Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

KB Home (NYSE:KBH) released its second quarter 2025 investor presentation on June 23, revealing how the homebuilder is navigating a challenging housing market characterized by elevated mortgage rates and softening demand. Following the earnings announcement, KB Home’s stock rose 3.03% in after-hours trading to $51.97, suggesting investors were encouraged by the company’s ability to maintain profitability despite industry headwinds.

The presentation highlighted KB Home’s continued reliance on its Built to Order (BTO) business model as a key differentiator in the competitive homebuilding landscape. This strategy, which allows buyers to customize their homes, has helped the company maintain relatively stable absorption rates compared to peers, even as overall market activity has slowed.

Quarterly Performance Highlights

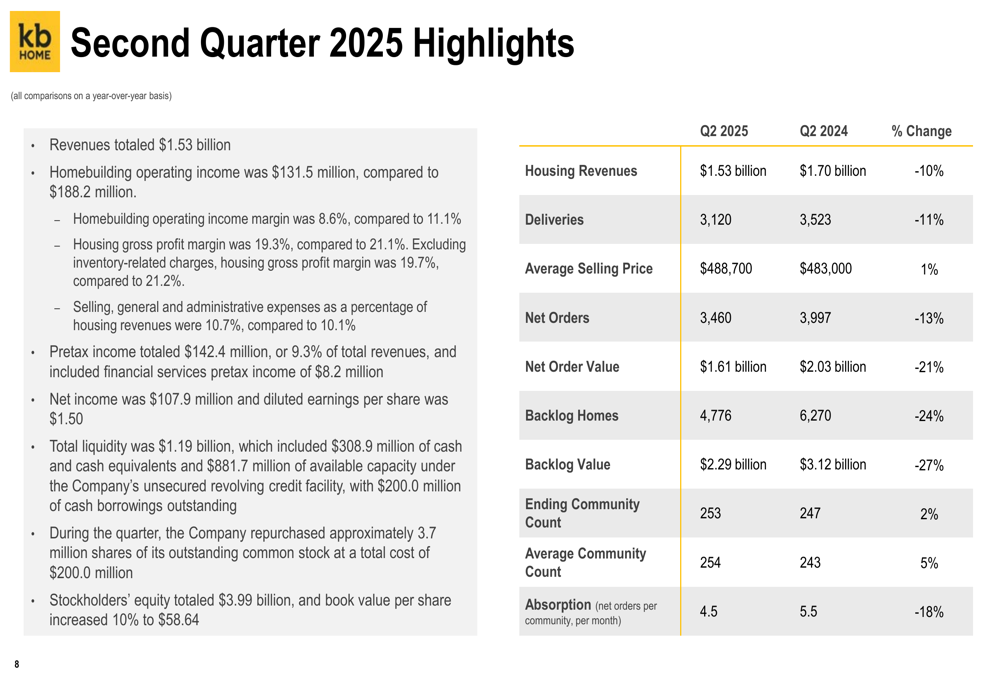

KB Home reported mixed financial results for Q2 2025, with several key metrics showing year-over-year declines. Housing revenues fell 10% to $1.53 billion, while home deliveries decreased 11% to 3,120 units. The company’s average selling price increased slightly by 1% to $488,700.

As shown in the following comprehensive financial overview from the presentation:

Net orders declined 13% to 3,460, while net order value fell more significantly by 21% to $1.61 billion. The company’s backlog also contracted, with backlog homes down 24% to 4,776 and backlog value down 27% to $2.29 billion compared to Q2 2024.

Profitability metrics showed compression, with homebuilding operating income margin decreasing to 9.0% from 11.1% in the same period last year. Housing gross profit margin declined to 19.3% (19.7% adjusted) from 21.1% (21.2% adjusted) in Q2 2024. Meanwhile, SG&A expenses as a percentage of housing revenues increased to 10.7% from 10.1% a year earlier.

Despite these challenges, KB Home’s earnings per share of $1.50 exceeded analyst expectations of $1.46, representing a 2.74% positive surprise according to the earnings report.

Business Model & Competitive Positioning

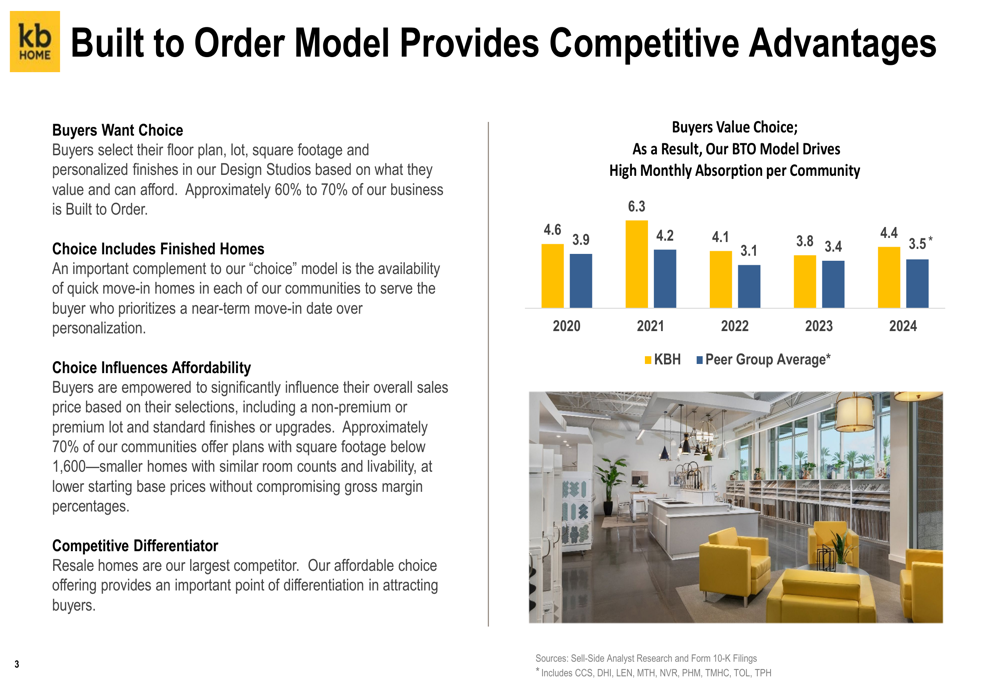

KB Home’s Built to Order model, which accounts for 60-70% of its sales, continues to be a cornerstone of its competitive strategy. This approach allows buyers to select their floor plan, lot, square footage, and personalized finishes, providing a level of customization that differentiates KB Home from many competitors.

The following slide illustrates how this model has helped KB Home maintain higher absorption rates compared to peers:

The company’s customer base remains diversified, with first-time homebuyers representing 50% of deliveries in Q2 2025. First move-up buyers accounted for 24%, while active adults and second move-up buyers represented 15% and 11%, respectively. This balanced customer mix helps KB Home navigate different segments of the housing market.

KB Home’s geographic footprint spans four regions: West Coast (California, Idaho, Washington), Southwest (Arizona, Nevada), Central (Colorado, Texas), and Southeast (Florida, North Carolina). The West Coast region contributed the largest share of homebuilding revenues at 43%, followed by Southwest (21%), Central (19%), and Southeast (17%).

Strategic Initiatives

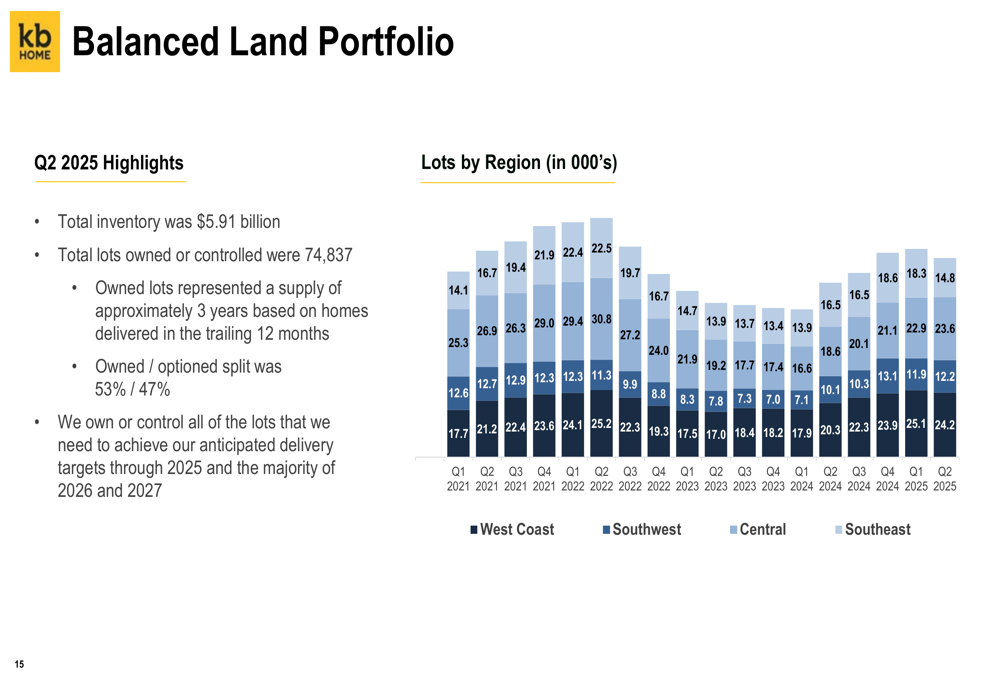

KB Home’s land strategy remains focused on maintaining a balanced portfolio that provides flexibility while securing future growth opportunities. As of Q2 2025, the company owned or controlled 74,837 lots, representing approximately three years of supply based on trailing 12-month deliveries.

The following chart illustrates the company’s balanced land portfolio strategy:

The company’s owned/optioned split stands at 53%/47%, providing a balance between land security and financial flexibility. KB Home noted that it owns or controls all lots needed to achieve delivery targets through 2025 and the majority of lots required for 2026 and 2027.

Sustainability continues to be a key strategic focus for KB Home, with the company highlighting its leadership in energy-efficient and water-conserving home construction. The presentation emphasized KB Home’s achievements in this area:

These sustainability initiatives not only appeal to environmentally conscious buyers but also provide tangible cost savings for homeowners through reduced utility bills, creating a compelling value proposition in a market where affordability remains a concern.

Financial Strength & Capital Allocation

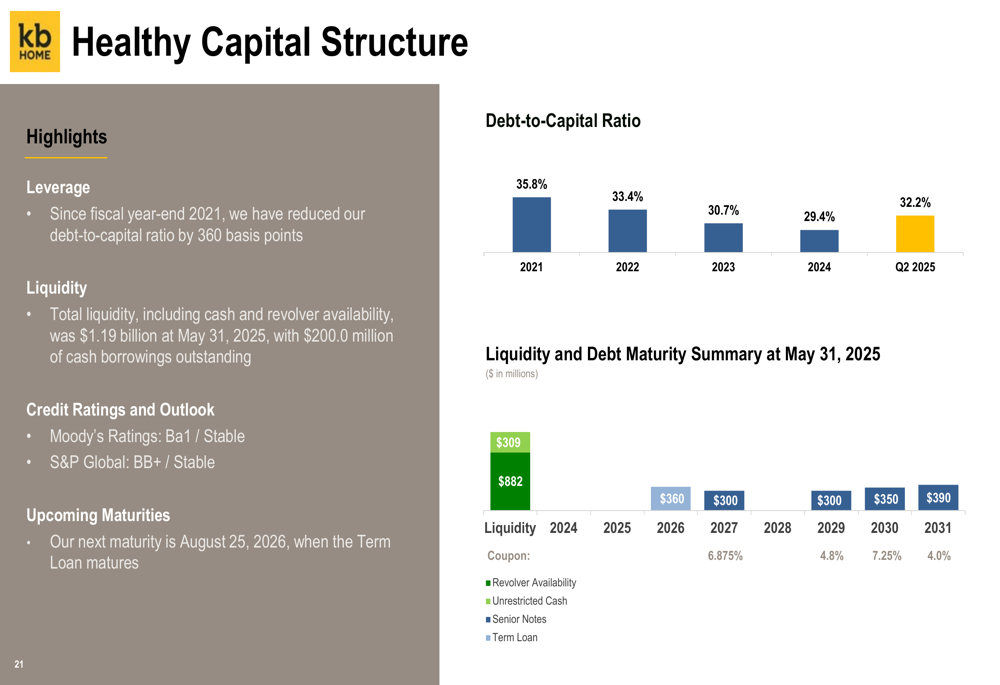

Despite the challenging market environment, KB Home has maintained a strong financial position. The company reported total liquidity of $1.19 billion as of May 31, 2025, and has continued to reduce its debt-to-capital ratio, which stood at 32.2% in Q2 2025, down from 35.8% in 2021.

The following slide illustrates KB Home’s capital structure and debt maturity profile:

KB Home has demonstrated a consistent commitment to returning capital to shareholders through share repurchases. The company has a $1 billion authorization approved in April 2024 and repurchased $200 million in shares during Q2 2025.

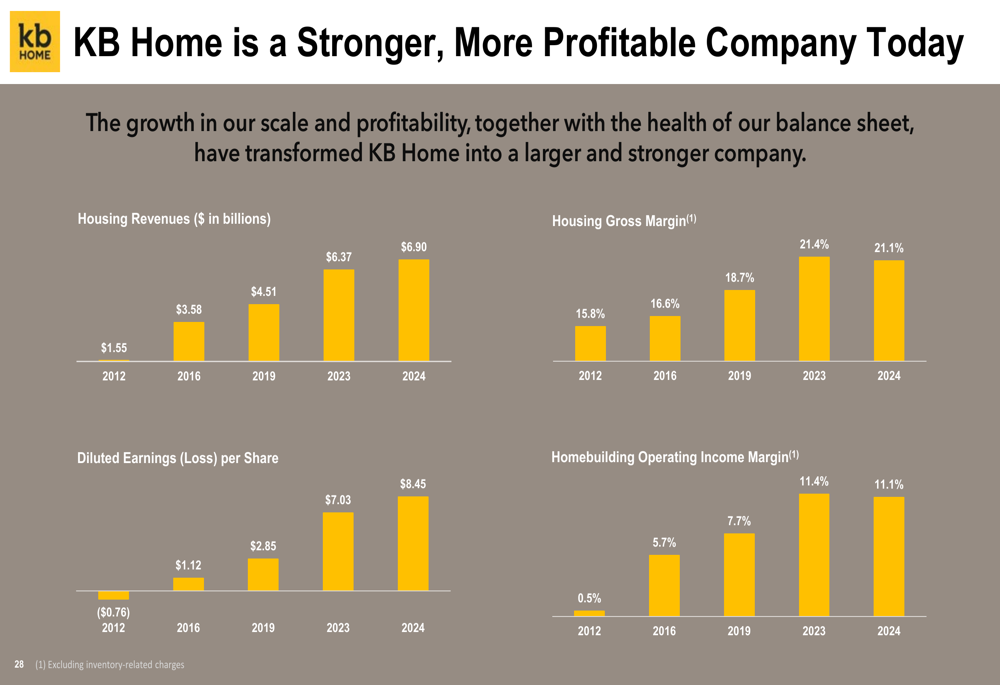

The long-term financial improvement of KB Home is evident in the following chart, which shows key metrics from 2012 to 2024:

This long-term perspective highlights how KB Home has transformed into a stronger, more profitable company over the past decade, with significant improvements in housing revenues, gross margins, and earnings per share.

Forward-Looking Statements

Looking ahead, KB Home revised its fiscal year 2025 housing revenue guidance to $6.3-$6.5 billion, with expected deliveries of approximately 13,200 homes. For the third quarter, the company projects housing revenues between $1.5 and $1.7 billion, with an average selling price ranging from $480,000 to $490,000.

The company remains focused on its core strengths, as summarized in this compelling overview:

Management expressed confidence in KB Home’s positioning despite market challenges. CEO Jeff Mezger stated, "We believe we are taking the right steps in the current market environment," emphasizing the company’s strategic focus on value delivery and transparency.

While KB Home faces headwinds from low consumer confidence and elevated mortgage rates, its Built to Order model, geographic diversification, and strong financial position provide resilience as it navigates the current housing market cycle. The company’s continued focus on sustainability and customer satisfaction further strengthens its competitive positioning for long-term growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.