Fed Governor Adriana Kugler to resign

Introduction & Market Context

LendingClub Corporation (NYSE:LC) presented its first quarter 2025 results on April 29, 2025, highlighting strong performance that exceeded financial targets. Despite the positive results, the company’s stock fell 6.19% in after-hours trading to $10.30, suggesting investors may have concerns beyond the headline numbers.

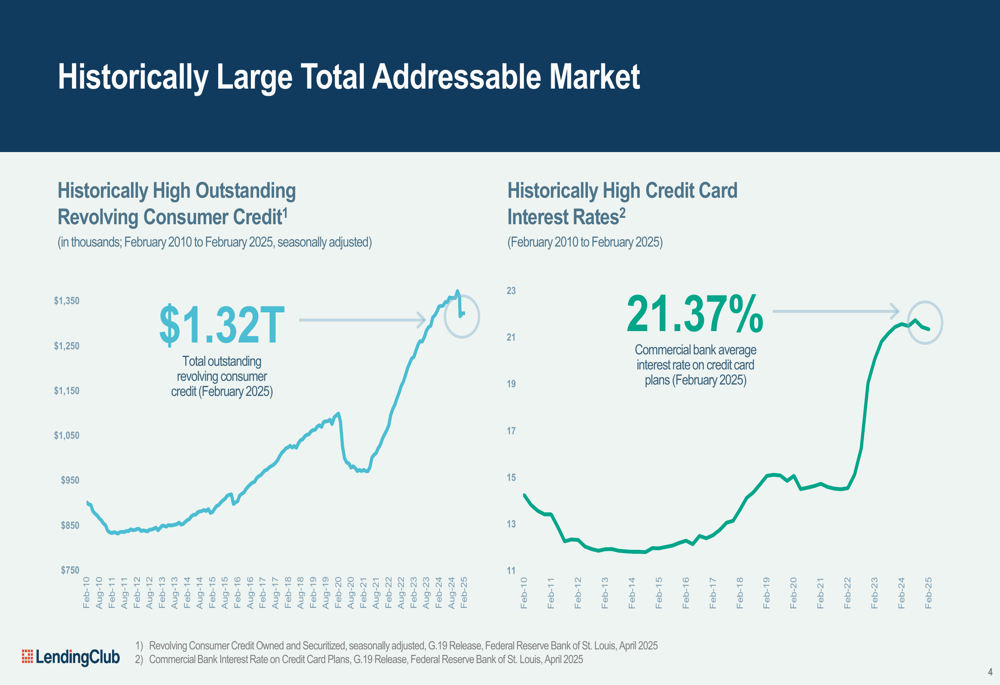

The presentation emphasized LendingClub’s position in a market characterized by historically high revolving consumer credit, which reached $1.32 trillion in February 2025, and credit card interest rates at 21.37%. This environment creates significant opportunity for LendingClub’s debt consolidation offerings.

As shown in the following chart of consumer credit and interest rates:

Quarterly Performance Highlights

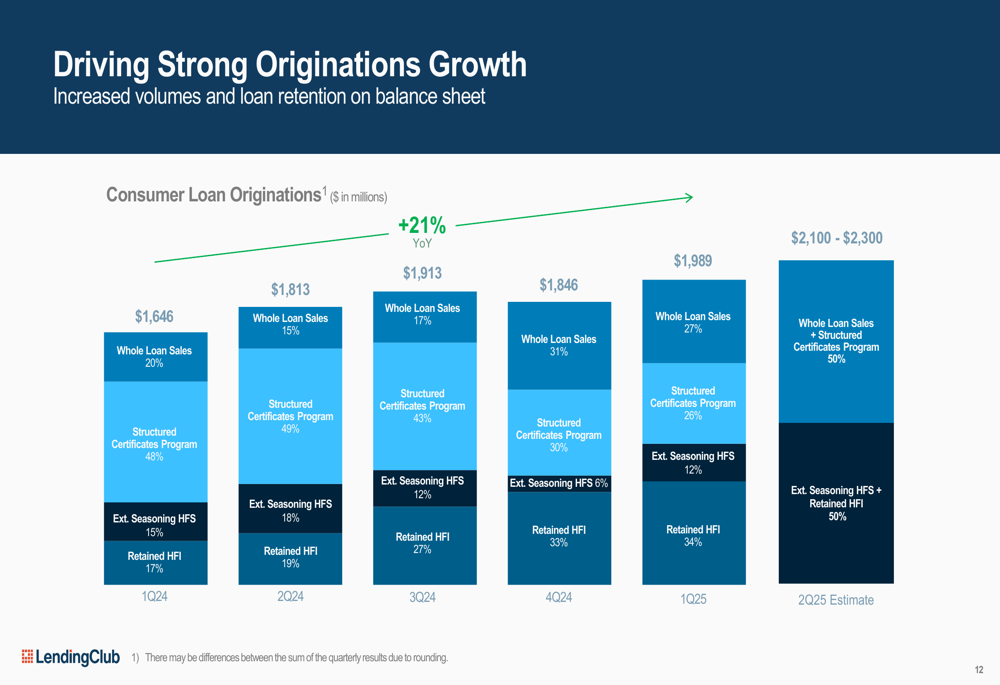

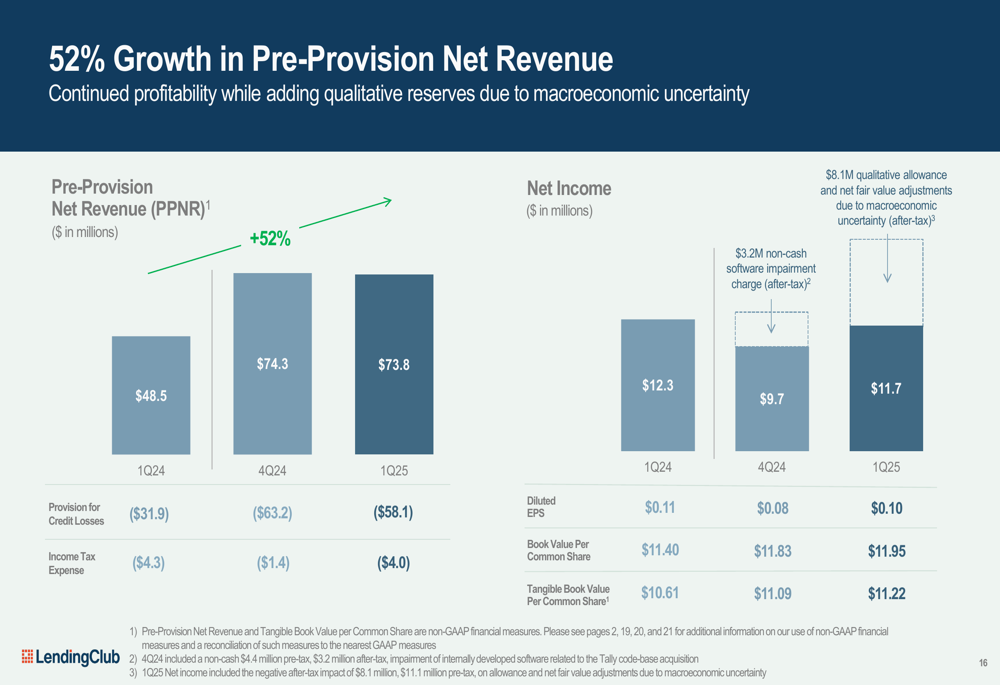

LendingClub reported total originations of $2.0 billion for Q1 2025, exceeding its guidance of $1.8-$1.9 billion and representing a 21% year-over-year increase. Pre-Provision Net Revenue (PPNR) reached $73.8 million, surpassing guidance of $60-$70 million and showing impressive 52% year-over-year growth.

The company’s financial performance exceeded targets across key metrics as illustrated in this summary:

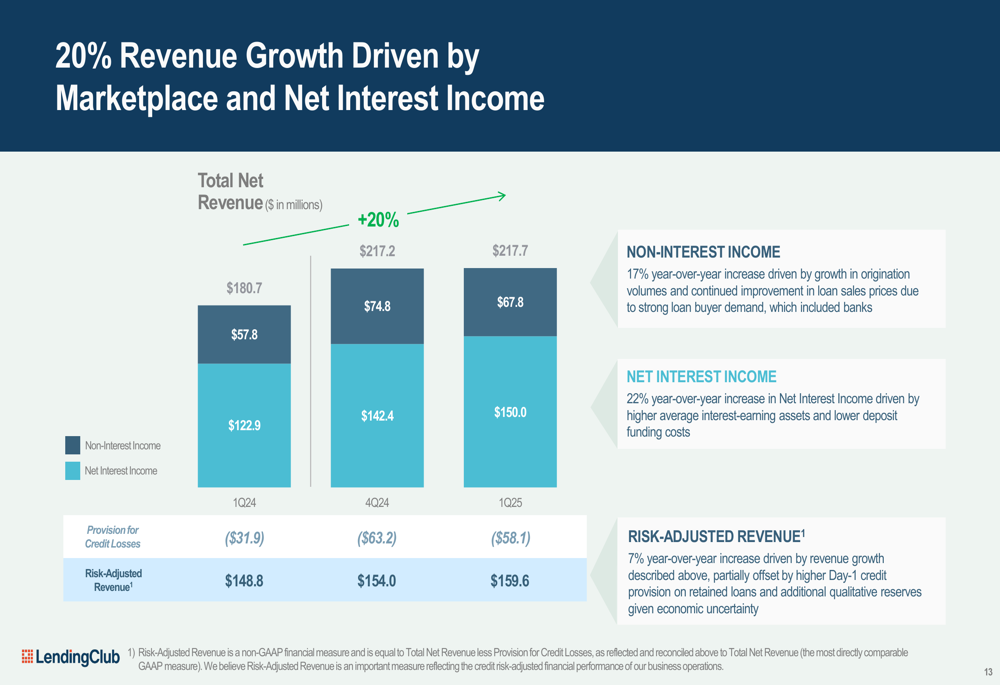

Total (EPA:TTEF) net revenue increased by 20% year-over-year, driven by both marketplace activity and net interest income. The breakdown of revenue components shows the diversified nature of LendingClub’s business model:

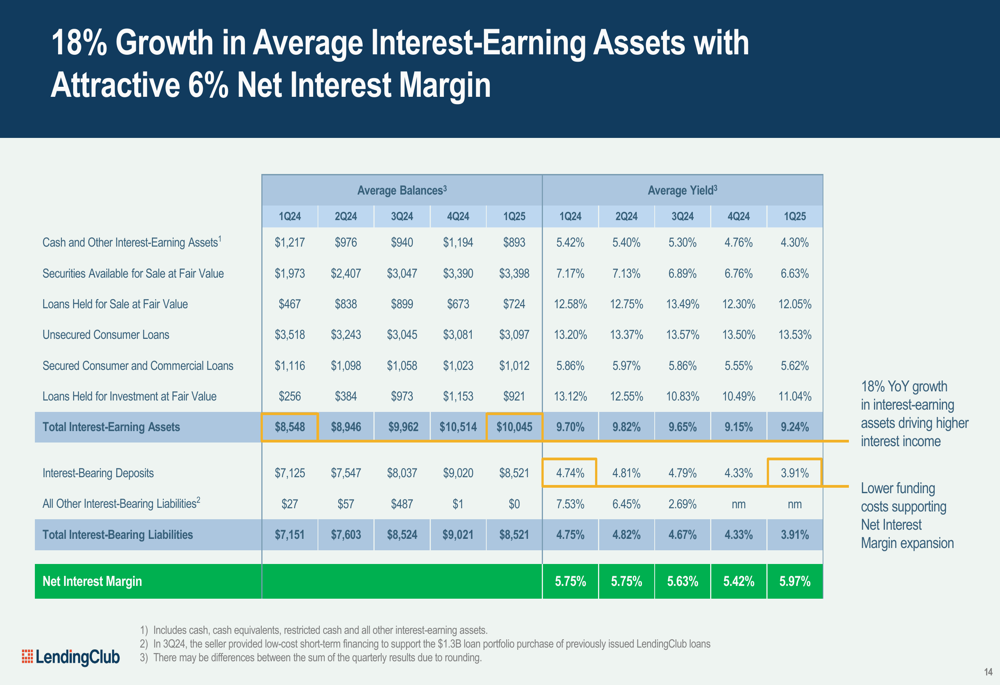

LendingClub also demonstrated strong growth in interest-earning assets, which increased 18% year-over-year while maintaining an attractive 6% net interest margin:

Strategic Positioning and Consumer Value Proposition

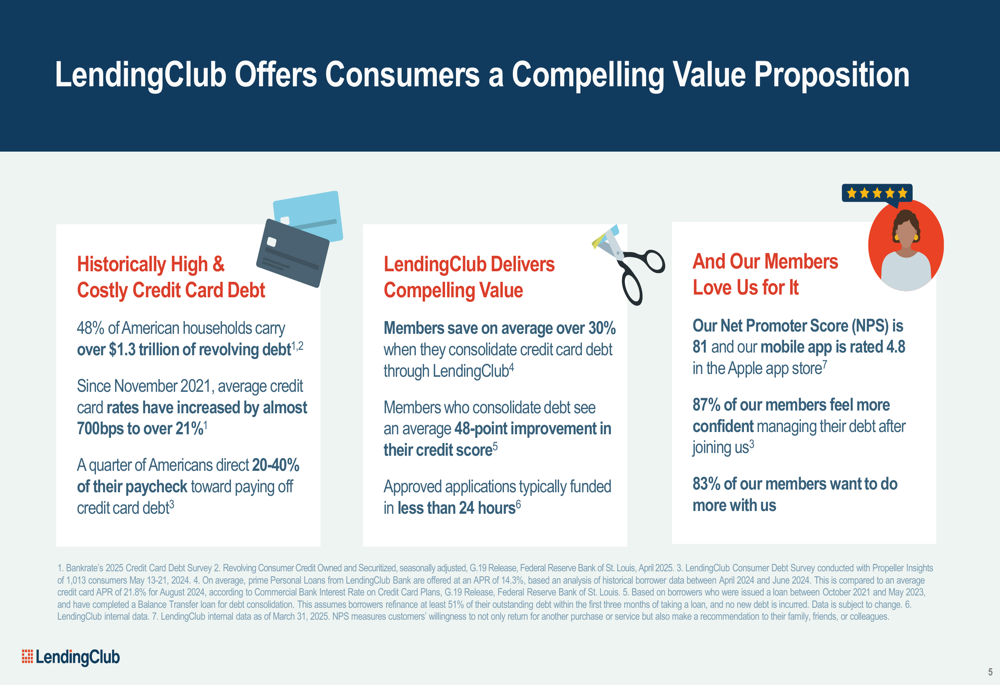

LendingClub positions itself as an "award-winning, member-focused digital marketplace bank" with over 5 million members and more than $100 billion in originations. The company’s value proposition centers on helping consumers manage high-interest credit card debt, offering an average savings of over 30% when consolidating debt and an average 48-point improvement in credit scores.

The following slide illustrates LendingClub’s consumer value proposition in the current high interest rate environment:

The company has been expanding its product offerings to build deeper relationships with members. Notable among these is LevelUp Savings, an award-winning high-yield savings account launched in August 2024 that has already attracted over 40,000 accounts totaling more than $1.9 billion in deposits. Another product, TopUp, allows members to refinance existing loans and add funds while maintaining a single monthly payment.

Credit Performance and Loan Disposition Strategy

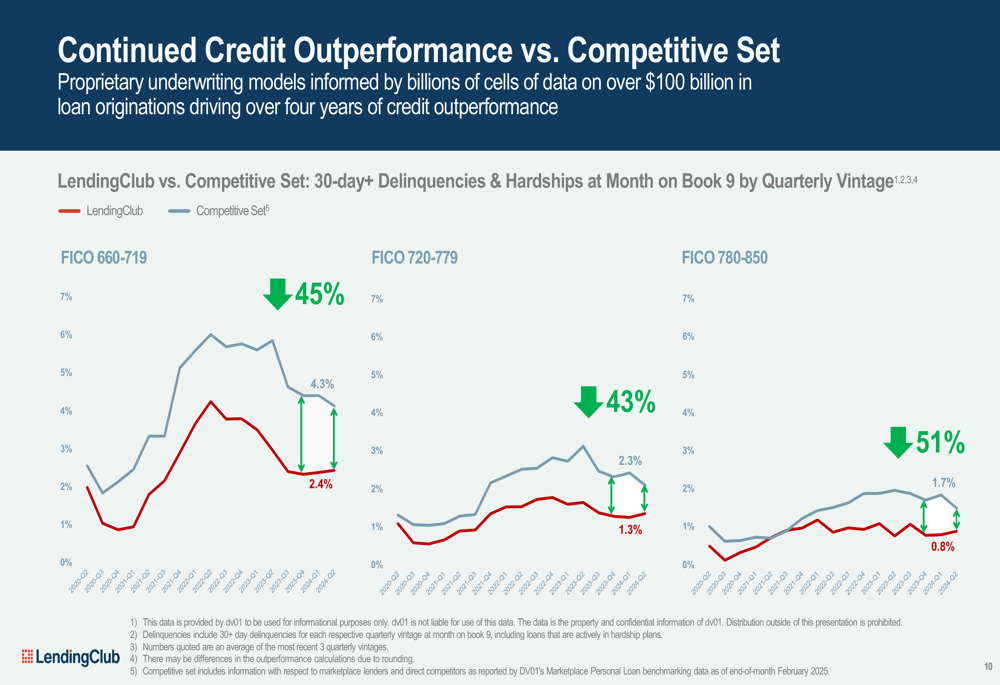

A key strength highlighted in the presentation is LendingClub’s credit outperformance compared to competitors. Across all FICO score ranges, LendingClub’s delinquency rates consistently trend below the competitive set, with the most recent three quarterly vintages in the FICO 660-719 range showing an average outperformance of 45%.

The company utilizes multiple loan disposition channels to optimize earnings and capital returns, including whole loan sales, structured certificates, extended seasoning, and held-for-investment approaches. This strategy has contributed to the strong originations growth shown below:

Pre-Provision Net Revenue showed significant growth of 52% year-over-year, reaching $73.8 million in Q1 2025:

Forward Guidance and Outlook

Looking ahead, LendingClub provided guidance for Q2 2025, projecting total originations of $2.1-$2.3 billion (16-27% year-over-year growth) and PPNR of $70-$80 million (27-46% year-over-year growth). For Q4 2025, the company maintains its target of over $2.3 billion in originations (25% year-over-year growth) and a return on tangible common equity exceeding 8% (150% year-over-year growth).

The company’s outlook assumes no deterioration in macroeconomic conditions and reflects continued positive momentum in originations. However, the after-hours stock decline of 6.19% following this report suggests investors may be concerned about factors not fully addressed in the presentation, potentially related to the previous quarter’s earnings miss or broader market sentiment about the lending sector.

This market reaction comes despite LendingClub’s apparent strong execution of its strategy to position itself between traditional banks and fintechs, combining the strengths of both while addressing their respective weaknesses in economics, scale, and resiliency.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.