These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Kinross Gold Corporation (NYSE:KGC) released its second quarter 2025 results on July 31, showcasing strong financial performance despite moderate cost pressures. The gold producer capitalized on favorable gold prices to generate record operating margins and cash flow while continuing to strengthen its balance sheet.

The company’s Q2 presentation emphasized its ability to deliver value through stable production, cost management, and advancing its project pipeline. This comes as gold prices have remained supportive, allowing major producers like Kinross to focus on debt reduction and shareholder returns.

Quarterly Performance Highlights

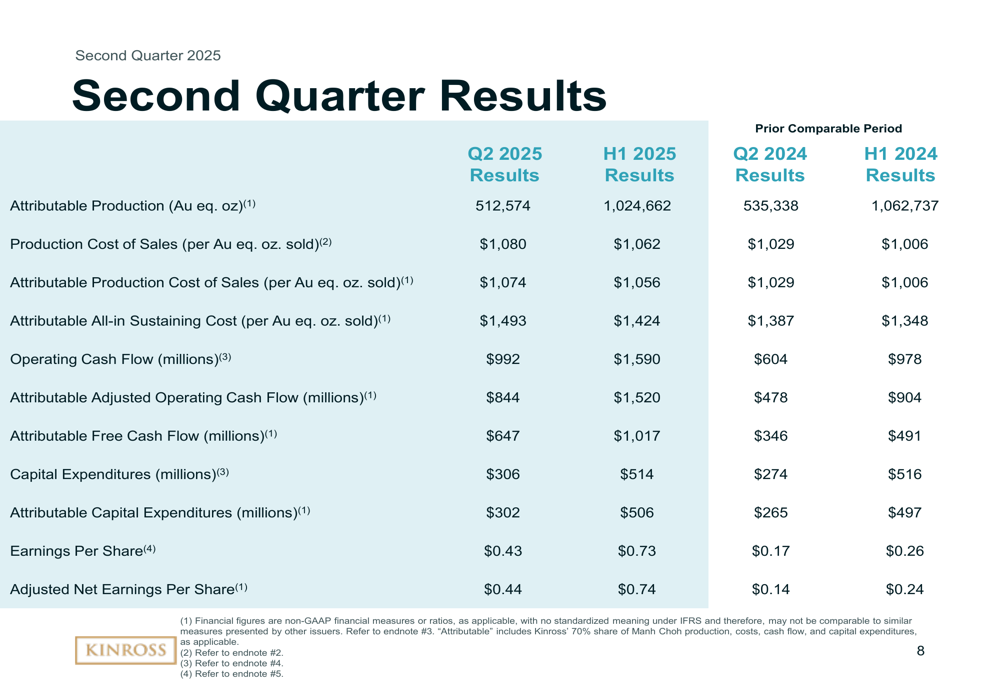

Kinross reported attributable production of 512,574 gold equivalent ounces in Q2 2025, slightly below the 535,338 ounces produced in the same period last year. For the first half of 2025, production totaled 1,024,662 ounces compared to 1,062,737 ounces in H1 2024.

Despite the modest production decline, Kinross delivered substantial improvements in key financial metrics, demonstrating the impact of higher gold prices and operational efficiency.

As shown in the following comprehensive results table:

Operating cash flow nearly doubled to $992 million in Q2 2025 from $604 million in Q2 2024, while attributable free cash flow jumped to $647 million from $346 million in the prior-year quarter. Earnings per share reached $0.43, significantly higher than the $0.17 reported in Q2 2024.

Production costs increased moderately to $1,080 per gold equivalent ounce sold in Q2 2025 from $1,029 in Q2 2024, while all-in sustaining costs rose to $1,493 per ounce from $1,387 in the comparable period. Despite these cost pressures, the company maintained strong margins due to favorable gold prices.

Balance Sheet Strength & Capital Returns

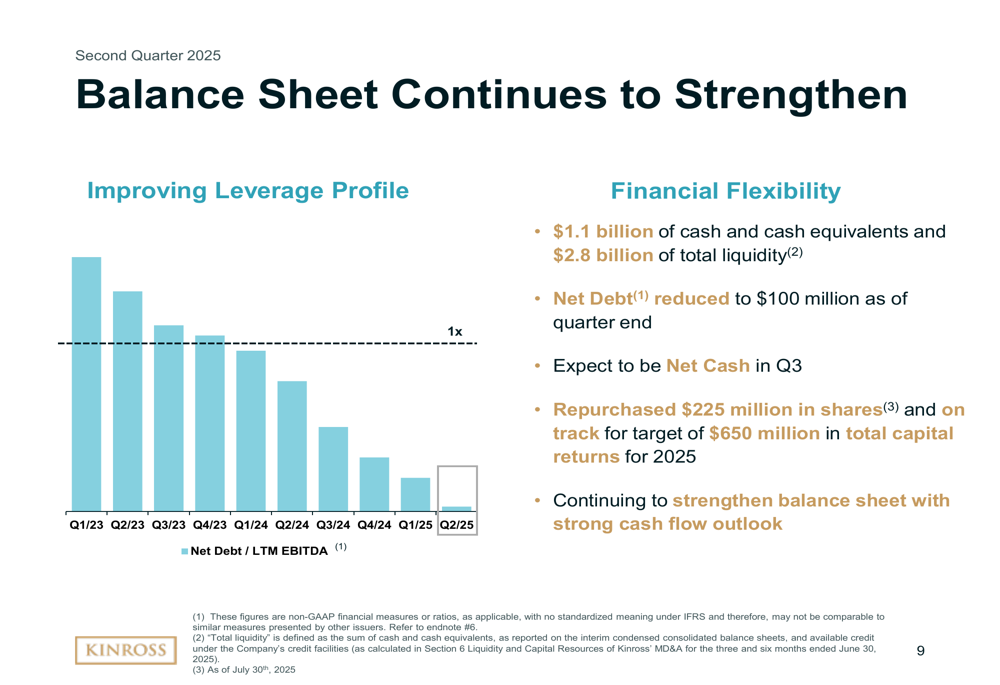

One of the most notable achievements highlighted in the presentation was Kinross’s continued balance sheet strengthening. The company has systematically reduced its leverage over the past ten quarters, with net debt declining to just $100 million by the end of Q2 2025.

The following chart illustrates this impressive debt reduction trajectory:

Kinross expects to achieve a net cash position in Q3 2025, supported by its strong cash flow generation. The company reported $1.1 billion in cash and cash equivalents and total liquidity of $2.8 billion as of the quarter end.

The improved financial position has enabled Kinross to enhance shareholder returns. The company repurchased $225 million in shares during the period and remains on track to deliver $650 million in total capital returns for 2025, including its sustainable quarterly dividend.

Guidance and Outlook

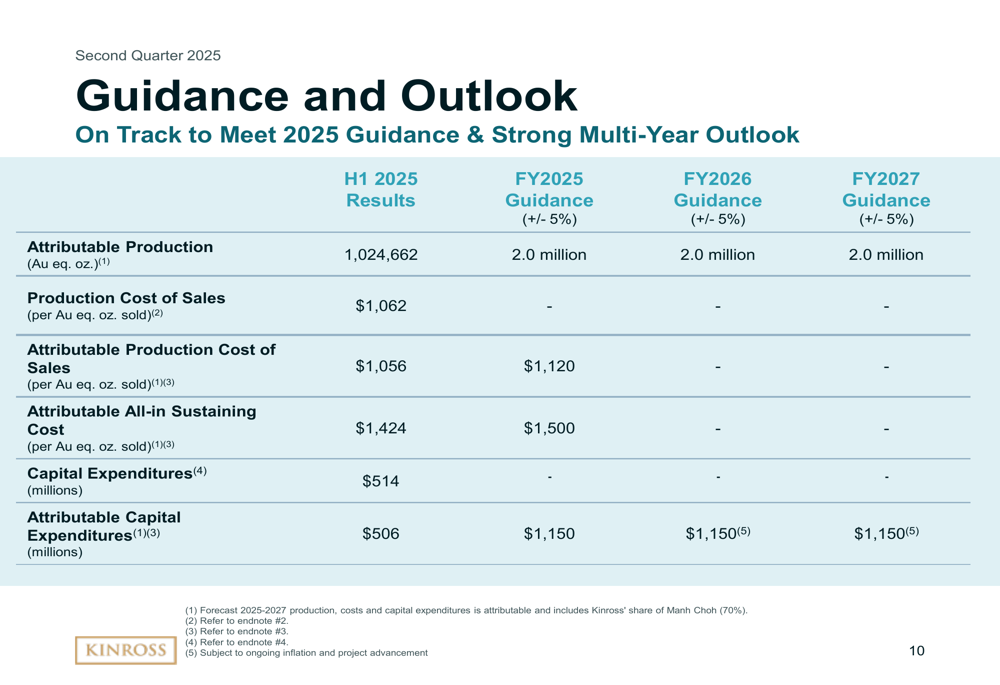

Kinross confirmed it remains on track to meet its 2025 production guidance of 2.0 million gold equivalent ounces (±5%) and maintained its stable multi-year outlook with the same production target for 2026 and 2027.

The detailed guidance table below shows the company’s expectations for key metrics:

For 2025, Kinross projects attributable production costs of $1,120 per gold equivalent ounce sold and all-in sustaining costs of $1,500 per ounce. Capital expenditures are expected to total $1,150 million for the year, with similar levels projected for 2026 and 2027.

Operational Performance

Paracatu in Brazil emerged as the strongest contributor in Q2, generating significant cash flow with production of 149,264 ounces at a cost of $958 per ounce. The operation benefited from higher throughput and strong recoveries, as shown in the following performance summary:

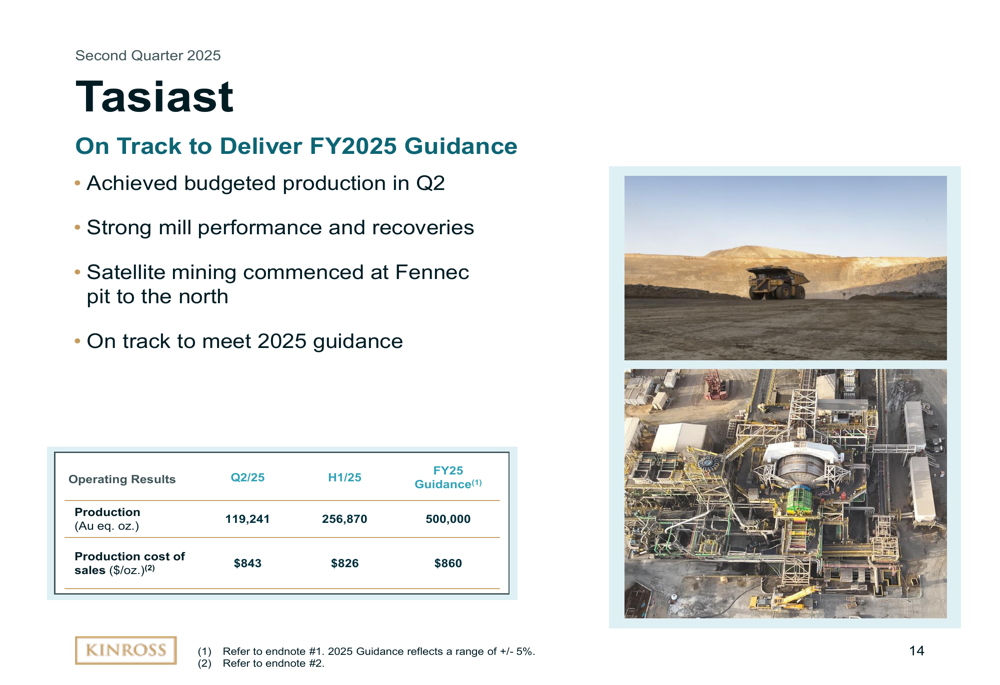

Tasiast in Mauritania delivered 119,241 ounces in Q2 at a cost of $843 per ounce, benefiting from strong mill performance and recoveries. The operation has begun satellite mining at the Fennec pit to the north and remains on track to meet its 2025 guidance of 500,000 ounces.

The company’s U.S. operations, including Fort Knox, Bald Mountain, and Round Mountain, collectively produced 189,930 attributable ounces in Q2 at a production cost of $1,229 per ounce. These operations are on track to meet their combined full-year guidance of 685,000 ounces.

Growth Projects & Exploration

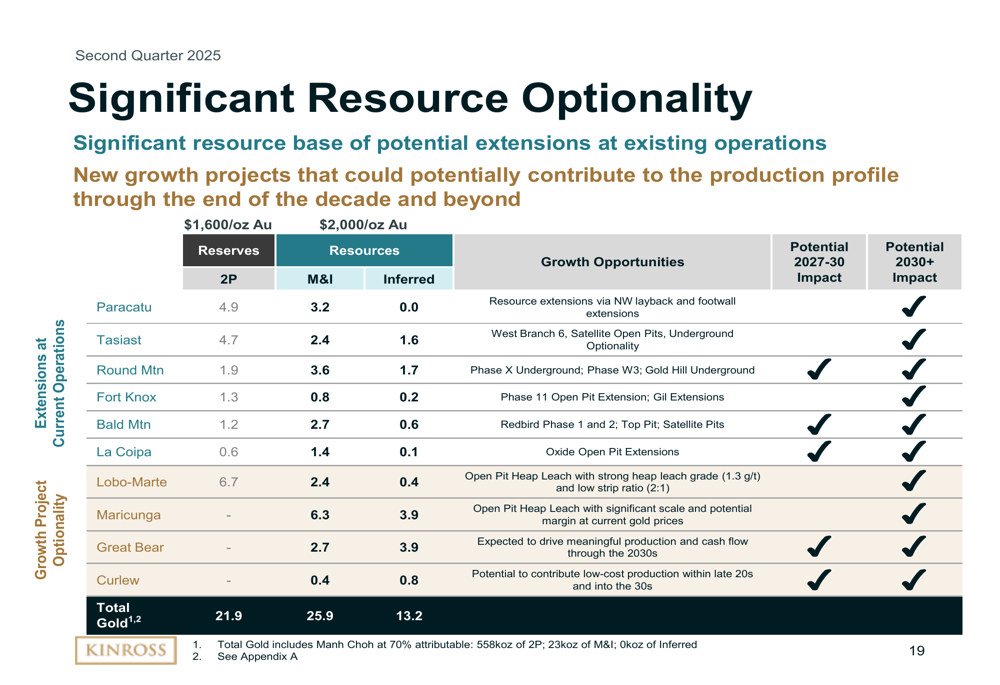

Kinross highlighted its significant resource optionality across its portfolio, with substantial reserves and resources under both $1,600/oz and $2,000/oz gold price scenarios. The company’s total proven and probable reserves stand at 21.9 million ounces using a $1,600/oz gold price assumption.

The following table details the company’s extensive resource base:

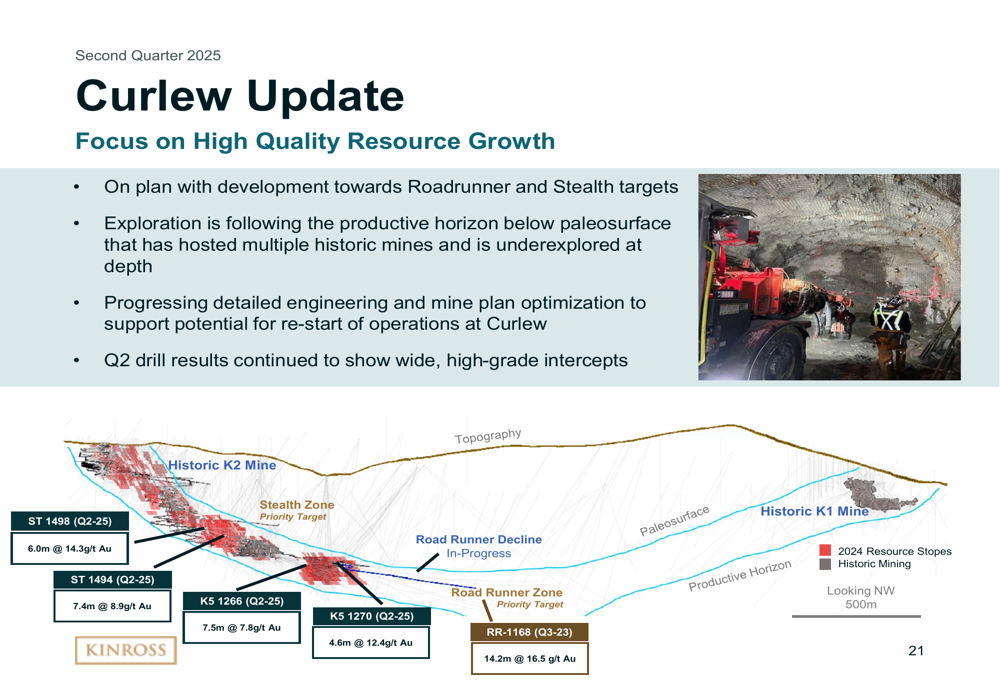

The company reported positive exploration results at its Curlew project, where development is progressing toward the Roadrunner and Stealth targets. Q2 drill results showed wide, high-grade intercepts, and the company is advancing detailed engineering and mine plan optimization to support a potential restart of operations.

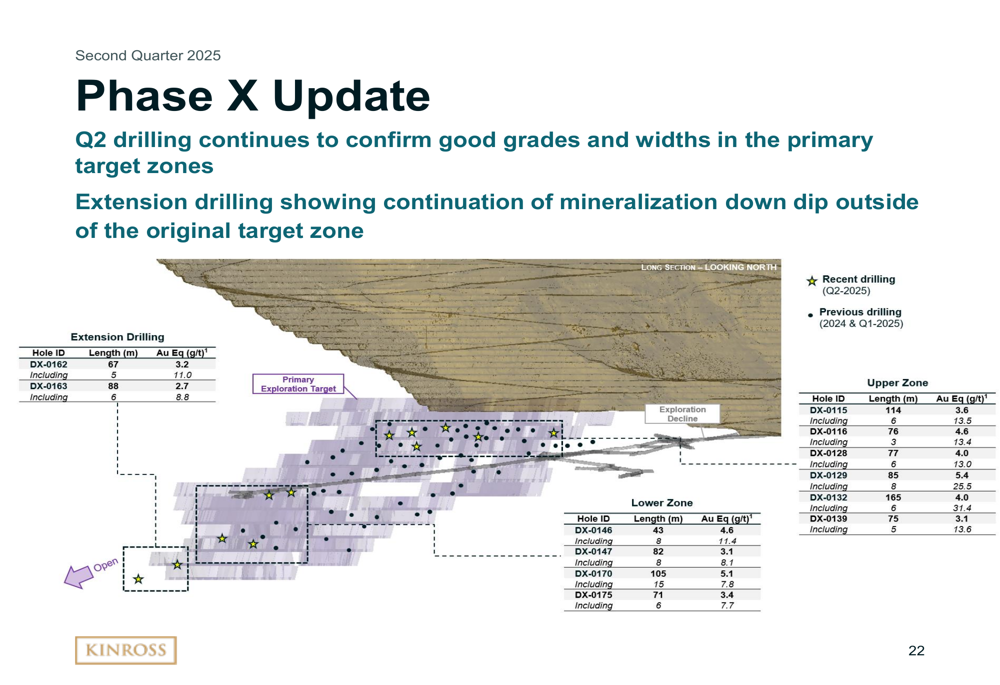

At Phase X, Q2 drilling confirmed good grades and widths in the primary target zones, with extension drilling showing continuation of mineralization down dip outside of the original target zone:

Forward-Looking Statements

Looking ahead, Kinross emphasized its strong production outlook, significant cash flow generation, and investment-grade balance sheet as key pillars of its strategy. The company remains committed to maintaining its attractive dividend and share buyback program while advancing its pipeline of exploration and development opportunities.

Management expects the positive momentum to continue in the second half of 2025, with operations on track to meet full-year guidance. The company’s transition to a net cash position in Q3 will mark an important milestone in its financial evolution and provide additional flexibility for future growth and shareholder returns.

With stable production projected through 2027 and multiple development projects advancing, Kinross appears well-positioned to capitalize on the current favorable gold price environment while maintaining its focus on operational excellence and disciplined capital allocation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.