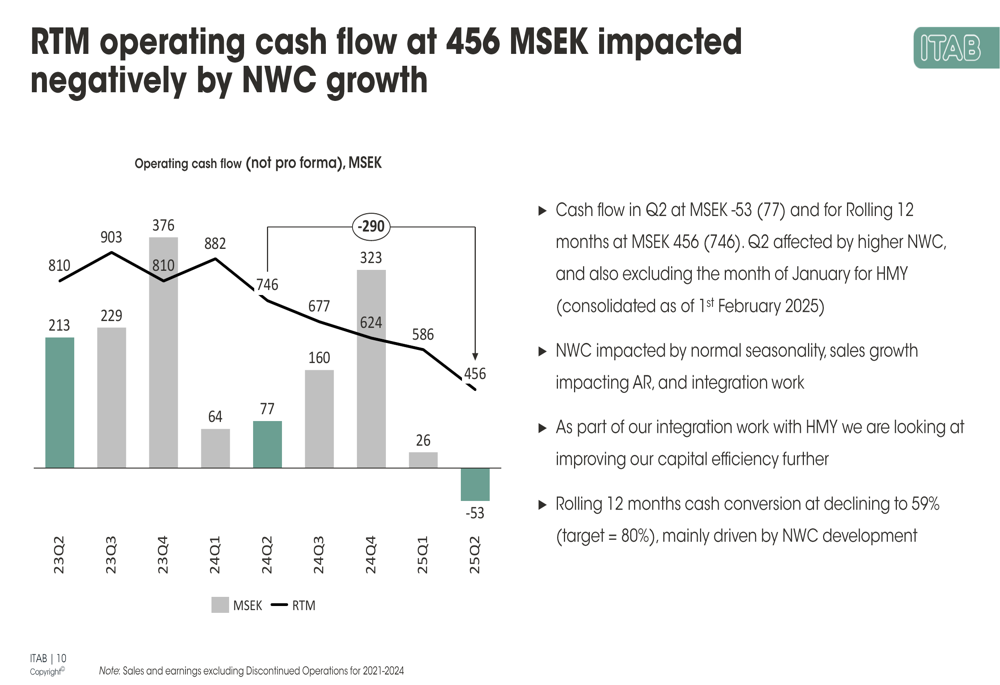

Cash flow also deteriorated markedly, with operating cash flow turning negative at -53 MSEK in Q2 2025 compared to a positive 77 MSEK in the same period last year. Management attributed this to higher net working capital requirements, normal seasonality, and ongoing integration work with HMY.

The cash flow trend over recent quarters illustrates this challenge:

Segment & Regional Performance

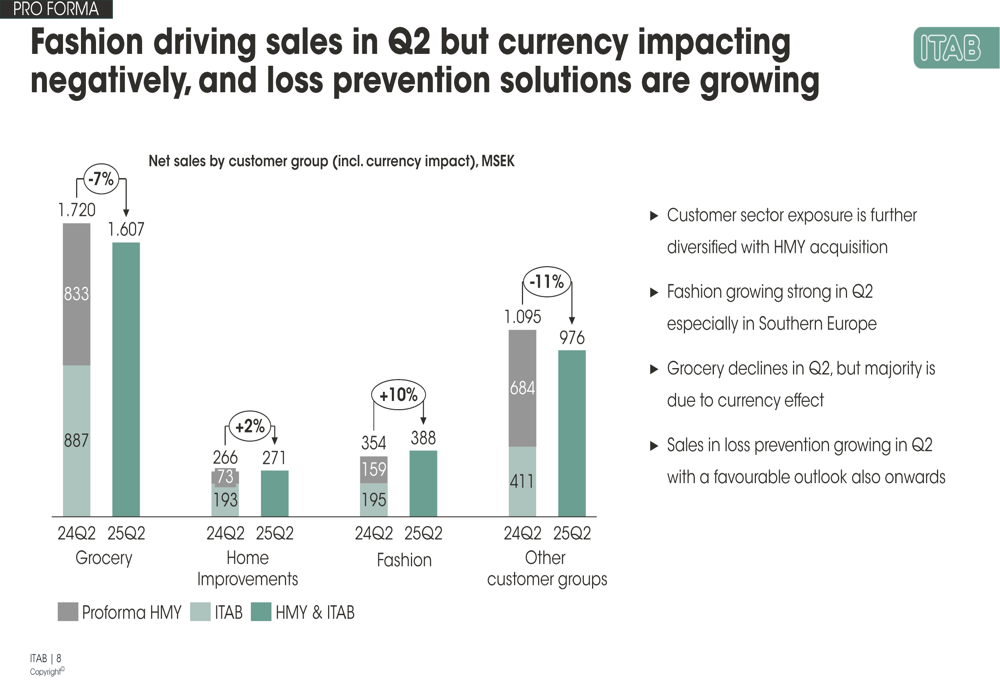

Despite the overall decline, ITAB’s presentation revealed interesting shifts in its business mix following the HMY acquisition. The Fashion segment emerged as a bright spot, growing 10% in Q2 to 388 MSEK, particularly in Southern Europe. Meanwhile, the company’s largest segment, Grocery (representing 51% of total sales), declined 7% to 1,607 MSEK, though management noted much of this was due to currency effects.

The segment performance breakdown shows these contrasting trends:

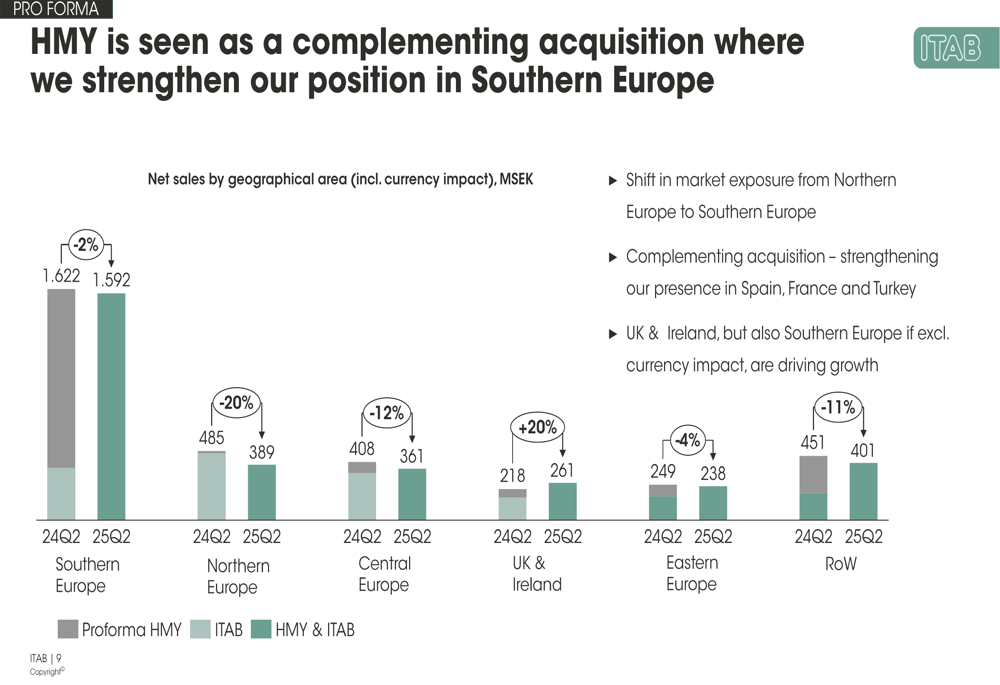

Geographically, the acquisition has shifted ITAB’s center of gravity from Northern Europe toward Southern Europe. The UK & Ireland region showed the strongest performance with 20% growth to 261 MSEK, while Northern Europe saw the steepest decline at 20% to 389 MSEK. Central Europe also weakened with a 12% drop to 361 MSEK.

The regional sales distribution highlights this geographical shift:

Acquisition Integration & Strategy

A central focus of ITAB’s presentation was the ongoing integration of HMY, which was consolidated as of February 1, 2025. Management emphasized the complementary nature of the acquisition, which has strengthened the company’s presence in Spain, France, and Turkey while diversifying its customer exposure.

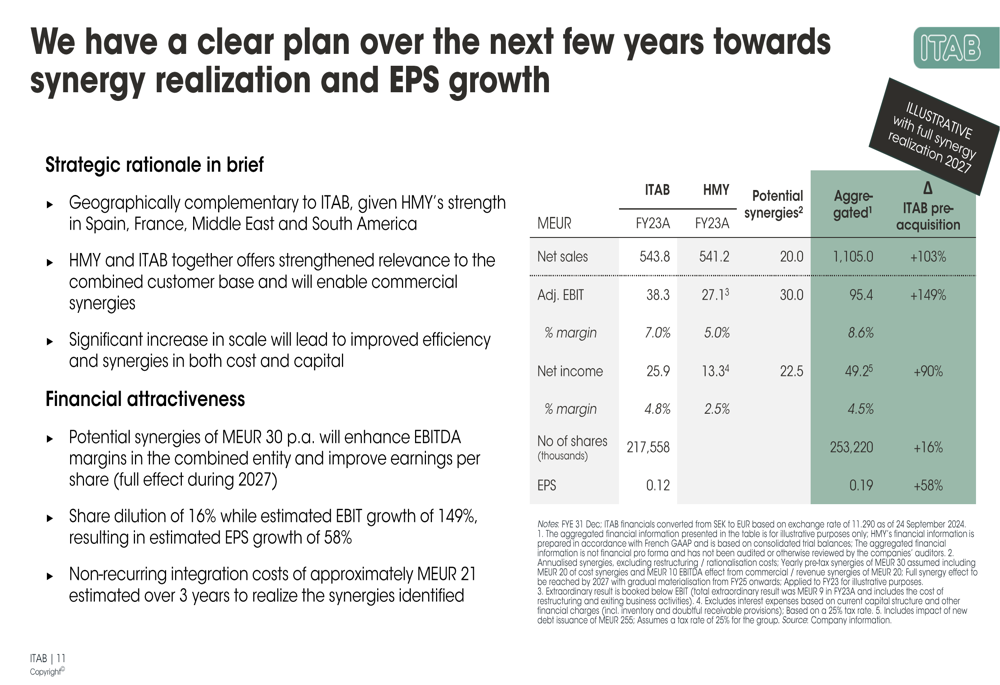

The company outlined ambitious synergy targets of 30 MEUR annually by 2027, which would significantly enhance margins and earnings per share. The presentation included a detailed vision for 2027, showing how the combined entity aims to achieve substantial growth in profitability.

The following chart illustrates ITAB’s 2027 vision and synergy targets:

According to the presentation, ITAB expects the HMY acquisition to ultimately deliver a 149% increase in adjusted EBIT and a 58% improvement in earnings per share, despite a 16% share dilution. However, the company acknowledged that realizing these synergies would require approximately 21 MEUR in non-recurring integration costs over three years.

Strategic Direction & Market Transformation

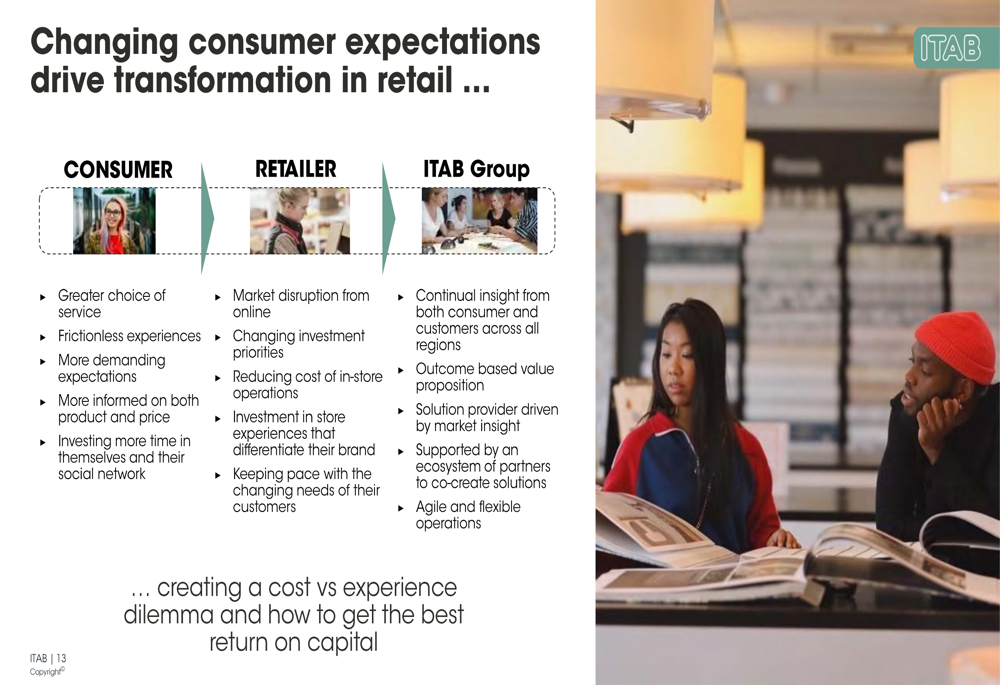

Beyond the immediate integration challenges, ITAB’s presentation emphasized the broader transformation occurring in retail and the company’s strategic response. Management highlighted changing consumer expectations and retailer priorities, positioning ITAB as a solution provider rather than merely a product supplier.

The company outlined its strategic approach to addressing these market changes:

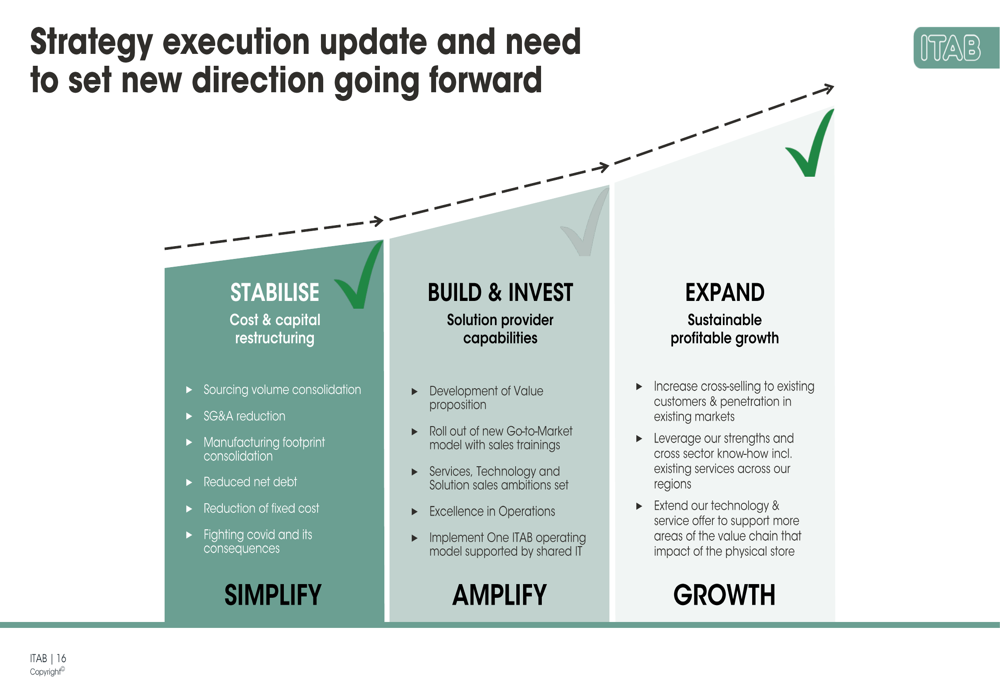

ITAB’s strategy execution is progressing through three phases: Stabilize, Build & Invest, and Expand. The company has completed most of the stabilization work, including cost restructuring and debt reduction, and is now focused on building solution provider capabilities and implementing a unified operating model.

Forward-Looking Statements

Despite the challenging Q2 results, ITAB maintained its confidence in the strategic rationale for the HMY acquisition and its longer-term outlook. Management emphasized that the first six months of 2025 showed 7% sales growth on a currency-adjusted basis, suggesting the Q2 weakness was partly due to comparison with an exceptionally strong prior-year period.

The company highlighted its key focus areas as "People first, Business continuity, Clear plan for the future" while working through the integration process. However, the significant stock price decline following the presentation suggests investors remain concerned about the near-term pressure on margins and cash flow.

With the retail sector continuing to transform and ITAB positioning itself as a partner in this evolution, the company faces the challenge of delivering on its integration promises while maintaining operational performance. The coming quarters will be crucial in determining whether ITAB can successfully navigate this transition period and begin realizing the promised synergies from its expanded European footprint.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.