Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Kraft Bank ASA (KRAB) presented its second-quarter 2025 results on August 14, 2025, showcasing significant profit growth and continued success with its unique business model focused on helping customers with financial challenges. The bank’s stock closed at 11.50 NOK on August 13, up 4.55% and approaching its 52-week high of 11.70 NOK, reflecting positive market sentiment ahead of the results.

Kraft Bank, which describes itself as "a mortgage bank for people with economic challenges," has built its business around helping customers refinance out of financial difficulties and eventually return to mainstream banking services.

Quarterly Performance Highlights

Kraft Bank reported a profit after tax of 16.6 million NOK for Q2 2025, representing a dramatic 538% increase from the 2.6 million NOK reported in the same period of 2024. The company noted that its year-to-date profit in 2025 has already exceeded the entire year of 2024.

Return on equity after tax reached 14.1% in Q2 2025, compared to just 2.3% in Q2 2024, approaching the bank’s stated goal of 15% ROE by year-end 2025. Interest income from lending grew by 27% compared to Q2 2024, demonstrating strong core business performance.

As shown in the following financial performance highlights from the presentation:

The bank reported book equity per share of 11.22 NOK at the end of the quarter. Capital adequacy stood at 24.8% for Q2, well above the applicable capital requirement of 23.7% (including management buffer). When including results from this year, capital adequacy improves further to 26.4%.

Social Impact Business Model

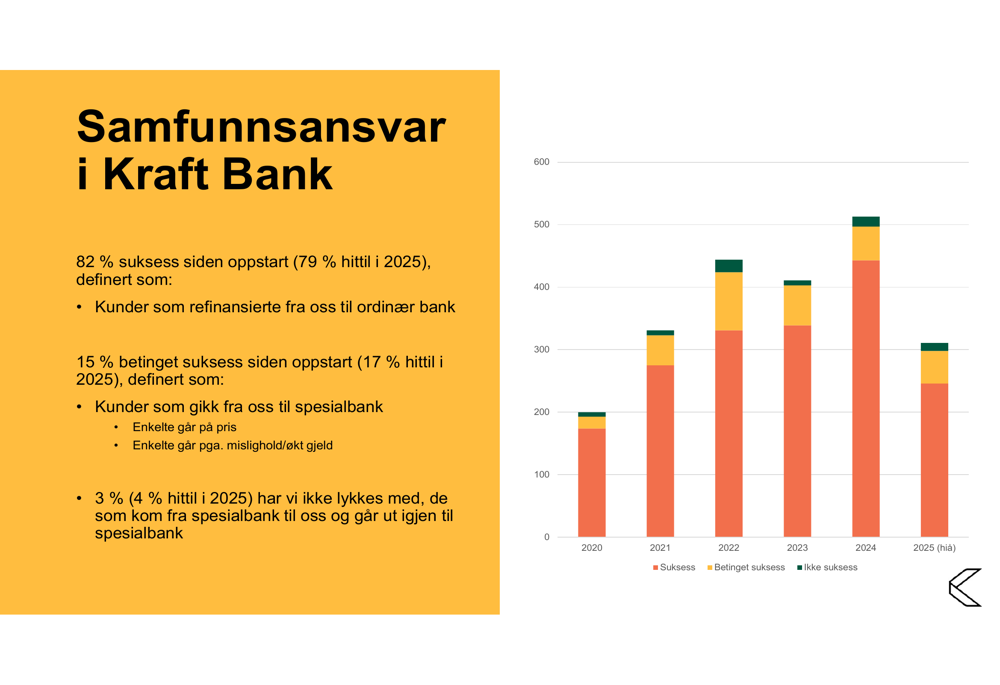

Kraft Bank’s business model is built around helping people overcome financial difficulties. Since its inception in 2018, the bank has helped 2,244 customers "recover" financially, with 150 customers achieving this milestone in the last quarter alone.

The bank measures its success through customer refinancing outcomes. As illustrated in the following chart, 82% of customers have successfully refinanced from Kraft Bank to an ordinary bank, which the company defines as a "success." Another 15% have achieved what the bank calls "contingent success," defined as customers who have moved to another specialized bank.

The bank emphasizes that when it helps customers avoid forced sale of their homes, families retain their residences and gain opportunities for fresh financial starts, positively impacting both individuals and local communities.

Detailed Financial Analysis

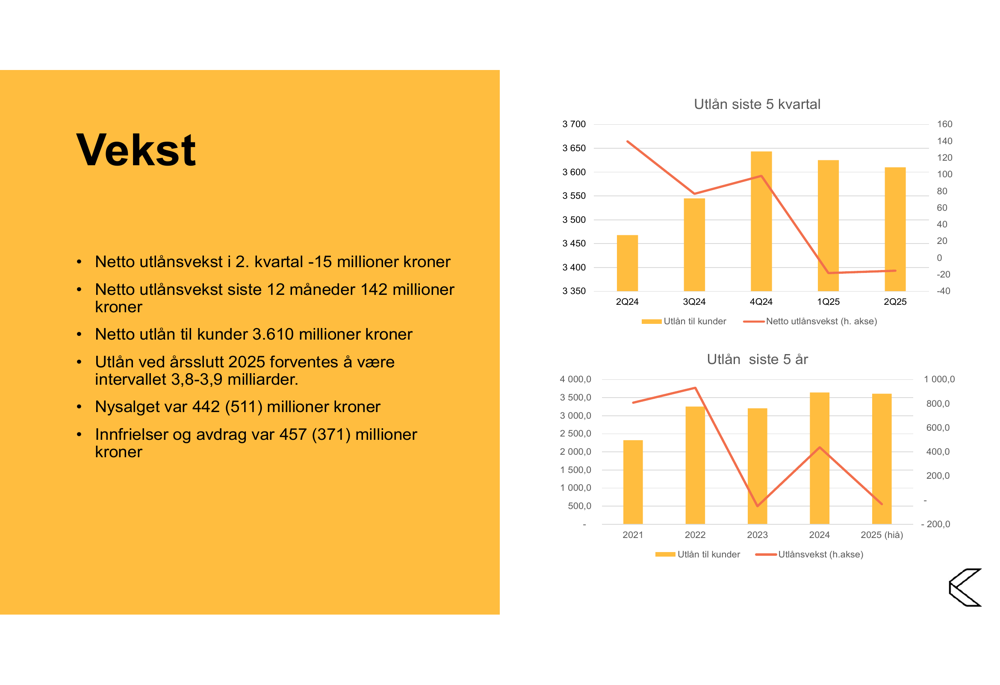

Kraft Bank’s loan portfolio showed modest movement in Q2 2025, with net lending declining by 15 million kroner during the quarter. However, the 12-month growth remains positive at 142 million kroner, bringing net loans to customers to 3,610 million kroner. The bank expects loans to reach between 3.8-3.9 billion kroner by year-end 2025.

The following chart illustrates the bank’s lending volume trends over recent quarters and years:

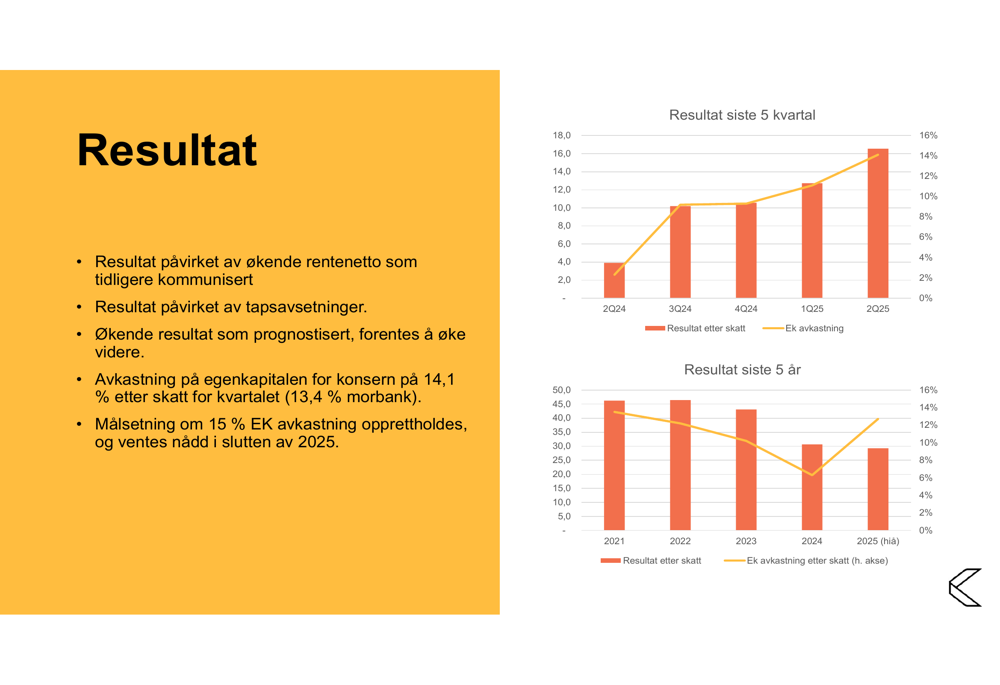

Profit performance has shown consistent improvement over recent quarters, as demonstrated in the following graph:

The bank attributes its improving results to increasing net interest income and good cost control, though results were partially offset by loss appropriations. Management expects profit to continue increasing through the remainder of 2025.

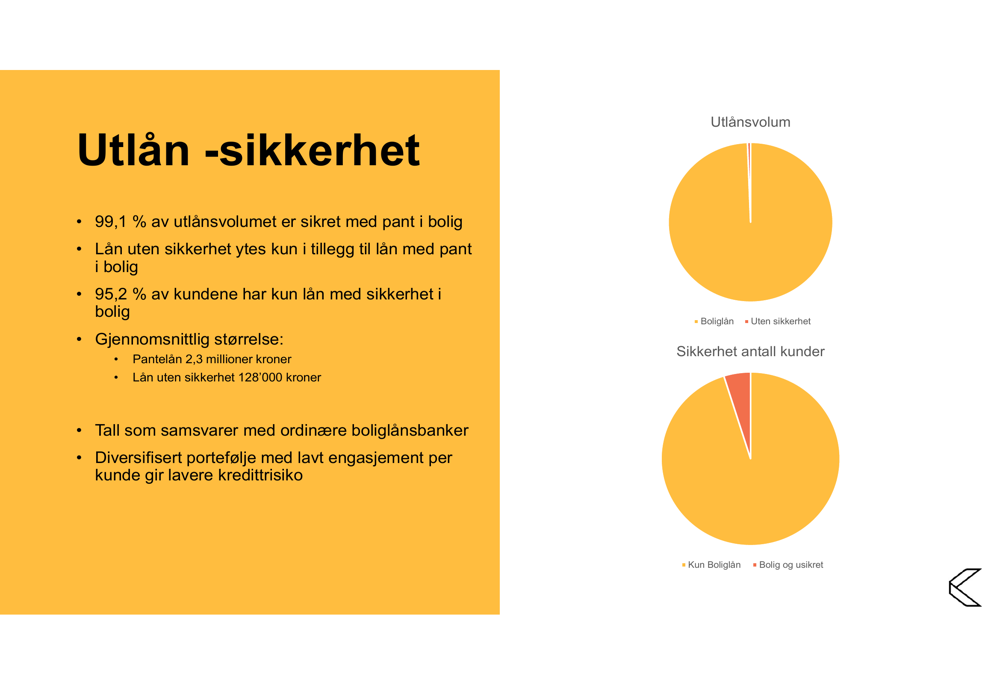

Kraft Bank maintains a conservative approach to loan security, with 99.1% of loan volume secured by mortgages. The average secured loan size is 2.3 million kroner, while unsecured loans (only provided alongside mortgage-backed loans) average 128,000 kroner.

The following charts illustrate the bank’s loan security distribution:

The bank’s loan portfolio shows prudent risk management, with 79% of loans under 6 million kroner and 94% of loans under 85% loan-to-value (LTV). The volume-weighted average LTV stands at 65.5%, with property values updated quarterly.

Forward-Looking Statements

Kraft Bank maintains its goal of achieving 15% return on equity by the end of 2025. The bank expects loans to reach between 3.8-3.9 billion kroner by year-end 2025, with continued normal cost development in line with inflation and wage settlements.

Management anticipates steady increases in earnings as loans with interest guarantees roll off the books. The bank plans some system upgrades in 2025 but notes these will not materially affect results as investments are amortized over three years.

Capital requirements are expected to remain stable, with the bank’s capital plan including potential issuance of fund obligations, revision of interim results, retained surplus, reduced growth, and possible additional equity to maintain strong capital adequacy.

As the bank continues to execute its unique business model of helping financially challenged customers, its financial performance appears to be accelerating, with Q2 2025 showing substantial improvement across key metrics compared to the previous year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.