Morgan Stanley again adjusts its Fed forecast, now sees 4 cuts in 2026

Introduction & Market Context

Kelly Services (NYSE:NASDAQ:KELYA) presented its first-quarter 2025 financial results on May 8, 2025, revealing a significant revenue boost from its Motion Recruitment Partners (MRP) acquisition but a substantial decline in earnings. The staffing company’s stock has already reacted negatively to the results, with premarket trading showing an 11.24% drop to $10.11, following a previous close of $11.39.

The Q1 2025 results mark a stark reversal from the company’s strong Q4 2024 performance, when Kelly Services beat analyst expectations with an EPS of $0.82 and saw its stock surge by 8.35%. The current quarter’s results reflect both the impact of the MRP acquisition completed on May 31, 2024, and ongoing challenges in the macroeconomic environment.

Quarterly Performance Highlights

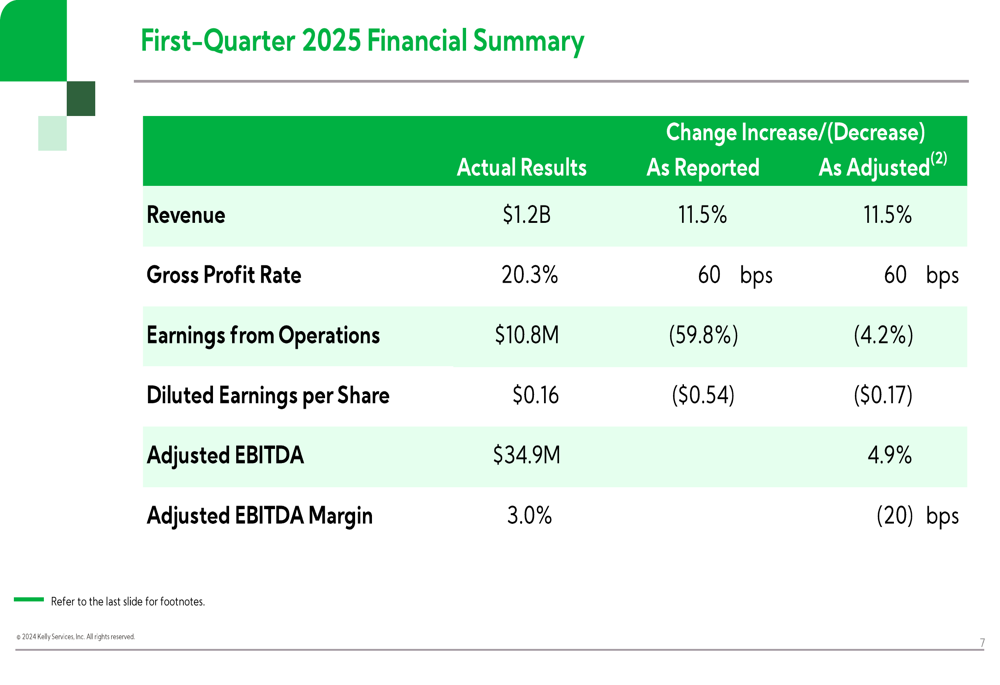

Kelly Services reported Q1 2025 revenue of $1.2 billion, representing an 11.5% increase on a reported basis compared to the same period last year. However, organic revenue growth was minimal at just 0.2%, including a 0.8% reduction due to U.S. federal government contracts.

As shown in the following financial summary, earnings metrics declined significantly year-over-year:

The company’s earnings from operations fell 59.8% as reported to $10.8 million, while diluted earnings per share dropped to $0.16, a $0.54 decrease from Q1 2024. On an adjusted basis, EPS was $0.39, still down $0.17 from the prior year. Adjusted EBITDA increased by 4.9% to $34.9 million, though the adjusted EBITDA margin contracted by 20 basis points to 3.0%.

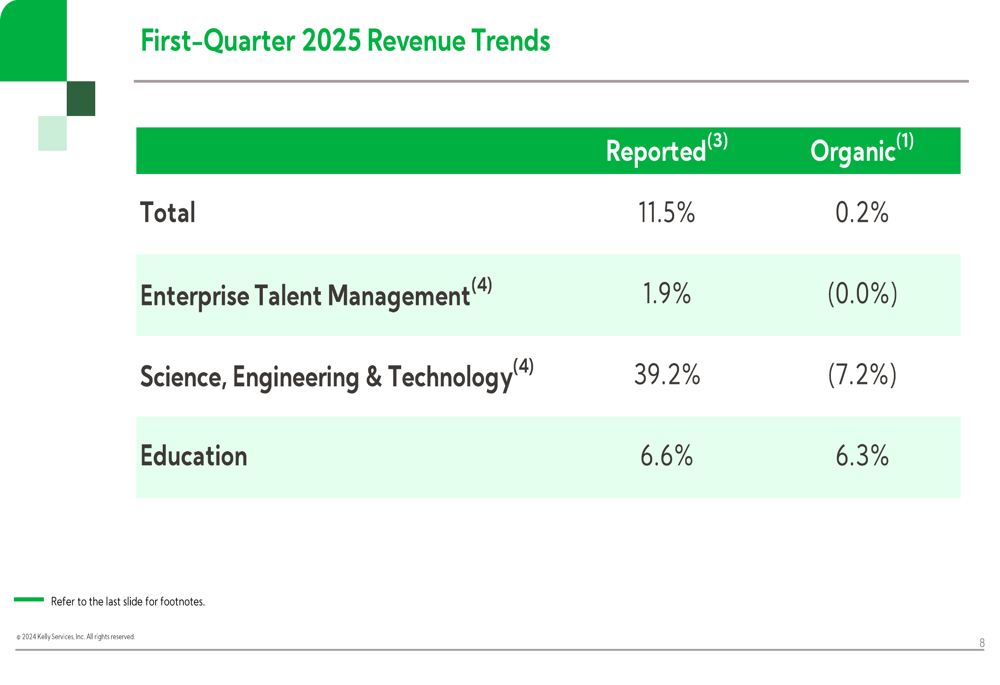

The revenue trends across Kelly’s business segments reveal varying performance:

The Science, Engineering & Technology (SET) segment showed the strongest reported growth at 39.2%, primarily due to the MRP acquisition, though organic revenue in this segment declined by 7.2%. The Education segment demonstrated the healthiest organic growth at 6.3%.

Detailed Financial Analysis

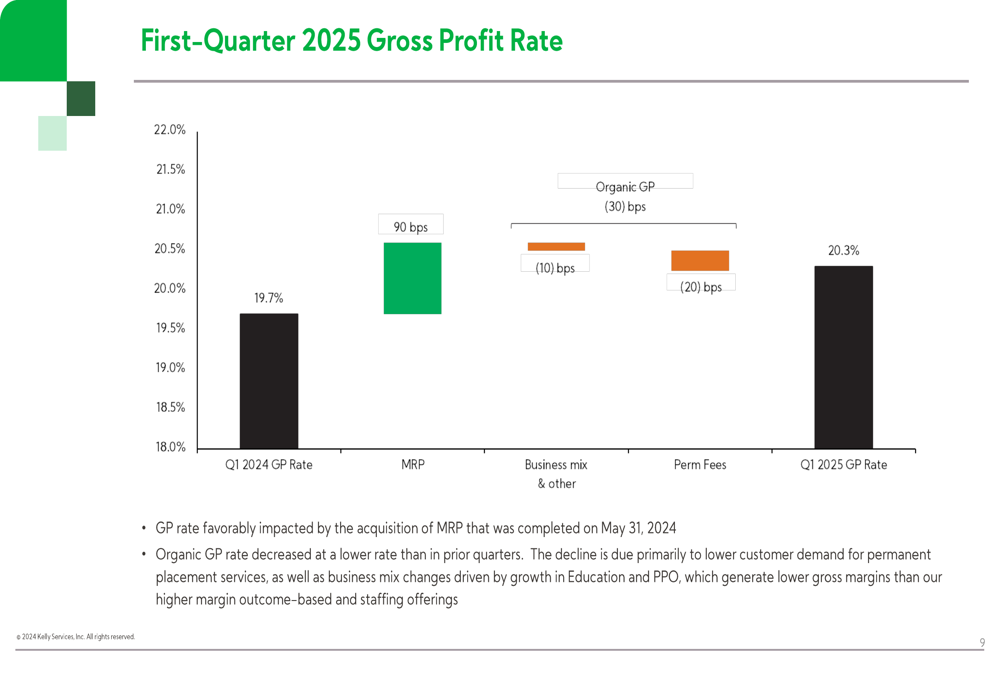

Kelly’s gross profit rate improved to 20.3%, a 60 basis point increase from Q1 2024. This improvement was largely driven by the MRP acquisition, which contributed 90 basis points to the gross profit rate, partially offset by declines in other areas.

The following chart illustrates the components affecting the gross profit rate:

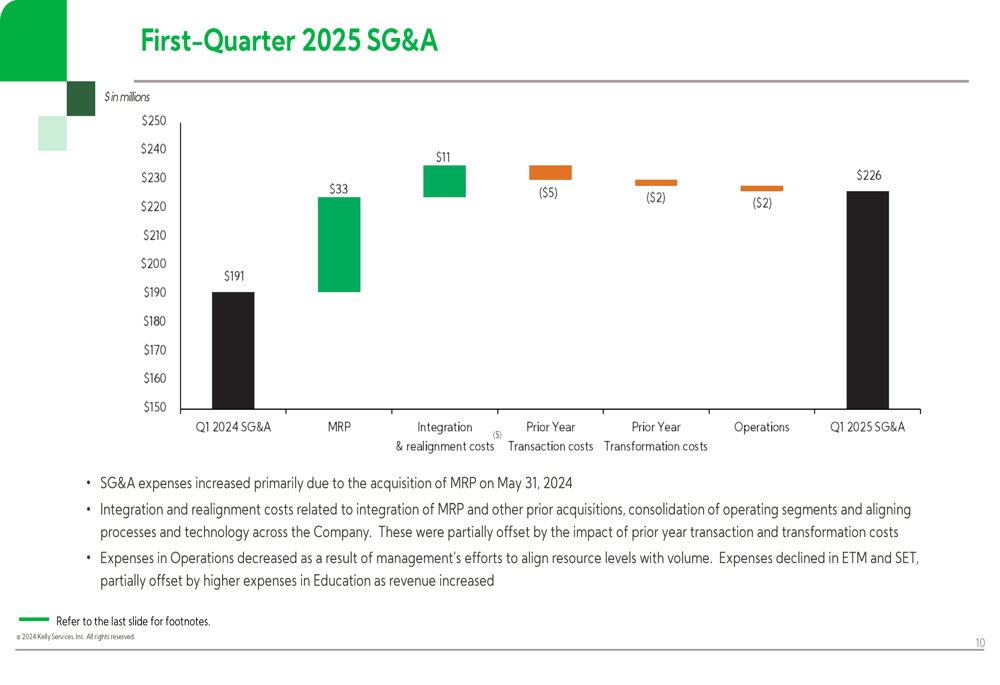

Selling, general, and administrative (SG&A) expenses increased substantially to $226 million, up from $191 million in Q1 2024. The MRP acquisition added $33 million to SG&A, while integration and realignment costs contributed an additional $11 million.

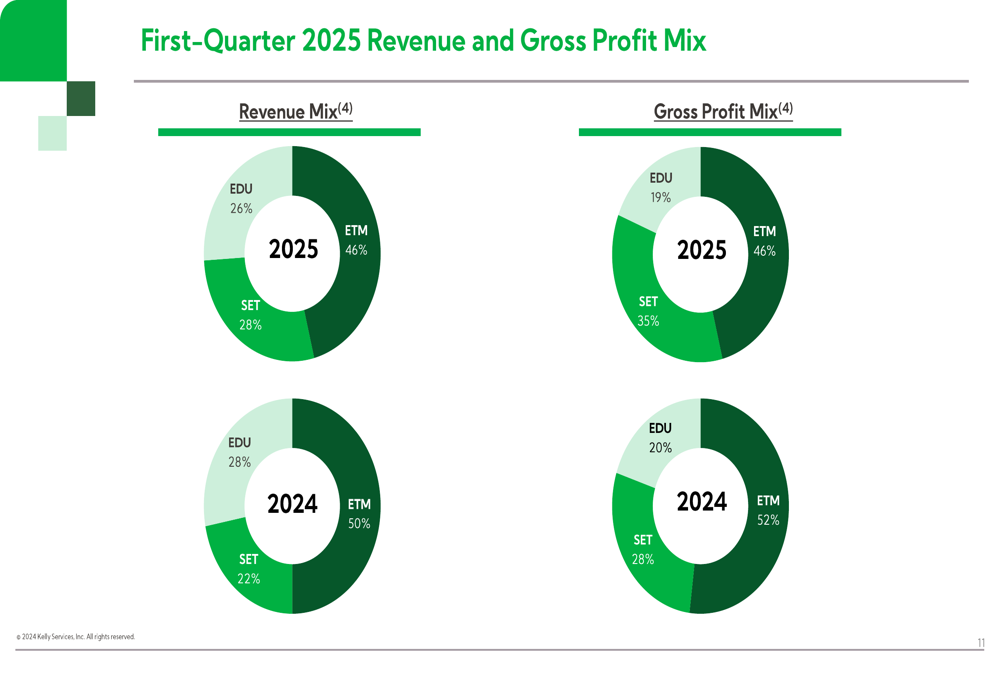

The company’s segment mix has shifted notably year-over-year, with SET growing its share of both revenue and gross profit:

This shift reflects Kelly’s strategic focus on higher-margin specialty businesses, particularly in the Science, Engineering, and Technology fields. The Enterprise Talent Management (ETM) segment’s share of revenue decreased from 50% to 46%, while Education maintained a relatively stable position.

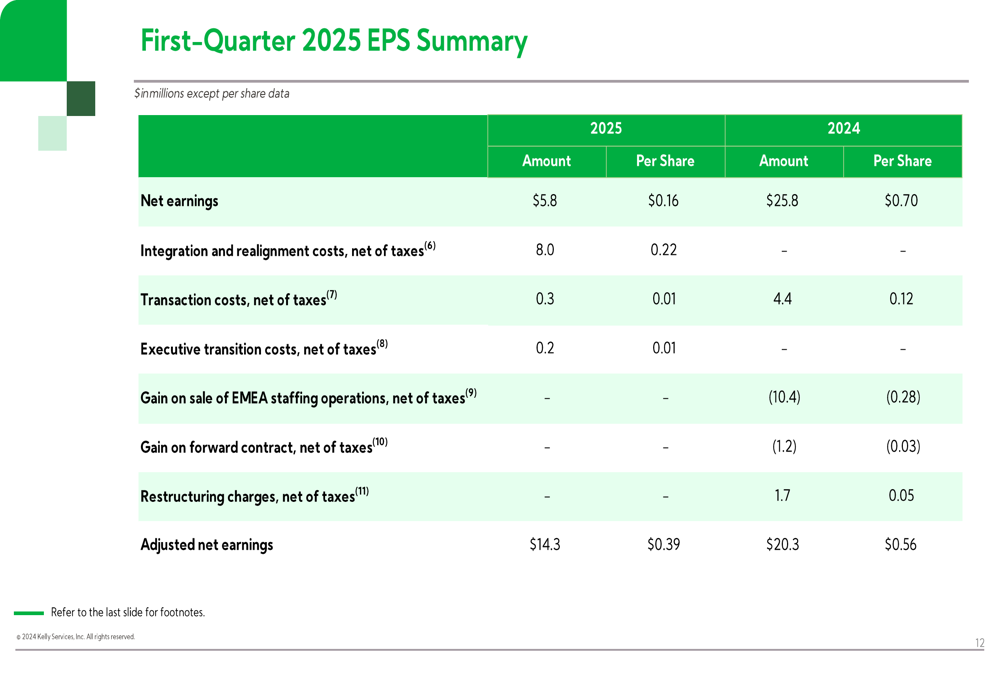

The company’s EPS performance breakdown shows the impact of various one-time items:

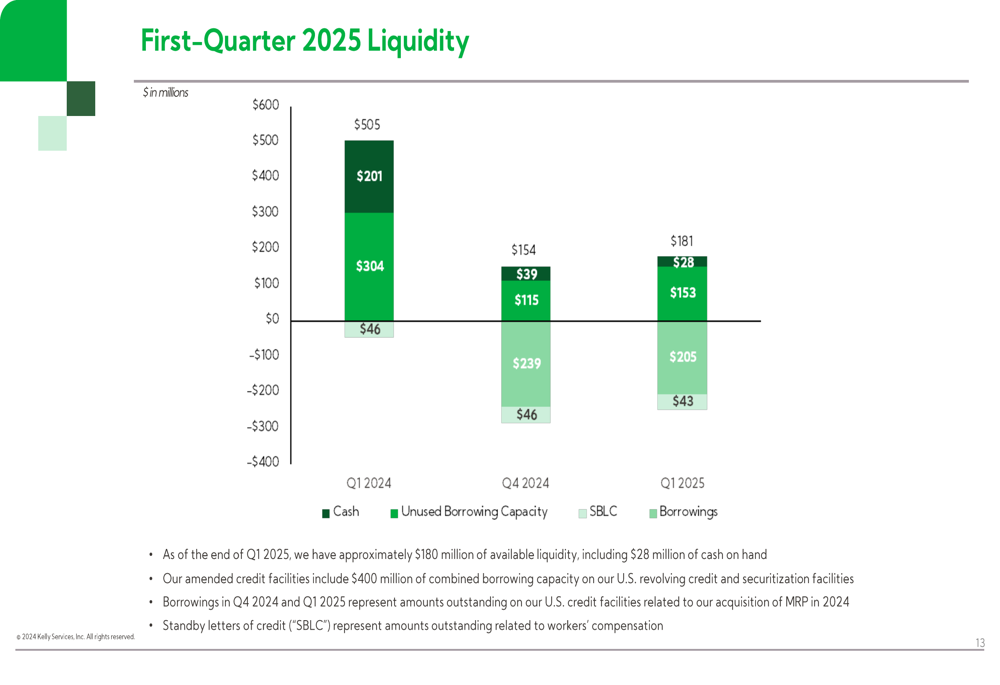

Kelly’s liquidity position has changed significantly over the past year, primarily due to the MRP acquisition. As of Q1 2025, the company reported approximately $180 million of available liquidity, including $28 million in cash on hand, with borrowings of $205 million related to the acquisition.

Strategic Initiatives

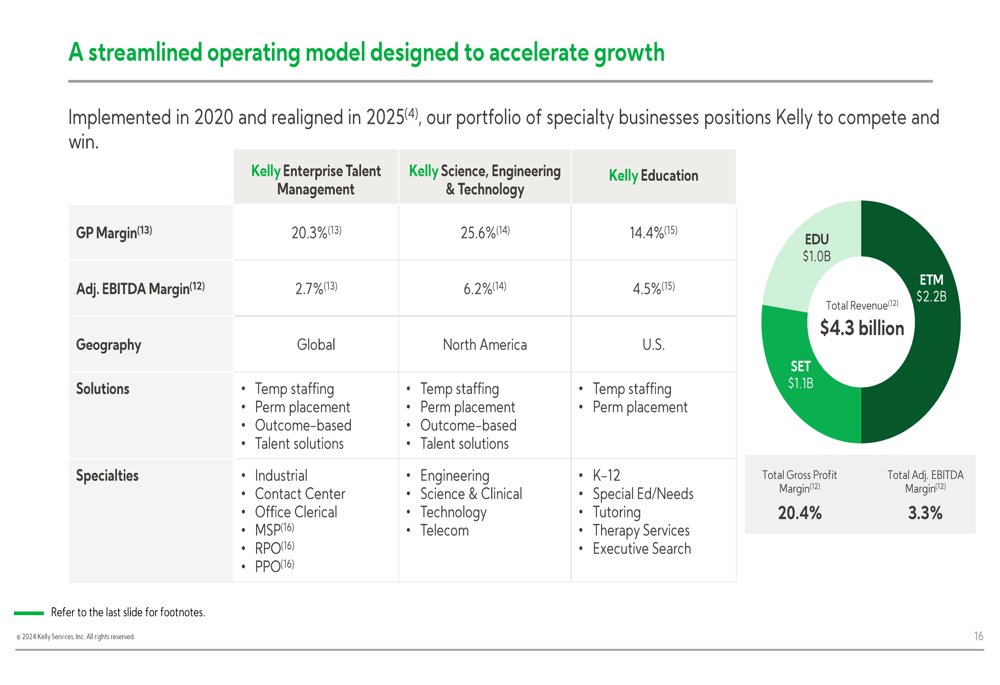

Kelly Services is executing a strategy to accelerate its focus on North American specialty staffing and global RPO/MSP (Recruitment Process Outsourcing/Managed Service Provider) businesses. The company has realigned its OCG and P&I segments and is working on integrating Motion Recruitment Partners.

The company’s streamlined operating model is designed to accelerate growth across different specialties:

Management emphasized maintaining focus on accelerating profitable growth through proactive expense management, specialization, and an inorganic strategy focused on high-margin SET and Education assets. The integration of MRP and other prior acquisitions, along with the consolidation of operating segments and alignment of processes and technology across the company, has resulted in significant integration and realignment costs in the quarter.

Forward-Looking Statements

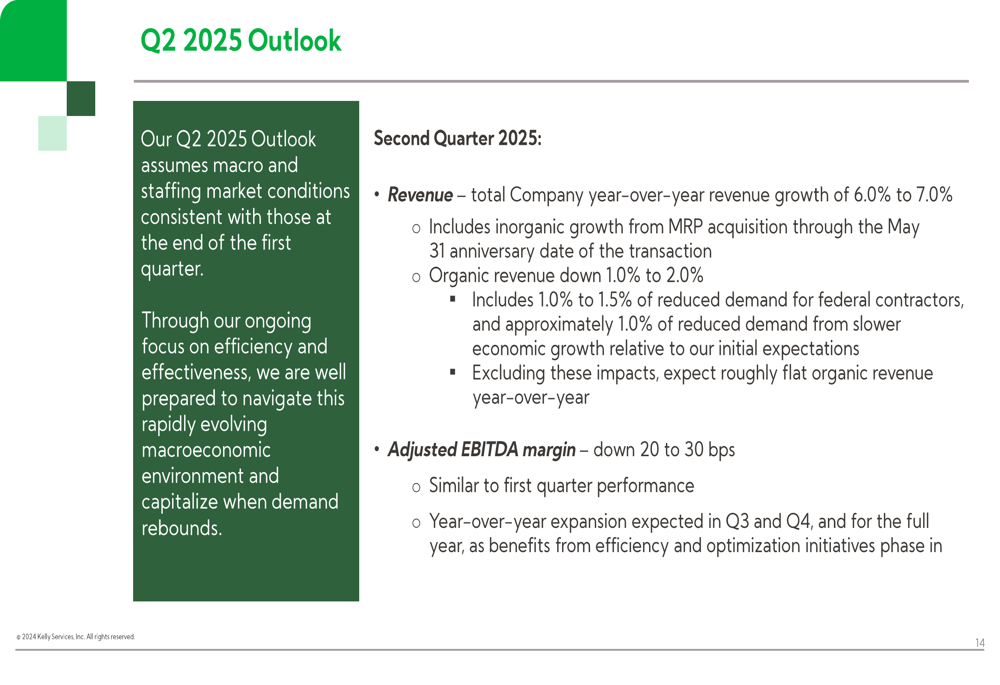

Kelly Services provided a cautious outlook for Q2 2025, projecting total company year-over-year revenue growth of 6.0% to 7.0%, including inorganic growth from the MRP acquisition. However, organic revenue is expected to decline by 1.0% to 2.0%, partially due to federal contractors and slower economic growth.

The adjusted EBITDA margin is expected to be down 20 to 30 basis points in Q2, similar to the first quarter. However, management anticipates year-over-year expansion in Q3 and Q4 as efficiency and optimization initiatives take effect.

This outlook stands in contrast to the company’s more optimistic projections following Q4 2024 results, when Kelly expected first-half 2025 revenue growth of approximately 10% and modest organic revenue growth. The current guidance suggests a more challenging operating environment than previously anticipated.

The company’s focus on integration and realignment appears to be a strategic necessity as it navigates through current market conditions, with expectations that these efforts will yield improvements in the latter half of 2025. Investors will be watching closely to see if Kelly can deliver on its projected second-half recovery while managing the substantial debt taken on for the MRP acquisition.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.