Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

Itera (OB:ITERA) released its Q2 2025 interim report on August 15, showing continued pressure on financial performance amid persistent market softness. The Nordic IT services provider reported a 9% organic revenue decline compared to the same period last year, with profitability significantly impacted. Despite these challenges, the company is advancing strategic initiatives in the defense sector and Ukraine reconstruction efforts while maintaining its dividend policy.

The company's stock closed at NOK 9.16 on August 14, up 1.35% from its previous close of NOK 9.04, but still trading closer to its 52-week low of NOK 8.00 than its high of NOK 12.00.

Quarterly Performance Highlights

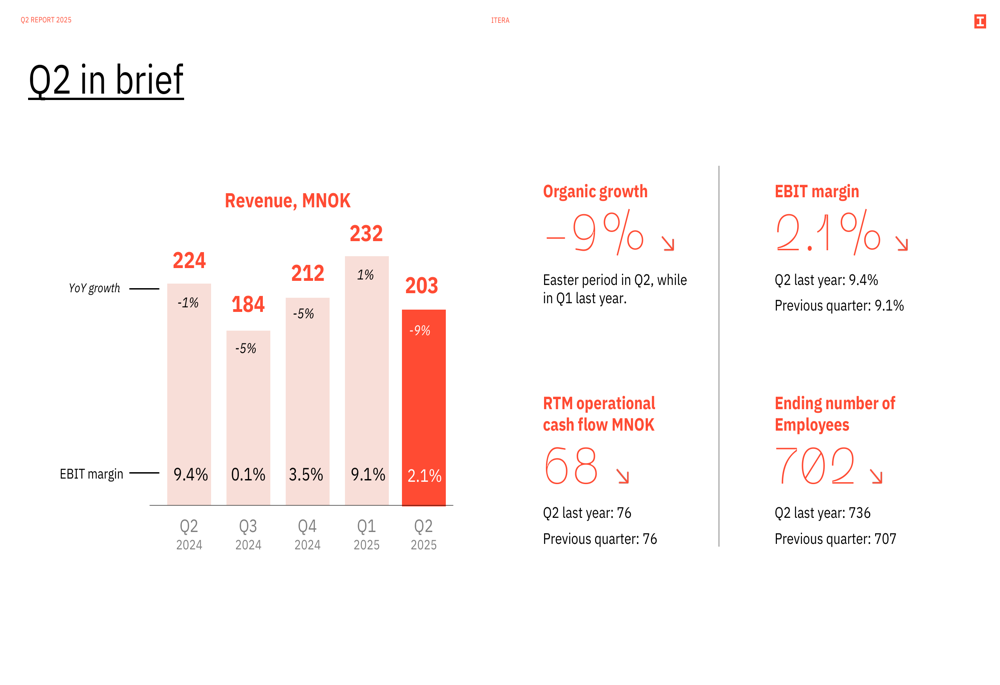

Itera's Q2 2025 financial results show a marked deterioration from both the previous quarter and year-over-year comparisons. Revenue fell to NOK 203 million, down from NOK 224 million in Q2 2024, representing a 9% organic decline. This follows a modest 1% growth reported in Q1 2025, indicating a significant reversal in business momentum.

As shown in the following key figures chart, profitability metrics declined substantially with EBIT margin dropping to 2.1% from 9.4% in the same period last year:

The company attributed the revenue decline to the soft market conditions and the impact of the Easter period falling in Q2. The sequential revenue trend shows volatility over the past five quarters, with the current quarter representing the second-lowest point in this period.

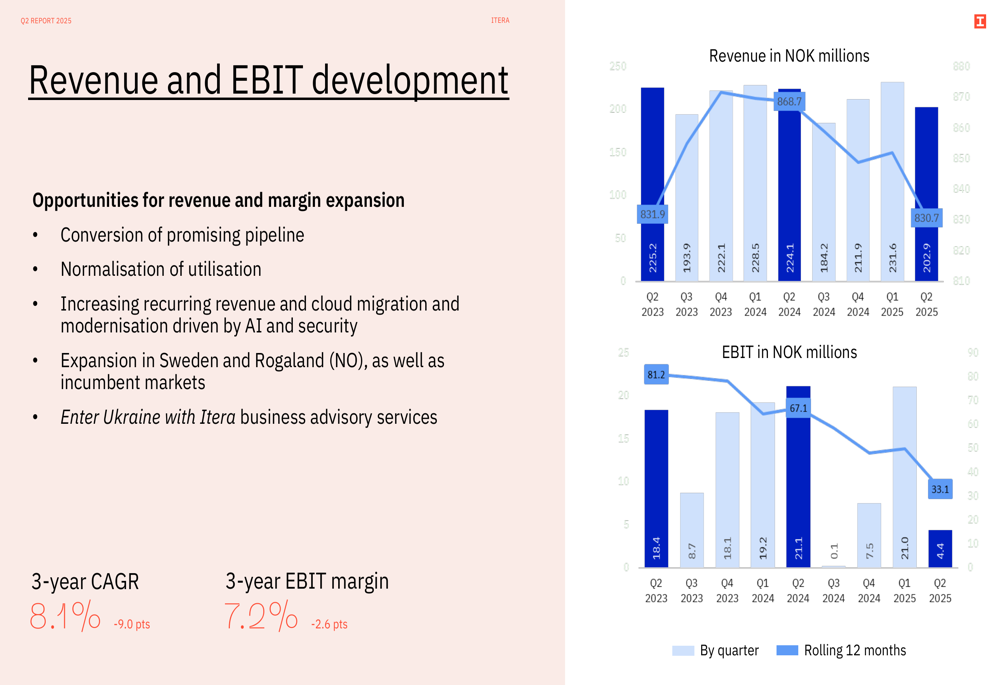

A closer examination of revenue and EBIT development reveals the extent of the profitability challenge:

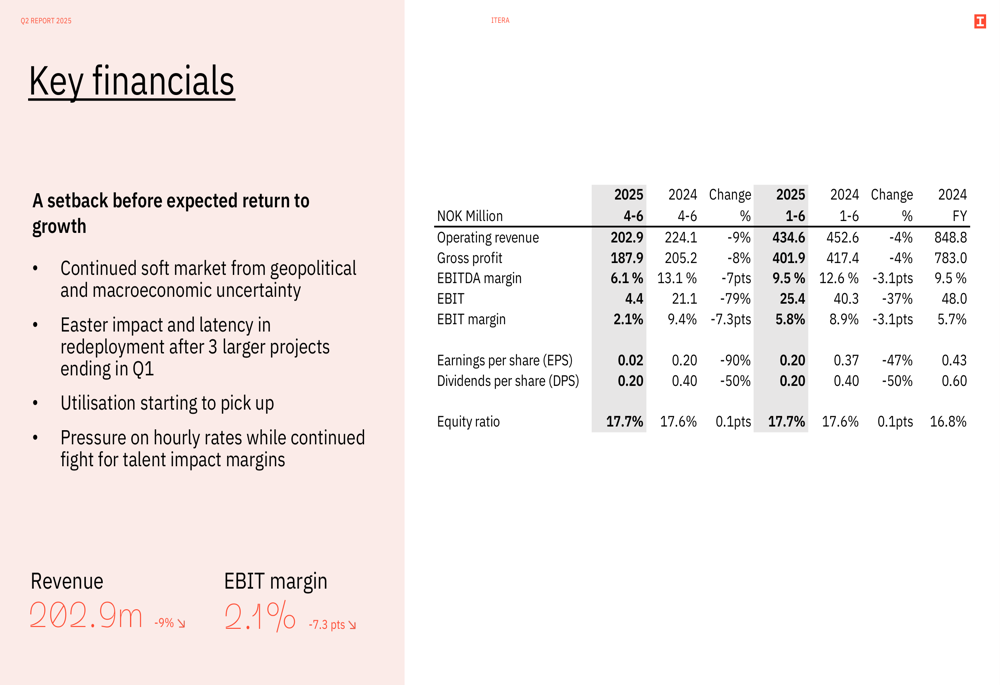

The financial review highlights that while the company maintains a solid cash position, both revenue and margins are under pressure across most business segments:

Revenue Composition and Customer Mix

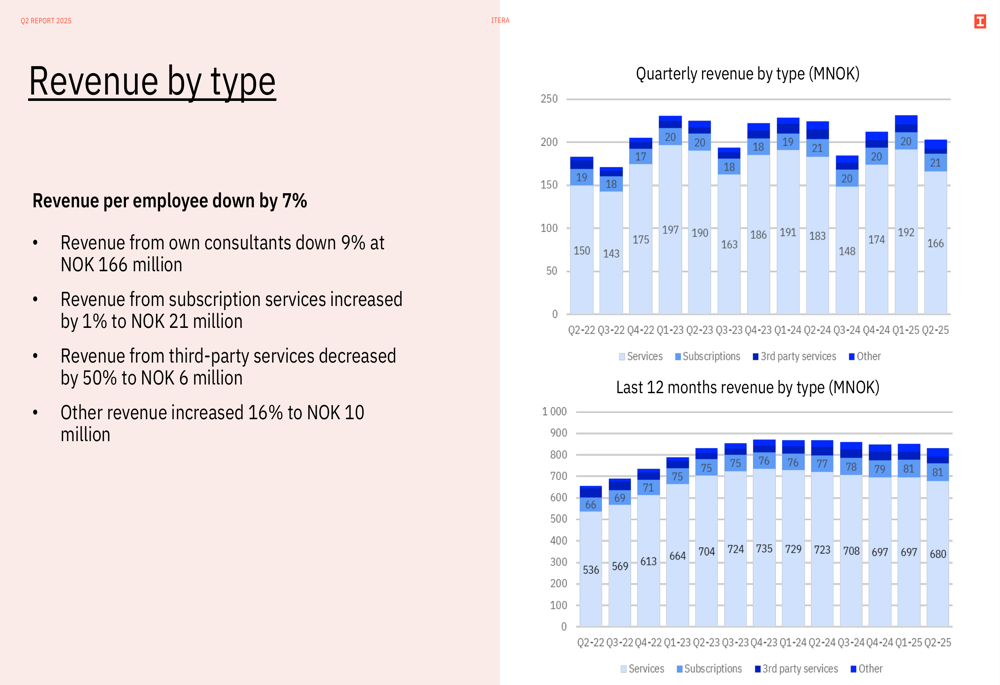

Itera's revenue breakdown shows declining performance across most service categories. Revenue from the company's own consultants, which forms the core of its business, decreased by 9% to NOK 166 million. Third-party services saw an even steeper decline of 50% to NOK 6 million, while subscription services managed a slight 1% growth to NOK 21 million.

The following chart illustrates the revenue distribution by type:

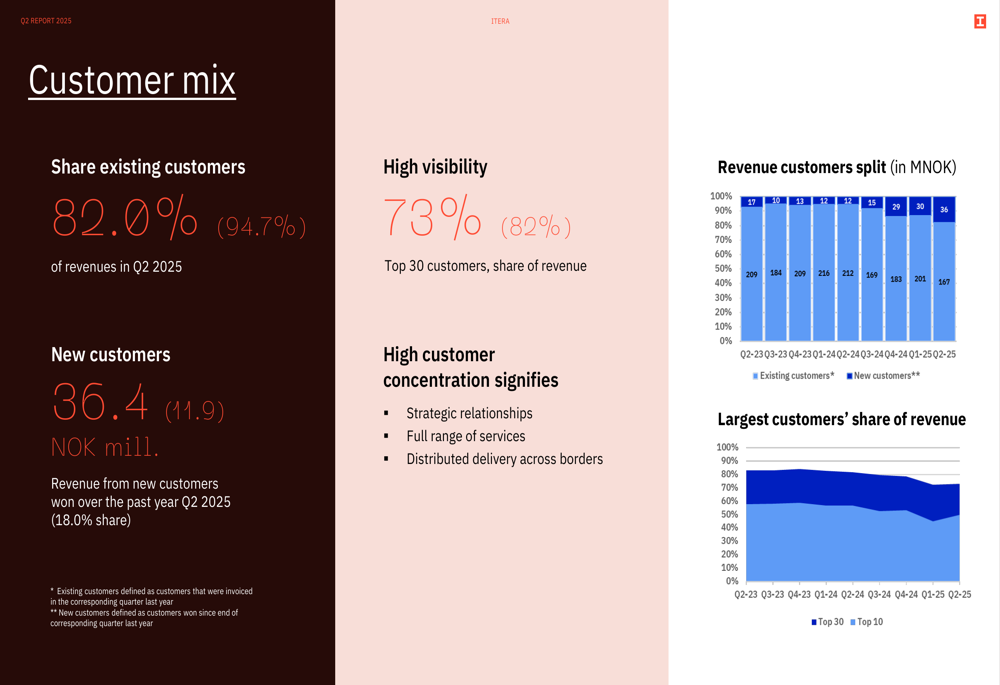

Despite the challenging environment, Itera maintained a relatively stable customer base, with 82% of revenue coming from existing customers, though this represents a decrease from 94.7% in the same period last year. The company's top 30 customers accounted for 73% of revenue, down from 82% previously, indicating some diversification in the customer portfolio.

The customer mix analysis shows:

Strategic Initiatives

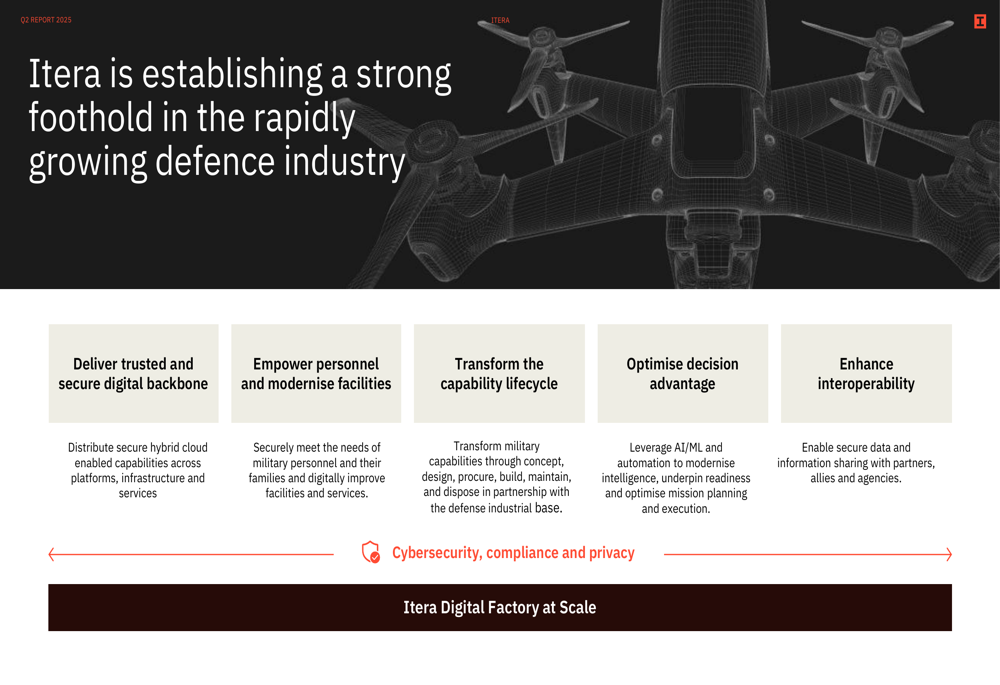

Amid financial headwinds, Itera is actively pursuing strategic growth opportunities, particularly in the defense sector and through its "Enter Ukraine with Itera" initiative. The company secured a significant NOK 1.5 billion housing and infrastructure deal between Vlasne Misto and Moelven Byggmodul at the Ukraine Recovery Conference in Rome.

The company is positioning itself in the rapidly growing defense industry with a comprehensive service offering:

Itera is also strengthening its presence across various sectors, announcing new framework agreements with Statkraft IT in the renewable energy sector and Bane NOR in the public transportation sector. Additionally, the company is expanding its geographic footprint, particularly in Iceland where it secured a framework agreement with Digital Iceland.

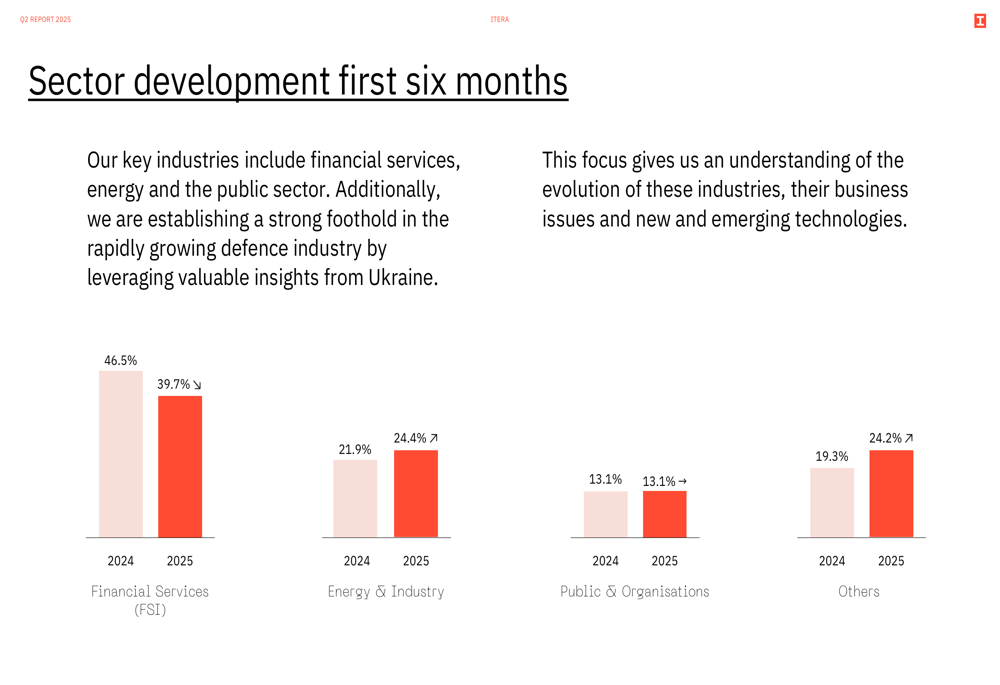

The sector development for the first six months of 2025 shows shifts in Itera's business focus:

Operational Efficiency and Workforce

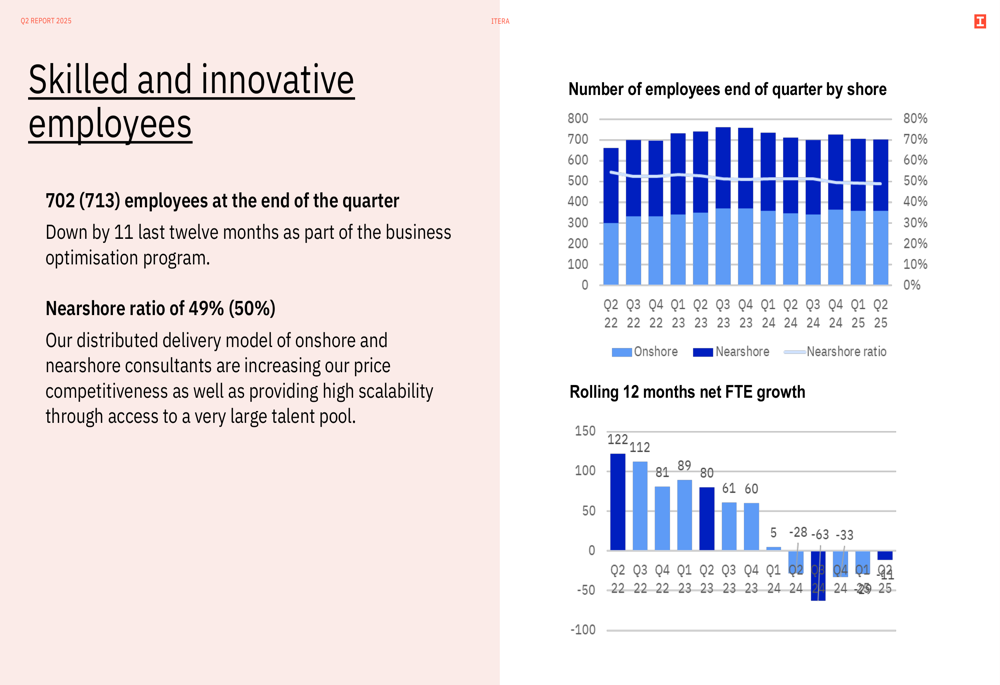

Itera reported 702 employees at the end of Q2 2025, down from 713 in the same period last year. The company maintains a nearshore ratio of 49%, slightly down from 50% previously, as part of its global delivery model across 8 countries and 14 offices in Europe.

The following chart illustrates the employee distribution and growth trends:

The company is enhancing its operational effectiveness through deeper AI integration, supported by reduced overhead and operating expenses. Itera highlighted how AI agents are redefining software development within the organization, with autonomous agents transforming development processes and scaling competence.

Cash Flow and Shareholder Returns

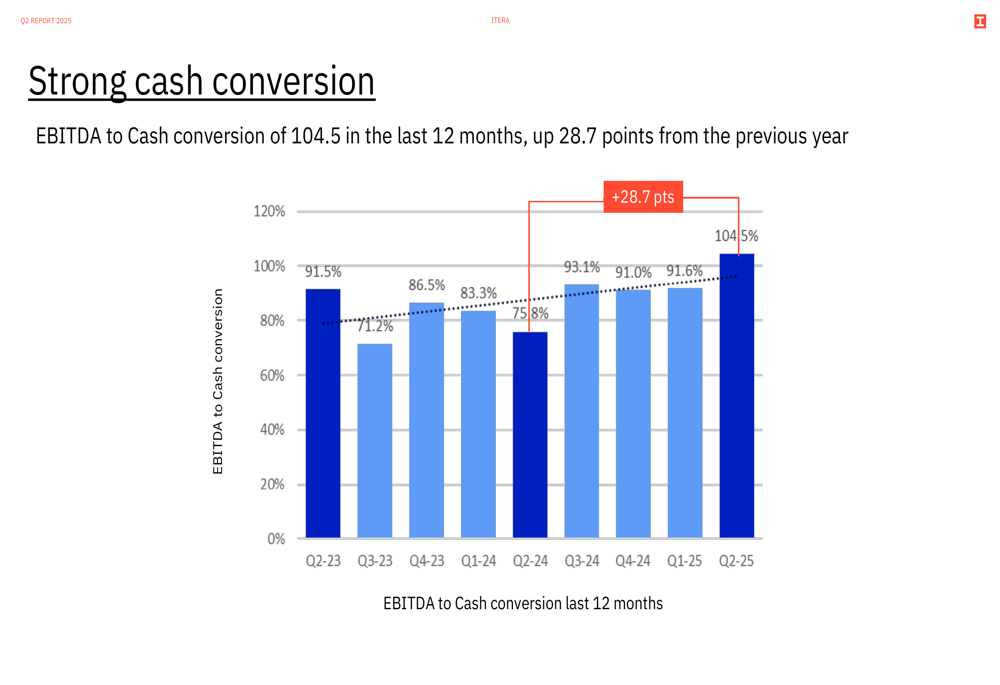

Despite the challenging revenue and profitability environment, Itera maintained strong cash flow performance with operational cash flow of NOK 20.8 million in Q2 2025 and NOK 68.3 million over the last 12 months. The company's EBITDA to cash conversion ratio improved to 104.5 over the last 12 months, up 28.7 points from the previous year.

The strong cash conversion is illustrated in the following chart:

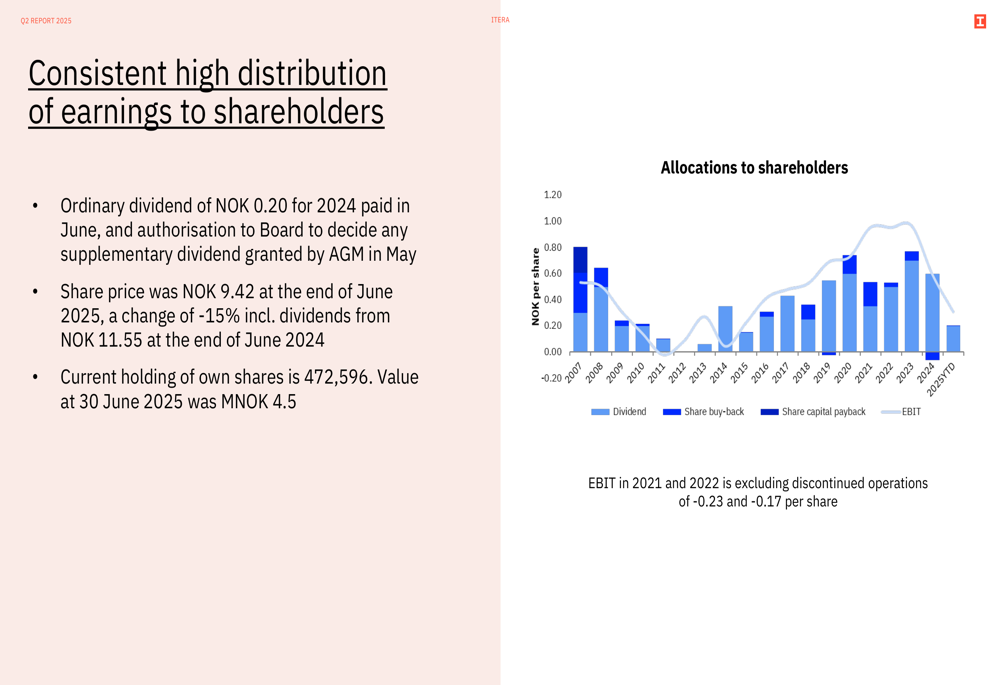

Itera paid an ordinary dividend of NOK 0.20 per share in June 2025, maintaining its track record of consistent shareholder returns. The company has a history of high distribution of earnings to shareholders, as shown in the allocations chart:

Forward-Looking Statements

Looking ahead, Itera's management expressed cautious optimism about market recovery, noting that while demand remains soft, there are signs of slight improvement. The company expects the ongoing shift towards cloud-native and data-driven solutions integrated with AI capabilities to drive substantial growth opportunities.

The outlook emphasizes several key focus areas:

- Underlying strong demand for digital transformation

- Readiness to migrate and operate larger scale cloud transformations to enable AI opportunities

- Potential profit spikes from the "Enter Ukraine with Itera" initiative

- Gaining momentum in the defense industry

- Continued focus on profitable growth and cash flow

Market Reaction and Analysis

The 9% revenue decline and sharp drop in EBIT margin to 2.1% represent a significant deterioration from the Q1 2025 results, where Itera reported 1% organic growth and a 9.1% EBIT margin. This suggests that market conditions have worsened considerably during the second quarter, despite the company's previous indications of market stabilization.

Despite these challenges, Itera's stock has shown resilience, trading at NOK 9.16 as of August 14, up 1.35% on the day. This may reflect investor confidence in the company's strategic initiatives and consistent dividend policy despite the current financial headwinds.

The contrast between Q1 and Q2 performance highlights the volatility in the IT services market and underscores the importance of Itera's strategic pivot toward defense and Ukraine-related opportunities as potential growth drivers in an otherwise challenging environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.