Fed Governor Adriana Kugler to resign

Itron Inc (NASDAQ:ITRI) shares tumbled 8.75% on Thursday after the smart grid solutions provider presented its second quarter 2025 results, revealing a mixed performance characterized by record profitability metrics but slightly lower revenue and reduced full-year sales guidance.

Introduction & Market Context

The July 31 earnings presentation showed that despite achieving record margins and significant earnings growth, investors focused on the company’s lowered revenue outlook and signs of slowing order momentum. Itron’s stock closed at $126.31, down from the previous day’s close of $138.42, with premarket trading already indicating a 5.36% decline before the market opened.

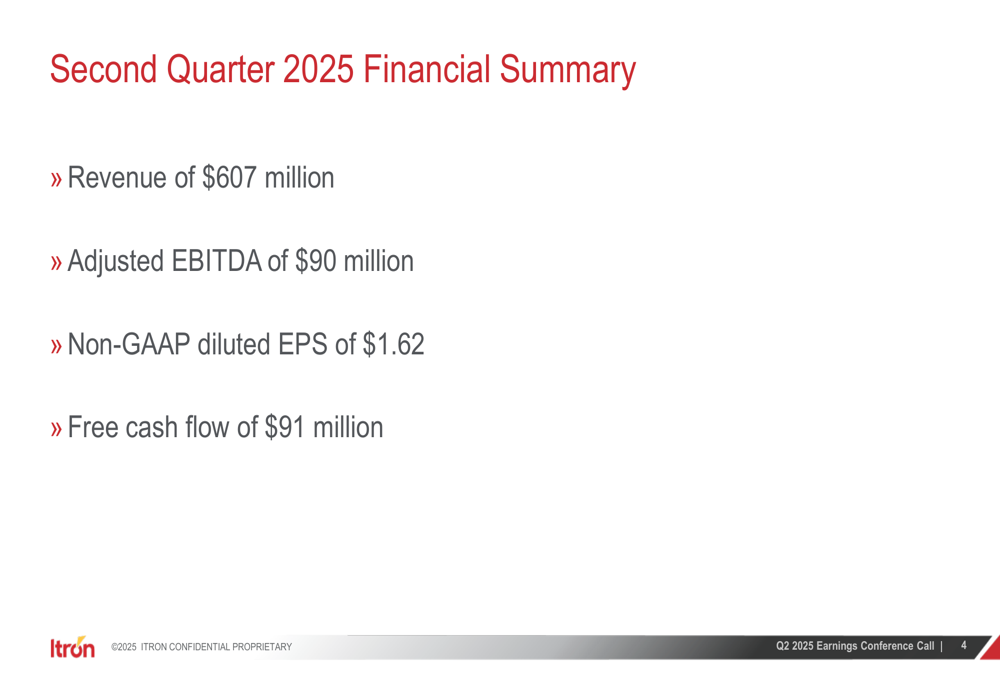

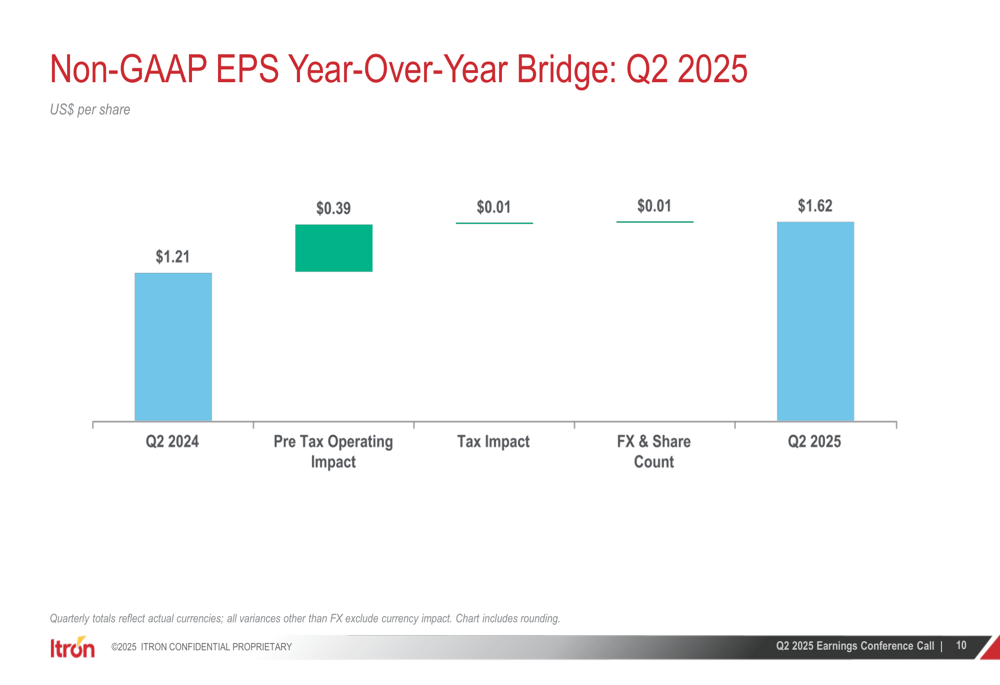

The company reported second quarter revenue of $606.8 million, marginally below the $609.1 million recorded in the same period last year, while non-GAAP earnings per share jumped 34% to $1.62, significantly above the $1.21 reported in Q2 2024.

Quarterly Performance Highlights

Itron’s Q2 2025 financial summary highlighted the company’s ability to drive profitability even with flat revenue. The presentation emphasized record quarterly margins, profitability, and free cash flow, alongside growth in the Outcomes segment’s recurring revenue and software licenses.

As shown in the following summary of key financial metrics:

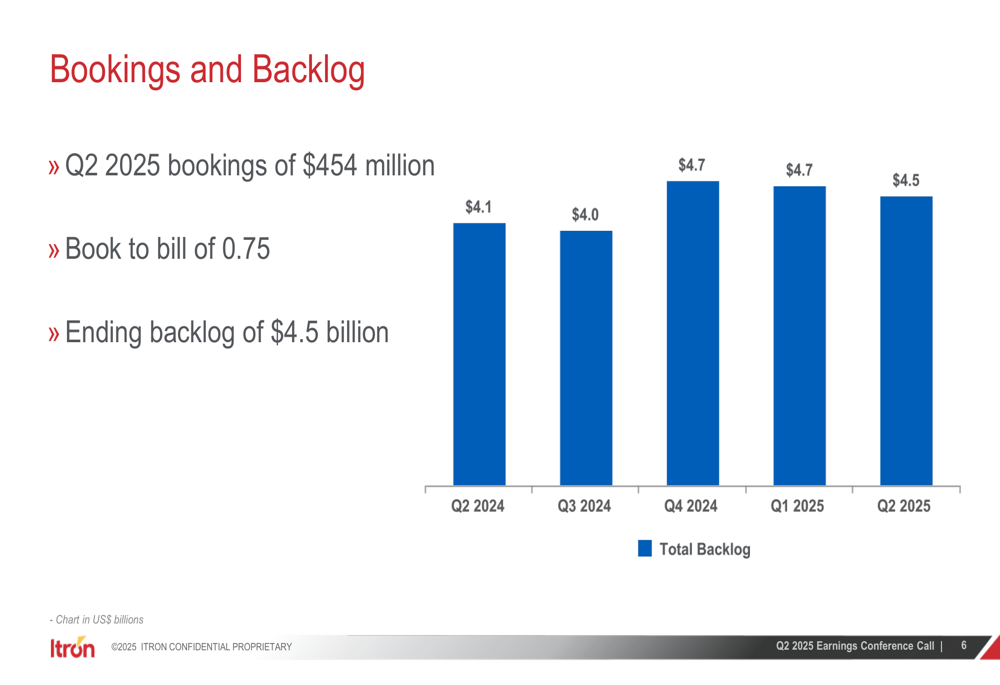

The company’s backlog remained robust at $4.5 billion, though slightly down from $4.7 billion in the previous quarter. This represents a book-to-bill ratio of 0.75 for Q2 2025, suggesting some moderation in new order intake.

The backlog trend over the past five quarters demonstrates Itron’s sustained business pipeline despite quarterly fluctuations:

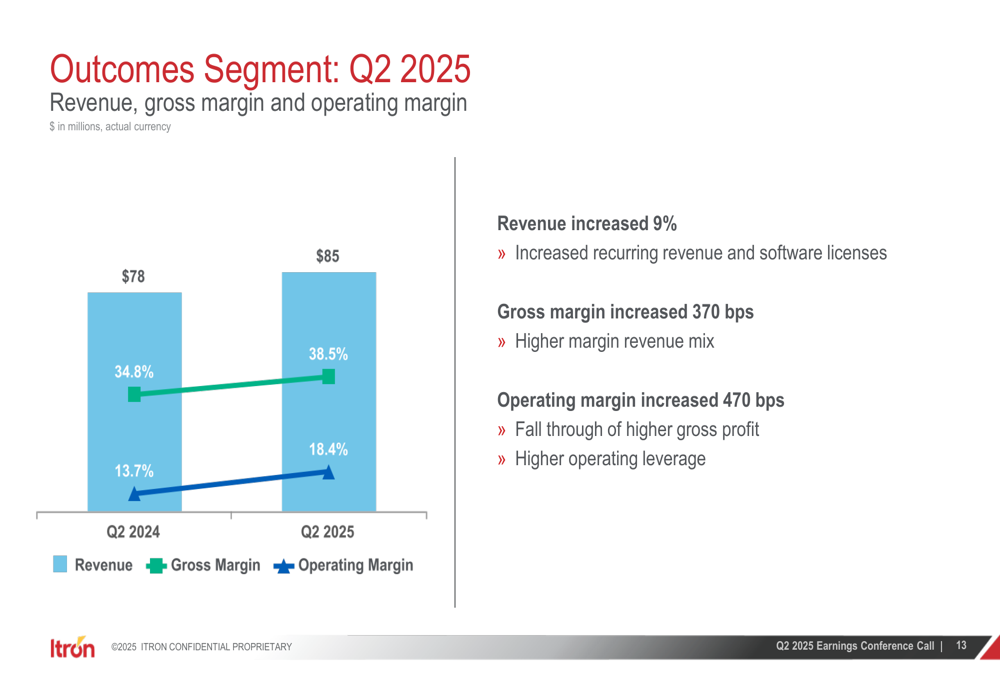

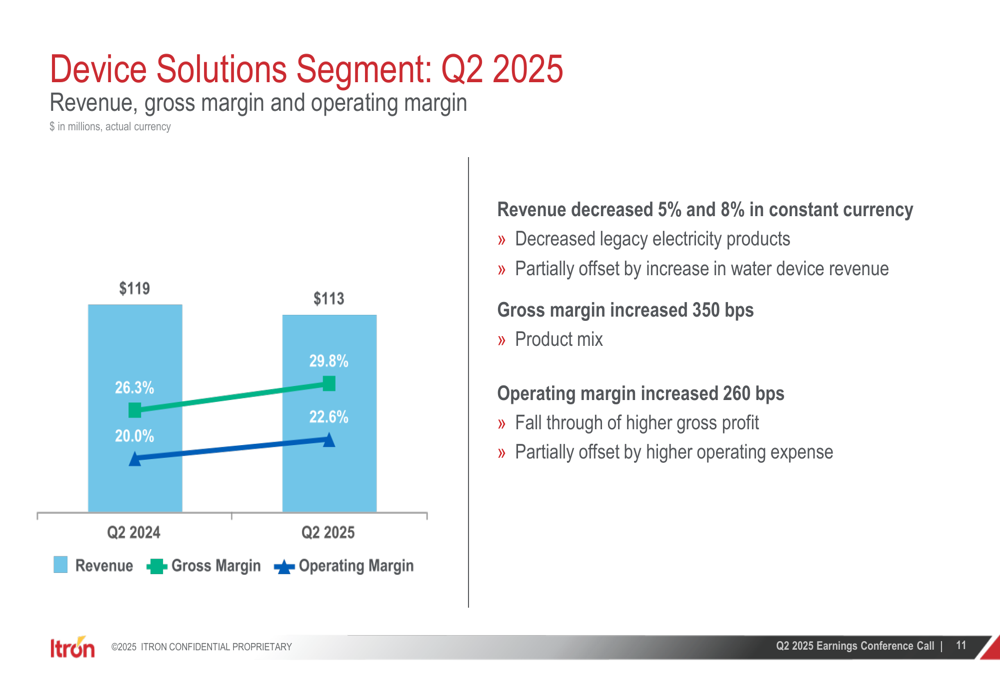

Segment performance revealed divergent trends across Itron’s business units. The Outcomes segment showed the strongest performance with 9% revenue growth, reaching $85 million, while Device Solutions and Networked Solutions experienced revenue declines of 8% and 1%, respectively.

The Outcomes segment’s improving margins reflect Itron’s strategic shift toward higher-value software and services:

Meanwhile, the Device Solutions segment saw revenue decrease to $113 million, though gross margin improved significantly by 350 basis points to 29.8%:

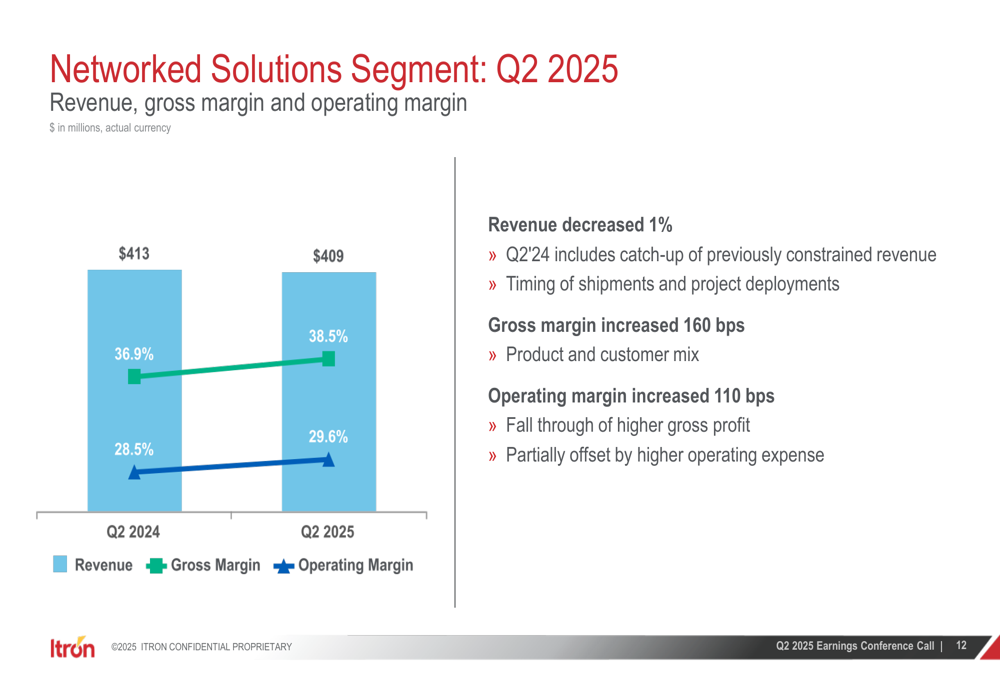

The Networked Solutions segment, Itron’s largest business unit, reported revenue of $409 million, a slight decrease from $413 million in Q2 2024, with gross margin improving by 160 basis points to 38.5%:

Detailed Financial Analysis

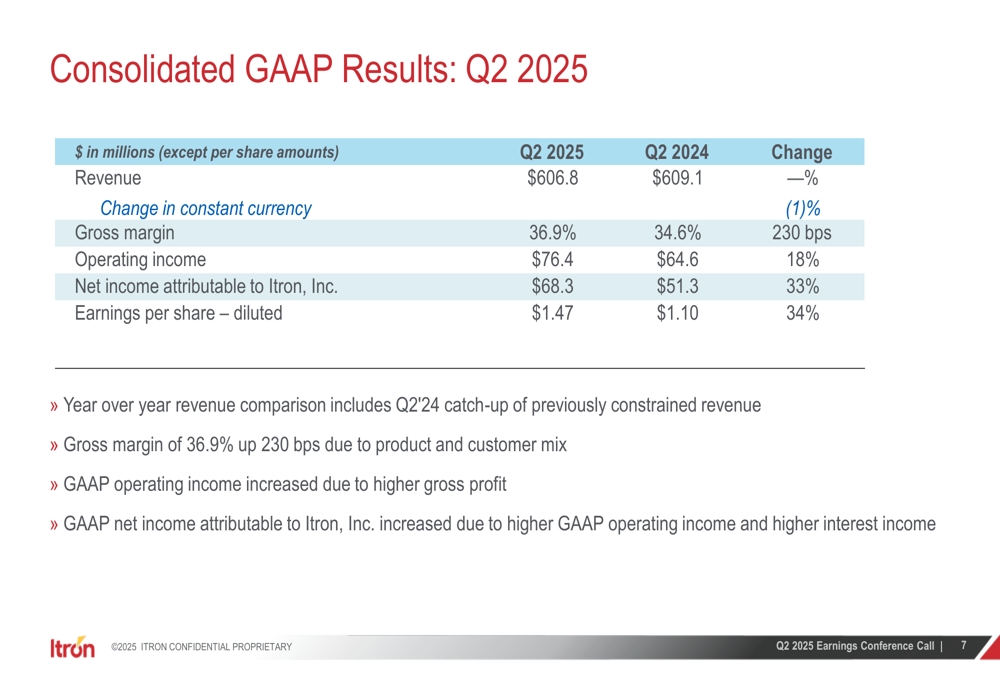

Itron’s consolidated GAAP results showed substantial margin improvement and earnings growth despite the flat revenue performance:

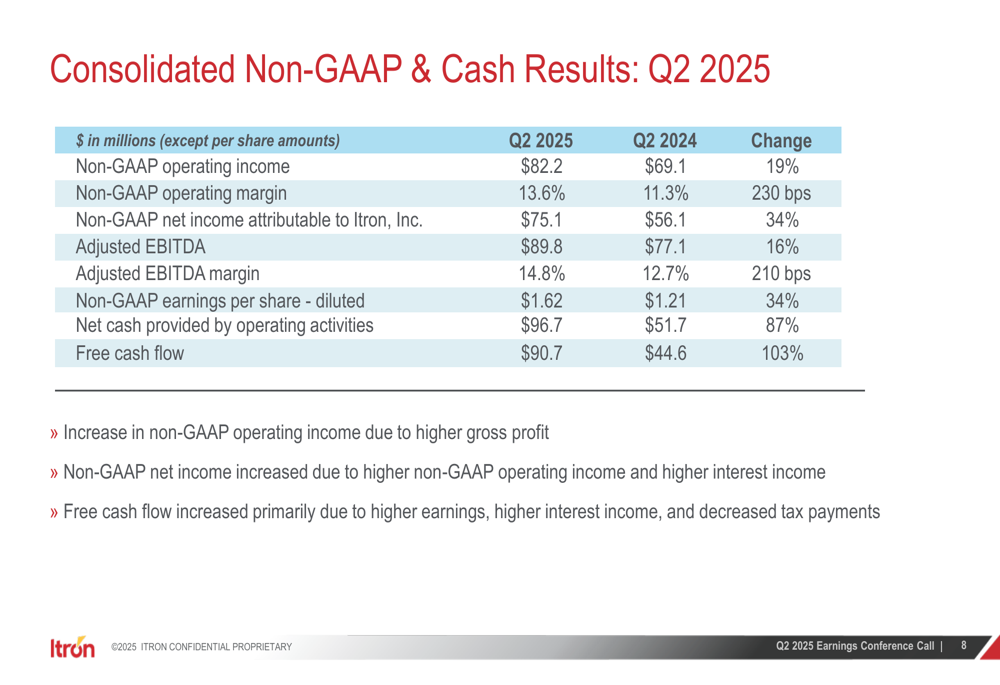

The company’s non-GAAP metrics demonstrated even stronger performance, with operating margin expanding 230 basis points to 13.6% and adjusted EBITDA increasing 16% to $89.8 million:

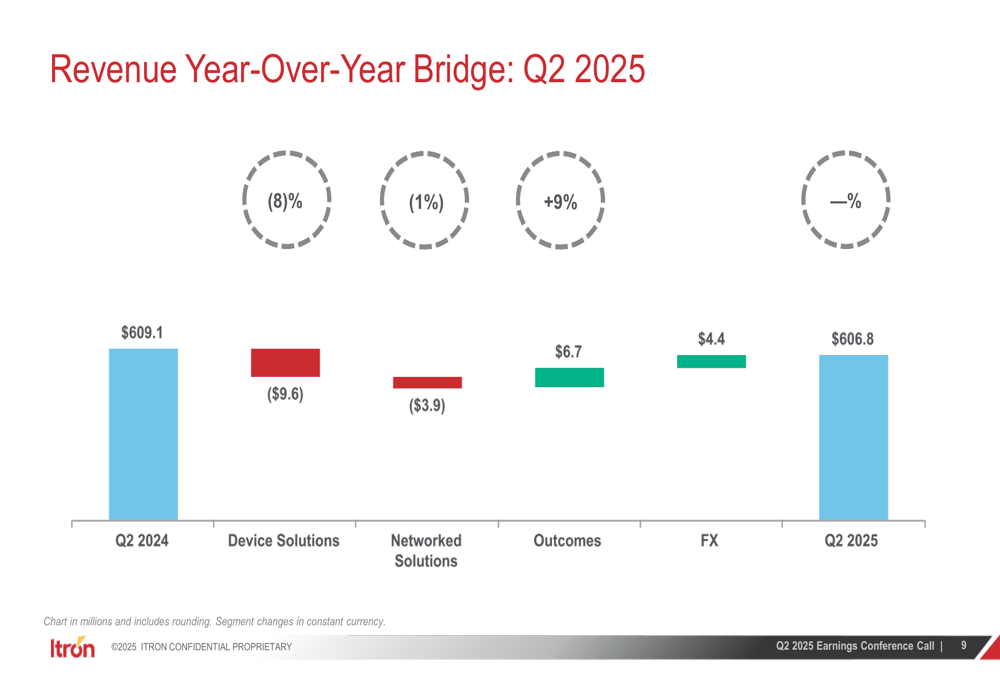

A detailed breakdown of the revenue changes revealed that currency effects provided a $4.4 million boost, partially offsetting declines in Device Solutions and Networked Solutions:

The non-GAAP EPS bridge illustrates that operational improvements were the primary driver of the 34% earnings growth:

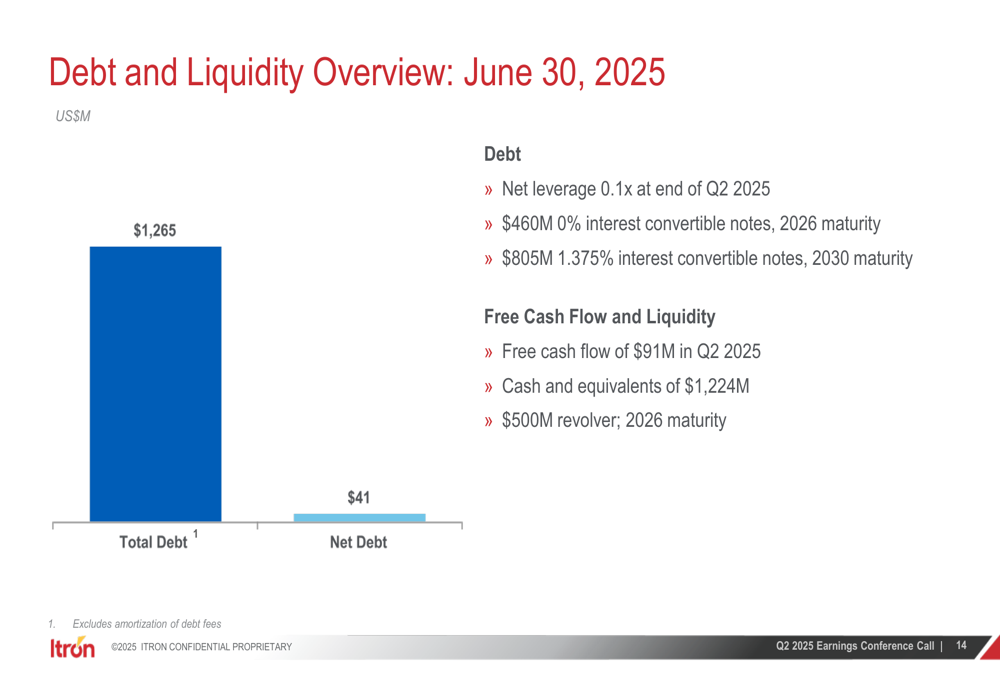

Itron’s balance sheet remains exceptionally strong, with $1,224 million in cash and equivalents against $1,265 million in total debt, resulting in a net leverage ratio of just 0.1x:

Forward-Looking Statements

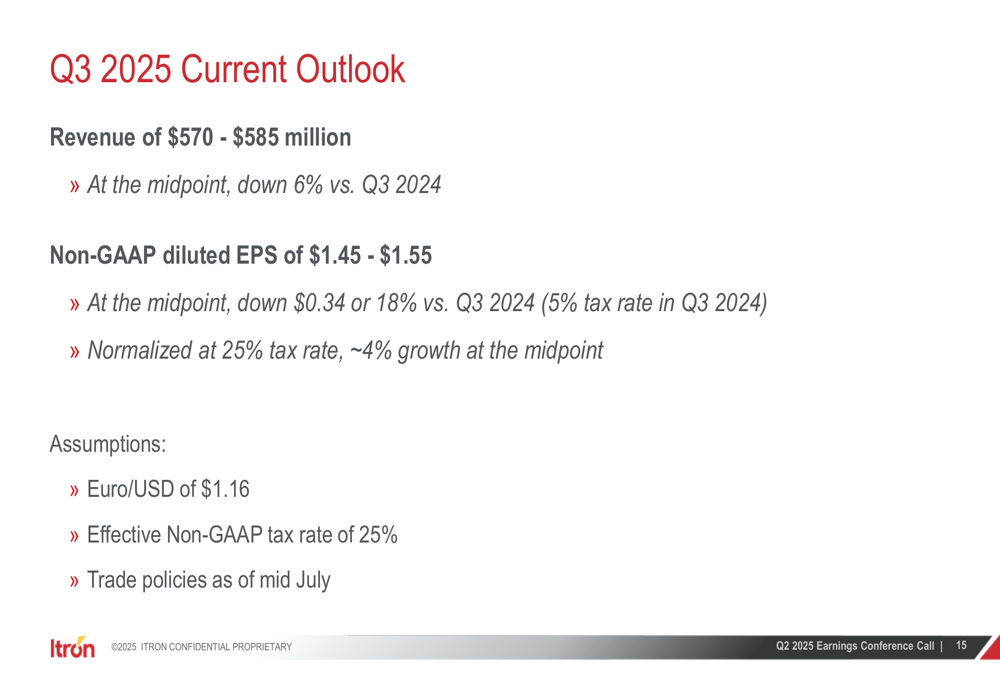

Itron’s guidance for Q3 2025 projects revenue of $570-$585 million, representing a 6% year-over-year decline at the midpoint, with non-GAAP diluted EPS of $1.45-$1.55:

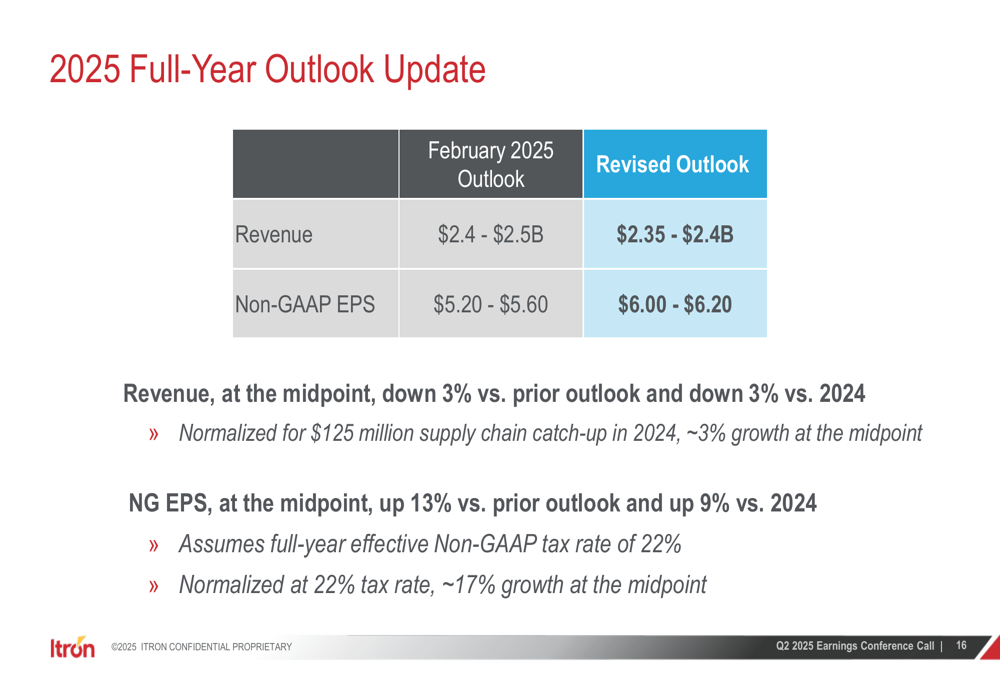

More significantly, the company revised its full-year 2025 outlook, lowering revenue expectations to $2.35-$2.4 billion from the previous range of $2.4-$2.5 billion. However, Itron simultaneously raised its non-GAAP EPS guidance to $6.00-$6.20, up from $5.20-$5.60 previously:

The revised guidance suggests that while Itron is facing revenue headwinds, its focus on higher-margin business and operational efficiency is yielding stronger-than-expected profitability.

Strategic Positioning

Itron’s presentation emphasized the company’s resilience "against dynamic economic and trade backdrop" and noted that demand for its Grid Edge Intelligence offering "remains constructive." The performance metrics indicate a strategic shift toward higher-margin business lines, particularly in the Outcomes segment with its recurring revenue model.

The significant stock decline following the earnings release suggests investors remain concerned about top-line growth prospects despite the impressive profitability metrics. The lower book-to-bill ratio of 0.75 may also indicate potential challenges in maintaining revenue momentum in coming quarters.

Nevertheless, Itron’s exceptionally strong balance sheet, with minimal net debt and substantial cash reserves, positions the company well to weather any market uncertainties and potentially pursue strategic acquisitions to drive future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.