Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

Leggett & Platt Incorporated (NYSE:LEG) released its first quarter 2025 financial results on April 28, 2025, showing improved profitability despite ongoing sales pressure. The diversified manufacturer’s stock reacted positively in after-hours trading, jumping 16.78% to $8.49, reflecting investor optimism about the company’s restructuring progress and margin improvements despite volume challenges.

The company continues to navigate a challenging economic environment with its comprehensive restructuring plan showing tangible benefits to the bottom line, even as sales declined across all segments. The presentation highlighted both the progress of ongoing initiatives and strategies to address potential tariff impacts across its diverse business portfolio.

Quarterly Performance Highlights

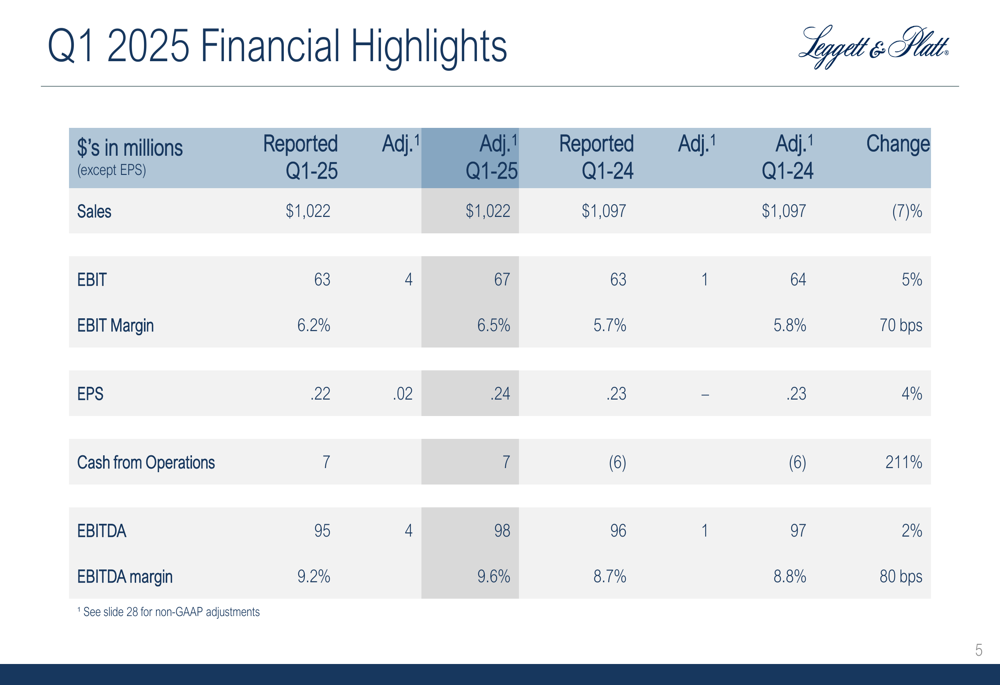

Leggett & Platt reported Q1 2025 sales of $1.022 billion, down 7% compared to Q1 2024, with volume decreases accounting for 5% of the decline. Despite lower sales, the company achieved adjusted EBIT of $67 million, up $3 million from the prior year, and improved its adjusted EBIT margin by 70 basis points to 6.5%.

As shown in the following financial highlights table, the company improved both EBIT and EBITDA margins on both a reported and adjusted basis:

The company’s adjusted EPS increased slightly to $0.24, up from $0.23 in Q1 2024, while cash flow from operations improved significantly to $7 million compared to negative $6 million in the prior-year period. This cash flow improvement came despite continued sales challenges, highlighting the company’s focus on operational efficiency.

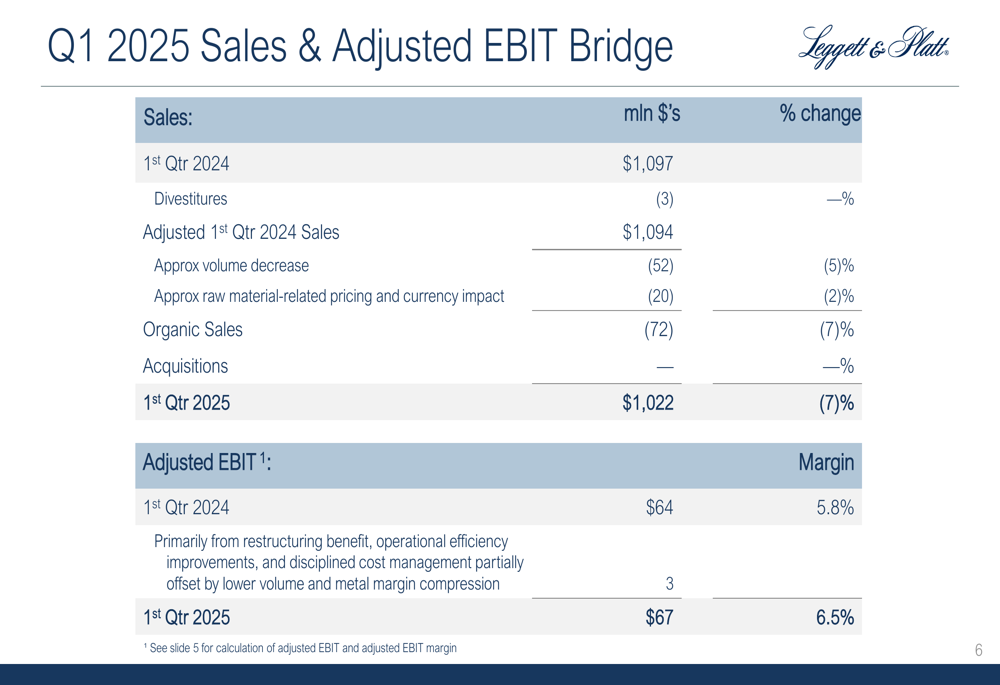

The sales and EBIT bridge analysis below illustrates how volume decreases were partially offset by operational improvements:

Restructuring Progress and Benefits

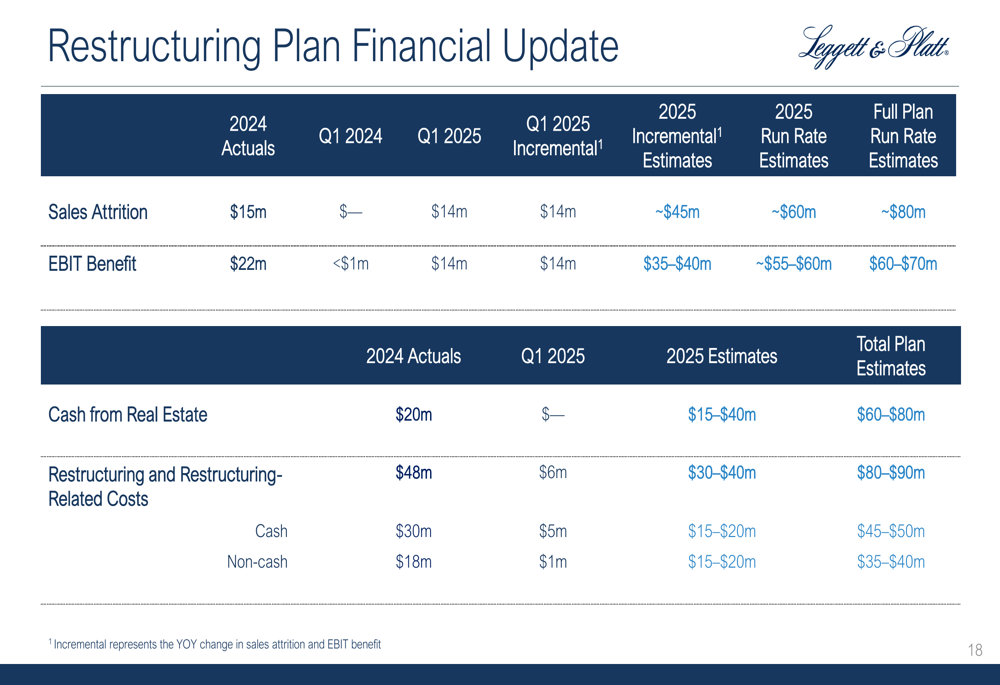

Leggett & Platt’s ongoing restructuring initiatives continue to deliver meaningful benefits to the bottom line. The company’s restructuring plan, which began in 2024, has already delivered $22 million in EBIT benefits last year and is expected to generate an additional $35-40 million in 2025.

The restructuring initiatives span across all segments, with significant progress in the Bedding Products segment, where the company reduced its footprint by 14 locations in 2024 and consolidated all domestic innerspring production into four remaining locations. In Q1 2025, the company divested a small U.S. machinery business as part of its ongoing portfolio optimization.

The following chart details the financial impact of the restructuring plan, including expected benefits and costs:

While the restructuring is expected to result in approximately $60-80 million in sales attrition at full run rate, the EBIT benefit is projected to reach $60-70 million. Additionally, the company expects to generate $60-80 million in cash from real estate sales throughout the plan period, with $20 million already realized in 2024 and an additional $15-40 million expected in 2025.

Segment Performance Analysis

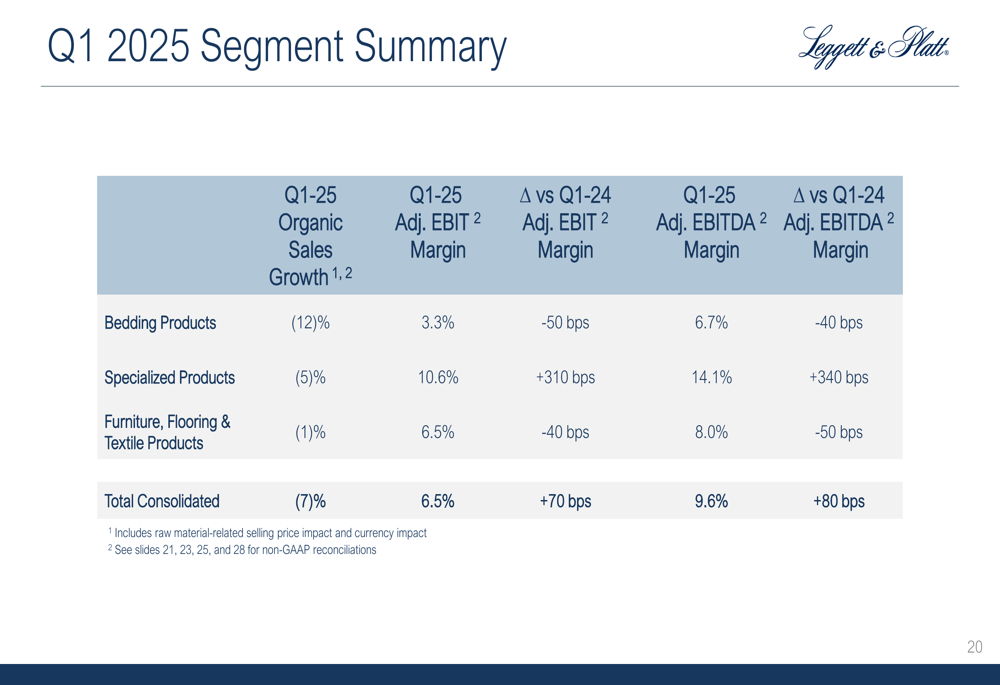

All three of Leggett & Platt’s business segments experienced organic sales declines in Q1 2025, though with varying degrees of impact on profitability:

The Bedding Products segment was most significantly impacted, with organic sales down 12% and adjusted EBIT margin declining 50 basis points to 3.3%. This decline was primarily driven by a 10% volume decrease, with raw material-related selling price decreases and currency impacts accounting for an additional 2% reduction.

In contrast, the Specialized Products segment showed notable margin improvement despite a 5% organic sales decline. Adjusted EBIT margin increased 310 basis points to 10.6%, driven by disciplined cost management, operational efficiency improvements, and restructuring benefits that more than offset lower volumes.

The Furniture, Flooring & Textile Products segment experienced the smallest sales decline at 1%, but saw adjusted EBIT margin decrease by 40 basis points to 6.5%, primarily due to raw material-related pricing adjustments.

Tariff Impact and Mitigation Strategies

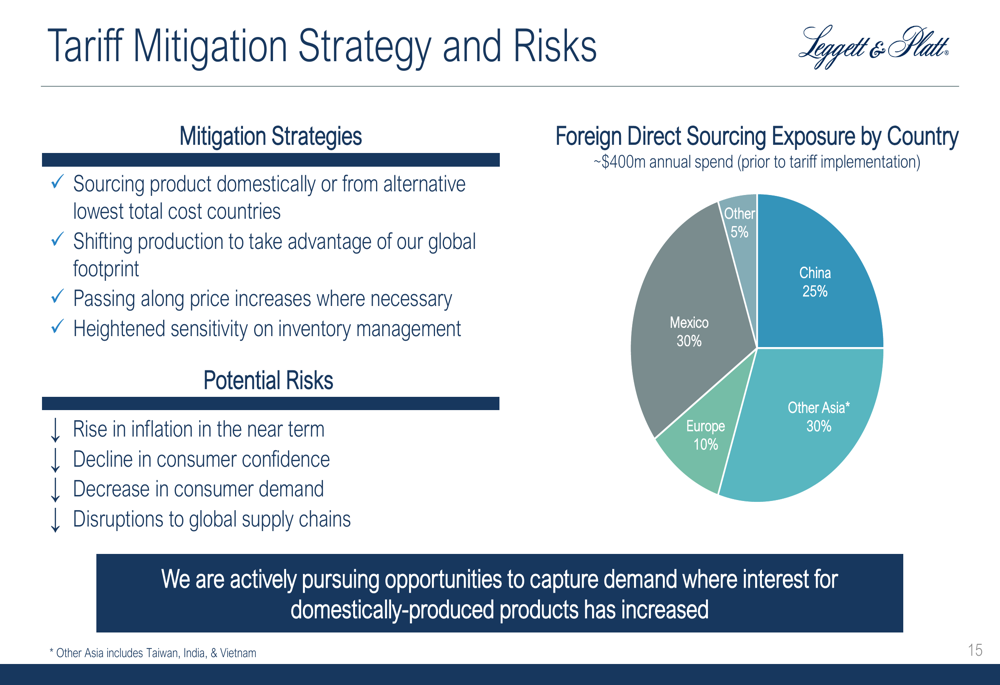

Leggett & Platt provided a comprehensive overview of potential tariff impacts across its business segments, along with strategies to mitigate these effects. The company’s exposure varies significantly by segment, with some areas potentially benefiting from tariffs while others face challenges.

The following slide outlines the company’s tariff mitigation strategies and potential risks:

The company has approximately $400 million in annual foreign direct sourcing exposure (prior to tariff implementation), with diversification across multiple regions including Mexico (30%), Other Asia (30%), China (25%), Europe (10%), and other regions (5%).

Mitigation strategies include sourcing products domestically or from alternative lowest-cost countries, shifting production to leverage the company’s global footprint, passing along price increases where necessary, and heightened sensitivity to inventory management.

Forward-Looking Statements

Leggett & Platt maintained its full-year 2025 guidance, projecting sales of $4.0-4.3 billion (down 2-9% versus 2024) and adjusted EPS of $1.00-1.20. The company expects demand to remain pressured due to economic uncertainty and restructuring-related sales attrition, with volume now projected to decline in the low to high single digits compared to previous guidance of low to mid-single digit declines.

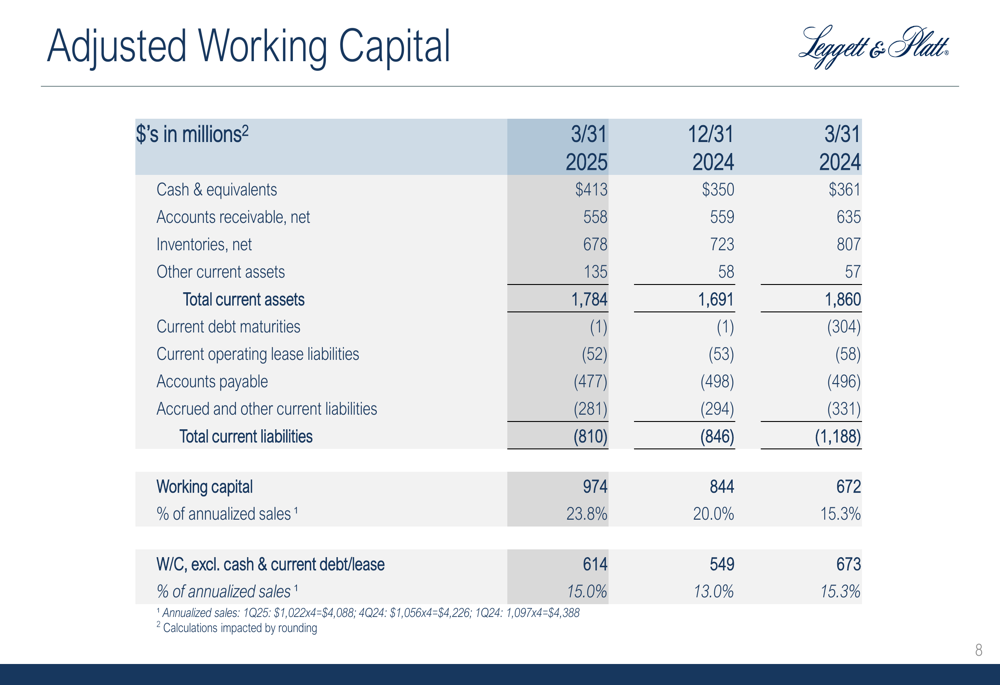

The company’s working capital position and leverage metrics show some pressure, with working capital as a percentage of annualized sales increasing to 23.8% as of March 31, 2025, compared to 20.0% at the end of 2024:

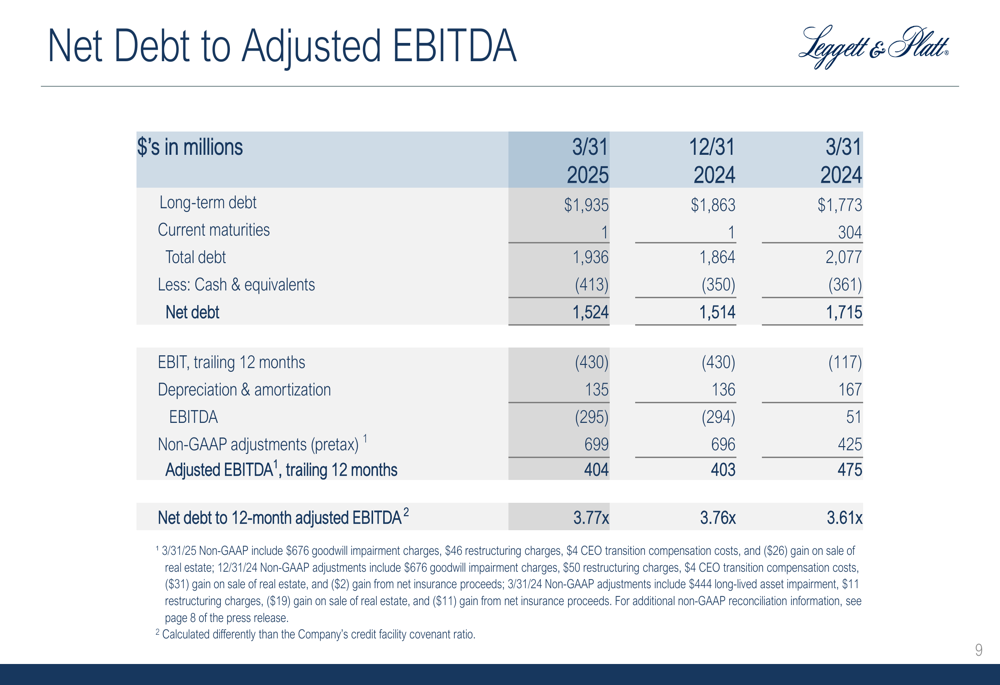

Net debt to adjusted EBITDA also increased slightly to 3.77x from 3.76x at year-end 2024, though it improved from 3.61x a year earlier:

Despite these challenges, Leggett & Platt expects operating cash flow of $275-325 million for the full year, supported by continued restructuring benefits, operational efficiency improvements, and metal margin expansion, which are expected to partially offset lower volume.

The company’s focus on disciplined cost management and restructuring initiatives appears to be yielding results, as evidenced by the margin improvements in Q1 despite ongoing sales pressure. As these initiatives continue to progress, Leggett & Platt aims to emerge as a more streamlined and profitable organization better positioned to navigate challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.