EOG Resources completes $5.6 billion acquisition of Encino Acquisition Partners

Introduction & Market Context

Kinross Gold Corporation (NYSE:KGC) presented its first quarter 2025 results on May 7, 2025, highlighting significant financial improvements despite a slight decrease in gold production. The company emphasized its "Delivering Value" strategy, which appears to be yielding results as evidenced by strengthened margins, increased cash flow, and a more robust balance sheet.

The gold producer reported stable production guidance for the next three years while advancing its project pipeline, positioning itself for sustainable long-term growth in a favorable gold price environment.

Quarterly Performance Highlights

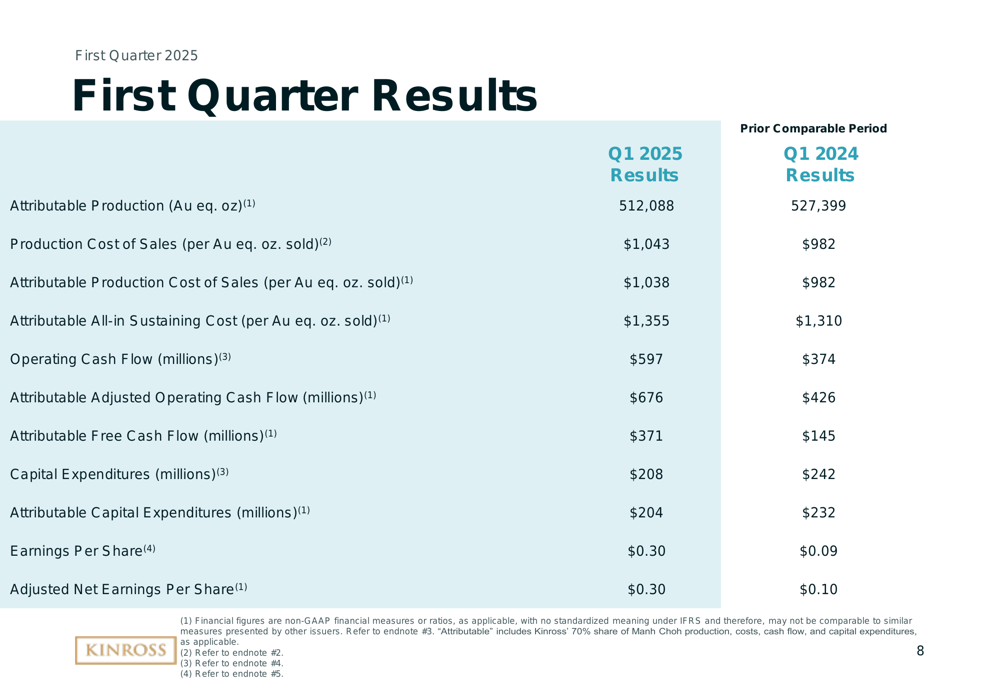

Kinross reported attributable gold equivalent production of 512,088 ounces in Q1 2025, representing a modest 2.9% decrease from 527,399 ounces in the same period last year. Despite this slight production dip, the company delivered impressive financial results, with earnings per share more than tripling year-over-year.

As shown in the following detailed financial comparison:

The standout metrics include a 60% increase in operating cash flow to $597 million (compared to $374 million in Q1 2024) and a 156% surge in attributable free cash flow to $371 million (versus $145 million in Q1 2024). Earnings per share reached $0.30, more than triple the $0.09 reported in the same quarter last year.

Production costs showed an increase, with production cost of sales rising to $1,043 per gold equivalent ounce sold, up from $982 in Q1 2024. Similarly, all-in sustaining costs increased to $1,355 per ounce from $1,310 in the comparable period.

Detailed Financial Analysis

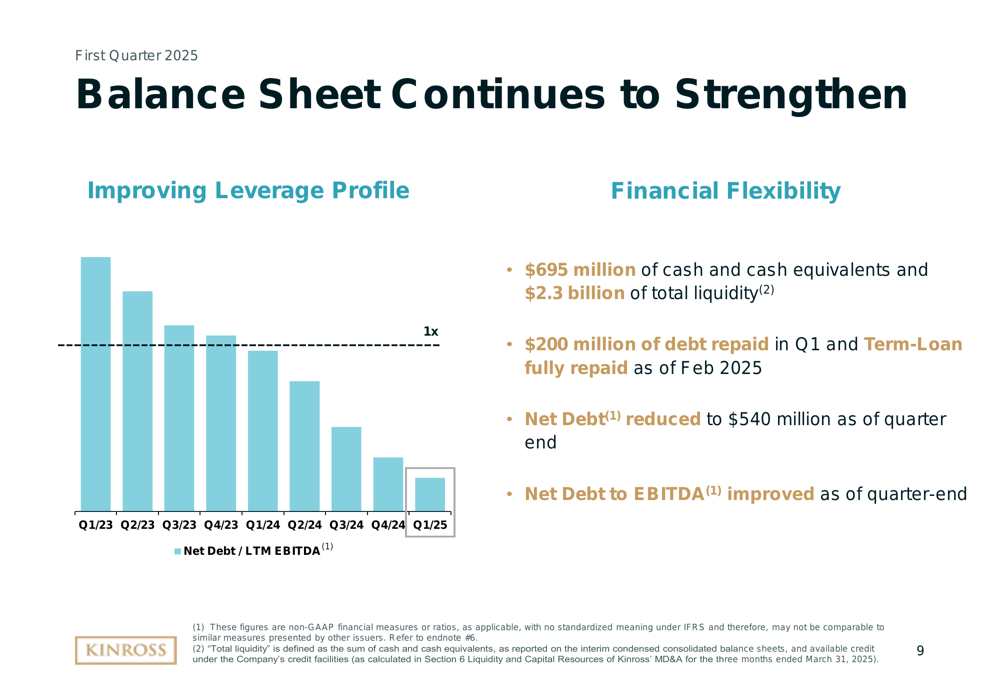

Kinross has made significant progress in strengthening its balance sheet, reducing its net debt to $540 million by the end of Q1 2025. The company repaid $200 million of debt during the quarter and fully repaid its Term-Loan as of February 2025. This debt reduction has improved the company’s leverage profile, with the net debt to EBITDA ratio approaching 1x.

The following slide illustrates the company’s improving financial position:

The company maintained strong liquidity with $695 million in cash and cash equivalents and total liquidity of $2.3 billion as of quarter-end. This financial flexibility supports Kinross’s commitment to shareholder returns through a sustainable quarterly dividend and increased share repurchases.

Operational Performance

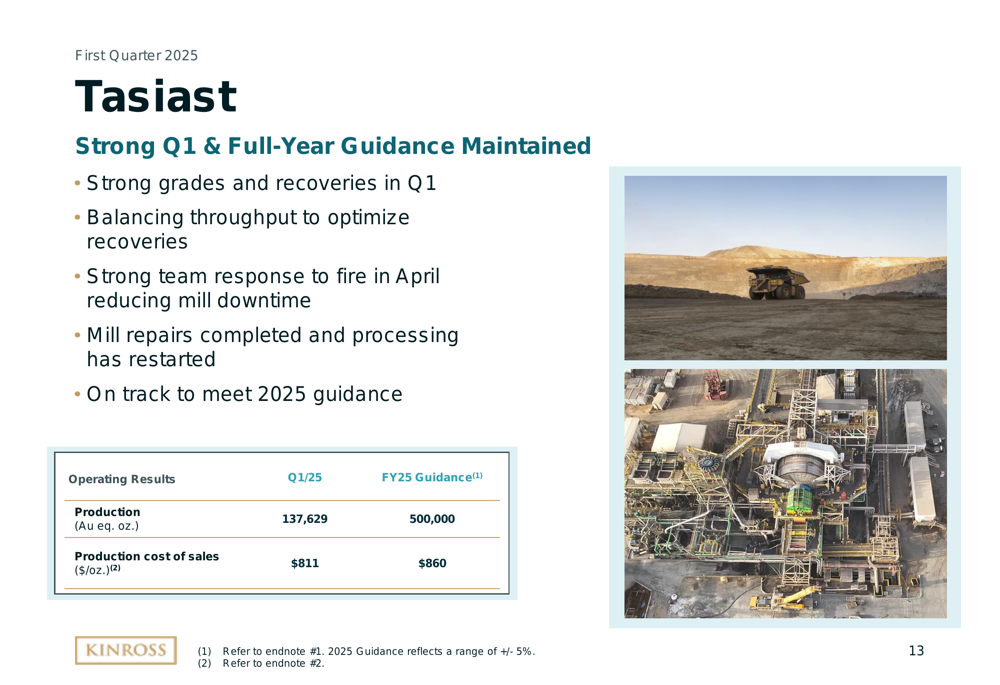

Kinross’s operational performance was led by strong contributions from its Tasiast and Paracatu mines, which produced 137,629 and 146,639 gold equivalent ounces, respectively, in Q1 2025.

The Tasiast mine in Mauritania delivered strong grades and recoveries in Q1, although the company reported a fire incident in April that temporarily affected mill operations. Management noted that repairs have been completed and processing has restarted, with the mine still on track to meet its 2025 guidance of 500,000 ounces.

The following slide details Tasiast’s performance:

Paracatu in Brazil also had a strong start to the year, with production improving over the prior quarter due to strong grades, improved recoveries, and timing of ounces processed. The site team successfully mitigated the impact of significant rainfall during the quarter, keeping the operation on budget.

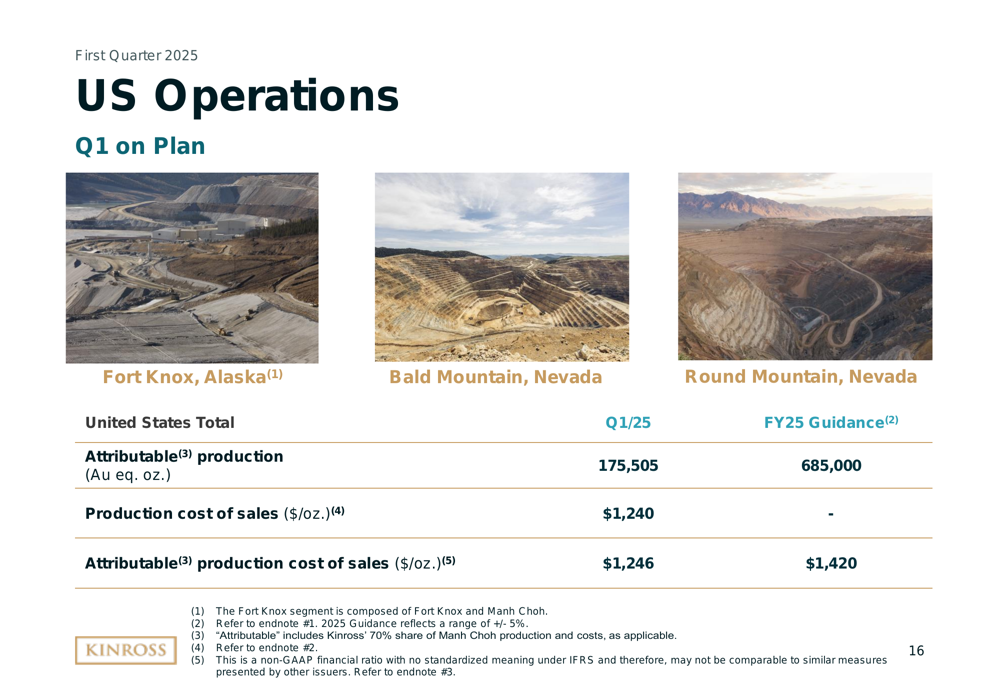

The company’s U.S. operations, including Fort Knox, Bald Mountain, and Round Mountain, collectively produced 175,505 attributable gold equivalent ounces in Q1, in line with the plan. These operations are on track to meet the full-year guidance of 685,000 ounces.

Strategic Initiatives

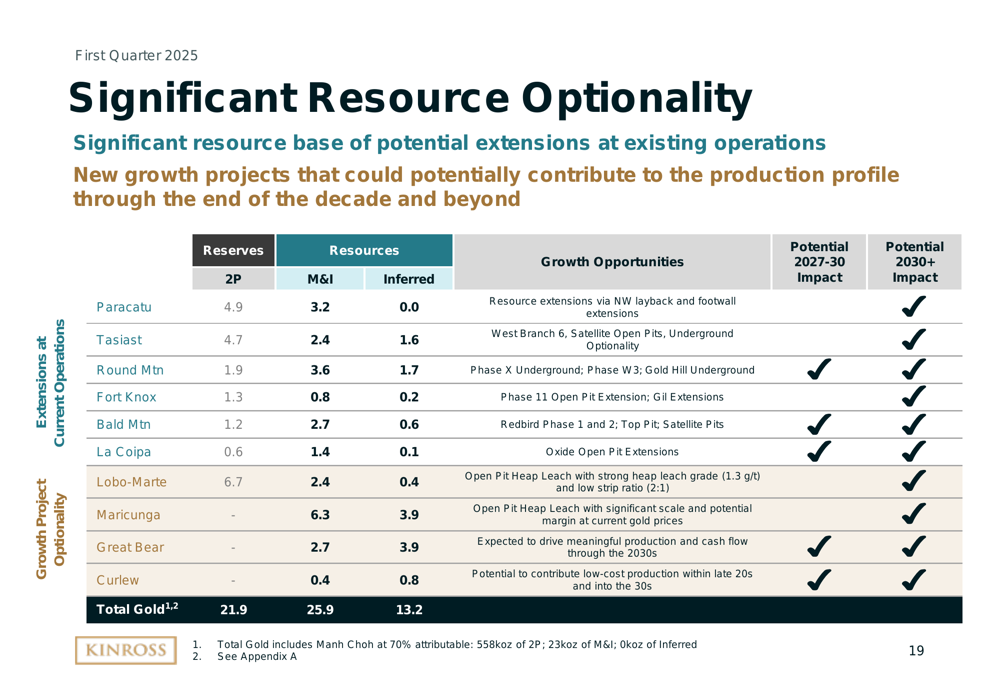

Kinross emphasized its robust project pipeline, which underpins its long-term production potential. The company has a significant resource base with 21.9 million ounces of proven and probable reserves, 25.9 million ounces of measured and indicated resources, and 13.2 million ounces of inferred resources.

The following slide illustrates the company’s resource optionality across its portfolio:

Key development projects include:

1. Great Bear Project: Surface works are progressing at the Advanced Exploration (AEX) site, with excavation for the underground portal construction underway. The company remains on track to start the exploration decline later this year.

2. Curlew Project: Underground development was re-initiated in Q1 to extend the decline at depth, targeting high-grade zones of mineralization. Q1 drill results continued to show wide, high-grade intercepts.

3. Phase X Project: Q1 drilling results confirmed good grades and widths in the primary target zones.

4. Lobo-Marte Project: Baseline studies to support the Environmental Impact Assessment are progressing well, with a project update expected in Q1 2026.

Forward-Looking Statements

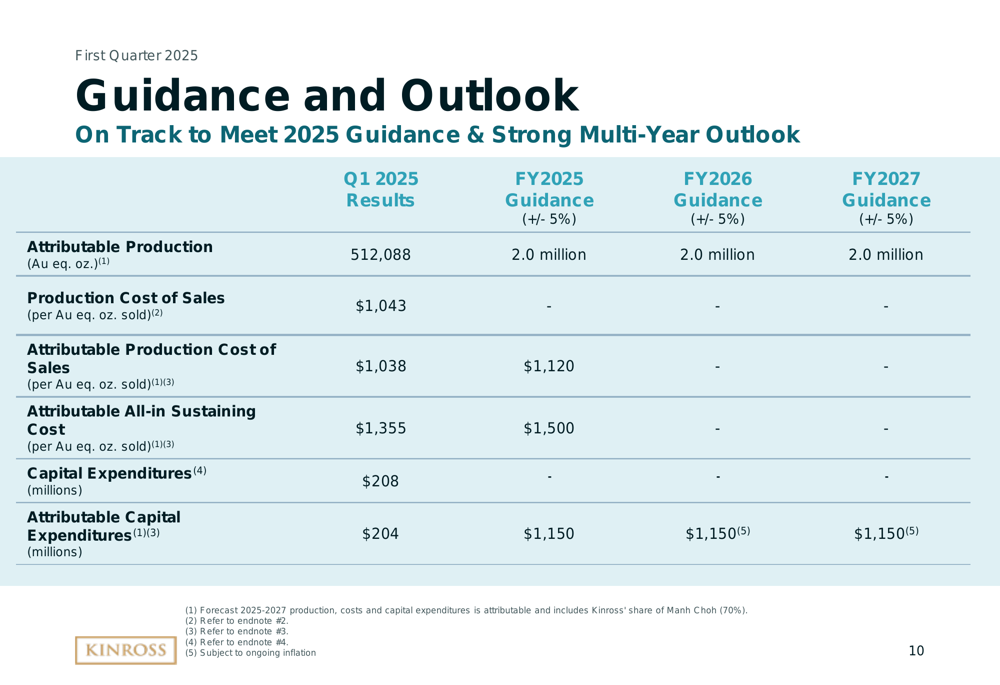

Kinross provided a stable multi-year production forecast of 2.0 million gold equivalent ounces annually (±5%) from 2025 through 2027. The company is on track to meet its 2025 guidance across all metrics.

The following guidance and outlook slide details the company’s expectations:

For 2025, Kinross expects attributable production cost of sales of $1,120 per gold equivalent ounce sold and attributable all-in sustaining costs of $1,500 per ounce. Capital expenditures are projected at $1,150 million for each of the next three years.

The company’s strong cash flow outlook supports its commitment to sustainable shareholder returns through a quarterly dividend and increased share repurchases, while maintaining investment in its project pipeline to drive future growth.

In conclusion, Kinross Gold’s Q1 2025 results demonstrate the company’s ability to generate significant cash flow and earnings growth despite slightly lower production volumes. With a strengthened balance sheet, stable production outlook, and advancing project pipeline, Kinross appears well-positioned to continue delivering value to shareholders in the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.