Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

JFrog Ltd. (NASDAQ:FROG), a leading DevOps and software supply chain management platform, presented its Q1 2025 financial results and strategic outlook on May 8, 2025. The company reported continued momentum with 22% year-over-year revenue growth, reaching $450 million on a trailing twelve-month basis. JFrog’s stock closed at $34.55, up 2.06% for the day, with after-hours trading showing an additional 1.13% gain to $35.66.

The presentation highlighted JFrog’s expanding footprint in the software development ecosystem, particularly in enterprise environments where the company now serves 82% of Fortune 100 companies. With a total addressable market estimated at over $40 billion, JFrog continues to position itself as a critical infrastructure provider for modern software development.

Executive Summary

JFrog’s Q1 2025 presentation emphasized its core value proposition as "The Liquid Software (ETR:SOWGn) Company," focused on creating frictionless software delivery from developer to device. With 7,300 customers and over 1,600 employees, the company has established itself as a key player in the DevOps and software supply chain security market.

As shown in the following snapshot of JFrog’s key metrics:

The company’s financial performance remains strong with $450 million in trailing twelve-month revenue, representing 22% year-over-year growth. JFrog also reported $119 million in free cash flow and a net dollar retention rate of 116%, indicating strong customer loyalty and expansion.

Financial Performance Highlights

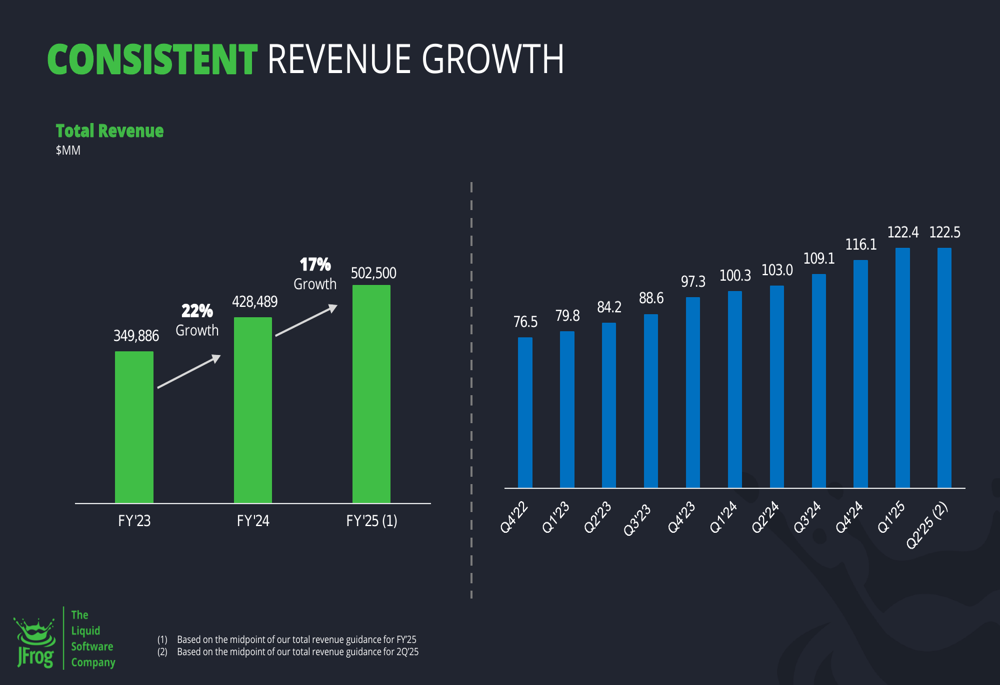

JFrog’s revenue has shown consistent growth over the past several years, with annual revenue increasing from $349.9 million in FY’23 to $428.5 million in FY’24, representing 22% growth. The company projects FY’25 revenue of approximately $502.5 million, indicating 17% growth.

The company’s quarterly revenue progression is illustrated in the following chart:

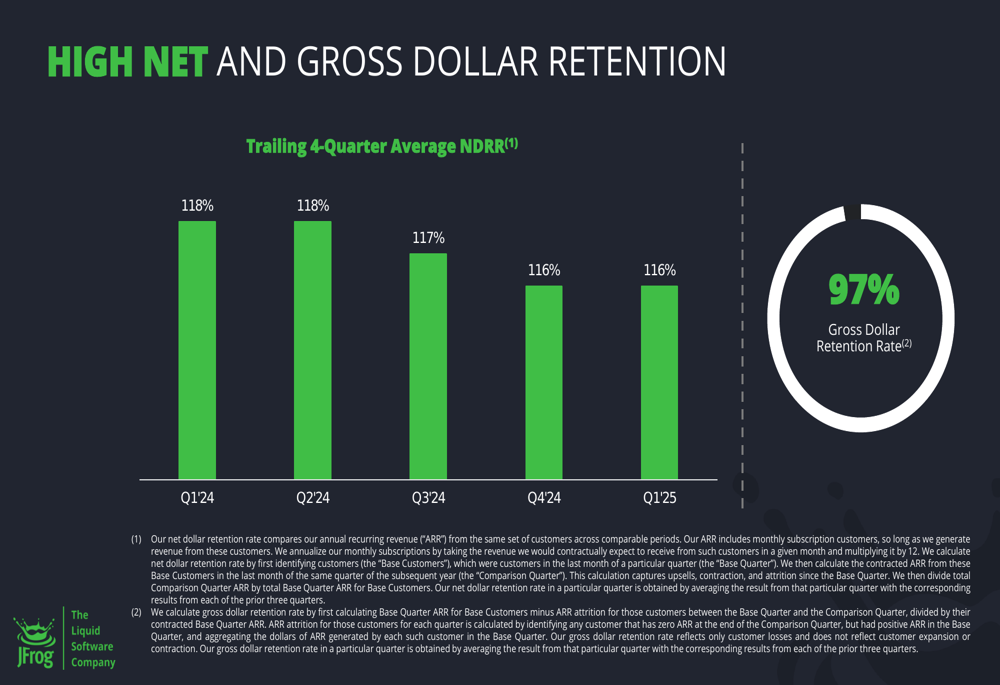

Customer retention metrics remain robust, with a net dollar retention rate of 116% for Q1’25, though this represents a slight decline from 118% in Q1’24. The company maintains a high gross dollar retention rate of 97%, demonstrating strong customer loyalty.

As shown in the following retention metrics chart:

JFrog’s gross margin for Q1’25 was 82.5%, down from 85.1% in Q1’24. This decline aligns with the company’s increasing focus on cloud revenue, which typically carries lower margins than self-hosted solutions. According to the recent earnings call, cloud revenue grew 38% year-over-year in Q3 2024, now comprising 39% of total revenues.

The company’s financial reconciliations show an operating loss of $22.97 million on a GAAP basis for Q1’25, but a non-GAAP operating income of $21.35 million. Free cash flow for Q1’25 was $28.15 million, up significantly from $16.63 million in Q1’24.

Strategic Initiatives

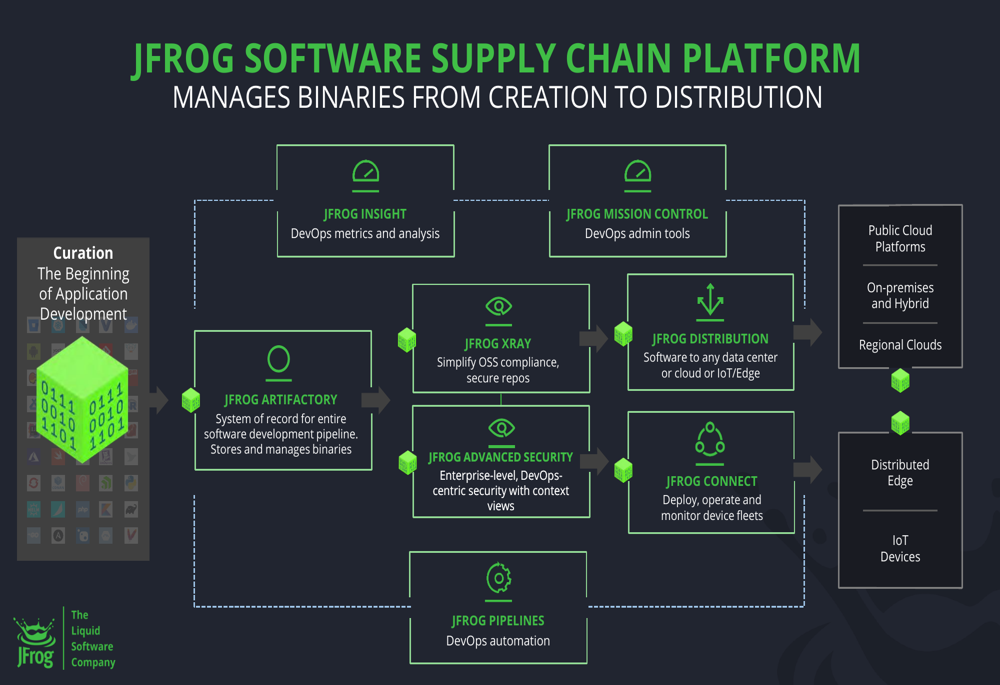

JFrog’s presentation emphasized its comprehensive software supply chain platform, which includes components for artifact management, security, distribution, and device management. The platform’s architecture is designed to address the complexity of modern software development across multiple environments and technologies.

The following diagram illustrates JFrog’s integrated platform approach:

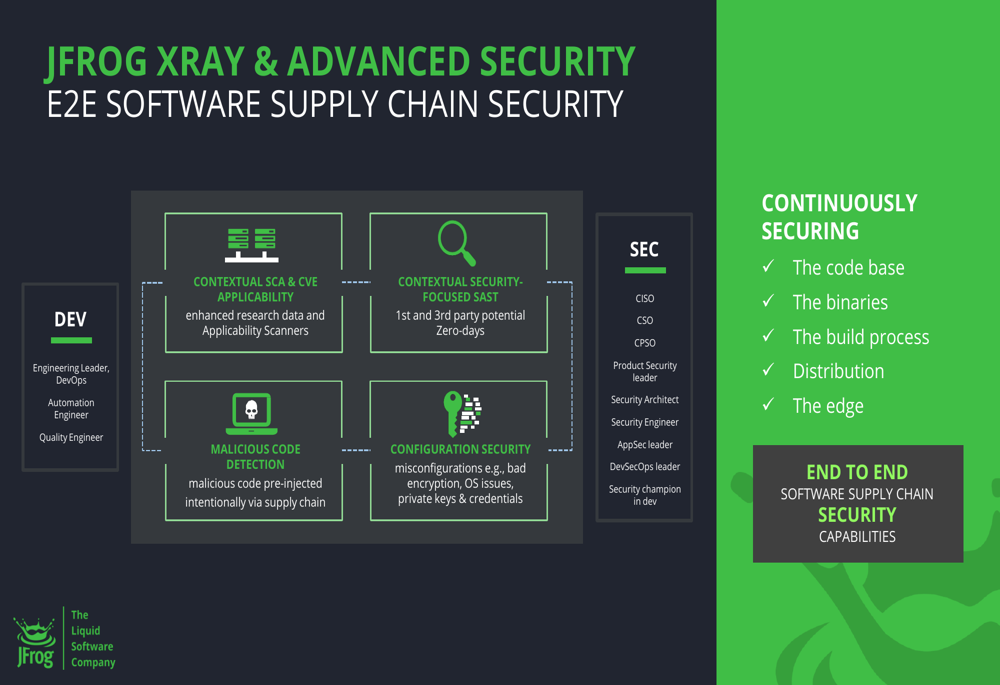

A key strategic focus for JFrog is security, with its Xray and Advanced Security products providing end-to-end protection for the software supply chain. The company is positioning these offerings to address growing concerns about software vulnerabilities and supply chain attacks.

As shown in the security capabilities diagram:

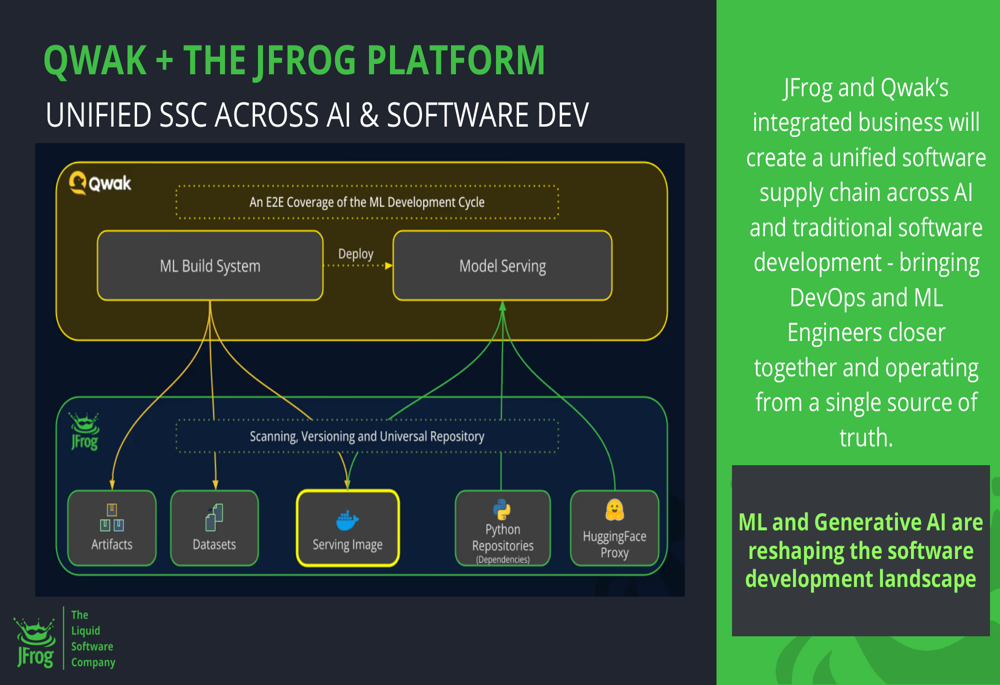

JFrog has also expanded into the Machine Learning Operations (MLOps) space, recognizing the increasing integration of AI and ML into software applications. The company recently acquired Qwak to strengthen its capabilities in this area, creating what it calls a "unified software supply chain across AI and traditional software development."

The following slide illustrates the integration of Qwak with the JFrog platform:

Competitive Industry Position

JFrog positions itself as a category-defining software company with unique advantages in addressing enterprise-scale software supply chain challenges. The company’s competitive differentiation includes its focus on binaries (compiled software components) as the foundation of software delivery, its flexible deployment options, and its comprehensive platform approach.

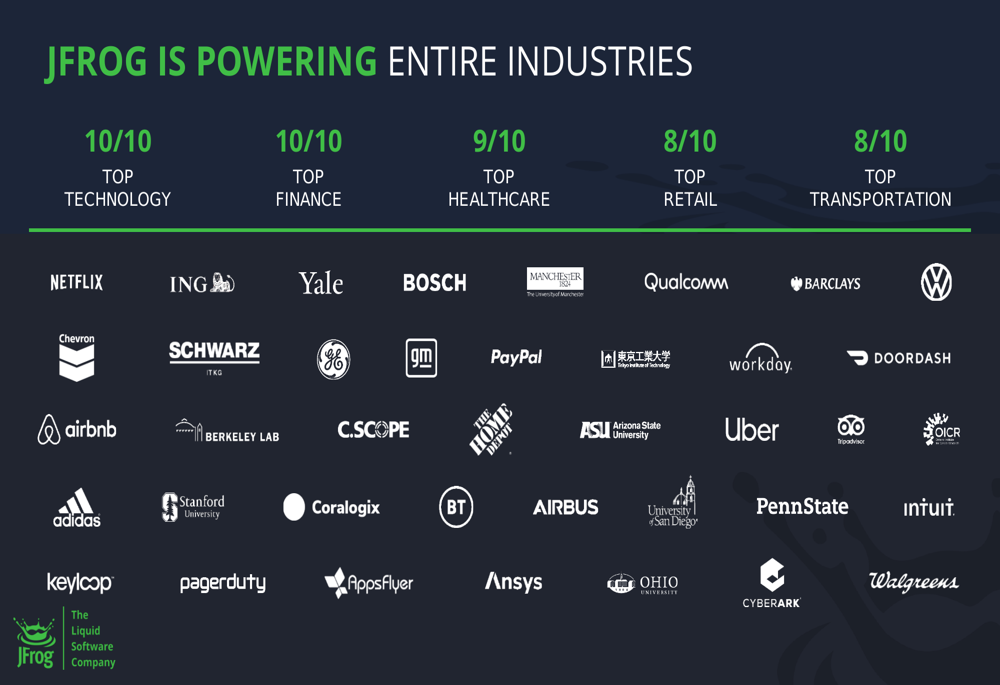

The company’s customer base spans multiple industries, with particularly strong penetration in technology, finance, and healthcare sectors. The following slide showcases JFrog’s customer reach:

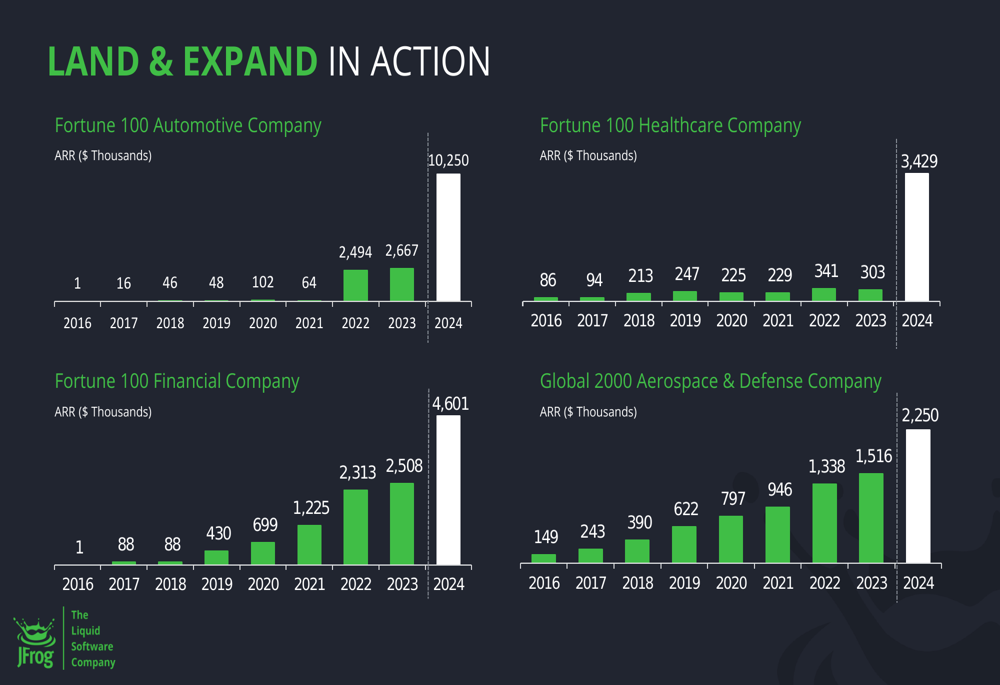

JFrog’s "land and expand" strategy has proven effective with enterprise customers, as demonstrated by several case studies of Fortune 100 companies that have significantly increased their annual recurring revenue (ARR) with JFrog over time.

As illustrated in these customer expansion examples:

The company’s multi-product strategy is also showing success, with 96% of customers adopting multiple JFrog products. Enterprise Plus subscriptions, which include the company’s most comprehensive offerings, now account for 54.9% of revenue in Q1’25, up from 49% in Q1’24.

Forward-Looking Statements

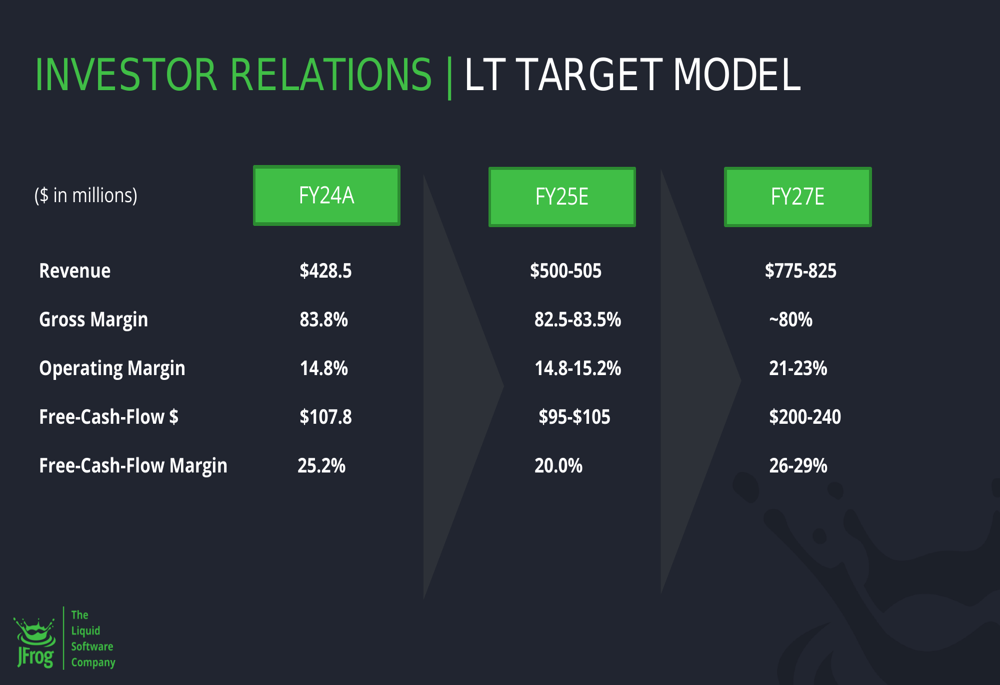

JFrog presented a long-term target model projecting growth to $775-825 million in revenue by FY’27, with operating margins expanding to 21-23% and free cash flow reaching $200-240 million.

The following table outlines JFrog’s long-term financial targets:

While the presentation maintains an optimistic outlook, the recent earnings call indicated a more cautious stance for 2025, particularly regarding large-scale migration deals and security implementations. The company expects cloud revenue to continue growing at around 40% annually, though this may be partially offset by slower growth in self-managed subscriptions.

JFrog’s strategic focus remains on expanding within its existing customer base, acquiring new customers, and extending its technology leadership. The company’s efficient go-to-market strategy combines high-touch enterprise sales with organic adoption and community-driven growth.

As JFrog continues to execute on its vision of "Liquid Software," the company appears well-positioned to capitalize on the growing importance of secure, efficient software delivery pipelines in an increasingly software-defined world. However, investors should monitor the balance between cloud growth and margin pressure, as well as the company’s ability to maintain its high customer retention rates in a competitive market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.