AbbVie, Novo get Berenberg boost while Lilly, Merck face downgrades

Introduction & Market Context

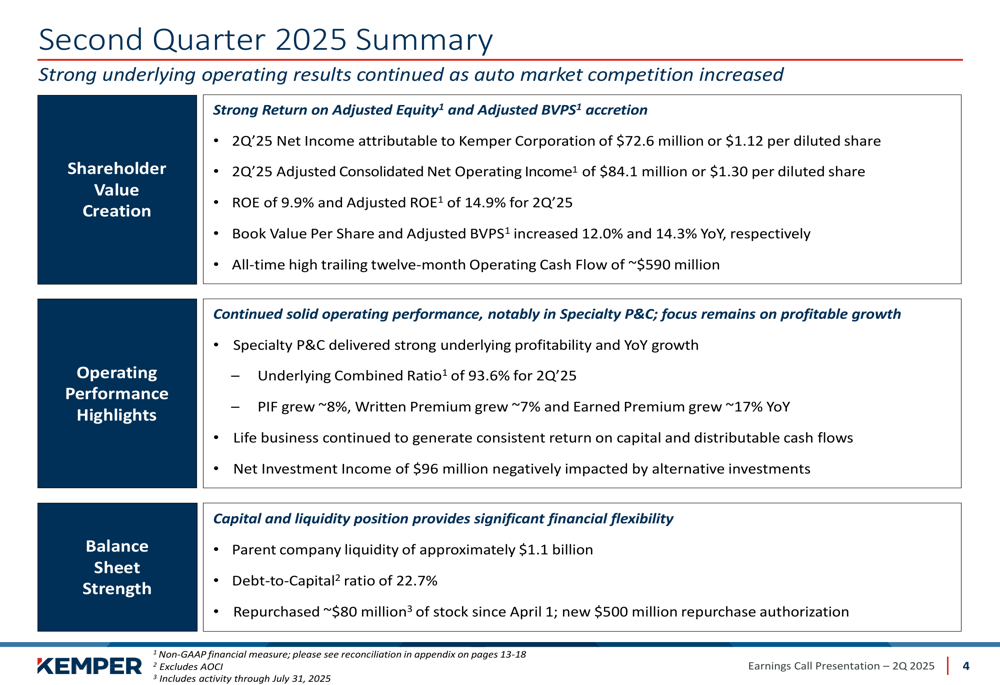

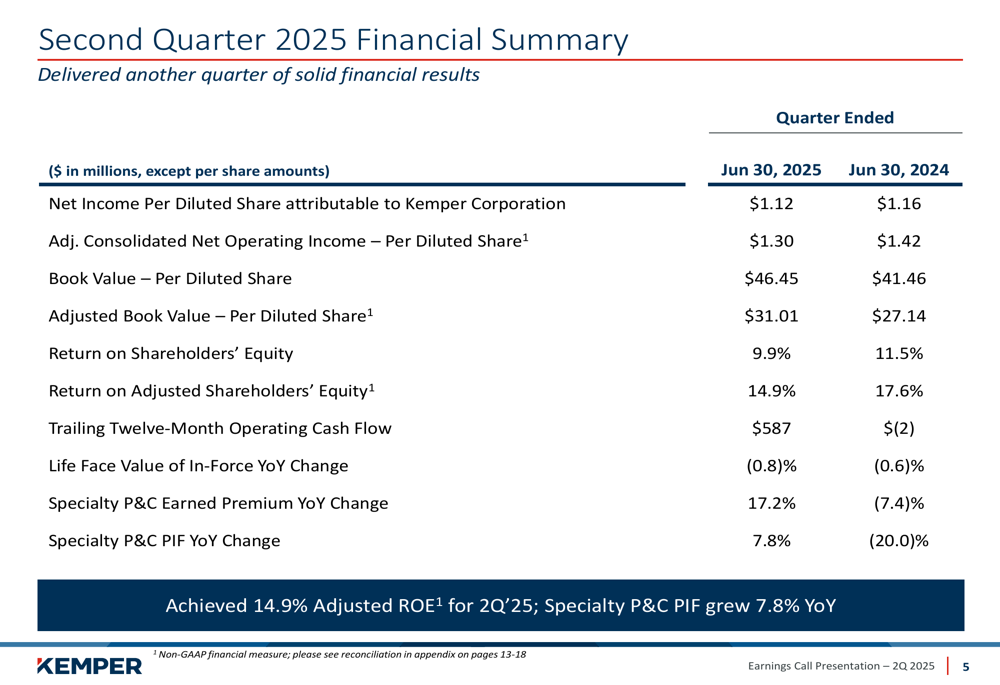

Kemper Corporation (NYSE:KMPR) presented its second quarter 2025 earnings results on August 5, 2025, highlighting continued profitability despite increasing competition in the auto insurance market. The specialty insurer, which focuses on underserved markets, reported net income of $72.6 million or $1.12 per diluted share, slightly below the $1.16 per share reported in the same quarter last year.

In after-hours trading following the presentation, Kemper’s stock rose modestly by 0.48% to $61.20, building on the 0.95% gain during regular trading hours.

Quarterly Performance Highlights

Kemper reported adjusted net operating income of $84.1 million or $1.30 per diluted share for Q2 2025, compared to $1.42 per diluted share in Q2 2024. While this represents a year-over-year decline, the company maintained strong profitability with a 14.9% return on adjusted shareholders’ equity.

As shown in the following comprehensive performance summary:

The company’s book value per share increased to $46.45, up from $41.46 in the same quarter last year, representing a 12% year-over-year improvement. Similarly, adjusted book value per share grew by approximately 14% year-over-year to $31.01.

The financial comparison between Q2 2025 and Q2 2024 reveals both areas of strength and challenges:

A notable achievement was Kemper’s all-time high operating cash flow of approximately $590 million on a trailing twelve-month basis, compared to just $(2) million in the prior year period. This dramatic improvement demonstrates the company’s enhanced operational efficiency and cash generation capabilities.

Segment Performance Analysis

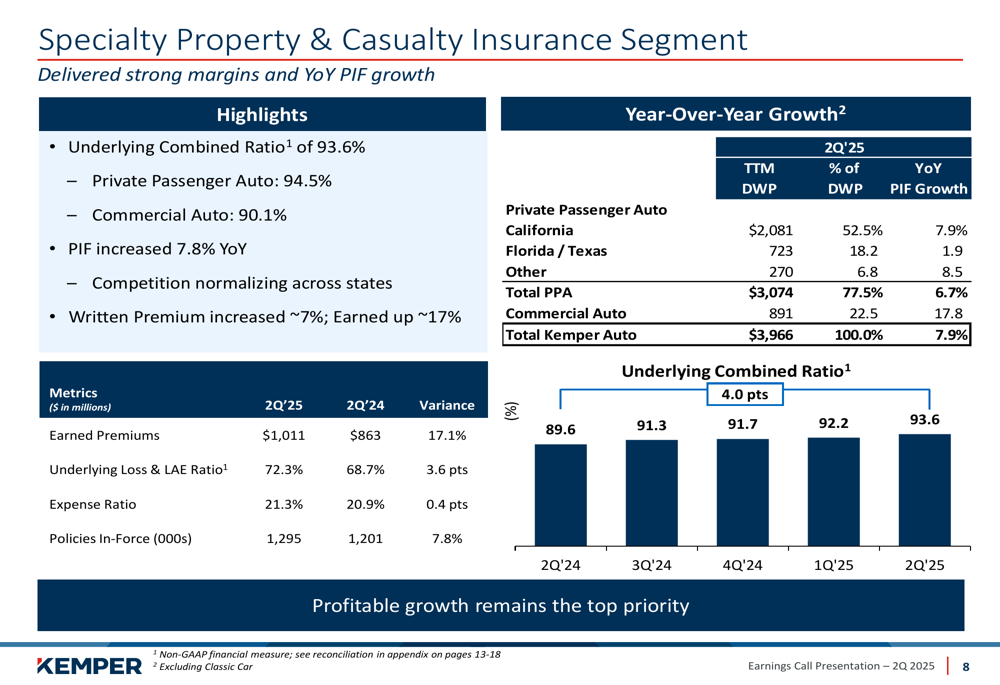

Kemper’s Specialty Property & Casualty segment, which includes its core auto insurance business, showed continued growth with policies in force increasing by 7.8% year-over-year. This represents a significant turnaround from the 20.0% decline reported in Q2 2024. Written premiums grew by approximately 7%, while earned premiums increased by 17.2% compared to the prior year.

The detailed segment performance shows strong growth in key markets, particularly California:

However, the underlying combined ratio for the Specialty P&C segment was 93.6%, showing a gradual increase from 89.6% several quarters ago. This trend suggests some pressure on underwriting margins, likely due to the "increased auto market competition" mentioned in the presentation.

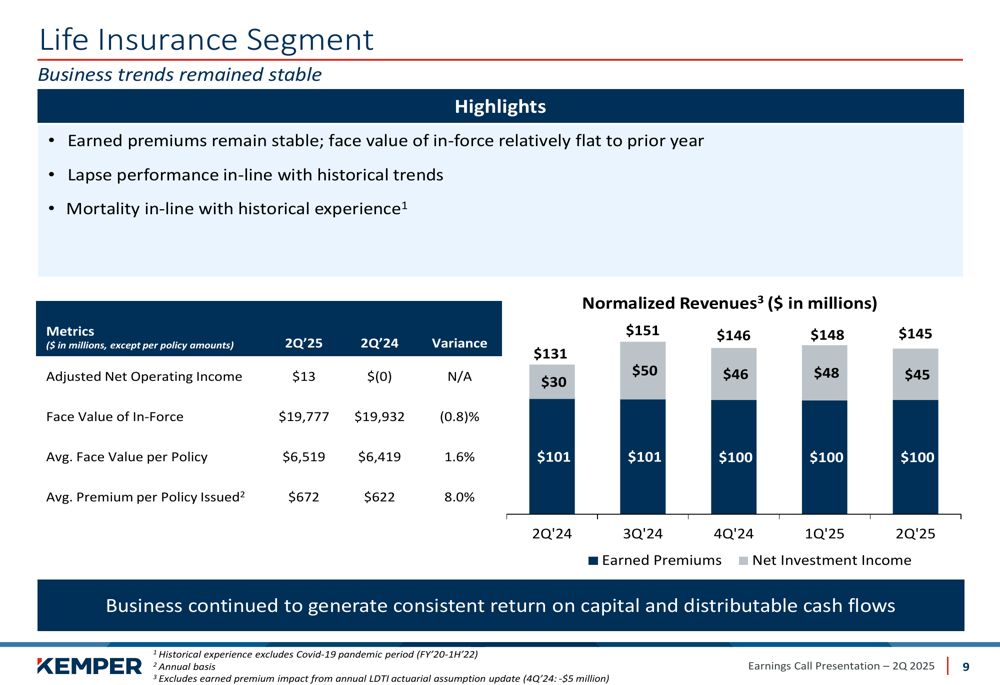

The Life Insurance (NSE:LIFI) segment showed stable performance with $13 million in adjusted net operating income for Q2 2025. The segment maintained consistent earned premiums and relatively flat face value of in-force policies compared to the prior year.

Investment Portfolio and Capital Position

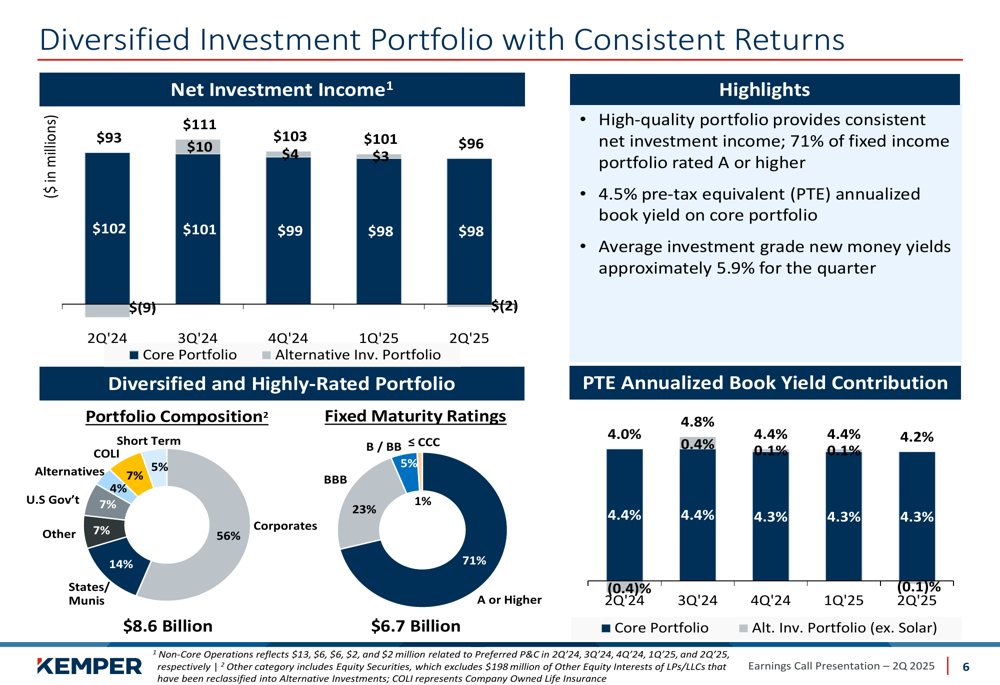

Kemper’s investment portfolio generated $96 million in net investment income during Q2 2025, with a pre-tax equivalent annualized book yield of 4.5% on the core portfolio. The company maintains a high-quality portfolio with 71% of fixed maturity investments rated A or higher.

The following chart illustrates the company’s investment income trends and portfolio composition:

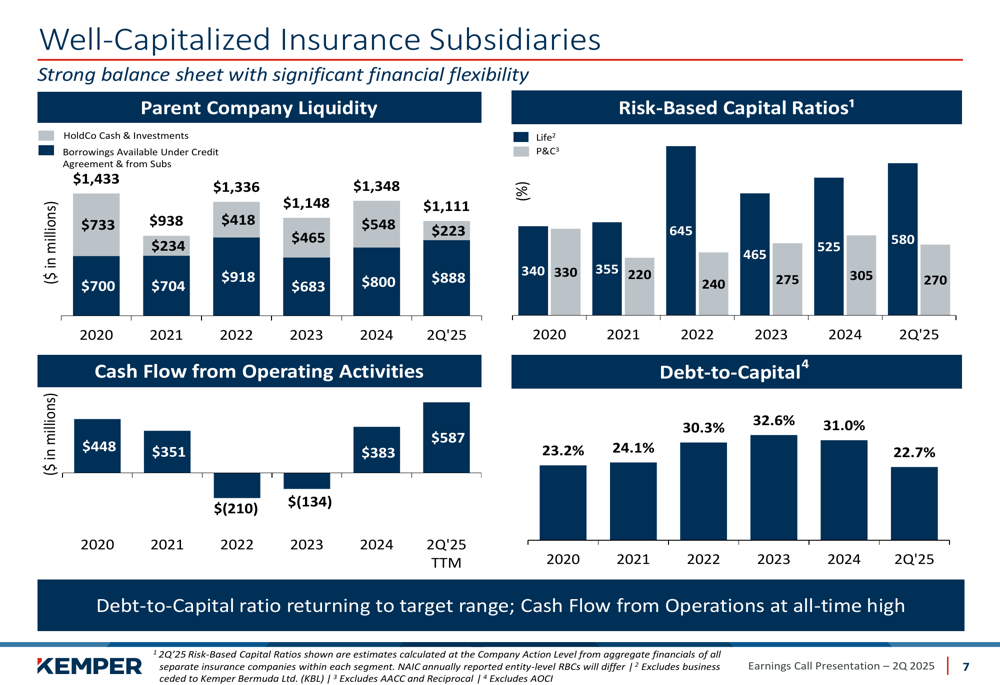

From a capital perspective, Kemper has strengthened its position with parent company liquidity of $1.1 billion and a debt-to-capital ratio of 22.7%, down significantly from 31.0% a year ago and approaching the company’s target range. This improvement provides the company with increased financial flexibility.

The capital position trends are illustrated in the following chart:

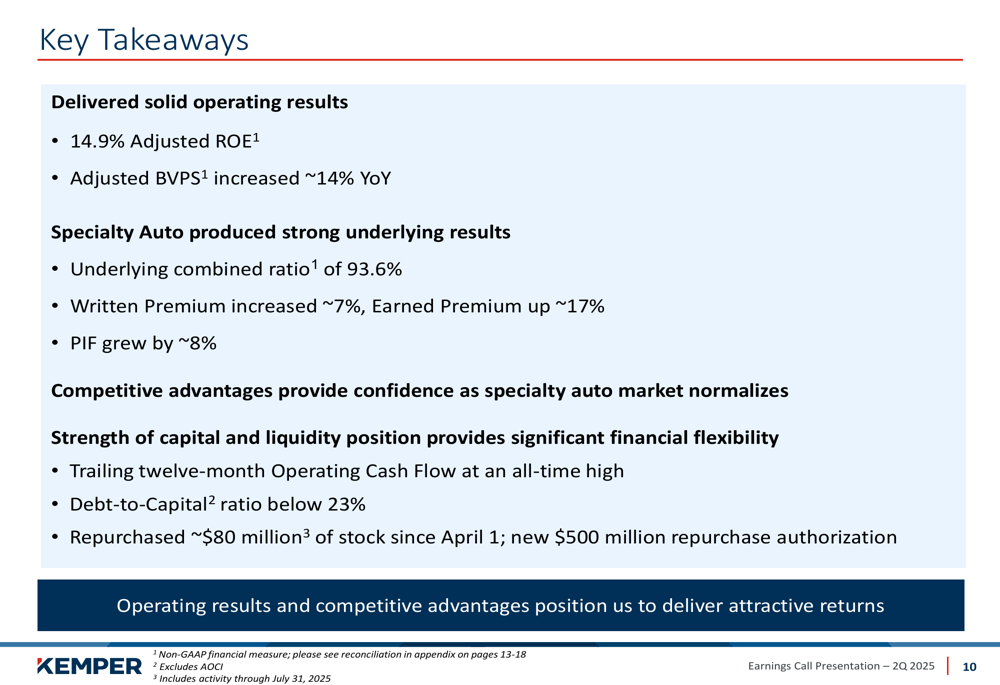

During the quarter, Kemper repurchased approximately $80 million in stock since April 1, 2025, and announced a new $500 million share repurchase authorization, signaling management’s confidence in the company’s financial outlook.

Forward-Looking Statements

Looking ahead, Kemper emphasized that its operating results and competitive advantages position the company to deliver attractive returns despite increasing competition in the auto insurance market. The company highlighted its focus on specialty and underserved markets, which require unique expertise and have limited competition.

As shown in the key takeaways slide:

This strategic positioning aligns with Kemper’s stated goal of targeting "top quartile value creation for customers, employees, and shareholders." The company’s focus on markets with limited competition and its differentiated capabilities in low-cost management, ease of use, and product sophistication are expected to help maintain profitability despite competitive pressures.

When compared to the Q1 2025 results, where Kemper reported earnings per share of $1.65 and a 92.2% underlying combined ratio, the Q2 results indicate some moderation in performance. The slight deterioration in the combined ratio from 92.2% to 93.6% and the decrease in earnings per share from $1.65 to $1.12 suggest that the competitive pressures mentioned in the presentation are having a tangible impact on the company’s operations.

Nevertheless, Kemper’s continued policy growth, strong capital position, and record operating cash flow provide a solid foundation for navigating these competitive challenges while maintaining attractive returns for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.