United Homes Group stock plunges after Nikki Haley, directors resign

Introduction & Market Context

J. Front Retailing Co., Ltd. presented its results for the interim period of fiscal year 2025 on October 14, 2025, revealing mixed performance across its business segments. The company, which operates department stores, shopping centers, and real estate development businesses in Japan, faced challenges in its core Department Store segment due to a slowdown in inbound tourism sales, while its Shopping Center (SC) and Developer segments showed growth.

The presentation highlighted the company’s progress on its FY2024-2026 Medium-term Business Plan, which aims to transform J. Front Retailing into a "value Co-creation Retailer" through store renovations, customer base expansion, and strategic property acquisitions.

Quarterly Performance Highlights

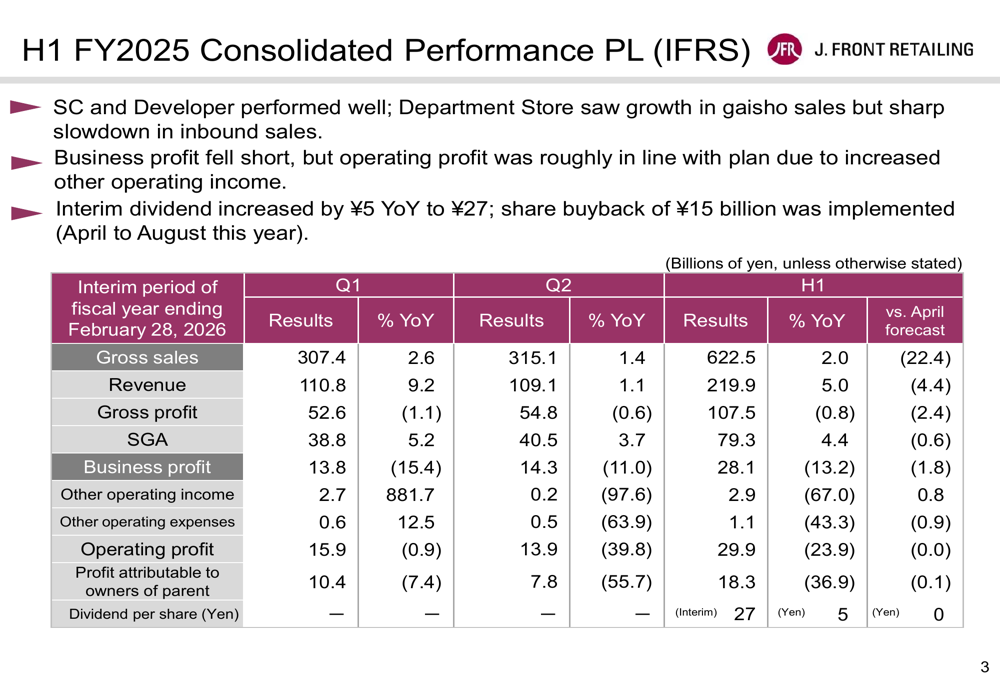

For the first half of FY2025, J. Front Retailing reported gross sales of ¥622.5 billion, falling short of the April forecast by ¥22.4 billion. Revenue reached ¥219.9 billion, below the April forecast by ¥4.4 billion. Business profit was ¥28.1 billion, missing the forecast by ¥1.8 billion, while operating profit came in at ¥29.9 billion, in line with expectations due to increased other operating income.

As shown in the following consolidated performance table, the company increased its interim dividend by ¥5 year-over-year to ¥27 per share and implemented a share buyback of ¥15 billion between April and August 2025:

Segment Performance Analysis

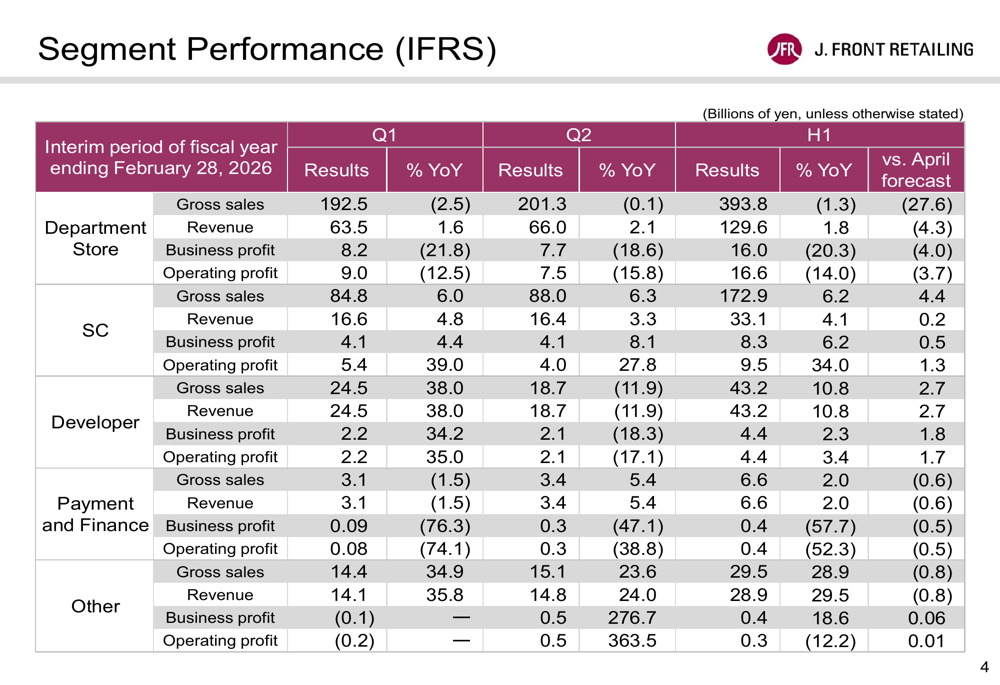

The company’s performance varied significantly across its business segments. The Department Store segment struggled with a sharp slowdown in inbound sales, despite strong performance in the gaisho (affluent customer) business. Business profit in this segment declined by 20.3% year-over-year to ¥16.0 billion.

In contrast, the SC segment performed well, with business profit increasing by 6.2% year-over-year to ¥8.3 billion. The Developer segment also showed growth, with business profit up 2.3% to ¥4.4 billion. The Payment and Finance segment saw a significant decline in business profit (-57.7%) due to upfront costs related to new card issuance.

The detailed segment performance is illustrated in the following table:

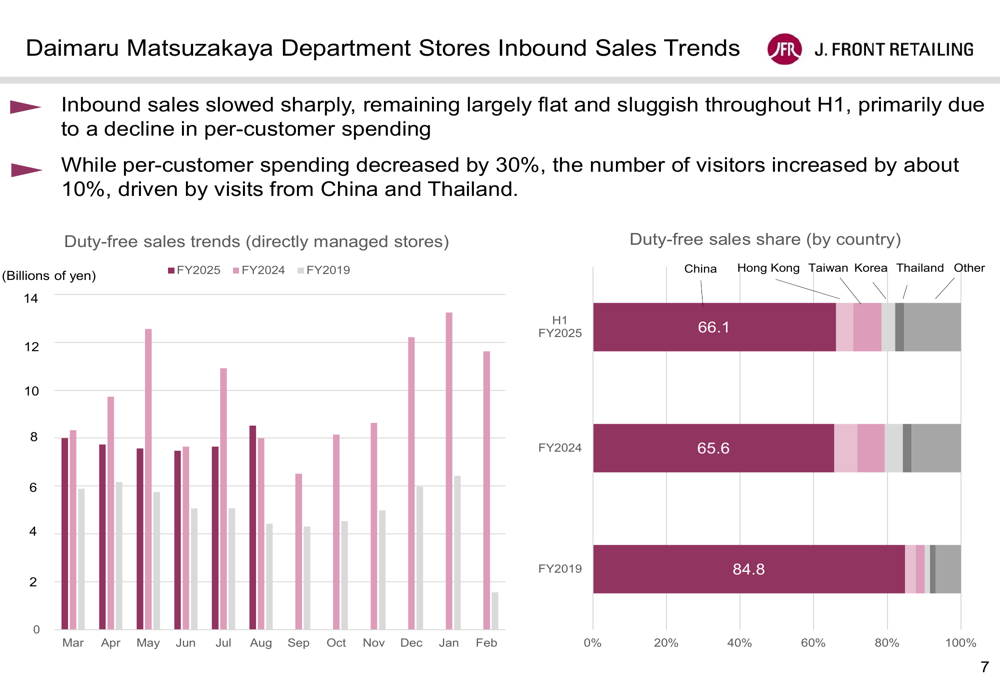

A key factor affecting the Department Store segment was the slowdown in inbound tourism sales. While the number of visitors increased by about 10%, per-customer spending decreased by approximately 30%. The duty-free sales share from China remained dominant at 66.1% in H1 FY2025, slightly higher than the 65.6% in FY2024 but significantly lower than the 84.8% in FY2019.

As shown in the following chart of inbound sales trends:

The company’s PARCO shopping centers showed strong performance, with total comparable stores recording a 7.2% increase in tenant transaction volume for H1 FY2025. Sendai PARCO and Nagoya PARCO showed double-digit revenue growth due to renovations, while Shibuya PARCO’s performance slowed due to ongoing renovation work.

Forward-Looking Statements

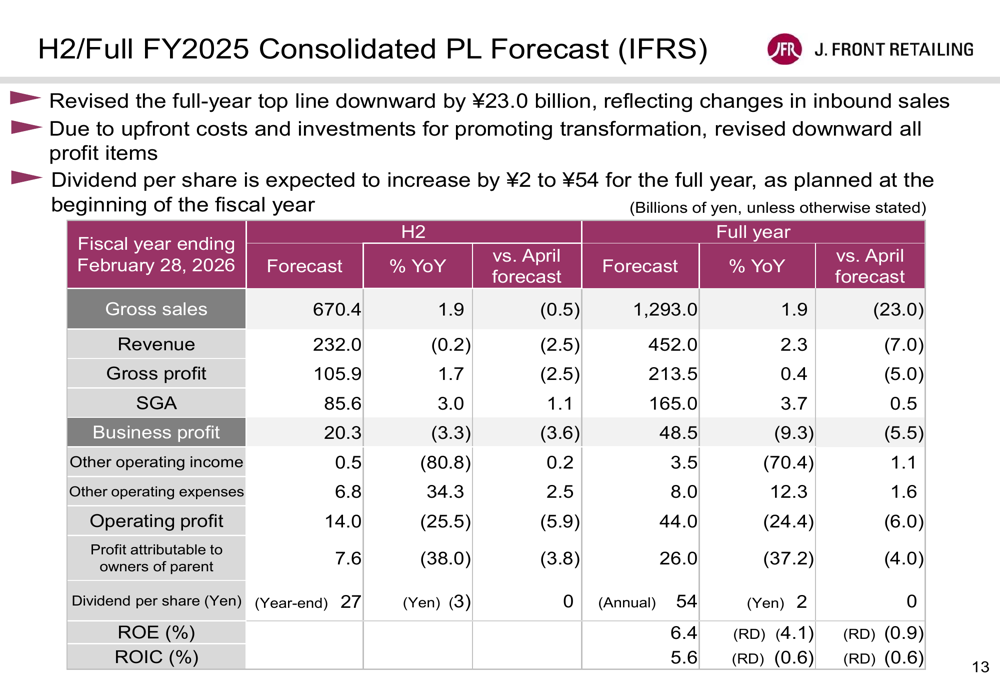

Based on the H1 results, J. Front Retailing revised its full-year forecasts downward. The company now expects gross sales of ¥1,293.0 billion (1.9% YoY), business profit of ¥48.5 billion (-9.3% YoY), and operating profit of ¥44.0 billion (-24.4% YoY). Profit attributable to owners of the parent is forecast at ¥26.0 billion (-37.2% YoY).

Despite the downward revisions, the company plans to increase its annual dividend to ¥54 per share, up ¥2 from the previous year, demonstrating its commitment to shareholder returns.

The revised full-year forecast is detailed in the following table:

The company’s business environment outlook for H2 FY2025 and beyond includes both positive and negative factors. Positive factors include favorable employment conditions, wage increases, economic measures, a rising stock market, wealthy consumption, and potential for increased per-person spending by inbound tourists. Negative factors include the unclear impact of U.S. tariff policy and rising prices dampening consumer confidence.

Strategic Initiatives

J. Front Retailing is making progress on its FY2024-2026 Medium-term Business Plan, focusing on maximizing investment returns and achieving transformation for future growth. Key initiatives include strategic renovations at Matsuzakaya Nagoya and Shibuya PARCO, development of key areas such as Sakae in Nagoya and Shinsaibashi, and card consolidation within the Group.

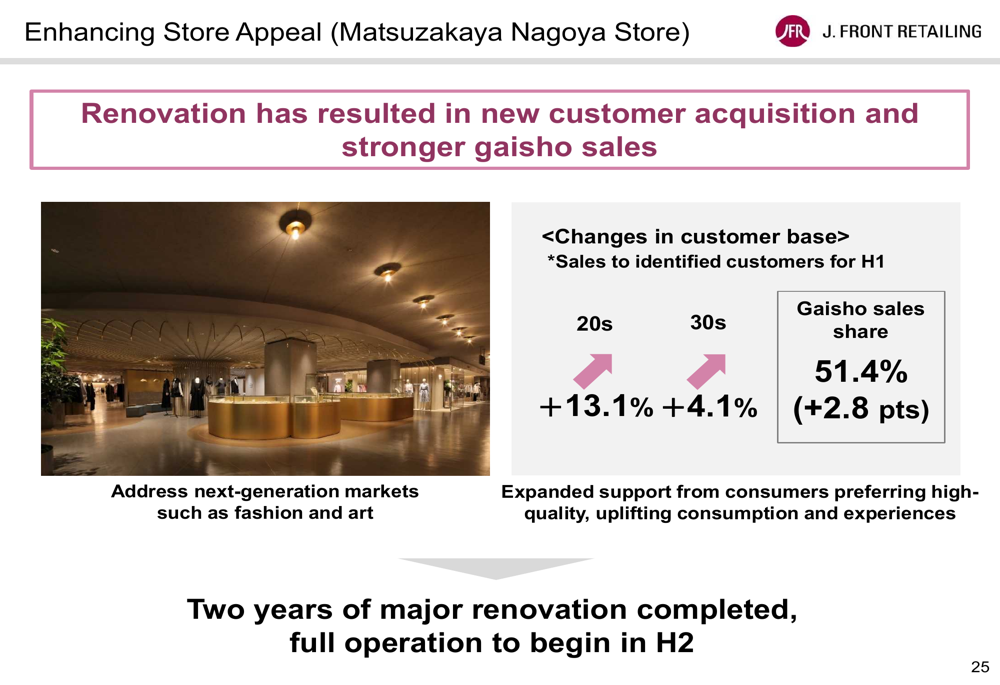

The renovation of Matsuzakaya Nagoya Store has already shown positive results, with increased sales to younger customers and stronger gaisho sales. As illustrated in the following image:

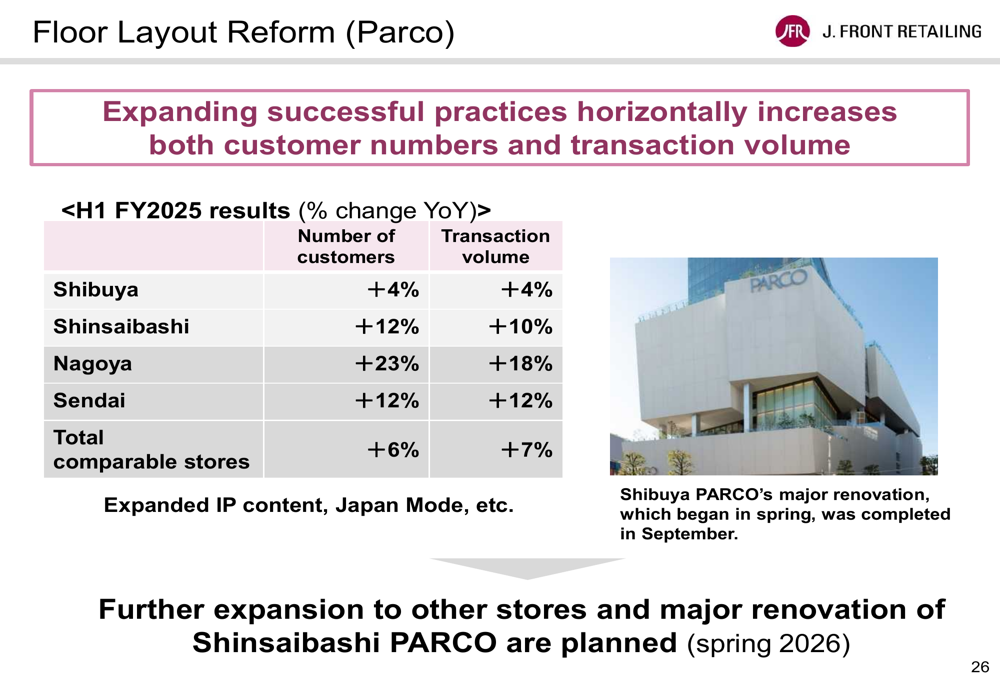

Similarly, the PARCO floor layout reforms have been successful across multiple locations, increasing both customer numbers and transaction volumes. The total comparable stores saw a 6% increase in customer numbers and a 7% increase in transaction volume.

As shown in the following image of PARCO’s performance:

The company is also focusing on expanding its overseas customer base through CRM initiatives for inbound tourists. Approximately 40,000 new members have been added to its app, bringing the total to around 120,000 members. Additionally, the company is strengthening its approach to the affluent market, with gaisho sales of luxury goods and watches forecast to increase by 6.9% and 8.2% year-over-year, respectively.

These strategic initiatives align with the company’s goal of transforming into a value Co-creation Retailer based on three values (Co-creation of Excitement, Co-prosperity with Communities, Co-existence with the Environment), three synergies (Customer, Area, Content), and one approach (One Team, True "Integration").

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.