ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

Kapsch TrafficCom, a provider of intelligent transportation systems, presented its financial year 2024/25 results on June 25, 2025, revealing a complex picture of operational challenges despite relatively stable revenue. The company faced significant pressure on profitability while continuing to strengthen its balance sheet position.

Executive Summary

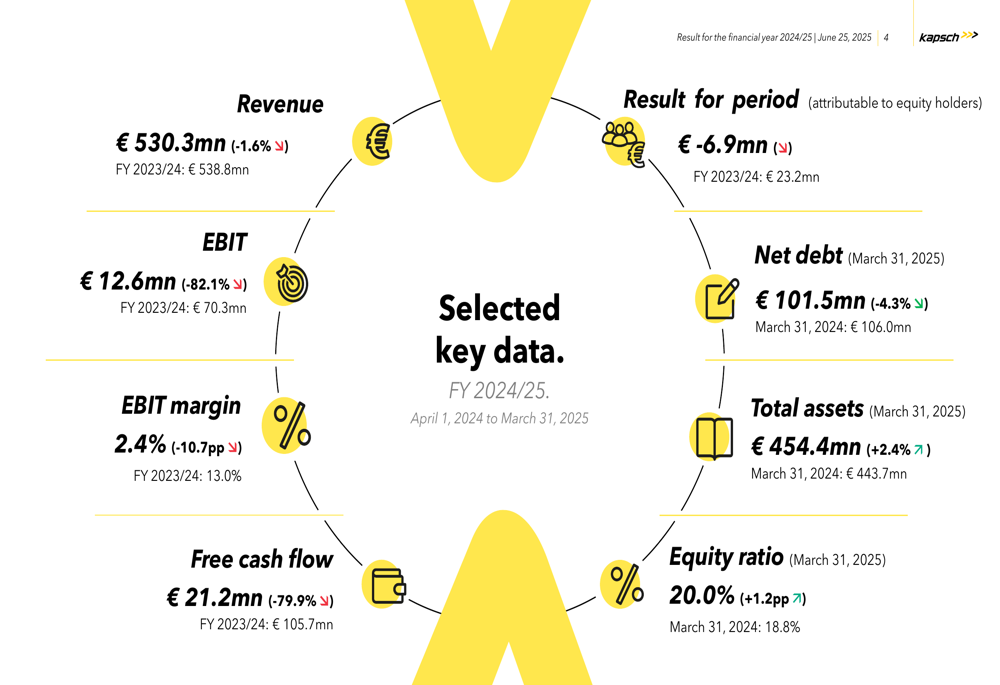

Kapsch TrafficCom reported revenue of €530.3 million for the financial year 2024/25, representing a slight decrease of 1.6% compared to the previous year. However, EBIT plummeted by 82.1% to €12.6 million, resulting in an EBIT margin of just 2.4%, down 10.7 percentage points year-over-year. The company attributed part of the revenue decline to deconsolidations during the period.

As shown in the following key data overview, the company posted a negative result attributable to equity holders of €6.9 million, a stark contrast to the €23.2 million profit recorded in the previous year:

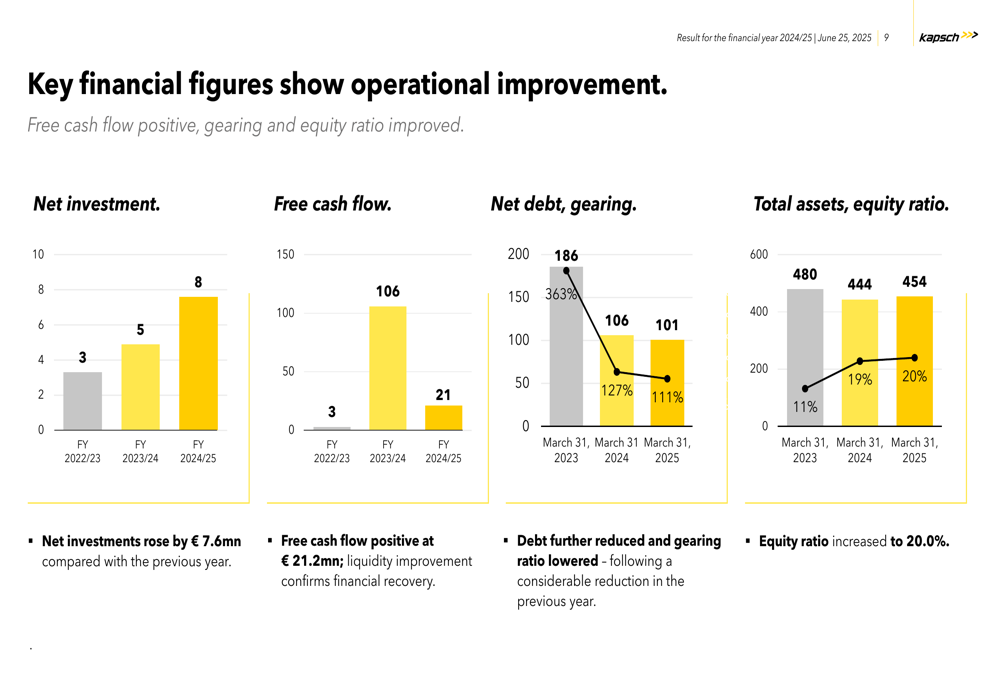

Despite these challenges, Kapsch TrafficCom continued to strengthen its balance sheet, reducing net debt to €101.5 million (down 4.3%) and improving its equity ratio to 20.0% (up 1.2 percentage points). The company maintained positive free cash flow of €21.2 million, though this represented a significant decline from the previous year’s €105.7 million.

Detailed Financial Analysis

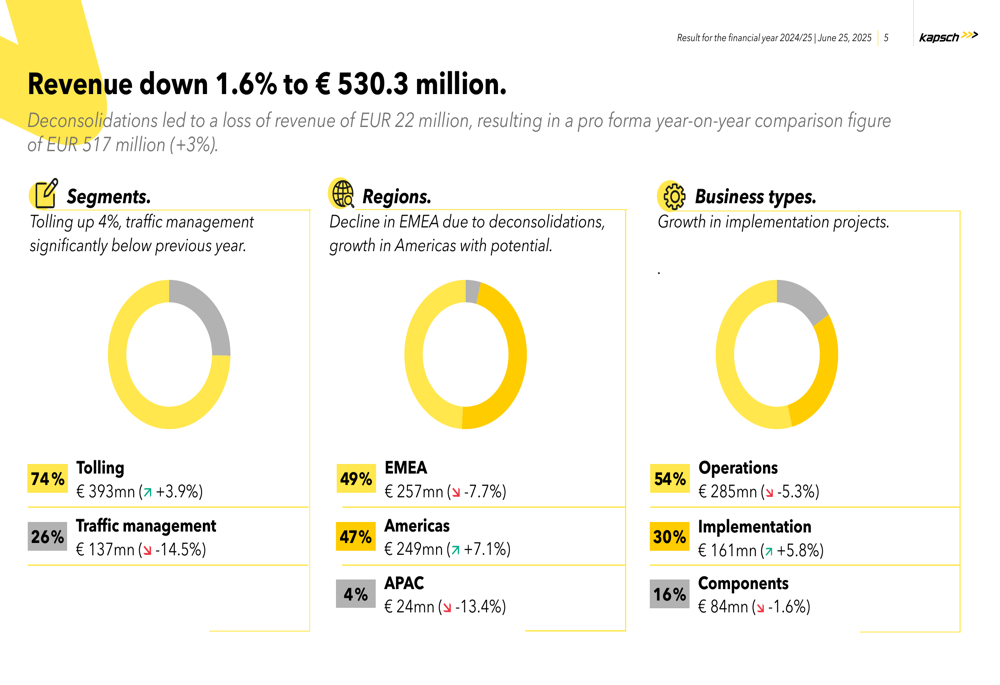

The company’s revenue breakdown reveals divergent performance across segments, regions, and business types. The tolling segment, which accounts for 74% of total revenue, grew by 3.9% to €393 million. In contrast, the traffic management segment declined by 14.5% to €137 million, representing 26% of total revenue.

The following chart illustrates this revenue distribution across segments, regions, and business types:

From a regional perspective, the Americas showed growth of 7.1% to €249 million (47% of total revenue), while the EMEA region, which accounts for 49% of revenue, declined by 7.7% to €257 million. The APAC region, representing just 4% of revenue, saw a decrease of 13.4% to €24 million.

Operations remained the largest business type at 54% of revenue, growing by 5.3% to €285 million. Implementation projects contributed 30% of revenue, increasing by 5.8% to €161 million, while components sales declined slightly by 1.6% to €84 million (16% of total revenue).

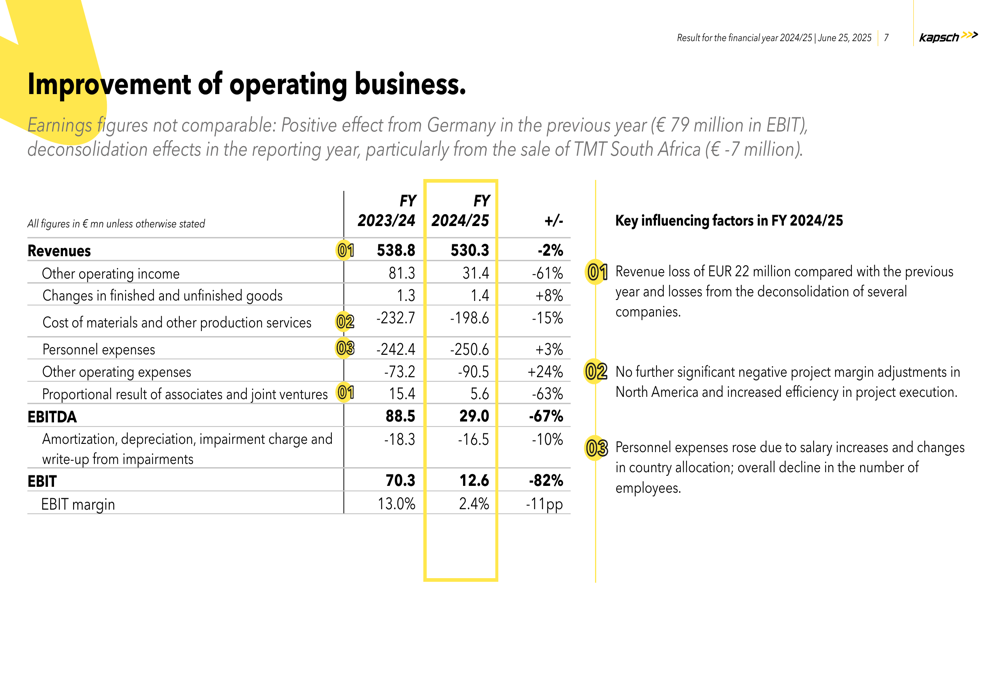

The company’s operating business showed mixed results, with significant changes in various cost categories:

Other operating income decreased dramatically by 61% to €31.4 million, while personnel expenses increased by 3% to €250.6 million despite an overall decline in the number of employees. Other operating expenses rose by 24% to €90.5 million. These factors, combined with a 63% decrease in the proportional result of associates and joint ventures, contributed to the steep decline in EBITDA and EBIT.

Segment Performance

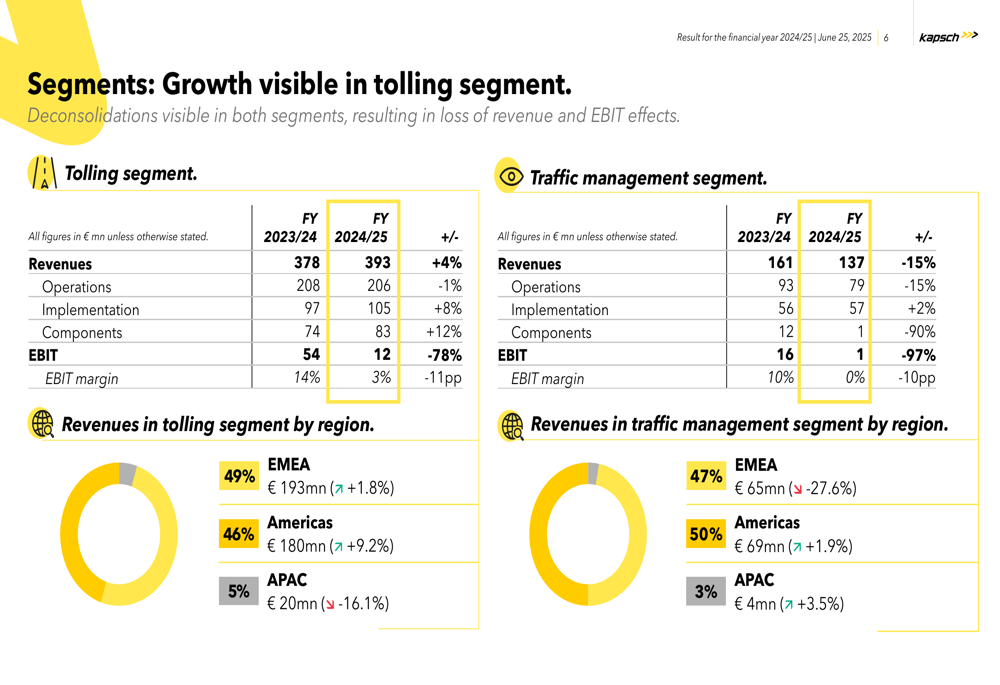

A closer examination of segment performance reveals that while the tolling segment achieved revenue growth, its profitability suffered significantly:

The tolling segment’s EBIT collapsed by 78% to €12 million, with the EBIT margin shrinking from 14% to just 3%. Within this segment, components sales showed the strongest growth at 12%, followed by implementation at 8%, while operations slightly declined by 1%.

The traffic management segment faced even greater challenges, with EBIT plummeting by 97% to just €1 million, effectively eliminating its profit margin. The segment’s revenue decline of 15% was driven primarily by a 90% drop in components sales and a 15% decrease in operations revenue, while implementation revenue grew modestly by 2%.

Balance Sheet Improvements

Despite the operational challenges, Kapsch TrafficCom continued to strengthen its financial position:

The company’s net debt decreased to €101.5 million as of March 31, 2025, down from €106.0 million a year earlier and €186 million two years ago. This improvement reduced the gearing ratio to 111%, compared to 127% in the previous year and 363% two years prior.

The equity ratio improved to 20.0%, continuing the positive trend from 18.8% a year earlier and just 11% two years ago. Free cash flow remained positive at €21.2 million, though significantly lower than the previous year’s €105.7 million, which had benefited from one-time effects.

Forward-Looking Statements

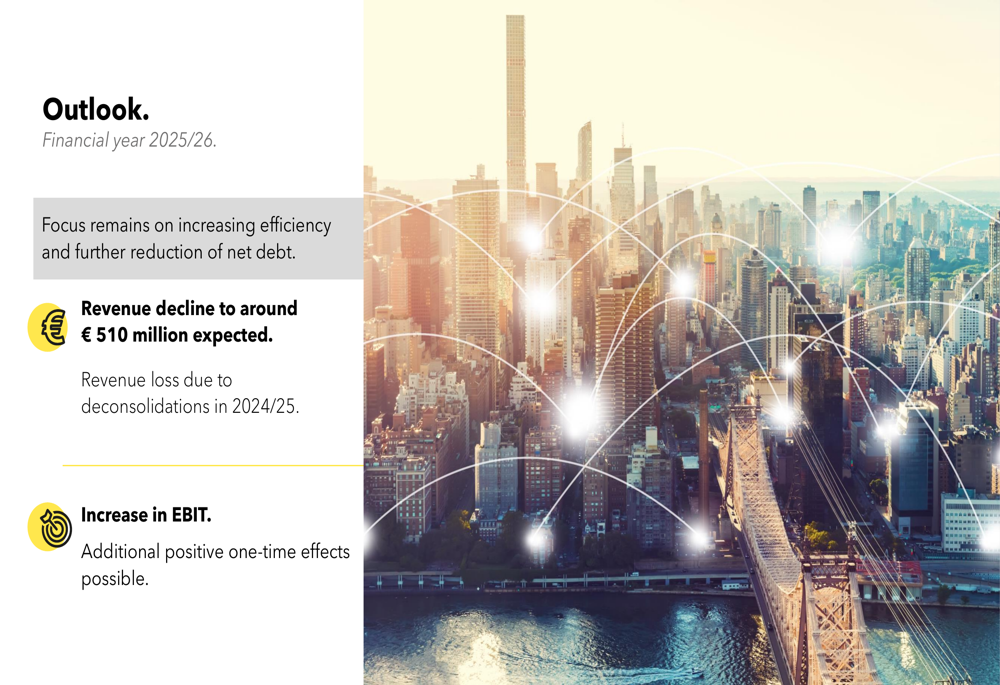

Looking ahead to the 2025/26 financial year, Kapsch TrafficCom expects further revenue decline to approximately €510 million, primarily due to deconsolidations in 2024/25:

Despite the projected revenue decrease, the company anticipates an increase in EBIT, with additional positive one-time effects possible. Management emphasized that the focus will remain on increasing operational efficiency and further reducing net debt.

The company’s financial recovery appears to be continuing, albeit at a slower pace than in the previous year, with balance sheet improvements providing a foundation for potential future growth despite the current profitability challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.