Microvast Holdings announces departure of chief financial officer

Introduction & Market Context

Knight-Swift Transportation (NYSE:KNX) released its second-quarter 2025 earnings presentation on July 23, showing significant year-over-year improvement in profitability metrics despite mixed segment performance. The company’s stock responded positively, trading up 1.35% to $45.79 in aftermarket trading following the results.

The transportation giant’s Q2 performance demonstrates a notable recovery from its first-quarter results, when the company missed EPS expectations and saw its stock decline. This quarter’s results suggest Knight-Swift’s cost reduction initiatives and operational efficiency measures are beginning to yield tangible benefits in a challenging transportation market.

Quarterly Performance Highlights

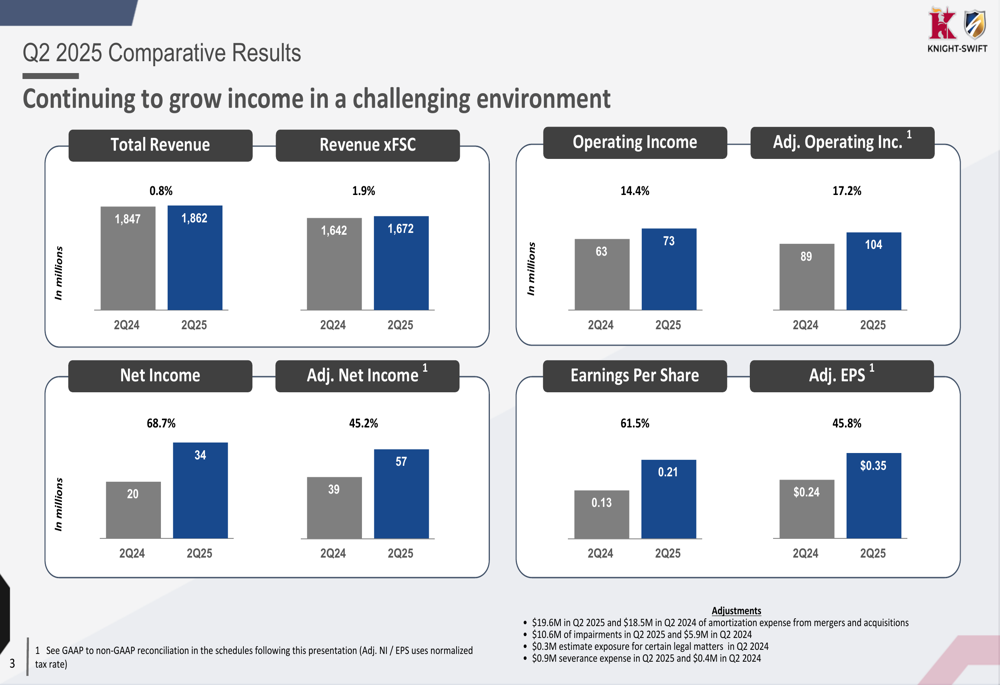

Knight-Swift reported total revenue of $1.86 billion for Q2 2025, a slight increase from $1.85 billion in the same period last year. More significantly, the company’s adjusted operating income rose to $104 million, up 16.9% from $89 million in Q2 2024.

Net income and earnings per share showed substantial year-over-year improvement. Adjusted net income reached $57 million, a 46.2% increase from $39 million in Q2 2024, while adjusted EPS jumped to $0.35, up 45.8% from $0.24 in the prior-year period.

As shown in the following comparative results chart:

The company’s adjusted results exclude several non-recurring items, including amortization expenses from mergers and acquisitions, impairments, legal matters, and severance expenses, providing a clearer picture of underlying operational performance.

Segment Performance Analysis

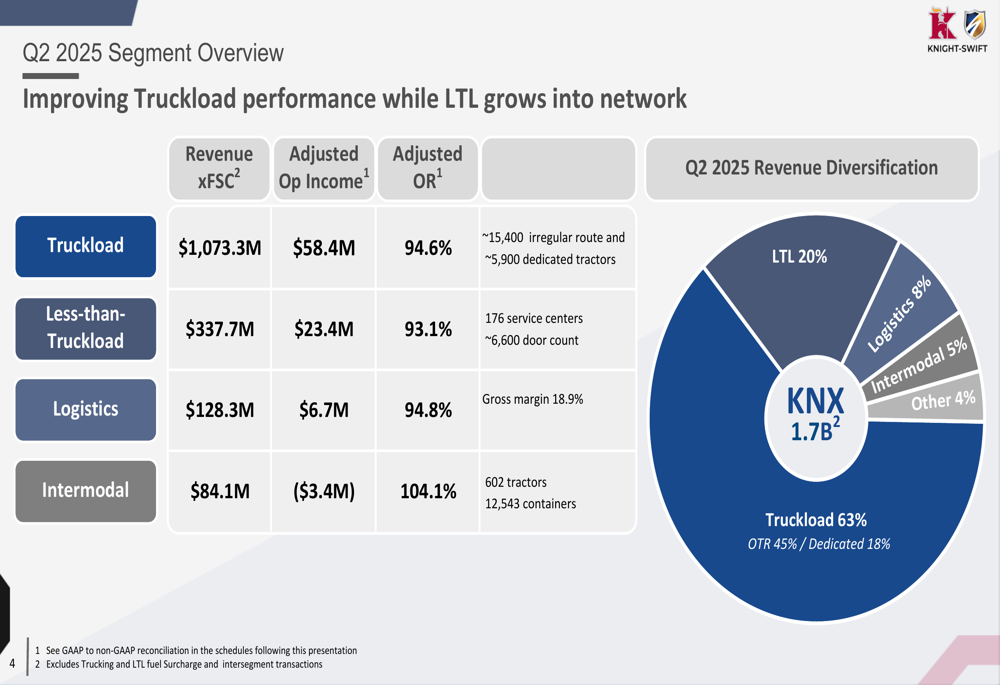

Knight-Swift’s business remains diversified across multiple transportation segments, with Truckload operations accounting for 63% of revenue, followed by Less-than-Truckload (LTL) at 20%, Logistics at 8%, and Intermodal at 5%.

The segment breakdown reveals varying performance across the company’s business units:

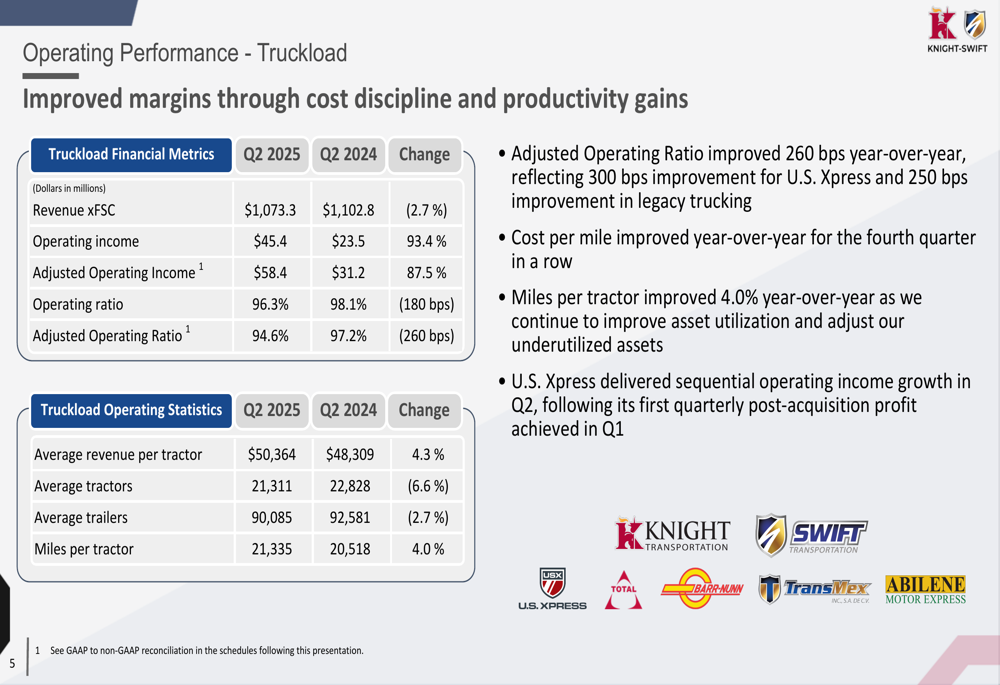

The Truckload segment, Knight-Swift’s largest business unit, demonstrated significant improvement with adjusted operating income of $58.4 million and an adjusted operating ratio of 94.6%, a 260 basis point improvement year-over-year. This improvement came despite a slight revenue decline, highlighting the effectiveness of cost control measures.

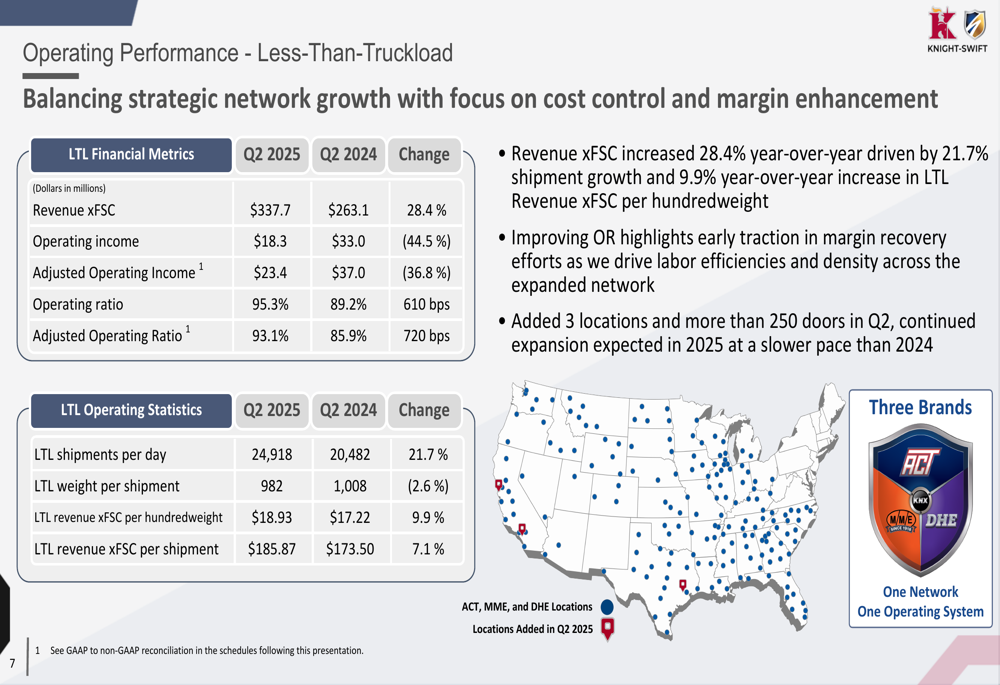

The Less-than-Truckload segment showed strong revenue growth of 28.4% year-over-year, reaching $337.7 million. However, profitability in this segment declined, with adjusted operating income falling to $23.4 million from $37.0 million and adjusted operating ratio deteriorating to 93.1% from 85.9% in Q2 2024.

The Logistics segment maintained relatively stable performance with revenue of $128.3 million and a 70 basis point improvement in adjusted operating ratio to 94.8%. Meanwhile, the Intermodal segment continued to struggle, posting an operating loss of $3.4 million and an operating ratio of 104.1%.

Strategic Initiatives

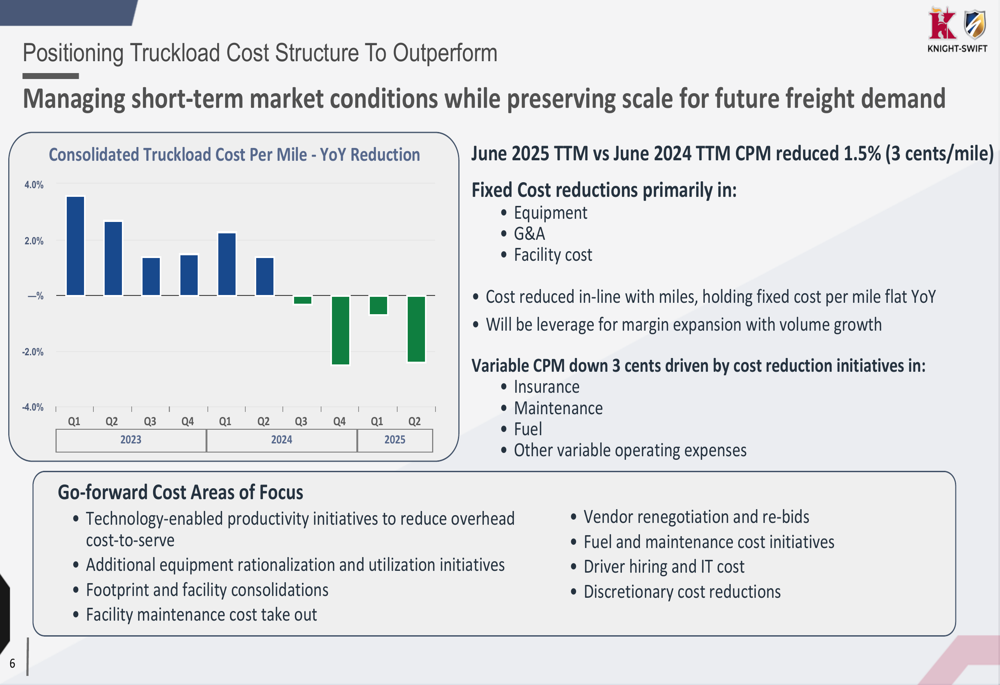

Knight-Swift’s presentation highlighted its focus on cost reduction initiatives, particularly within the Truckload segment. The company reported a 1.5% reduction in cost per mile for the trailing twelve months ended June 2025 compared to the same period in 2024.

These cost improvements were achieved through multiple initiatives targeting both fixed and variable expenses:

Management identified four key areas for continued cost reduction: technology-enabled productivity, equipment rationalization, facility consolidations, and maintenance cost optimization. These initiatives appear to be gaining traction, particularly in the Truckload segment where adjusted operating ratio improved significantly despite revenue pressure.

The company also noted that U.S. Xpress, acquired in 2023, delivered sequential operating income growth in Q2, suggesting the integration of this acquisition is progressing positively.

Forward-Looking Statements

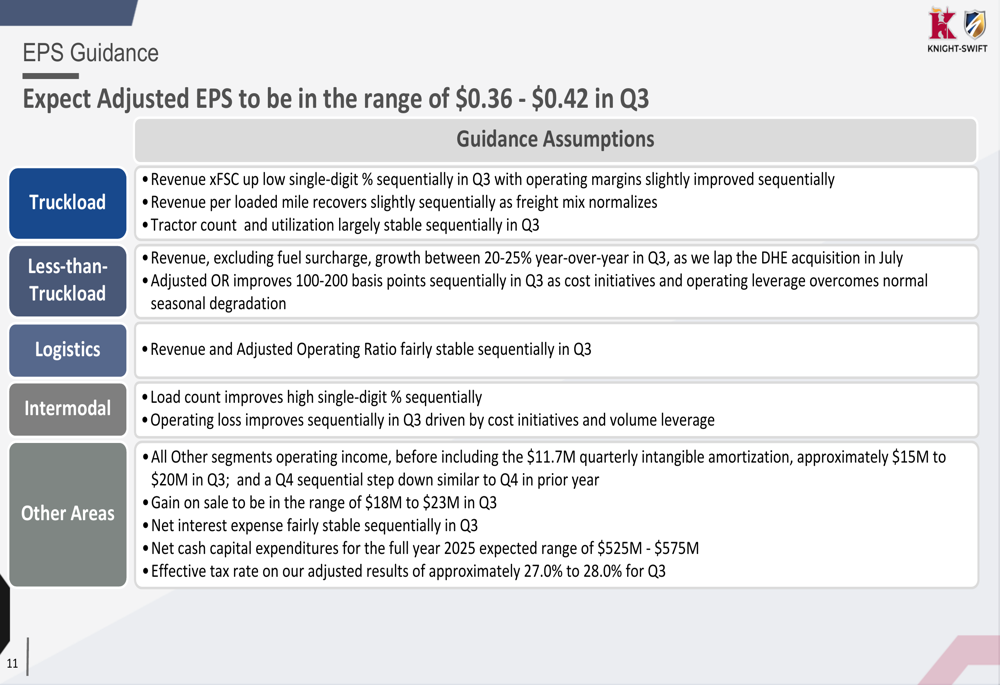

Looking ahead, Knight-Swift provided adjusted EPS guidance of $0.36 to $0.42 for the third quarter of 2025, suggesting continued sequential improvement from Q2’s $0.35.

The guidance is based on specific assumptions for each business segment:

This guidance represents a significant improvement from the company’s Q1 2025 performance when it reported adjusted EPS of $0.28 and missed analyst expectations. The projected Q3 range also suggests management expects the positive momentum in cost control and operational efficiency to continue.

Market Perspective

Knight-Swift’s Q2 results and Q3 guidance appear to have reassured investors after a challenging first quarter. The stock, which had declined 25.08% year-to-date following Q1 results, showed signs of recovery with the positive aftermarket reaction to Q2 earnings.

The company’s focus on cost reduction and operational efficiency seems well-timed given the uncertain market conditions referenced in previous earnings calls, including trade policy uncertainties and potential impacts on container imports.

While challenges remain, particularly in the Intermodal segment and with margin pressure in the growing LTL business, Knight-Swift’s diversified business model and demonstrated ability to improve profitability through cost control position the company to navigate the current transportation market environment.

The sequential improvement from Q1 to Q2 and the positive guidance for Q3 suggest Knight-Swift may be turning the corner after a difficult start to 2025, though investors will likely continue monitoring segment performance closely, particularly the ongoing integration of acquisitions and the profitability trajectory of the expanding LTL business.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.