Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

JOST Werke AG (ETR:JST) presented its second quarter and first half 2025 results on August 14, 2025, highlighting strong M&A-driven growth amid challenging market conditions. The company’s stock closed at €51.40 on August 13, up 1.38% ahead of the earnings presentation.

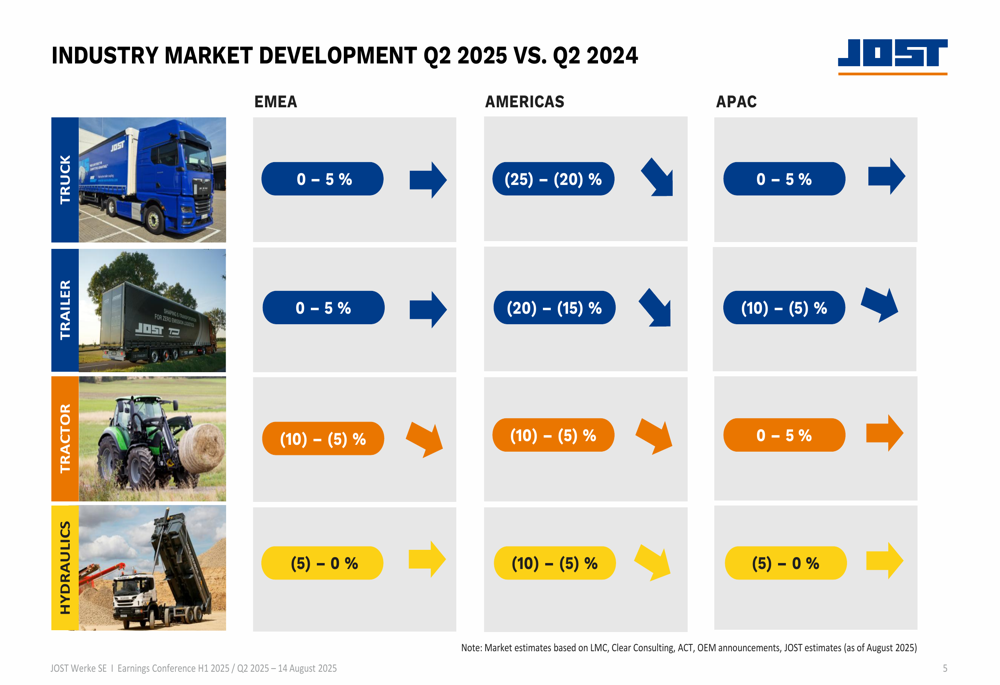

The global commercial vehicle and agricultural equipment markets showed mixed signals during Q2 2025, with EMEA stabilizing, Americas experiencing significant contraction, and APAC showing modest growth in select segments. JOST’s diversified business model across regions and applications has helped buffer against these varying market conditions.

As shown in the following industry market development chart:

Quarterly Performance Highlights

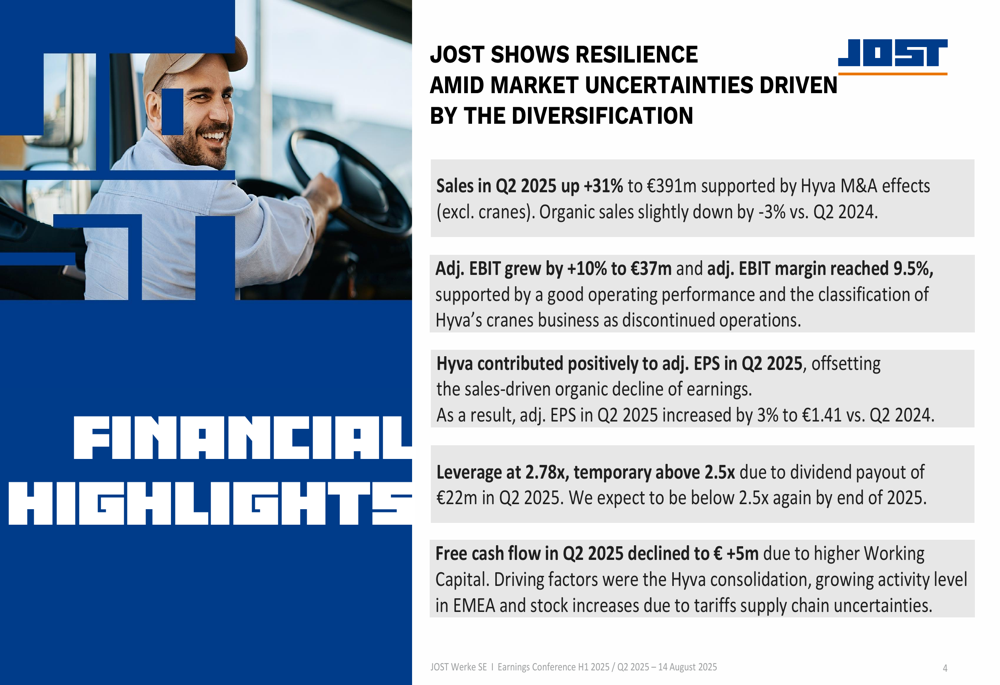

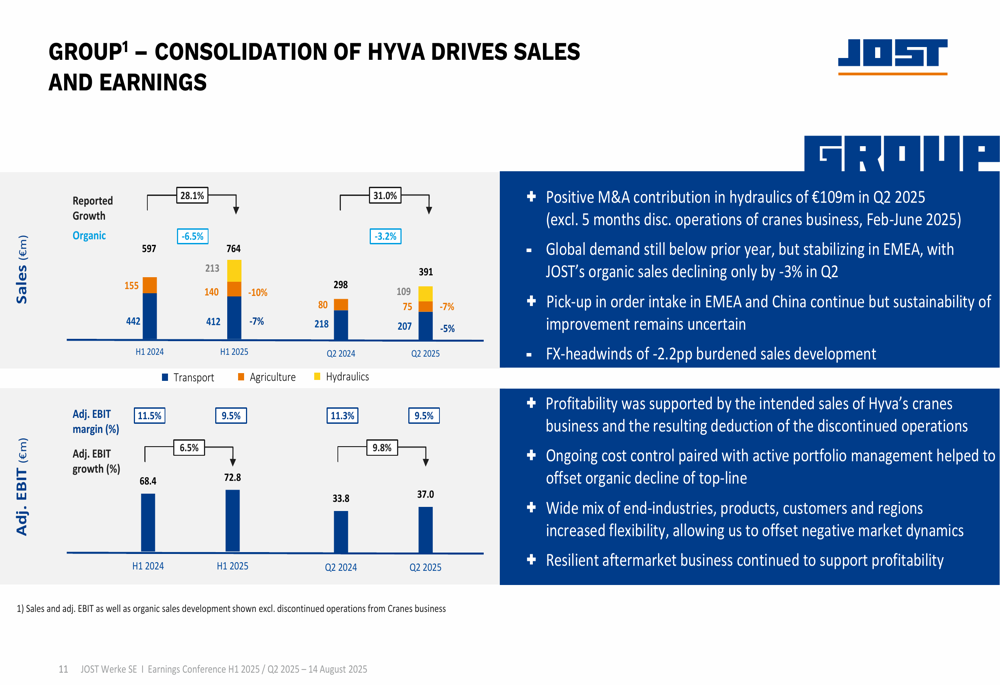

JOST reported Q2 2025 sales of €391 million, representing a 31% increase compared to Q2 2024, primarily driven by the Hyva acquisition. However, organic sales declined slightly by 3% year-over-year, showing some improvement from the 9% organic decline reported in Q1 2025.

Adjusted EBIT grew by 10% to €37 million, with an adjusted EBIT margin of 9.5%. This margin was supported by good operating performance and the classification of Hyva’s cranes business as discontinued operations. Adjusted earnings per share increased by 3% to €1.41 in Q2 2025, reversing the 3% decline seen in Q1.

The following chart illustrates the key financial highlights:

For the first half of 2025, JOST reported sales of €764 million, up from €597 million in H1 2024. Adjusted EBIT reached €72.8 million with a margin of 9.5%, compared to €68.4 million and 11.5% in H1 2024, indicating margin pressure despite absolute earnings growth.

Regional Performance Analysis

JOST’s performance varied significantly across regions, reflecting different market dynamics and the impact of the Hyva acquisition:

In EMEA, sales increased by 21% to reach €391 million in H1 2025, with organic growth of 3.7%. The region benefited from €25 million in M&A sales contribution from Hyva in Q2. Adjusted EBIT grew 5.8% to €10.9 million as market demand in both transport and agriculture segments stabilized.

The Americas region saw sales grow by 8% to €202 million in H1 2025, entirely driven by Hyva’s €24 million contribution, while organic sales declined by 11.1%. The adjusted EBIT margin contracted from 13.4% to 10.9%, reflecting challenging market conditions as truck and trailer demand fell by 20-25% amid tariff uncertainties.

APAC delivered the strongest growth, with sales more than doubling to €187 million in H1 2025 from €91 million in H1 2024, supported by a €60 million contribution from Hyva. Despite this impressive growth, the adjusted EBIT margin declined from 17.6% to 14.1% as the business mix shifted.

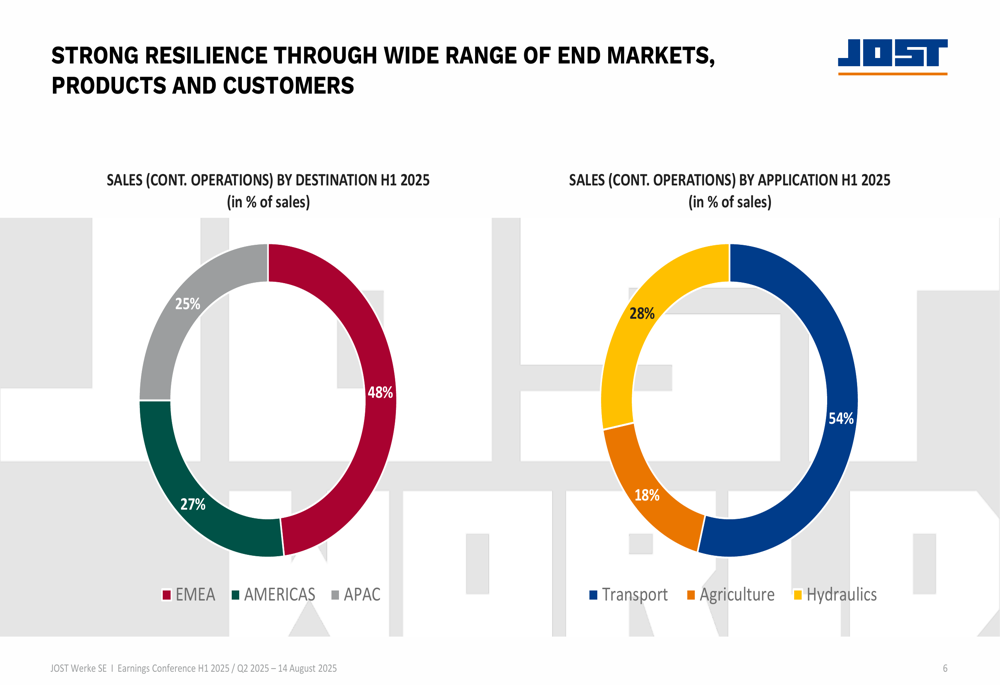

The company’s sales distribution highlights its geographic and application diversification:

Strategic Initiatives

A key strategic focus for JOST in Q2 2025 was the integration of Hyva, which management described as "fully on track" with the first synergies already implemented. The company prepared the exit of the non-core cranes business during Q2, with a sale and purchase agreement signed on August 11, 2025.

JOST also reported market share gains in the agricultural segment in APAC and South America, signing new long-term contracts with agricultural OEMs. This aligns with the company’s strategy to diversify beyond its traditional transport focus.

On the financial front, JOST successfully placed a promissory note loan of €320 million in Q2 2025, increasing its long-term loan maturity profile at what management described as "attractive conditions."

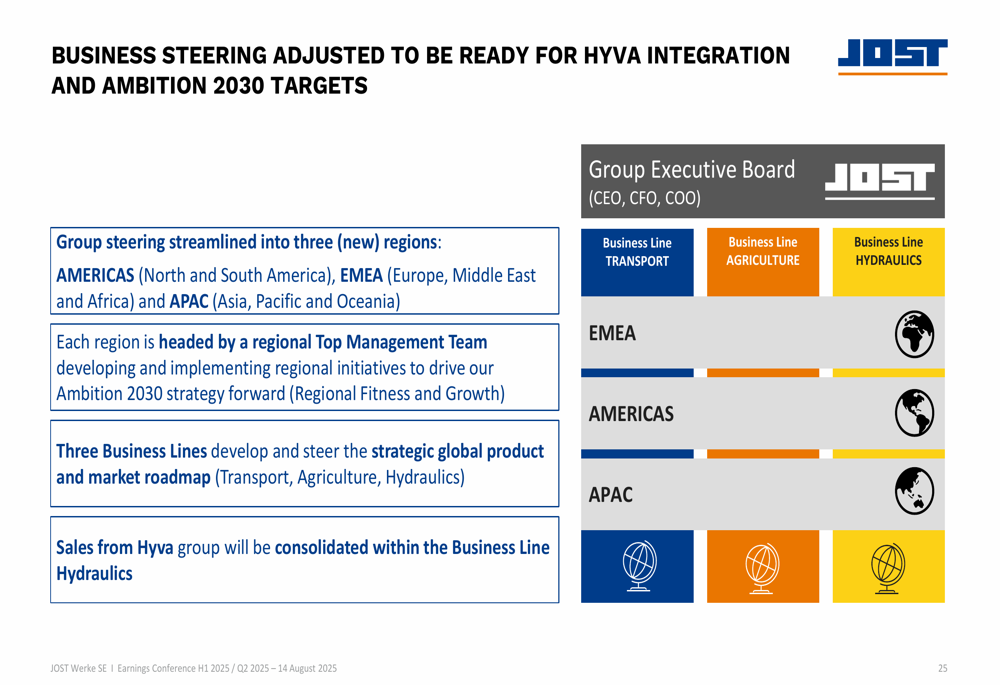

The company has adjusted its business steering structure to streamline operations into three regions:

Financial Position and Outlook

JOST’s leverage ratio increased to 2.78x as of June 30, 2025, temporarily exceeding the company’s 2.5x target due to the €22 million dividend payout in Q2. Management expects leverage to return below 2.5x by the end of 2025.

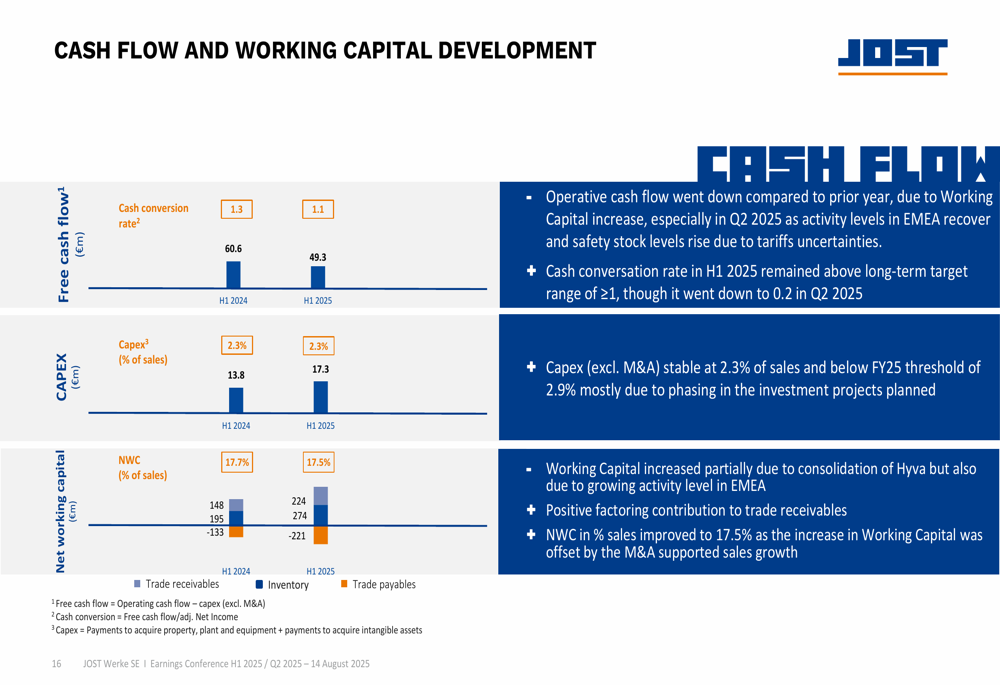

Free cash flow in Q2 2025 declined to €5 million due to higher working capital, driven by the Hyva consolidation, growing activity levels in EMEA, and inventory increases related to tariff and supply chain uncertainties.

The following chart illustrates the company’s cash flow and working capital development:

JOST’s equity ratio decreased significantly from 40.4% at the end of 2024 to 21.3% as of June 30, 2025, while ROCE declined from 17.1% to 13% over the same period, reflecting the financial impact of the Hyva acquisition.

Despite these challenges, JOST confirmed its outlook for fiscal year 2025, projecting:

Management remains confident in the company’s resilience and growth prospects, highlighting the potential upside in EMEA and agriculture markets. The company expects market conditions to vary by region, with EMEA showing modest growth, Americas continuing to face headwinds, and APAC offering growth opportunities, particularly in the agricultural segment.

As global markets navigate through uncertainties, JOST’s strategy of geographic and product diversification, complemented by strategic acquisitions, positions the company to weather market fluctuations while pursuing long-term growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.