BofA: Investors pour into bonds, pull back from crypto

Introduction & Market Context

KLA Corporation (NASDAQ:KLAC) reported its third-quarter fiscal 2025 results on April 30, 2025, showcasing robust financial performance driven by continued strength in semiconductor process control and expanding market leadership. The company’s stock closed at $687.95 before the earnings release and saw a 2.12% increase during regular trading.

The semiconductor equipment manufacturer continues to benefit from the industry’s increasing focus on advanced node technologies and the growing importance of process control in semiconductor manufacturing. KLA’s performance comes amid ongoing industry investment in AI-related semiconductor technologies and a gradual recovery in memory spending.

Quarterly Performance Highlights

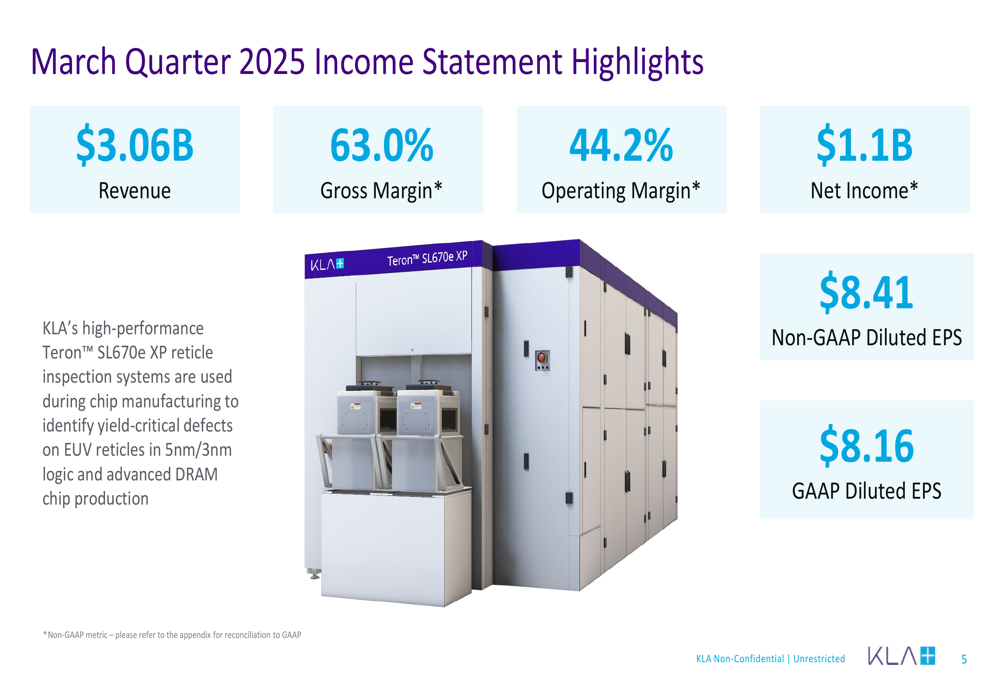

KLA reported revenue of $3.06 billion for the quarter ended March 31, 2025, representing a 30% year-over-year increase, though slightly down 0.4% sequentially. The company delivered impressive profitability with a non-GAAP gross margin of 63.0% and operating margin of 44.2%.

As shown in the following income statement highlights:

Non-GAAP diluted earnings per share reached $8.41, while GAAP diluted EPS came in at $8.16. Net income on a non-GAAP basis was $1.1 billion for the quarter. These results demonstrate KLA’s ability to maintain strong profitability even as it navigates a complex semiconductor equipment market.

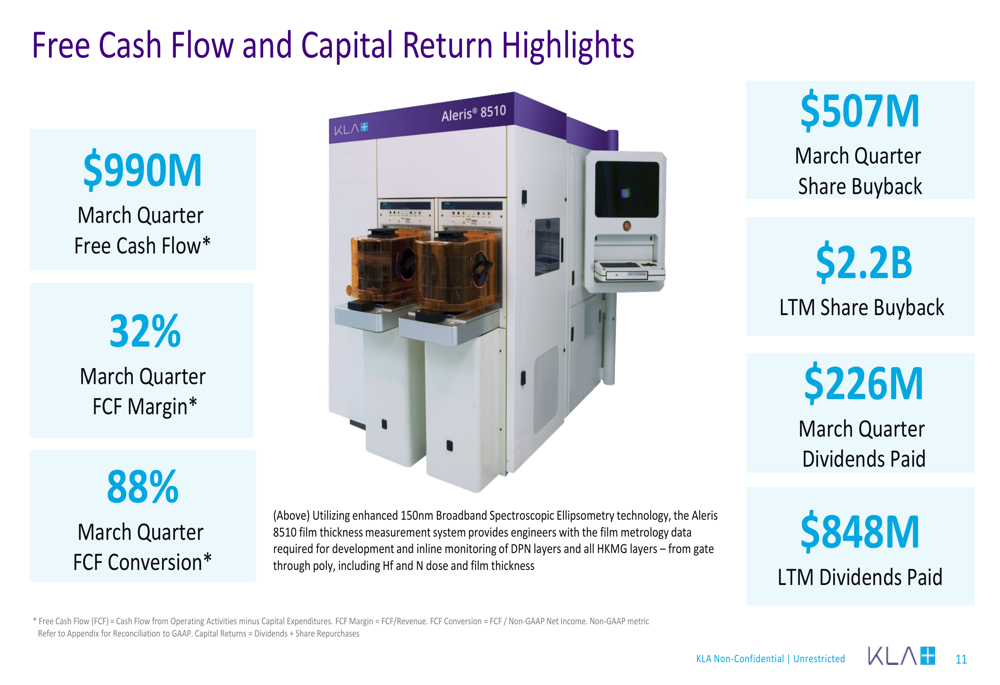

The company generated $990 million in free cash flow during the quarter, representing a 32% FCF margin and 88% FCF conversion rate. This robust cash generation supported KLA’s capital return program, with $507 million allocated to share repurchases and $226 million to dividends in the quarter.

Segment and Geographic Performance

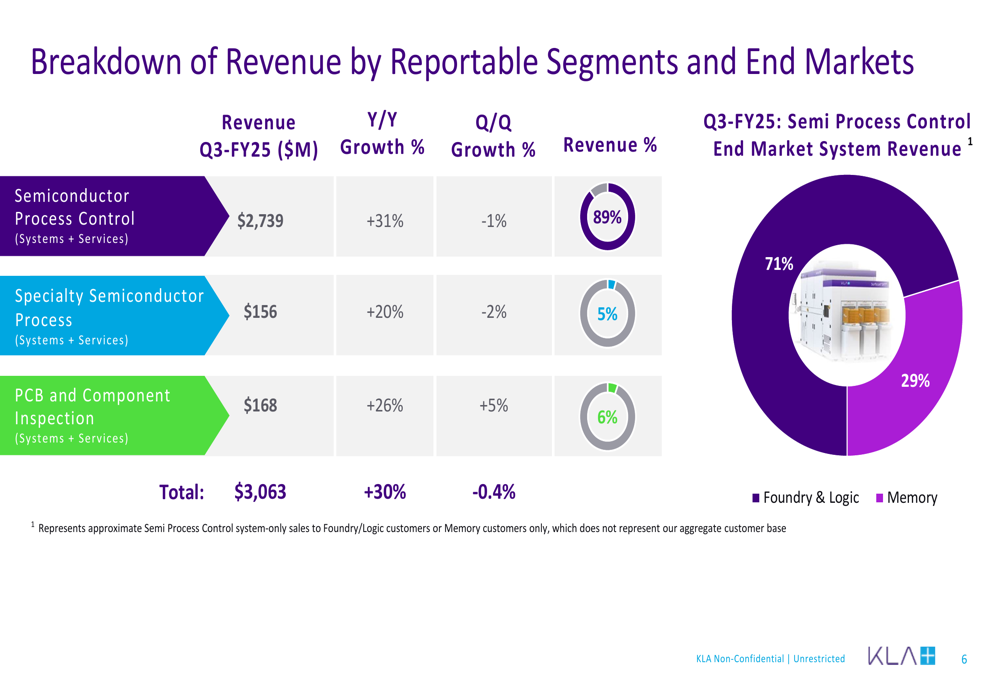

KLA’s Semiconductor Process Control segment, which includes both systems and services, continued to dominate the company’s revenue mix, contributing $2.74 billion or 89% of total revenue. This segment grew 31% year-over-year but declined slightly by 1% quarter-over-quarter.

The breakdown of revenue by reportable segments shows consistent growth across KLA’s business units:

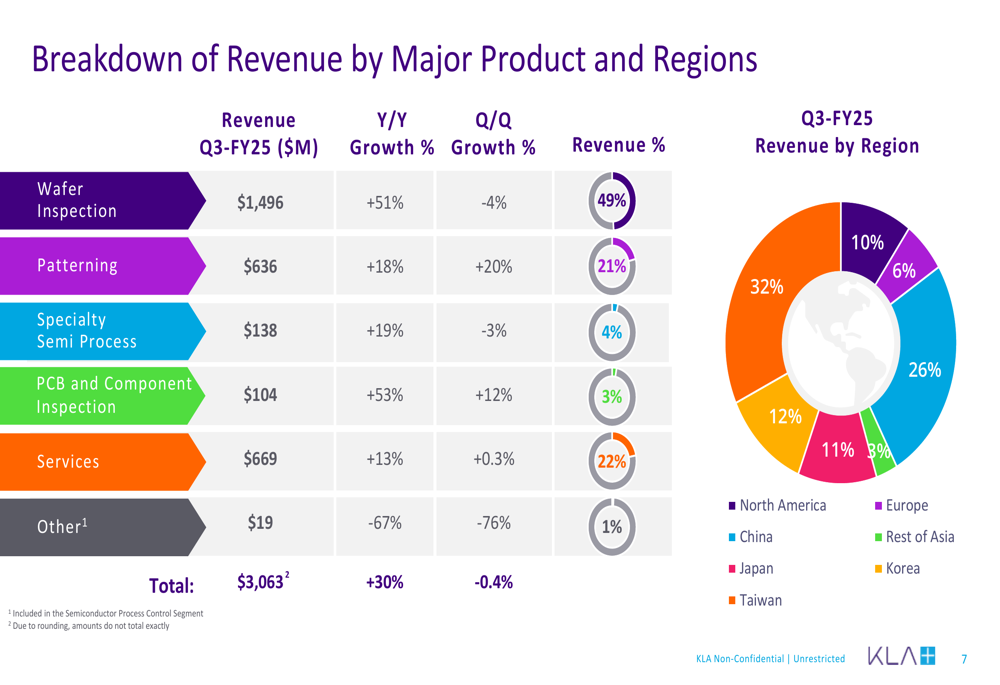

By product category, Wafer Inspection represented the largest portion of revenue at $1.5 billion (49%), growing an impressive 51% year-over-year. Patterning contributed $636 million (21%) with 18% year-over-year growth, while Services accounted for $669 million (22%) with 13% year-over-year growth.

Geographically, China remained KLA’s largest market at 32% of revenue, followed by Rest of Asia at 26%. This geographic distribution highlights KLA’s global footprint and the importance of Asian markets in the semiconductor equipment industry:

Market Leadership Position

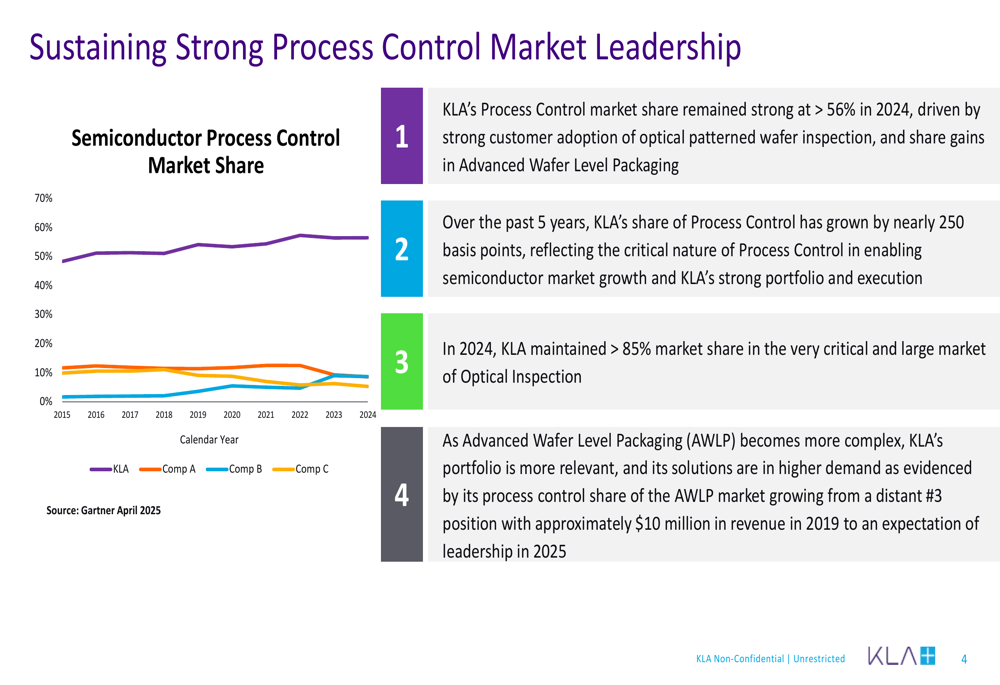

KLA continues to strengthen its dominant position in the semiconductor process control market. According to data presented, the company maintained over 56% market share in 2024, with its share growing by nearly 250 basis points over the past five years.

The company’s leadership is particularly strong in optical inspection, where it maintained over 85% market share in 2024. Additionally, KLA is making significant progress in the AWLP (Advanced Wafer-Level Packaging (NYSE:PKG)) market, expecting to move from a distant third position in 2019 to market leadership in 2025.

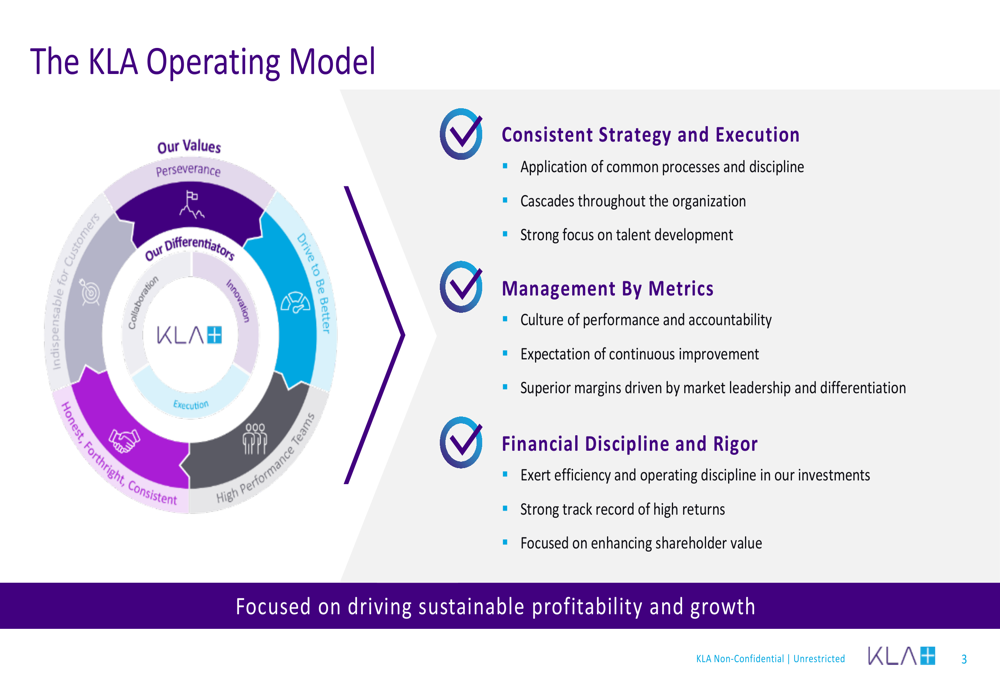

This market leadership is underpinned by KLA’s operating model, which emphasizes consistent strategy execution, performance accountability, and financial discipline. The company’s focus on innovation and customer collaboration continues to drive its competitive advantage in the semiconductor equipment market.

Capital Return and Balance Sheet Strength

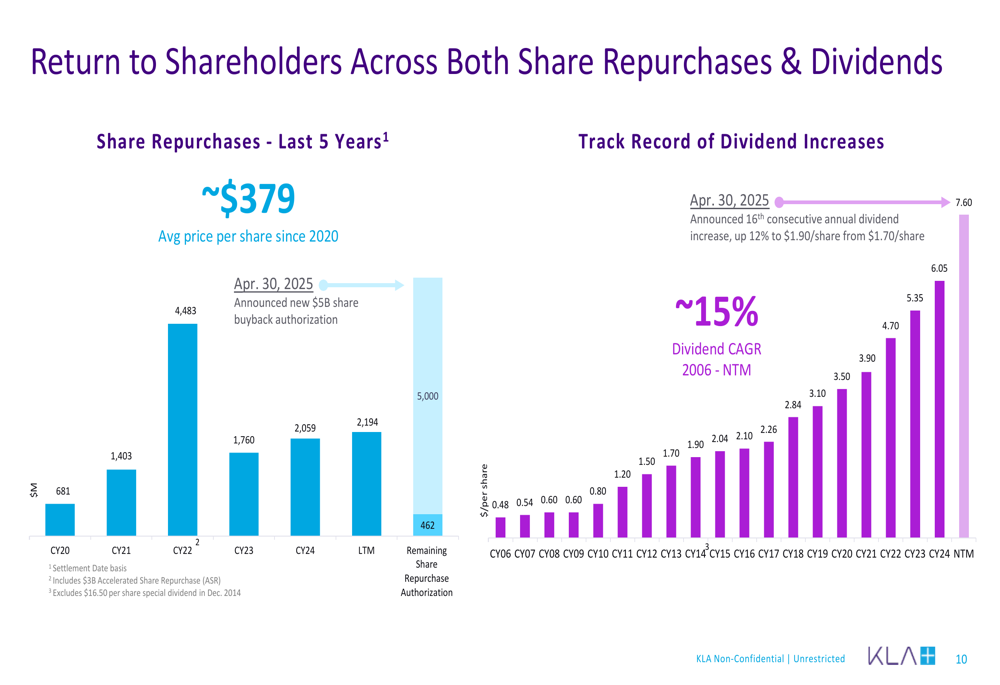

KLA announced a new $5 billion share repurchase authorization on April 30, 2025, reinforcing its commitment to returning capital to shareholders. The company also declared its 16th consecutive annual dividend increase, raising the quarterly dividend by 12% to $1.90 per share from $1.70.

Over the past five years, KLA has repurchased shares at an average price of $379 per share, demonstrating the company’s long-term approach to capital allocation. The dividend has grown at a compound annual growth rate of approximately 15% since 2006.

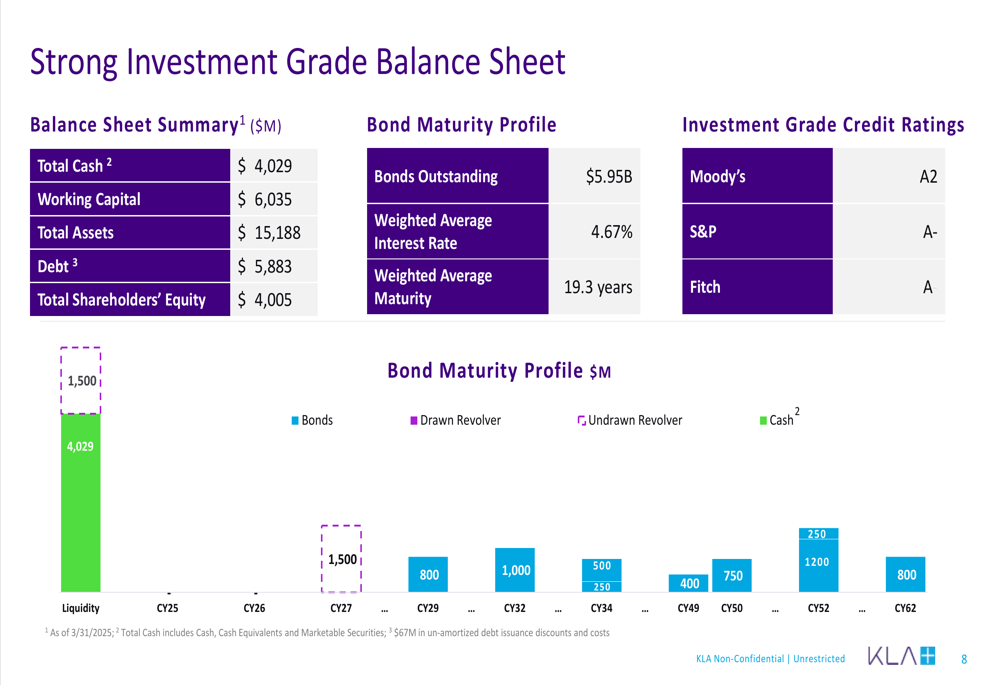

KLA maintains a strong investment-grade balance sheet with $4.03 billion in total cash and $5.88 billion in debt. The company’s weighted average interest rate on outstanding bonds is 4.67% with a weighted average maturity of 19.3 years. KLA holds investment-grade credit ratings from all major agencies: Moody’s (A2), S&P (A-), and Fitch (A).

Forward Guidance and Outlook

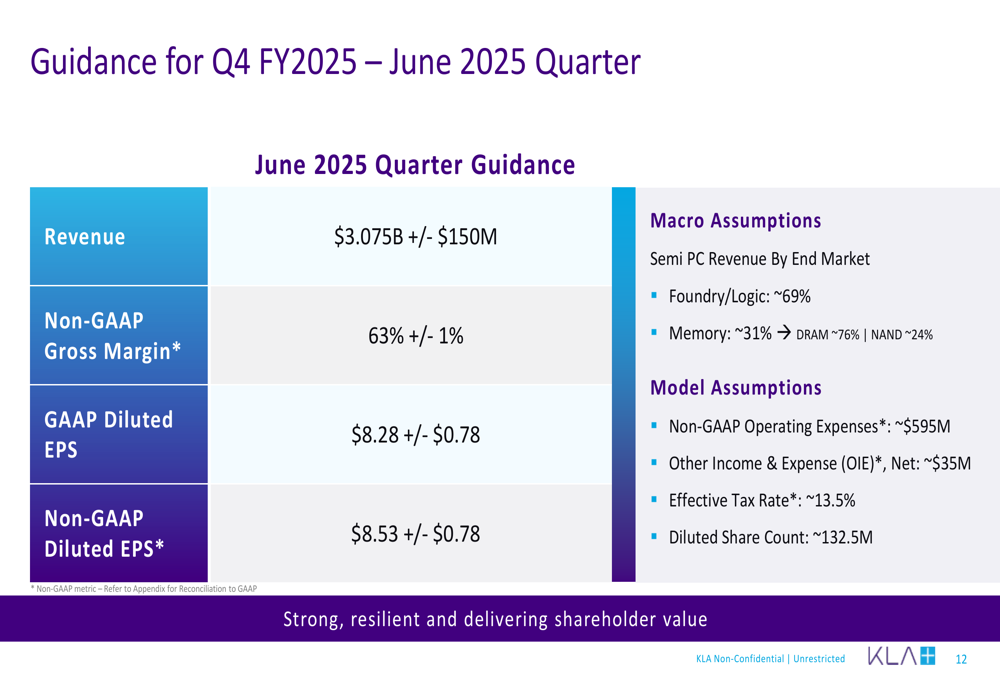

Looking ahead to the fourth quarter of fiscal 2025 (June 2025 quarter), KLA provided the following guidance:

The company expects revenue of $3.075 billion (±$150 million) and non-GAAP diluted EPS of $8.53 (±$0.78). The gross margin is projected to remain strong at 63% (±1%), consistent with the March quarter. KLA anticipates that Foundry/Logic will represent approximately 69% of Semiconductor Process Control revenue, with Memory accounting for the remaining 31%.

KLA’s consistent financial performance, strong market position, and robust capital return program position the company well for continued success in the semiconductor equipment market. The company’s focus on process control technologies remains critical as semiconductor manufacturers push toward more advanced nodes and complex designs to support AI and other emerging applications.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.