Behind US stock gains, gold’s climb reflects growing market uncertainty: Macquarie

Introduction & Market Context

Kroger Company (NYSE:KR) released its Q2 2025 earnings presentation on September 11, 2025, showcasing solid performance across key metrics and prompting management to raise full-year guidance. The grocery giant’s shares responded positively in premarket trading, rising 1.94% to $68.33, as investors digested results that demonstrated resilience in the competitive grocery sector.

The company’s performance comes amid a challenging retail environment where consumer spending patterns continue to evolve. Following a strong Q1 where Kroger beat EPS expectations, the Q2 results further cement the company’s strategic positioning in both physical and digital retail channels.

Quarterly Performance Highlights

Kroger delivered robust Q2 2025 results, with identical sales excluding fuel increasing by 3.4%, demonstrating stronger growth compared to the 3.2% reported in Q1. The company’s digital transformation continues to gain momentum, with eCommerce sales growing by 16% year-over-year.

As shown in the following quarterly results summary:

The company reported GAAP earnings per share of $0.91 and adjusted EPS of $1.04, representing 12% growth. While this marks a sequential decline from the $1.49 EPS reported in Q1, it reflects typical quarterly seasonality in the grocery business. GAAP operating profit reached $863 million, while adjusted FIFO operating profit was significantly higher at $1,091 million.

Revised Guidance & Outlook

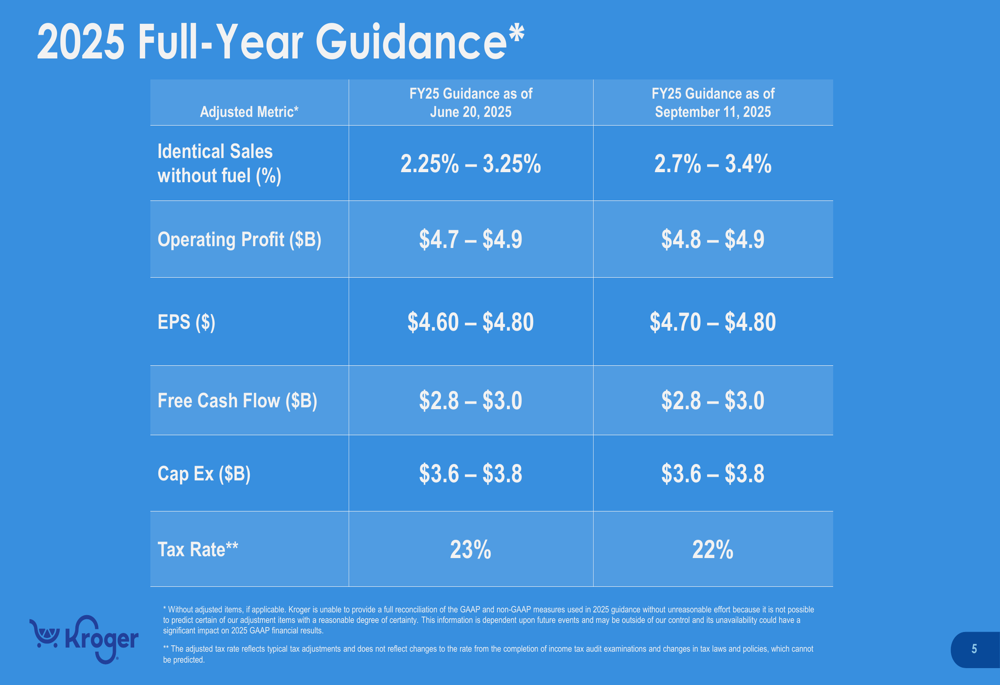

Based on the strong Q2 performance, Kroger has revised its full-year 2025 guidance upward across several key metrics. The company now expects identical sales without fuel to grow between 2.7% and 3.4%, up from the previous range of 2.25% to 3.25% provided in June.

The updated guidance demonstrates management’s increasing confidence in Kroger’s business model and execution capabilities:

Operating profit expectations have been tightened to the upper end of the previous range, now projected at $4.8 to $4.9 billion. Similarly, EPS guidance has been raised to $4.70-$4.80 from the previous $4.60-$4.80 range. The company maintained its free cash flow projection of $2.8-$3.0 billion and capital expenditure plans of $3.6-$3.8 billion, while lowering its expected tax rate to 22% from 23%.

Strategic Growth Initiatives

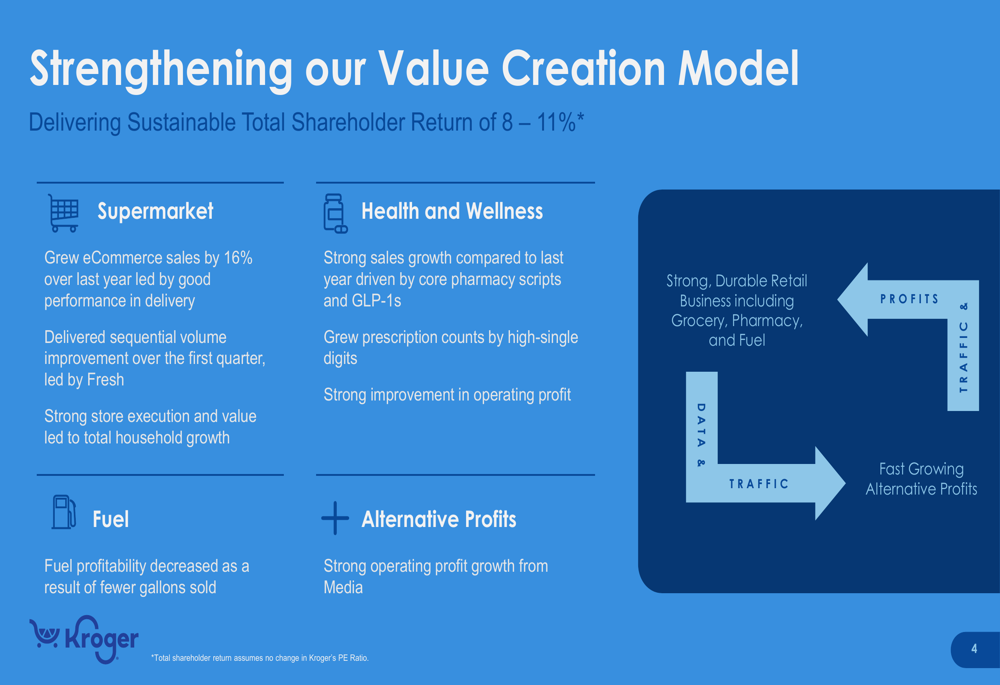

Kroger’s presentation highlighted its value creation model, which focuses on leveraging its core supermarket business while expanding into higher-growth areas. The strategy emphasizes three key pillars that work together to drive sustainable shareholder returns.

The company’s value creation model illustrates how these elements interconnect:

In the supermarket segment, Kroger is seeing sequential volume improvement led by fresh categories, while strong store execution is driving household growth. The Health and Wellness division is experiencing robust growth from pharmacy prescriptions, particularly noting the impact of GLP-1 medications, with prescription count growth in high single digits.

While fuel profitability decreased due to lower gallons sold, Kroger’s alternative profit streams, particularly its Media business, delivered strong operating profit growth. This diversification helps offset challenges in traditional segments and provides additional growth avenues.

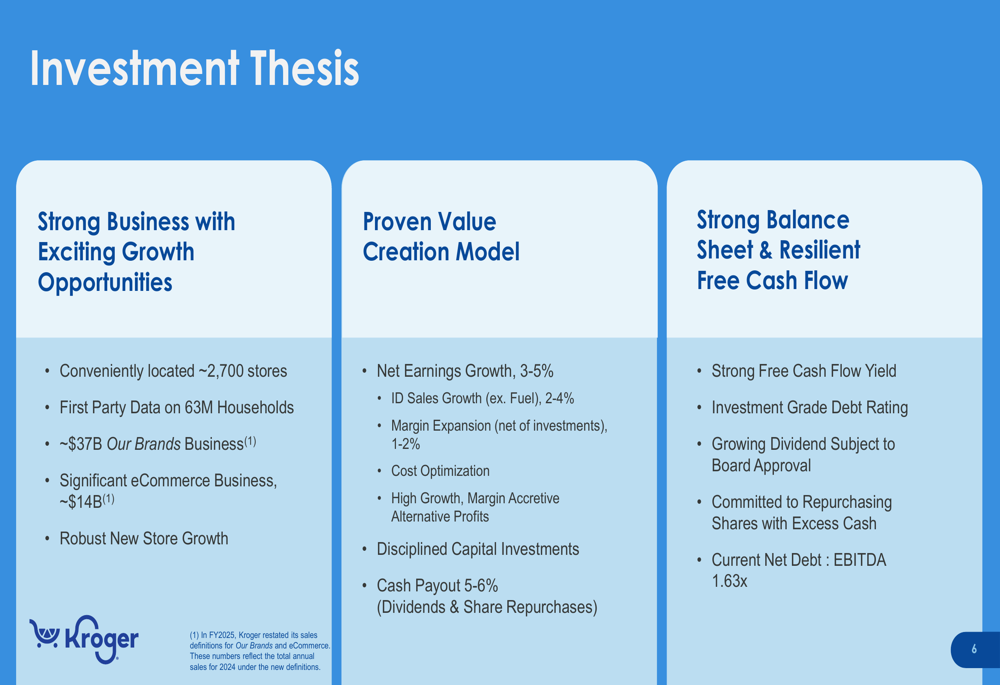

Financial Position & Investment Thesis

Kroger maintains a solid financial position with a net debt to EBITDA ratio of 1.63x, positioning the company well for continued investment in growth initiatives while returning capital to shareholders.

The company’s investment thesis is built on three foundational elements:

With approximately 2,700 stores and data from 63 million households, Kroger has significant scale advantages. Its private label "Our Brands" business generates approximately $37 billion in sales, while its eCommerce presence has grown to roughly $14 billion.

The company’s proven value creation model targets net earnings growth of 3-5% and identical sales growth of 2-4%, supported by margin expansion and cost optimization efforts. Kroger’s disciplined capital allocation strategy includes a cash payout of 5-6% through dividends and share repurchases.

Supplemental Financial Information

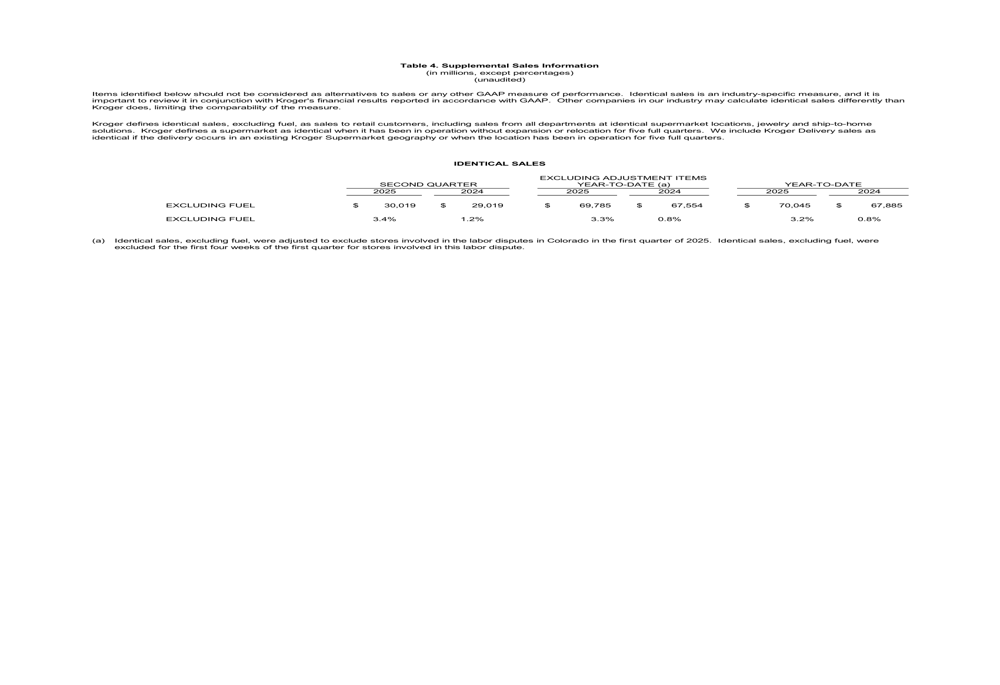

Kroger’s identical sales performance, a key metric for grocery retailers, shows consistent growth when excluding fuel. The detailed breakdown reveals the strength of the company’s core operations:

Year-to-date identical sales increased 3.2% compared to 0.8% in the prior year, reaching $69,785 million in 2025 versus $67,554 million in 2024. This acceleration in growth rate demonstrates Kroger’s ability to attract and retain customers despite intense competition in the grocery sector.

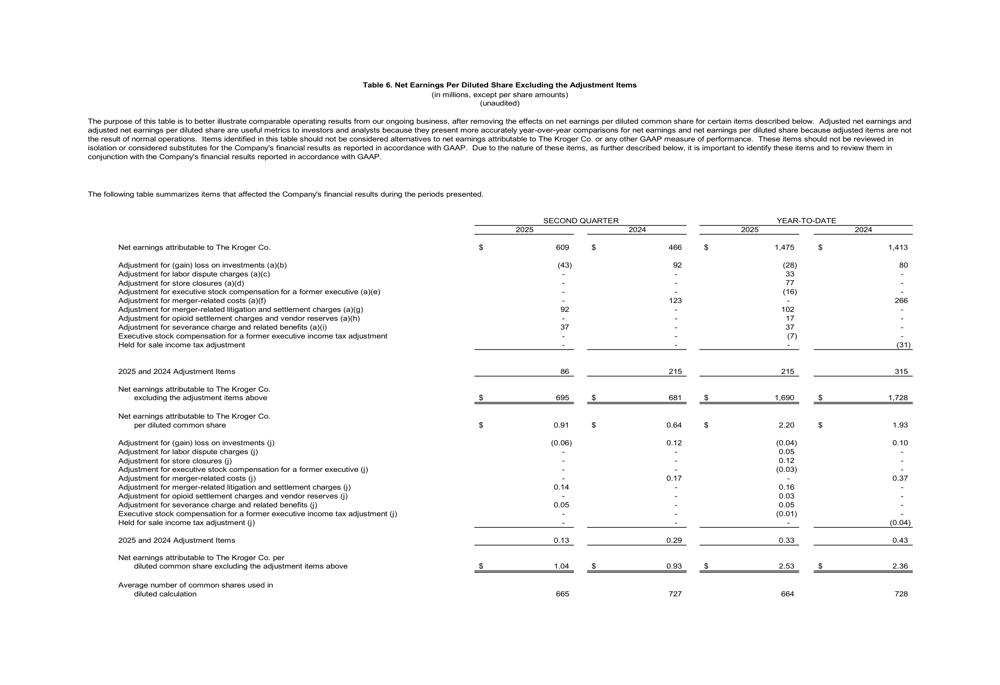

The company’s adjusted earnings metrics provide a clearer picture of operational performance by excluding one-time items. For Q2 2025, adjustments to net earnings include items related to merger costs, labor disputes, and investment gains/losses:

These adjustments help investors better understand Kroger’s underlying business performance and make more accurate year-over-year comparisons by removing factors not related to normal operations.

As Kroger continues to execute on its strategic initiatives and navigate the evolving retail landscape, the raised guidance and solid Q2 performance suggest management’s confidence in the company’s ability to deliver sustainable growth and shareholder value through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.