Gold prices steady above $3,400/oz on rate cut bets; PCE data awaited

Introduction & Market Context

Lam Research Corporation (NASDAQ:LRCX) presented its March quarter 2025 financial results on April 23, 2025, showcasing strong performance that exceeded guidance across key metrics. The semiconductor equipment manufacturer reported significant growth in revenue and earnings per share, supported by record foundry revenues and gross margins.

Following the announcement, Lam Research’s stock rose 5.12% in after-hours trading to reach $70 per share, reflecting positive investor sentiment about the company’s performance and outlook. This price movement brings the stock closer to recovering from its 52-week range of $56.32 to $113.

Quarterly Performance Highlights

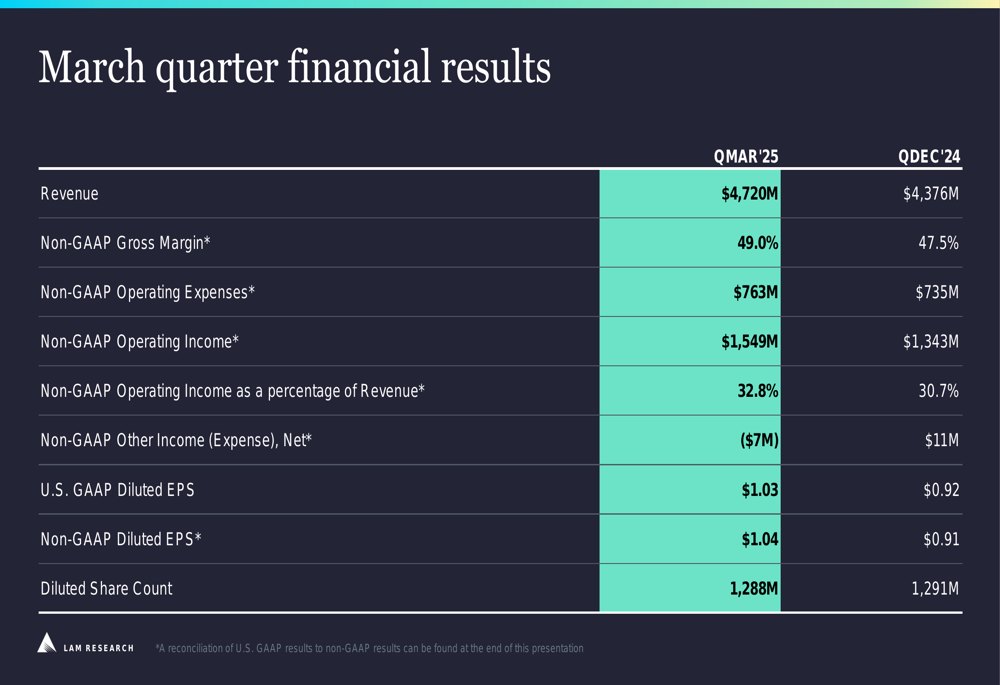

Lam Research reported March quarter revenue of $4.72 billion, up 7.9% from the December quarter’s $4.38 billion. Non-GAAP earnings per share reached $1.04, a 14.3% increase from $0.91 in the previous quarter. Both figures exceeded the company’s guidance midpoints.

As shown in the following quarterly highlights slide:

The company achieved record foundry revenues, demonstrating solid product momentum in leading-edge technology inflections. Additionally, Lam Research posted a record gross margin of 49.0%, up from 47.5% in the December quarter, which the company attributed to positive contributions from operational investments.

Detailed Financial Analysis

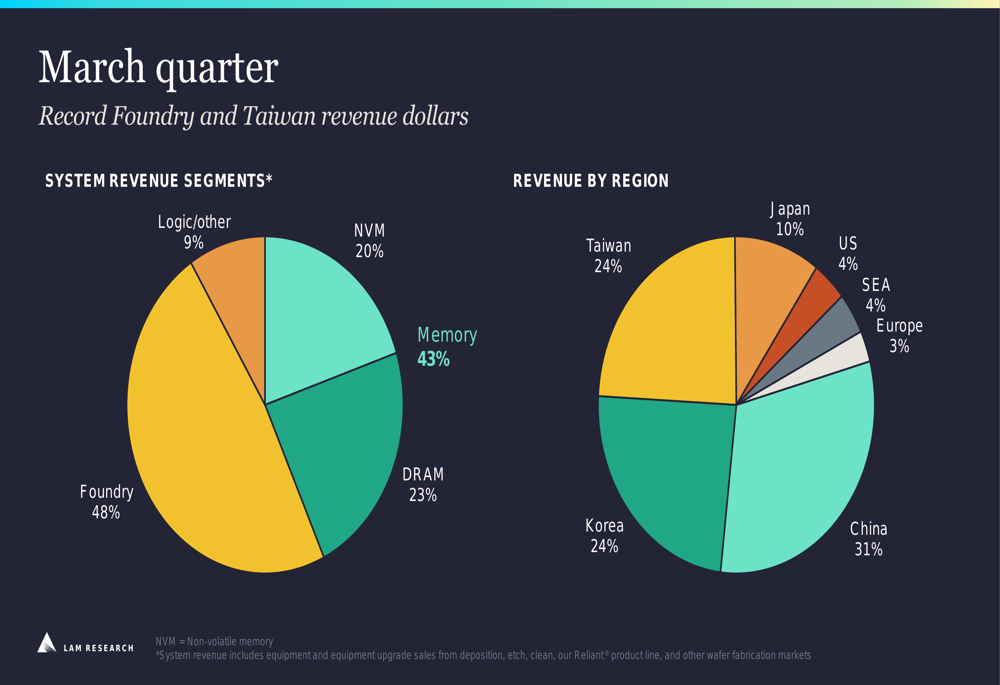

Lam’s system revenue segments for the March quarter showed a strong foundry presence, accounting for 48% of revenue. Memory contributed 43% (split between 23% DRAM and 20% NVM), while logic and other segments represented 9%. Geographically, China remained the largest market at 31% of revenue, followed by Taiwan and Korea at 24% each.

The following chart breaks down Lam’s revenue by segment and region:

The company’s Customer Support Business Group (CSBG) generated $1.68 billion in revenue for the March quarter, down slightly from $1.75 billion in the December quarter but up significantly from $1.40 billion in the March 2024 quarter, showing strong year-over-year growth in this segment.

Lam Research’s financial performance showed improvements across multiple metrics. Non-GAAP operating income increased to $1.55 billion, representing 32.8% of revenue compared to 30.7% in the previous quarter. The company generated $1.02 billion in free cash flow and returned capital to shareholders through $347 million in share repurchases and $296 million in cash dividends.

The comprehensive financial results are detailed in the following slide:

Strategic Initiatives

Lam Research outlined three key drivers for its expected outperformance in the semiconductor equipment market: expanding its served available market (SAM) faster than wafer fabrication equipment (WFE) growth, gaining market share with new products targeting billion-dollar inflections, and growing CSBG revenue faster than its installed base.

The company’s strategy is illustrated in this slide:

Product momentum remains strong, particularly in deposition and etch technologies. Lam highlighted multiple key wins for its Striker SPARC ALD product at leading-edge foundry customers, increased adoption of ALTUS Halo Mo across leading 3D NAND customers, and multiple wins for its Akara product in DRAM applications.

As shown in the following product momentum slide:

The company also reported strength in its CSBG and Semiverse Solutions businesses, with record upgrade revenues driven by NAND technology conversions and DRAM and logic tool repurposing. Lam signed a new multi-year spares agreement with a large memory customer and displaced a competitor in power device fabrication. Additionally, new licensing agreements were signed with three large customers for its SEMulator3D product.

Forward-Looking Statements

For the June 2025 quarter, Lam Research provided an optimistic outlook with revenue guidance of $5.00 billion (±$300 million), representing approximately 6% sequential growth at the midpoint. The company expects non-GAAP gross margin to improve to 49.5% (±1%) and non-GAAP earnings per share to reach $1.20 (±$0.10).

The detailed guidance is presented in this slide:

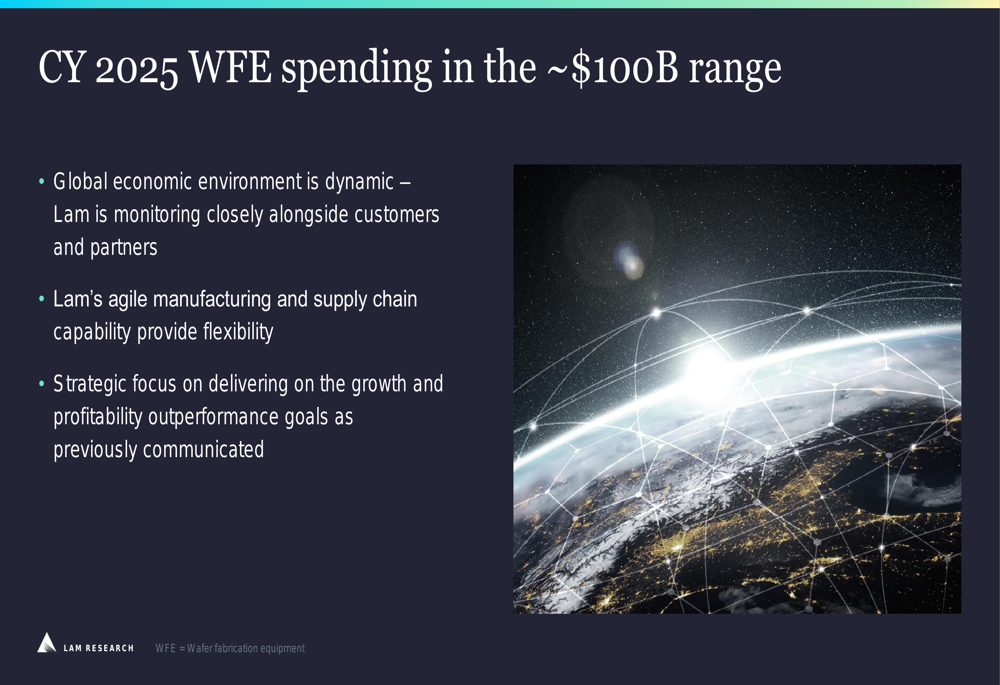

Looking at the broader market, Lam Research expects calendar year 2025 wafer fabrication equipment (WFE) spending to be in the approximately $100 billion range. The company acknowledged that the global economic environment remains dynamic and emphasized its agile manufacturing and supply chain capabilities that provide flexibility in responding to market changes.

CEO Tim Archer and CFO Doug Bettinger led the presentation, highlighting the company’s strategic focus on delivering growth and profitability outperformance as previously communicated to investors. The company’s execution of this strategy is supported by new product momentum, key customer wins, installed base value creation, and innovations in Equipment Intelligence solutions and virtual process development.

Lam Research’s strong March quarter results and positive June quarter outlook suggest the company is well-positioned to capitalize on semiconductor industry demand and technology inflections, continuing the momentum seen in the previous quarter’s performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.