Gold prices just lower; monthly gains on track

Introduction & Market Context

Kymera Therapeutics (NASDAQ:KYMR) presented its Fourth Quarter and Full Year 2024 results on February 27, 2025, highlighting significant progress in its protein degradation platform focused on immunology. The company’s stock has shown resilience in recent months, trading at $44.53 as of July 2, 2025, well above its 52-week low of $19.45 but still below its high of $53.27.

The clinical-stage biopharmaceutical company is positioning itself as a leader in targeted protein degradation, developing oral small molecule degraders that aim to match or exceed the efficacy of biologics while offering the convenience of daily pill administration. This approach addresses a significant market opportunity in immune-inflammatory diseases, where many patients prefer oral therapies over injections.

Executive Summary

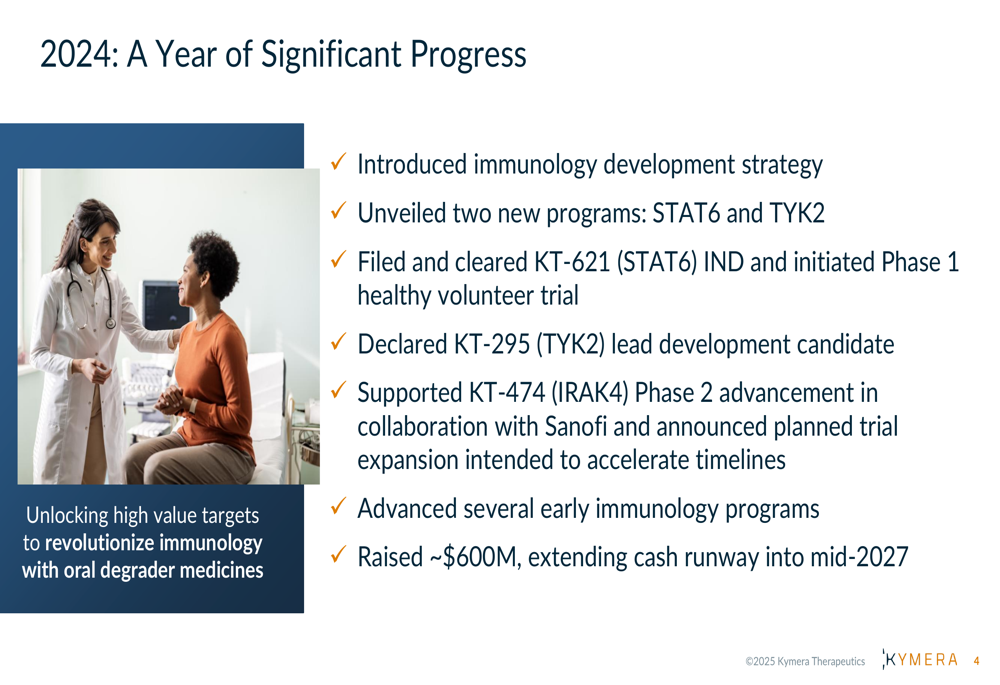

Kymera characterized 2024 as a year of "significant progress," marked by the introduction of its immunology development strategy, the unveiling of two new programs (STAT6 and TYK2), and advancement of its existing pipeline. The company successfully raised approximately $600 million during the year, extending its cash runway into mid-2027, which was later improved to early 2028 according to the Q1 2025 earnings report.

As shown in the following comprehensive overview of the company’s achievements:

The company’s strategy centers on developing oral protein degraders that could potentially replace injectable biologics in treating various immunological conditions. This approach has gained traction with investors, as evidenced by Kymera’s ability to secure substantial funding despite the challenging biotech financing environment.

Strategic Initiatives

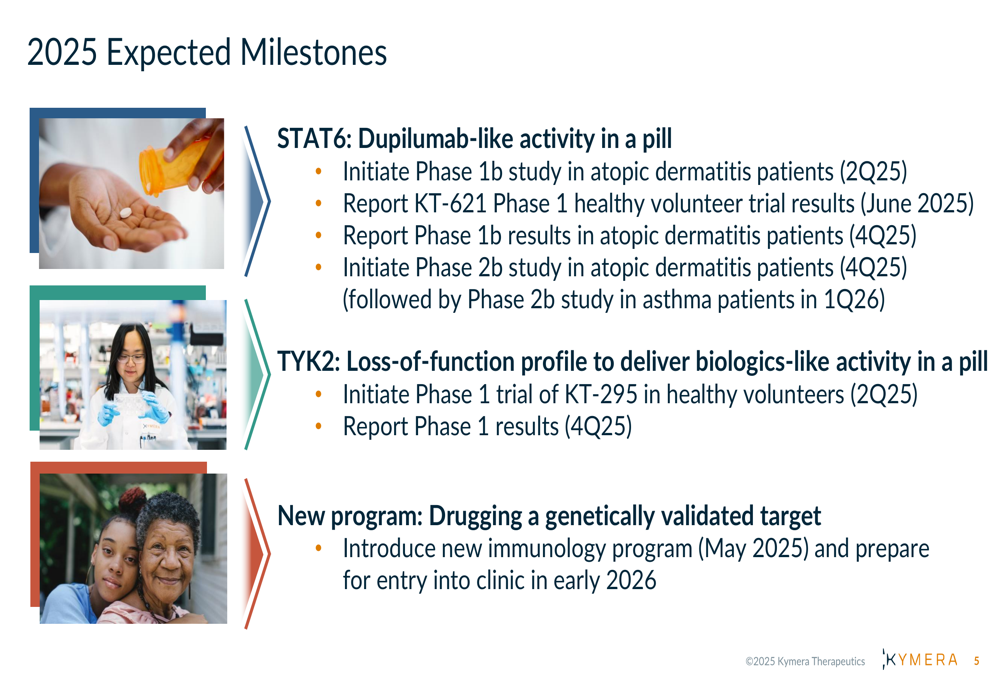

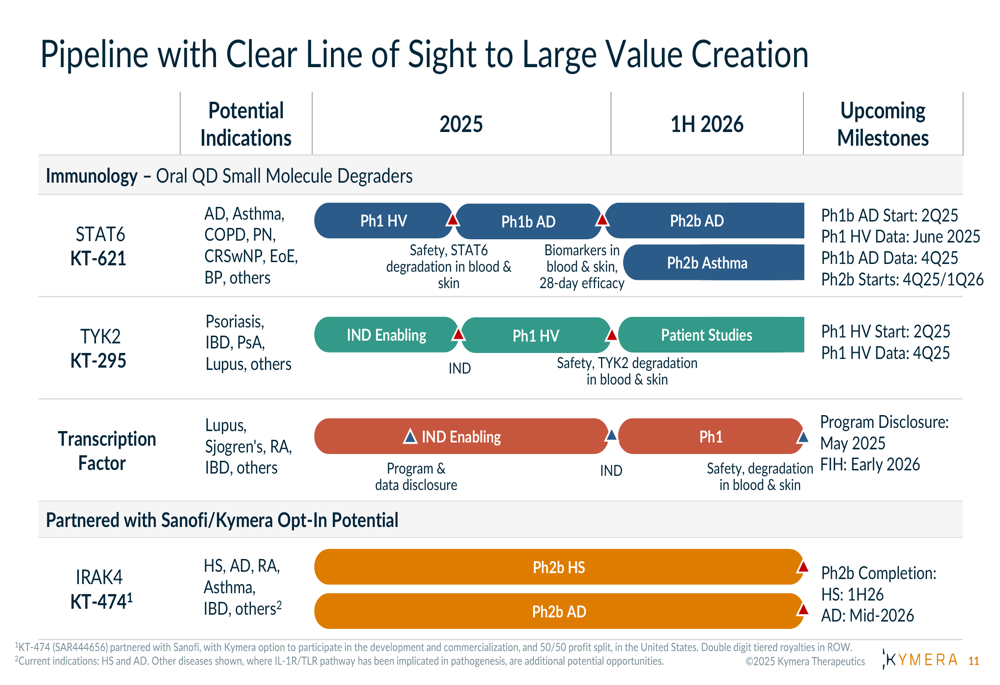

Kymera’s strategic focus on immunology is supported by a robust pipeline of novel protein degraders. The company has outlined an ambitious roadmap for 2025, with multiple clinical milestones expected across its key programs.

The following slide details the company’s expected milestones for 2025:

The STAT6 program (KT-621) represents Kymera’s most advanced wholly-owned asset, positioned as a potential "dupilumab-like activity in a pill." The company plans to initiate a Phase 1b study in atopic dermatitis patients in Q2 2025, with results from both the Phase 1 healthy volunteer trial and Phase 1b study expected later in the year.

For its TYK2 program (KT-295), Kymera aims to deliver "biologics-like activity in a pill" with a loss-of-function profile. The Phase 1 trial in healthy volunteers is scheduled to begin in Q2 2025, with results anticipated in Q4 2025. However, it’s worth noting that according to the recent earnings report, there has been a decision to pause the TYK2 degrader program, suggesting a strategic reallocation of resources.

Additionally, Kymera plans to introduce a new immunology program targeting a genetically validated target in May 2025, with preparations for clinical entry in early 2026.

Detailed Pipeline Analysis

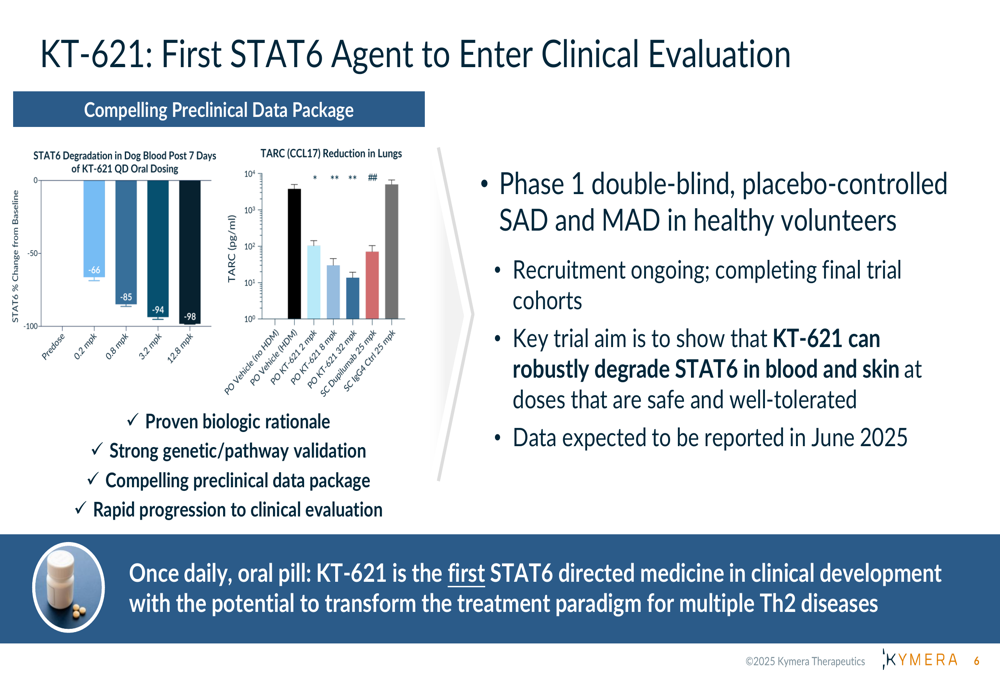

Kymera’s lead program, KT-621, is the first STAT6 agent to enter clinical evaluation. The company presented compelling preclinical data showing STAT6 degradation in dog blood and TARC reduction in lungs.

The following slide provides details on the KT-621 program:

The development path for KT-621 is clearly defined, with a Phase 1 study in healthy volunteers currently underway and expected to report data in June 2025. This will be followed by a Phase 1b study in atopic dermatitis patients and parallel Phase 2b trials in both atopic dermatitis and asthma.

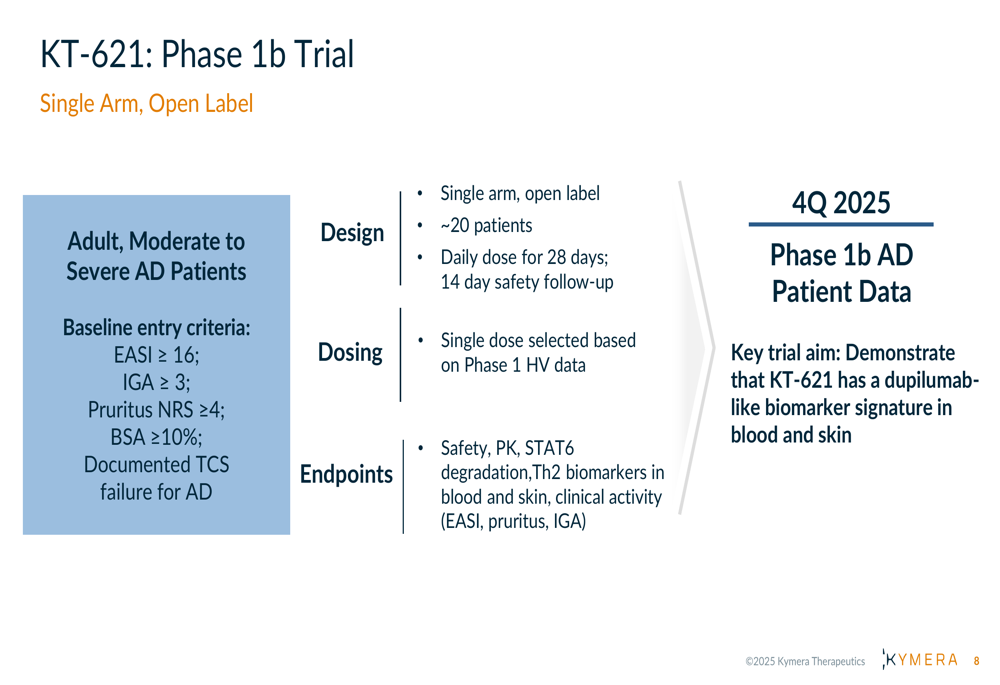

The Phase 1b trial design is detailed in the following slide:

Kymera’s partnered program with Sanofi (NASDAQ:SNY), KT-474 (IRAK4), is showing early signs of strong clinical activity. Phase 2b trials in both hidradenitis suppurativa (HS) and atopic dermatitis (AD) are ongoing, with Sanofi announcing plans to expand these trials to accelerate progression toward pivotal studies.

The company’s comprehensive pipeline is illustrated in the following slide:

Financial Analysis

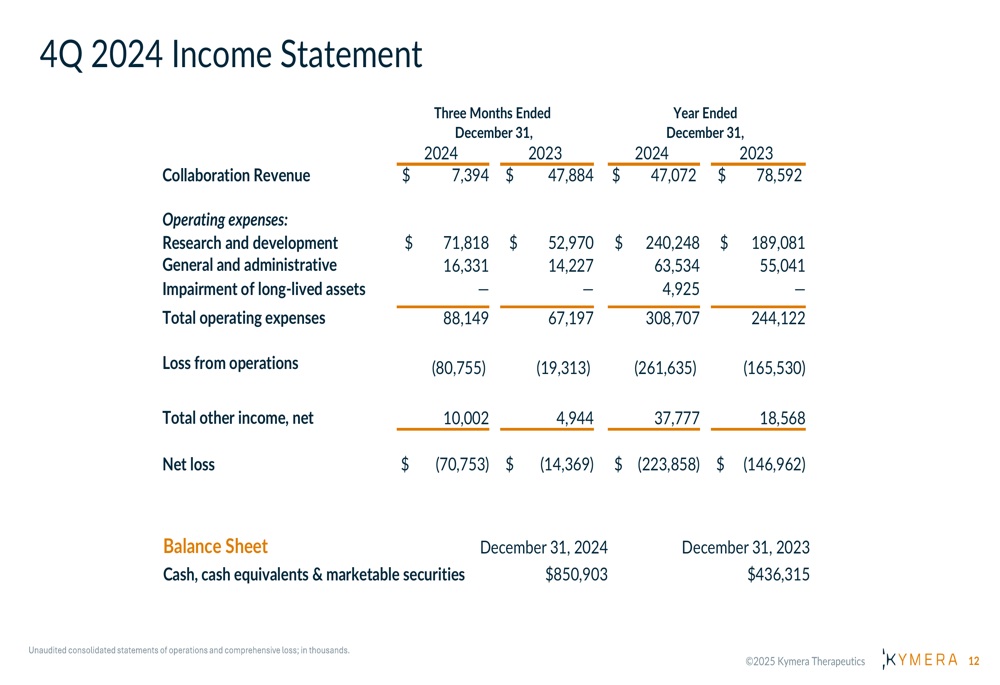

Kymera reported collaboration revenue for both the three months and year ended December 31, 2024. While specific financial details from the presentation are limited, the Q1 2025 earnings report indicates that the company outperformed expectations with an EPS of -0.82 (versus forecast of -0.89) and revenue of $22.1 million (versus forecast of $11.38 million).

The company’s strong cash position, bolstered by the approximately $600 million raised in 2024, provides runway into early 2028, allowing Kymera to advance its pipeline without immediate financing concerns. This financial stability is particularly valuable in the current biotech funding environment.

The income statement from the presentation shows:

Forward-Looking Statements

Kymera has set ambitious goals for 2025, with multiple clinical readouts expected across its pipeline. The company’s focus on oral protein degraders for immunological conditions positions it in a potentially lucrative market, competing with established biologics like dupilumab.

CEO Nello Mainolfi expressed confidence in the company’s approach, stating: "We believe with this modality, we can give rise to a series of new programs and medicines that can overcome the challenges that industry has faced for the past twenty years."

The company’s Chief Medical (TASE:BLWV) Officer, Jared Gollob, emphasized the potential of their lead program, noting: "Targeting STAT6 for degradation with KT621 is the only oral small molecule approach with the potential to achieve a dupilumab-like profile with once daily dosing."

While Kymera faces the typical risks associated with clinical-stage biotechnology companies, including clinical trial outcomes and regulatory hurdles, its differentiated approach to protein degradation and strong financial position provide a solid foundation for executing its strategic vision. The decision to pause the TYK2 program, however, indicates that the company is making strategic choices about resource allocation, which investors should monitor closely.

As Kymera advances its pipeline, particularly the STAT6 program, upcoming clinical data readouts in 2025 will be critical in validating the company’s approach and determining its long-term success in the competitive immunology therapeutic landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.