Apple investigating outages affecting Apple TV+, Apple Music services

Introduction & Market Context

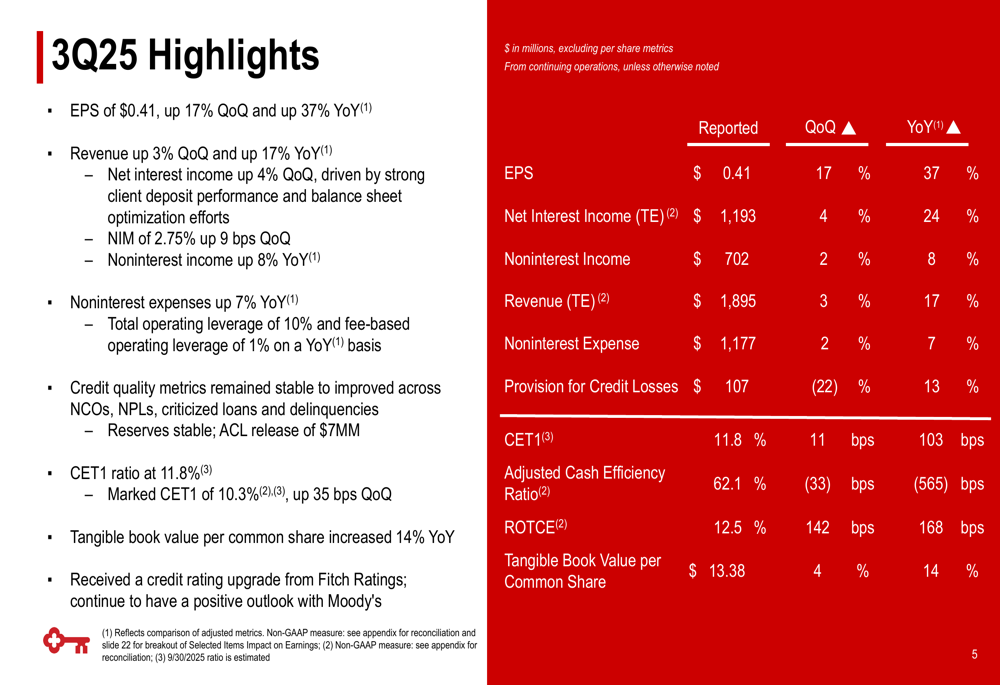

KeyCorp (NYSE:KEY) presented its third quarter 2025 earnings results on October 16, 2025, reporting stronger-than-expected financial performance despite facing market headwinds. The bank delivered an earnings per share (EPS) of $0.41, exceeding analyst expectations of $0.38 by 7.89%, while revenue reached $1.9 billion, surpassing forecasts by 1.06%.

Despite these positive results, KeyCorp’s stock experienced a pre-market decline of 3.5%, trading at $17.11, and continued falling to $16.93 during regular trading hours, representing a 4.54% drop from the previous close of $17.73. This market reaction suggests investors may be concerned about broader economic challenges or specific headwinds facing the banking sector.

Quarterly Performance Highlights

KeyCorp reported significant year-over-year improvements across key financial metrics in the third quarter. EPS increased by 37% compared to the same period last year, while revenue grew by 17%. The company achieved a net interest margin (NIM) of 2.75%, up 9 basis points quarter-over-quarter, hitting its year-end target ahead of schedule.

As shown in the following comprehensive overview of Q3 2025 highlights, KeyCorp demonstrated strength across multiple performance indicators:

The bank’s return on tangible common equity (ROTCE) reached 12.5%, improving by 142 basis points quarter-over-quarter and 168 basis points year-over-year. Tangible book value per common share increased by 14% year-over-year to $13.38. Additionally, KeyCorp received a credit rating upgrade from Fitch Ratings during the quarter, further validating its financial strength.

Detailed Financial Analysis

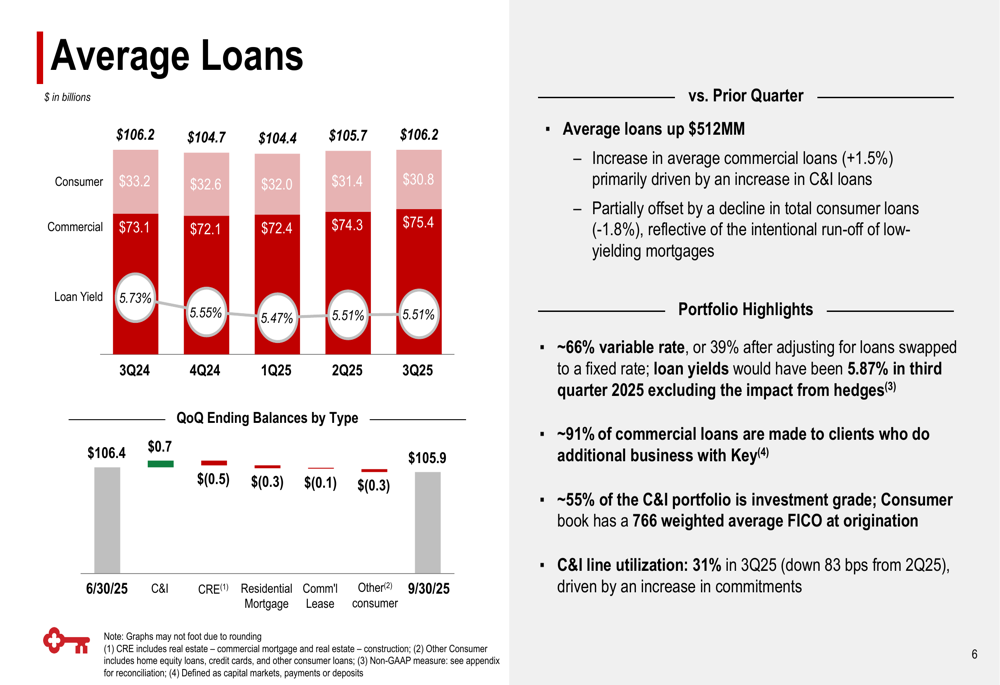

KeyCorp’s loan portfolio showed a strategic shift toward commercial lending, with average commercial loans increasing by 1.5%, primarily driven by growth in C&I loans. This growth was partially offset by a 1.8% decline in consumer loans, reflecting an intentional reduction in low-yielding mortgages.

The following chart illustrates the composition and trends in KeyCorp’s loan portfolio:

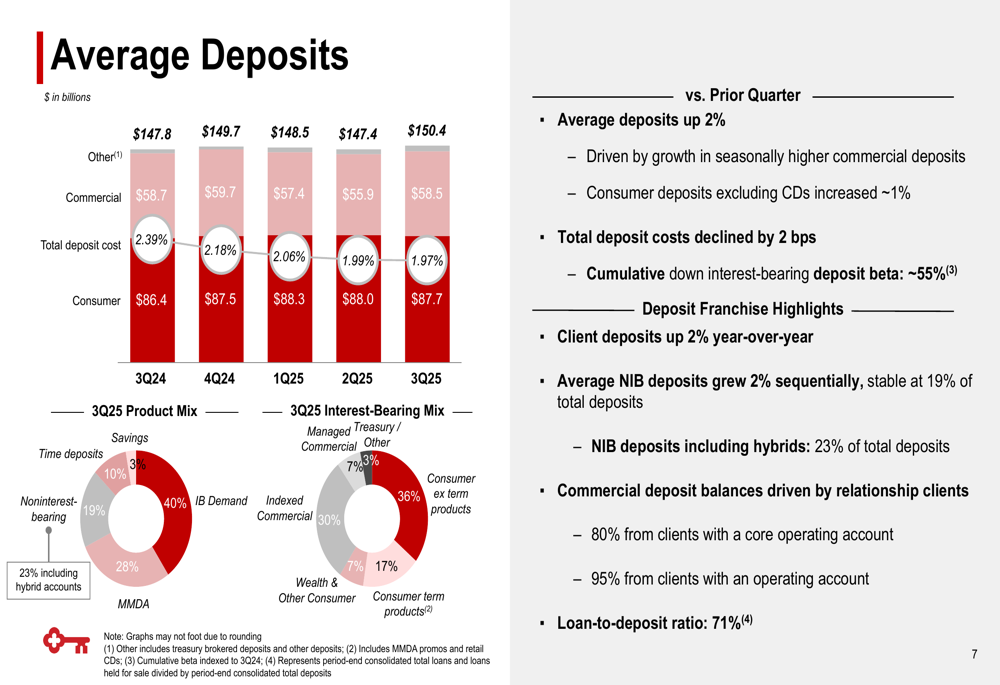

On the deposit front, KeyCorp reported a 2% year-over-year increase in average deposits, driven by seasonally higher commercial deposits. Consumer deposits excluding CDs increased by approximately 1%. The bank’s deposit costs declined by 2 basis points, with a cumulative down interest-bearing deposit beta of approximately 55%.

The following visualization shows the deposit trends and composition:

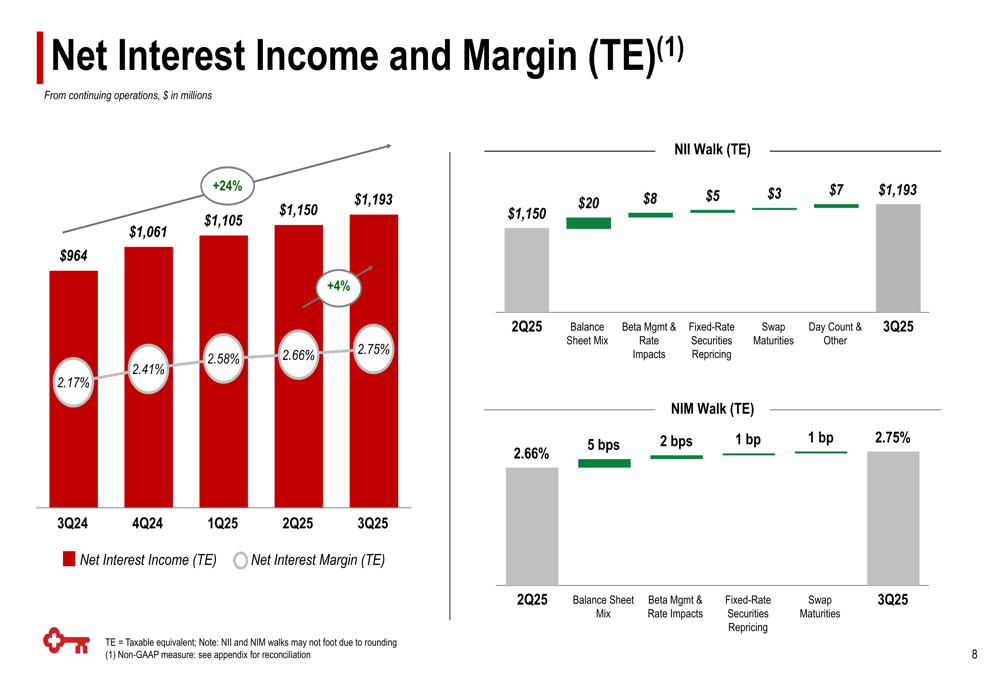

Net interest income (NII) showed impressive growth, increasing by 24% year-over-year to $1,193 million in Q3 2025, up from $964 million in Q3 2024. This growth was supported by improvements in balance sheet mix, beta management, and swap maturities.

As shown in the following chart, both NII and NIM have demonstrated consistent improvement:

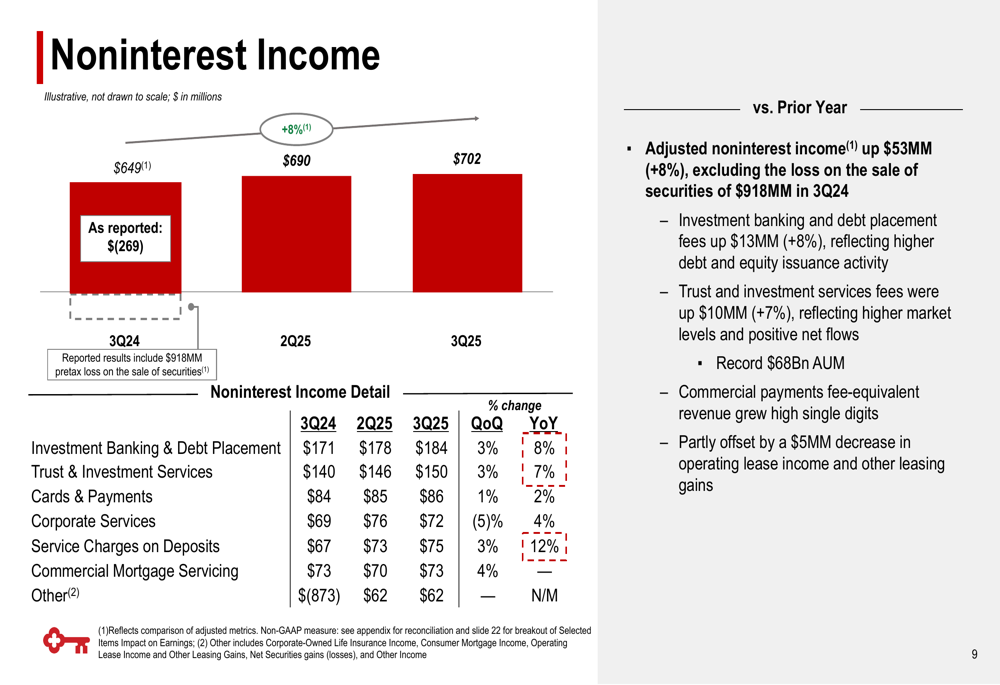

Noninterest income grew by 8% year-over-year to $702 million, excluding the loss on sale of securities of $918 million in Q3 2024. This growth was driven by strong performance across multiple fee-based businesses, with investment banking and debt placement fees increasing by 8% and trust and investment services revenue growing by 7%.

The following breakdown illustrates the composition and growth of noninterest income:

Credit Quality & Capital Position

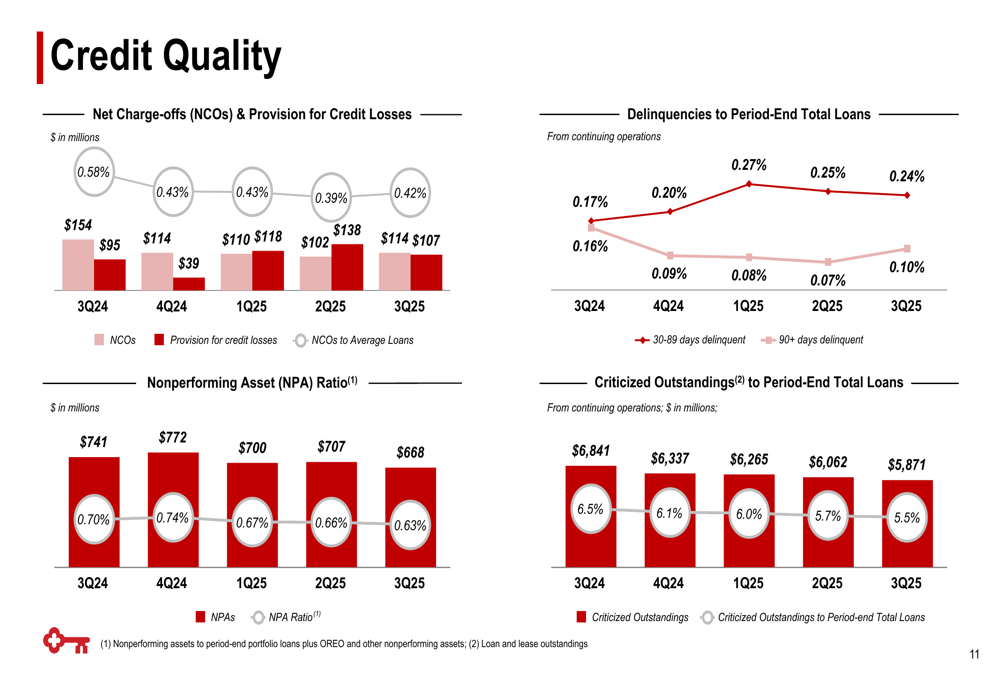

KeyCorp maintained strong credit quality metrics in Q3 2025, with net charge-offs (NCOs) to average loans at 42 basis points and nonperforming assets (NPAs) to loans plus OREO at 63 basis points. The company’s allowance for credit losses remained stable, with a small release of $7 million during the quarter.

The following chart provides a detailed view of credit quality trends:

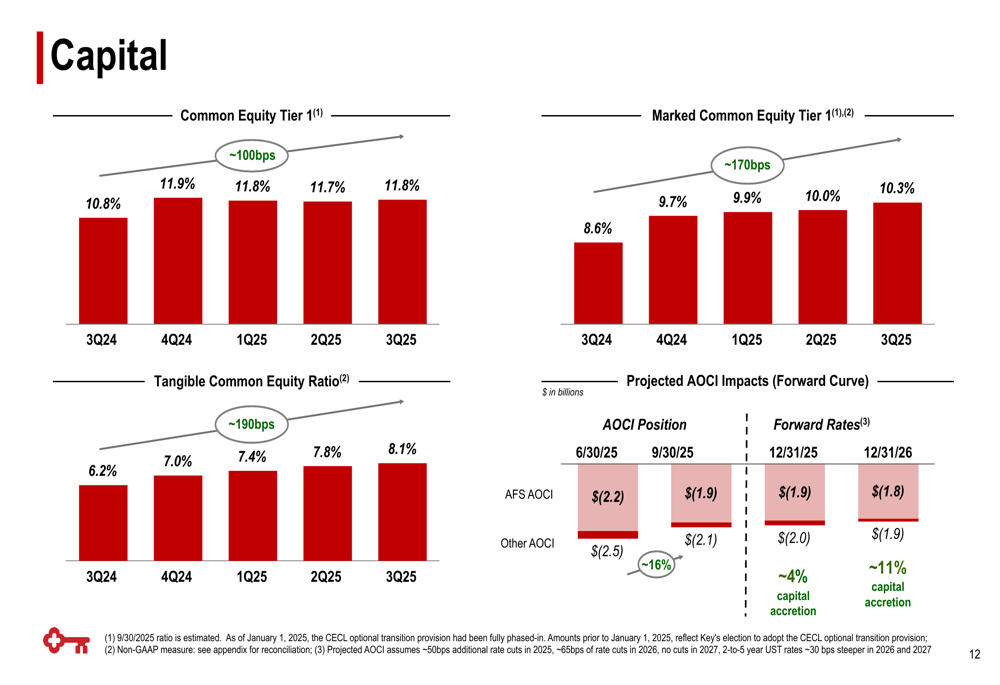

Capital ratios continued to strengthen, with the Common Equity Tier 1 (CET1) ratio increasing to 11.8%, up from 10.8% a year ago. The Marked CET1 ratio, which adjusts for unrealized losses in the available-for-sale securities portfolio, improved to 10.3%, up approximately 170 basis points year-over-year.

As illustrated in the following capital metrics overview:

Strategic Initiatives & Medium-Term Targets

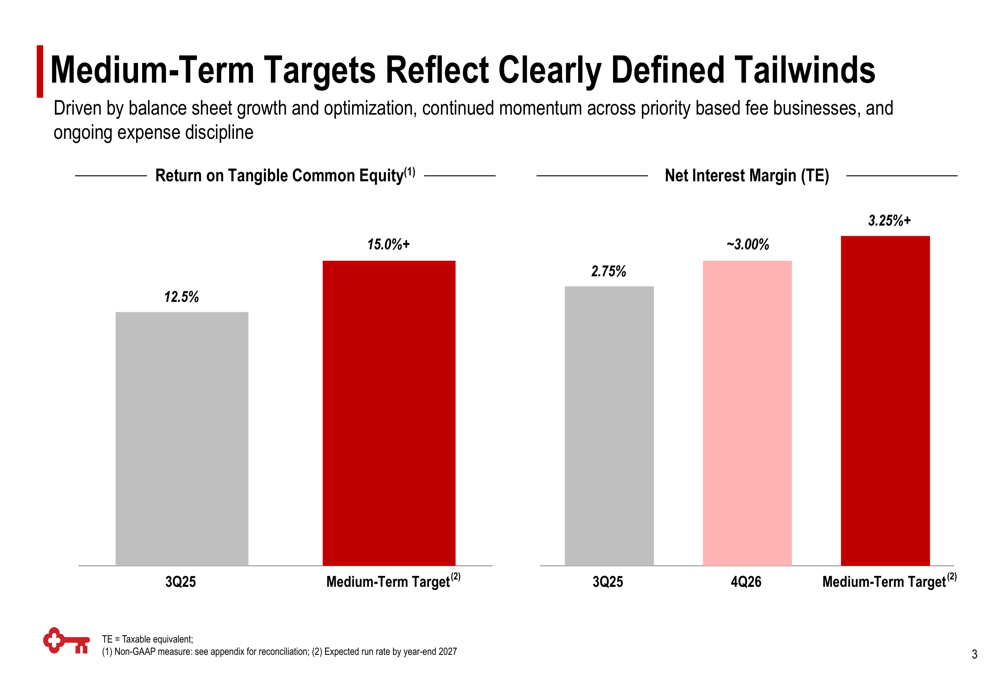

KeyCorp outlined ambitious medium-term targets, expecting to achieve a return on tangible common equity (ROTCE) of 15% or higher by the end of 2027, compared to the current 12.5%. The company also aims to increase its net interest margin to 3.25% or higher by the medium term, from the current level of 2.75%.

During the earnings call, CEO Chris Gorman emphasized that "The 15% should not be viewed as a final goal, but rather an important milestone on our journey to achieving higher levels of both sustainable profitability and returns for our shareholders."

The following chart illustrates KeyCorp’s medium-term financial targets:

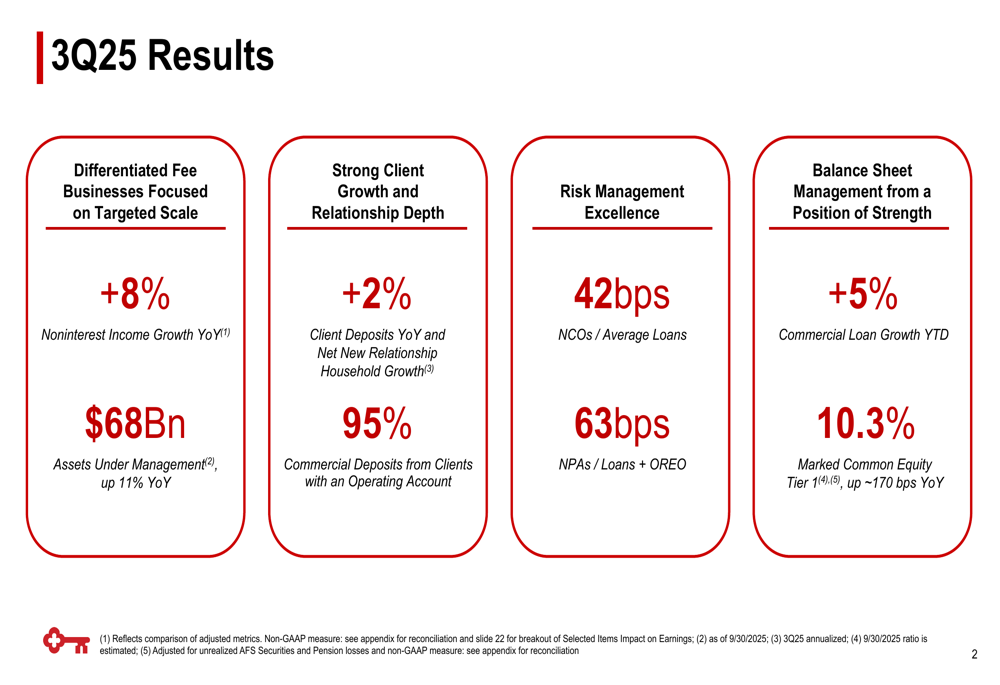

The bank is focusing on four strategic priorities: differentiated fee businesses with targeted scale, strong client growth and relationship depth, risk management excellence, and balance sheet management from a position of strength. Assets under management reached $68 billion, up 11% year-over-year, and 95% of commercial deposits came from clients with an operating account.

As shown in this overview of KeyCorp’s strategic focus areas and achievements:

2025 Outlook & Forward Guidance

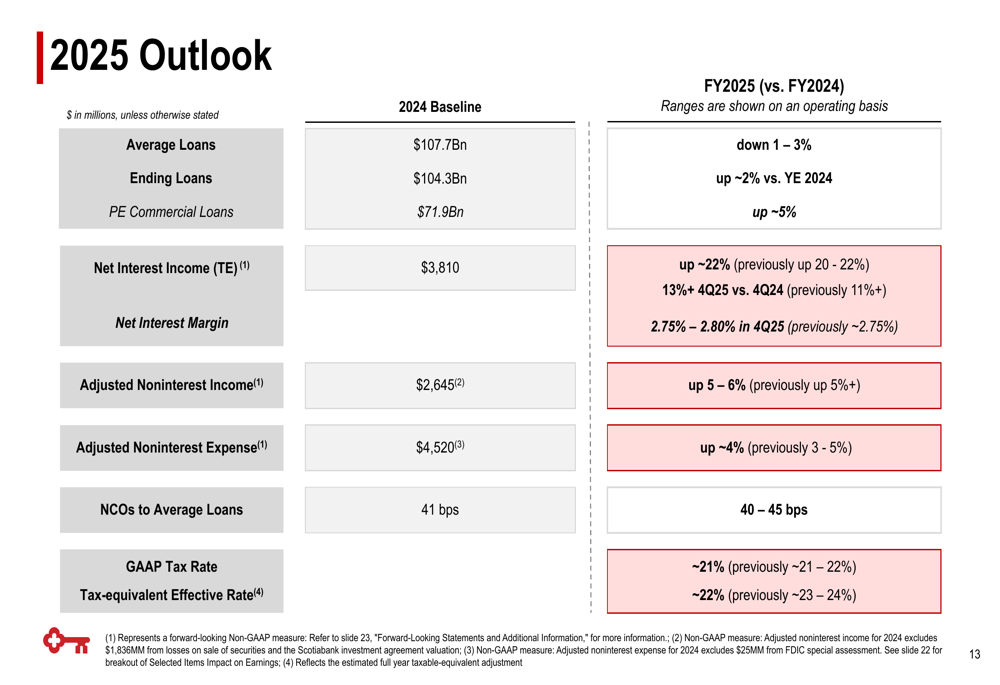

Looking ahead, KeyCorp provided an updated outlook for 2025, raising some of its previous guidance. The company now expects net interest income to increase by approximately 22% (previously 20-22%) and noninterest income to grow by 5-6% (previously 5%+). Net interest margin is projected to reach 2.75-2.80% in Q4 2025, slightly higher than the previous guidance of approximately 2.75%.

While average loans are expected to decline by 1-3% for the full year, ending loans are projected to increase by approximately 2% compared to year-end 2024, with commercial loans specifically expected to grow by around 5%.

The detailed 2025 outlook is presented in the following comprehensive guidance:

CFO Clark Kayet highlighted the bank’s selective approach to deposits during the earnings call, stating, "We have a business model that allows us to be very discerning about which deposits we take and at what price."

Despite the positive earnings report and improved outlook, investors appear concerned about potential challenges, including regulatory changes, market volatility, and interest rate fluctuations. The company’s significant exposure to energy and healthcare sectors may also pose sector-specific risks that could impact future performance.

KeyCorp plans to repurchase approximately $100 million of common stock in Q4 2025, reflecting confidence in its financial position. With strong pipelines in place, management anticipates a record revenue year in 2025 and maintains a positive outlook for 2026, despite the cautious market reaction to its Q3 results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.