Boeing secures $883 million Army contract for cargo support services

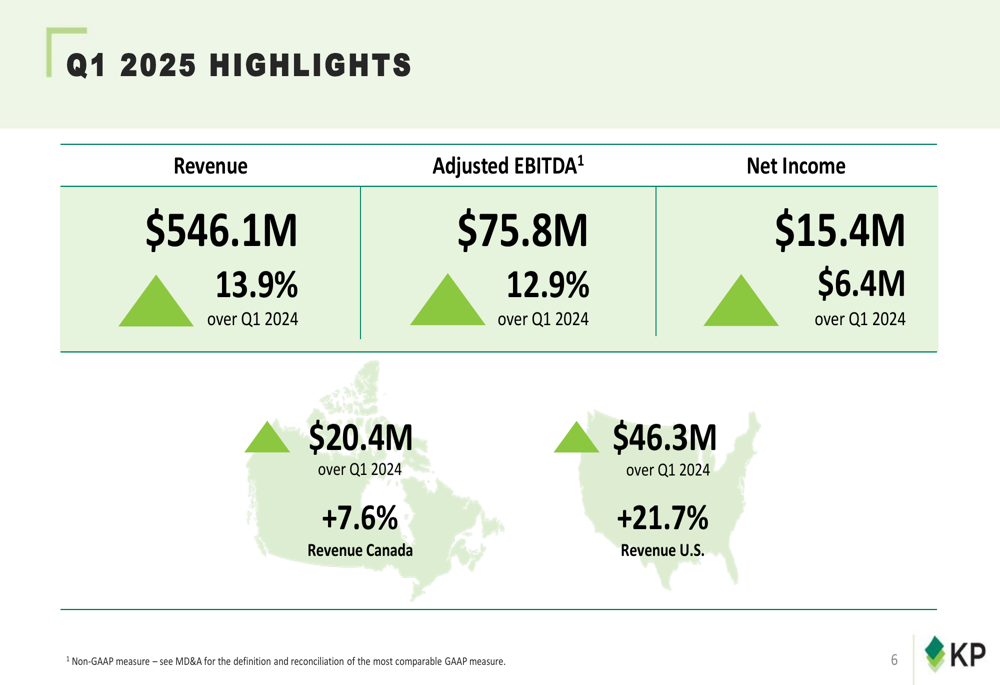

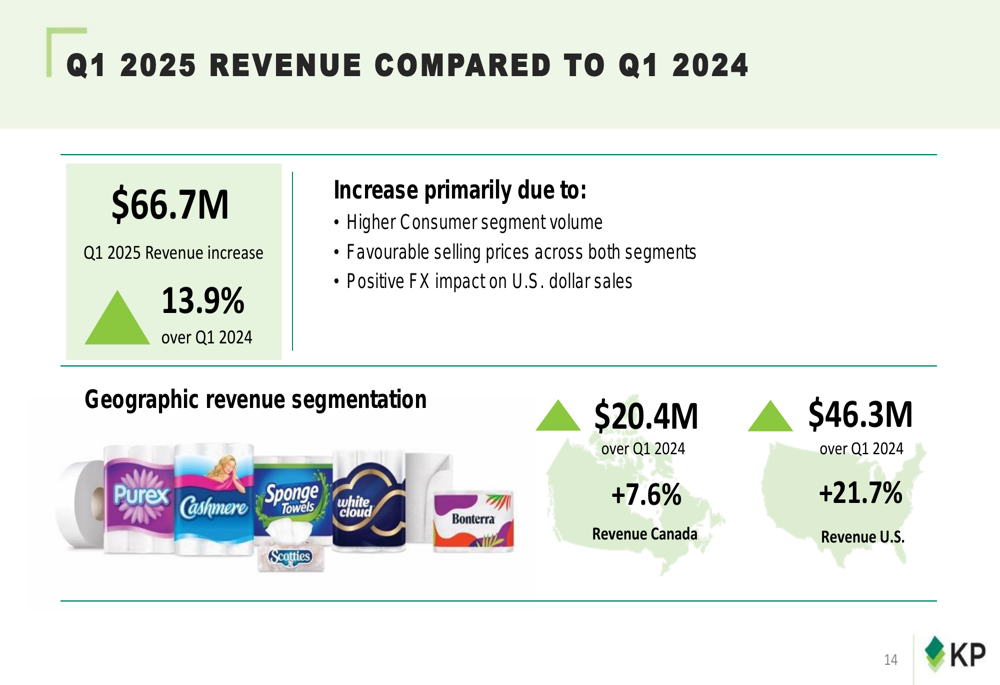

KP Tissue Inc (TSX:KPT) reported strong first-quarter results on May 14, 2025, with revenue increasing 13.9% year-over-year to $546.1 million, driven primarily by robust growth in the U.S. market and improved selling prices across segments. The company’s shares closed at $8.39 on May 13, near its 52-week high of $8.65.

Quarterly Performance Highlights

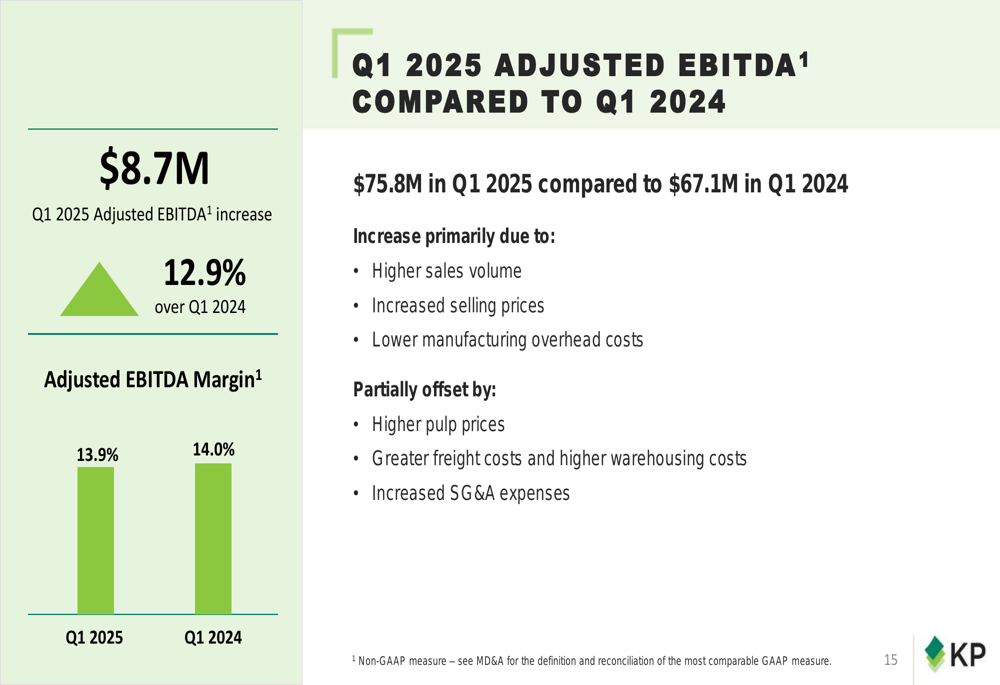

KP Tissue delivered significant improvements across key financial metrics in Q1 2025. Net income reached $15.4 million, a substantial rebound from the $13.7 million loss reported in Q4 2024 and $6.4 million higher than Q1 2024. Adjusted EBITDA grew 12.9% year-over-year to $75.8 million, with margins holding steady at 13.9% compared to 14.0% in the prior-year period.

As shown in the following financial highlights:

The company’s growth was geographically uneven, with U.S. revenue surging 21.7% ($46.3 million) compared to Q1 2024, while Canadian revenue increased by a more modest 7.6% ($20.4 million). This geographic disparity highlights KP Tissue’s expanding footprint in the U.S. market.

Segment Analysis

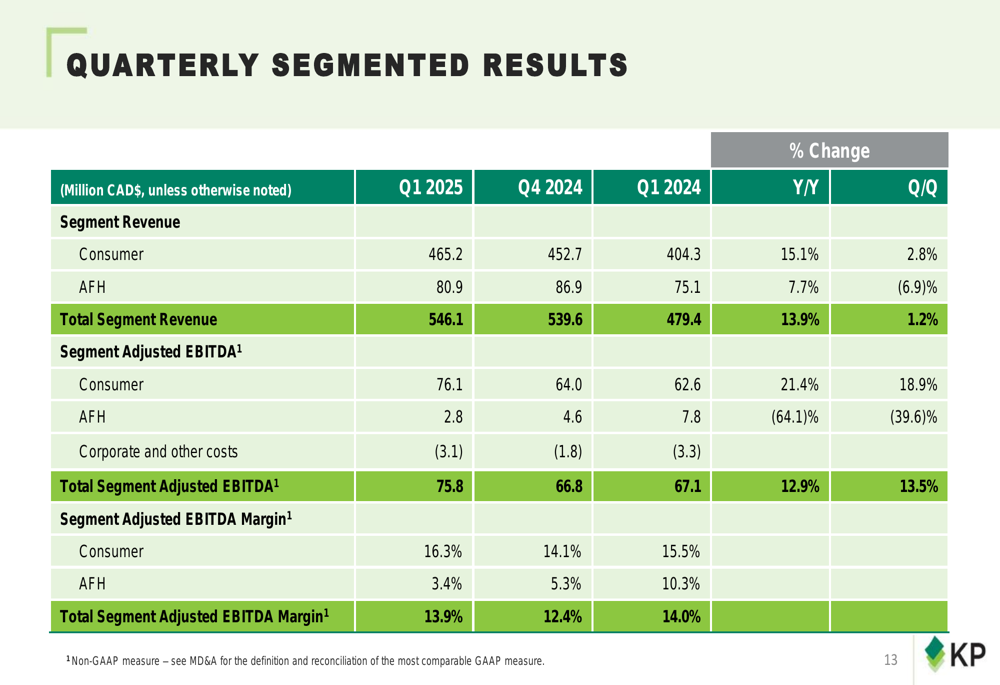

KP Tissue’s segment performance showed a stark contrast between its Consumer and Away-From-Home (AFH) divisions. The Consumer segment posted impressive results with a 15.1% year-over-year revenue increase to $465.2 million and a 21.4% jump in Adjusted EBITDA to $76.1 million. Conversely, the AFH segment struggled with profitability despite 7.7% revenue growth, as its Adjusted EBITDA plummeted 64.1% to $2.8 million.

The segmented results reveal the diverging performance trajectories:

Management attributed the AFH segment’s profitability challenges to higher costs for externally purchased products and paper. However, they noted that the successful startup of the Sherbrooke paper machine is expected to improve margins starting in Q2 2025. The company also plans to launch Cashmere and Scotties brands for the commercial market in June, potentially strengthening its AFH positioning.

Operational Updates and Market Position

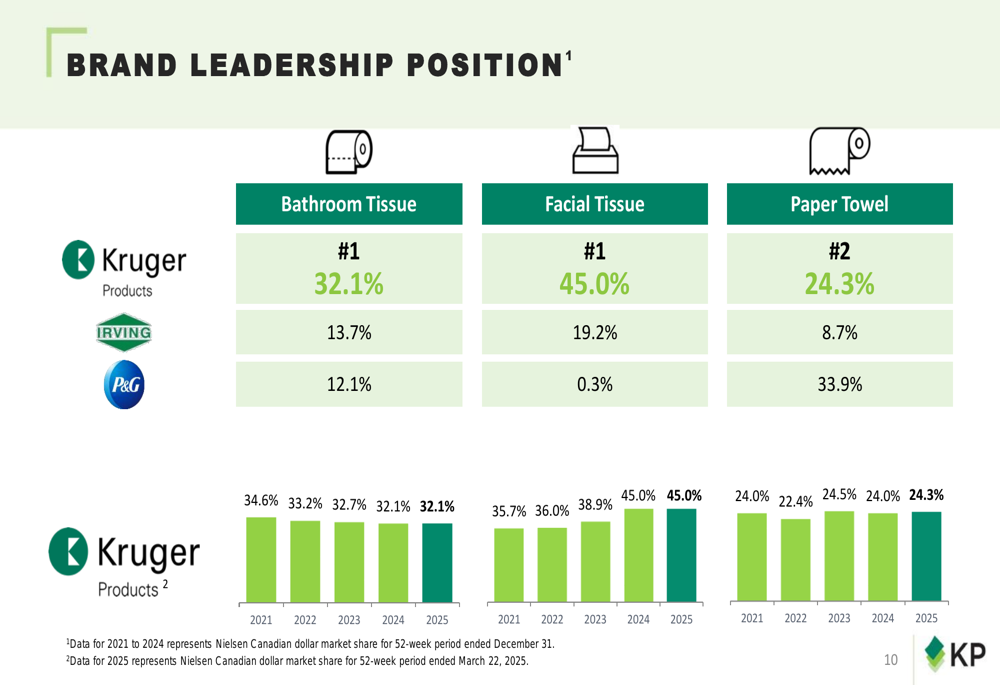

KP Tissue maintains dominant market positions in Canada, holding the #1 spot in both Bathroom Tissue (32.1% market share) and Facial Tissue (45.0%), while ranking #2 in Paper Towel (24.3%). These strong market positions provide a solid foundation for the company’s growth strategy.

The following chart illustrates KP Tissue’s market leadership:

On the operational front, the company reported that production rates exceeded forecasts in Q1, with particularly strong performance from new assets. The new LDC paper machine and facial converting assets are surpassing start-up expectations, while the TAD paper machine and converting output remains strong year-over-year. Management expects production increases for the remainder of 2025 as new assets reach their maturity curve.

Cost Pressures and Margin Management

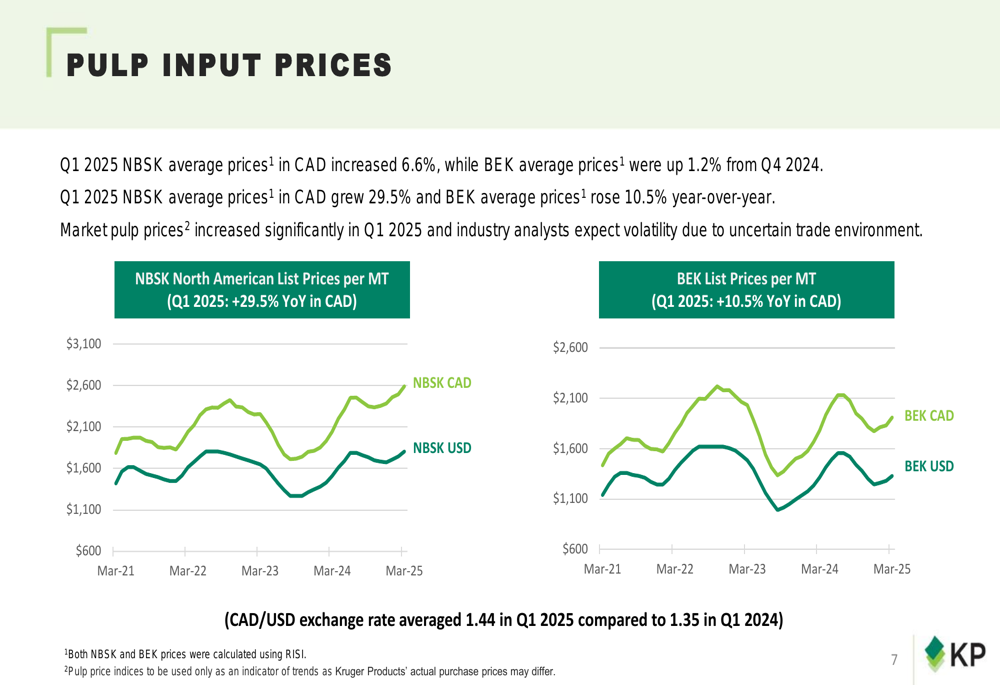

Rising pulp prices presented a significant challenge in Q1 2025, with NBSK pulp prices increasing 29.5% year-over-year and BEK pulp prices up 10.5%. The company also faced pressure from a weaker Canadian dollar, with the CAD/USD exchange rate averaging 1.44 in Q1 2025 compared to 1.35 in Q1 2024.

The following chart shows the pulp price trends affecting the company’s cost structure:

Despite these cost pressures, KP Tissue successfully expanded its Adjusted EBITDA by 12.9% year-over-year, primarily through higher sales volume, increased selling prices, and lower manufacturing overhead costs. These positive factors outweighed the negative impacts of higher pulp prices, increased freight and warehousing costs, and greater SG&A expenses.

Financial Position and Capital Allocation

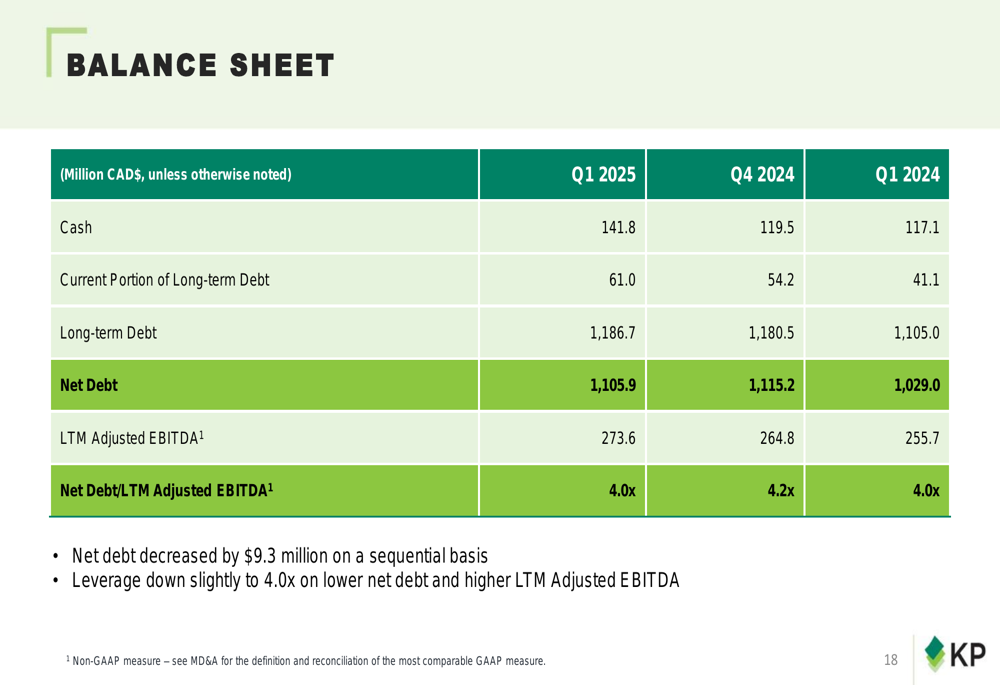

KP Tissue’s balance sheet showed improvement in Q1 2025, with cash increasing to $141.8 million from $119.5 million in Q4 2024. Net debt decreased by $9.3 million sequentially to $1,105.9 million, helping to reduce the leverage ratio to 4.0x from 4.2x in the previous quarter.

Capital expenditures totaled $17.5 million in Q1 2025, including $15.4 million related to the Sherbrooke Expansion Project. The company anticipates total CAPEX of $80-$100 million for 2025, continuing its investment in growth initiatives while managing leverage.

Sustainability and Strategic Initiatives

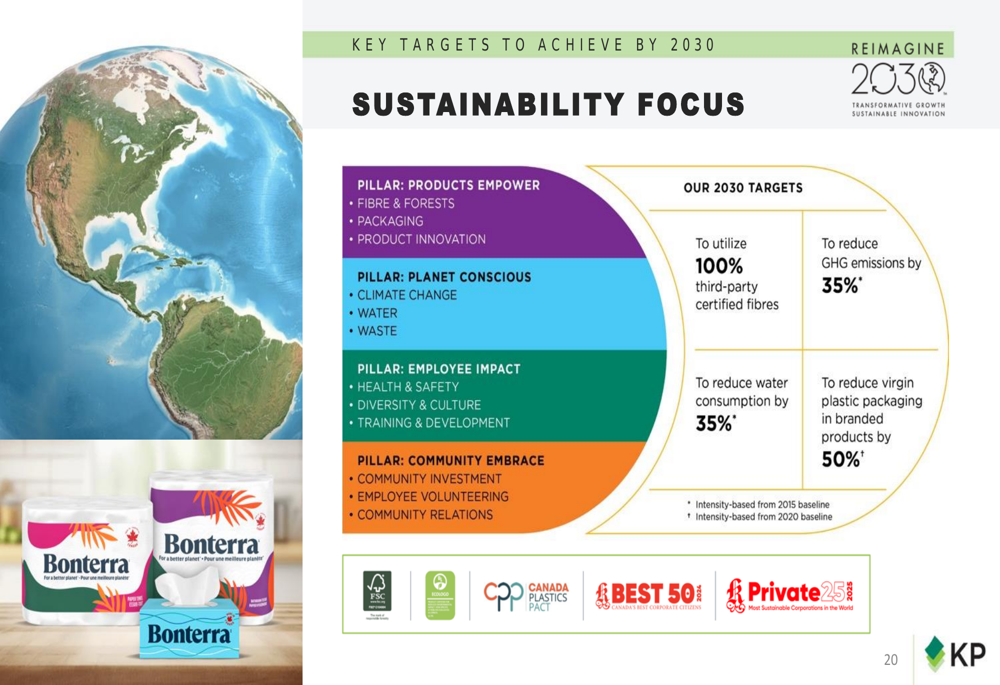

KP Tissue outlined ambitious sustainability targets for 2030, structured around four pillars: Products Empower, Planet Conscious, Employee Impact, and Community Embrace. Key goals include utilizing 100% third-party certified fibers, reducing GHG emissions by 35% from 2015 levels, cutting water consumption by 35%, and reducing virgin plastic packaging in branded products by 50% from 2020 levels.

The company’s sustainability roadmap is illustrated below:

Looking ahead, management expects continued strong growth in U.S. sales while monitoring the trade environment and leveraging its "Made in Canada" positioning. The company plans to manage margins amid a changing cost base, invest in brands to drive long-term market share, and significantly reduce reliance on purchased paper with the Sherbrooke LDC paper machine.

Forward Outlook

KP Tissue’s management expressed confidence in the company’s growth trajectory, particularly in the U.S. market. The successful startup of new production facilities is expected to drive operational efficiencies and margin improvements throughout 2025, especially in the AFH segment.

While the company faces challenges from rising pulp prices and potential trade uncertainties, its strong market positions, brand investments, and operational improvements position it well for continued growth. The rebound in net income from Q4 2024’s loss to Q1 2025’s $15.4 million profit demonstrates KP Tissue’s ability to navigate a complex market environment while delivering improved financial results.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.