Foremost Clean Energy plans 2,500-metre drill program at Jean Lake property

Introduction & Market Context

Light & Wonder Inc. (NASDAQ:LNW) presented its second quarter 2025 earnings on August 6, 2025, highlighting continued profitability growth despite a slight revenue decline. The gaming technology company’s stock rose 2.87% to $90.92 on the day of the presentation, reflecting positive investor sentiment following the results.

The company’s Q2 performance marks a significant improvement from its Q1 2025 results, when it missed both EPS and revenue expectations, causing the stock to dip. This quarter’s results demonstrate Light & Wonder’s ability to expand margins and grow profitability even with flat revenue.

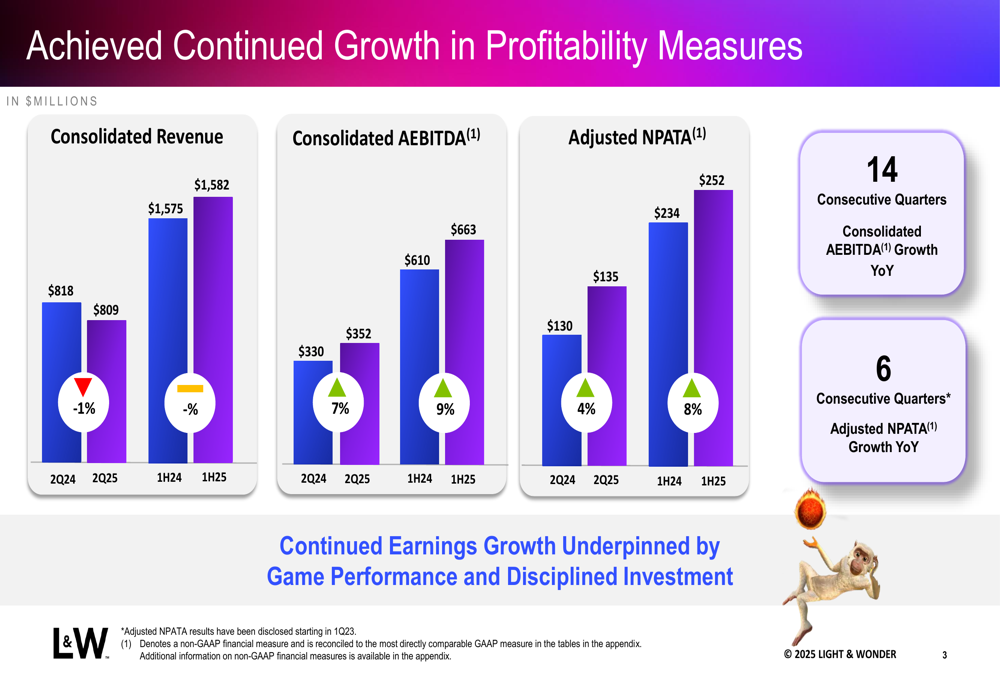

As shown in the following consolidated financial performance chart, the company achieved growth in key profitability metrics while revenue remained relatively stable:

Quarterly Performance Highlights

Light & Wonder reported consolidated revenue of $809 million for Q2 2025, down 1% year-over-year from $818 million in Q2 2024. Despite this slight decline, consolidated AEBITDA grew 7% to $352 million, with AEBITDA margin expanding 400 basis points to 44%. Adjusted NPATA increased 4% to $135 million, with Adjusted NPATA per share rising over 11% to $1.58.

The company has now achieved 14 consecutive quarters of year-over-year consolidated AEBITDA growth and 6 consecutive quarters of Adjusted NPATA growth, underscoring the sustainability of its profitability improvements.

Performance varied across business segments:

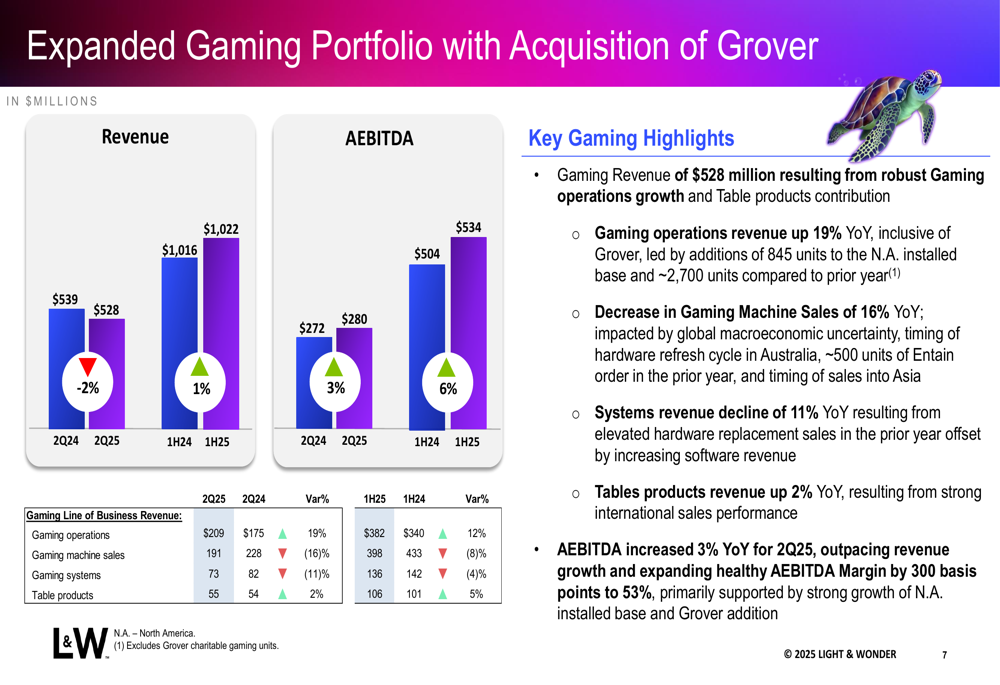

- Gaming: Revenue declined 2% to $528 million, while AEBITDA increased 3% to $280 million

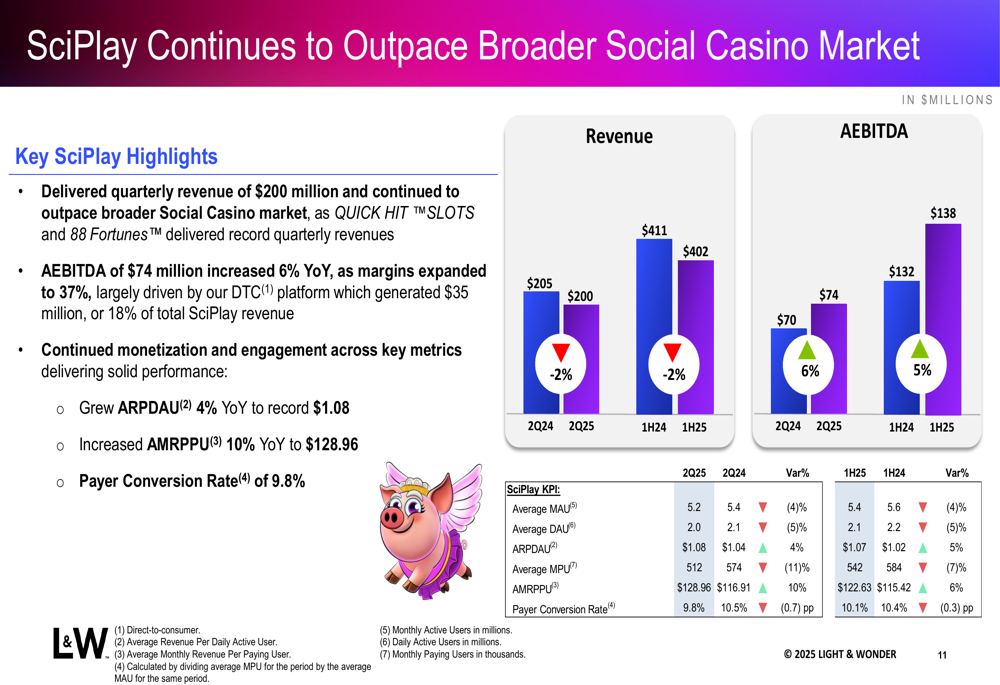

- SciPlay (NASDAQ:SCPL): Revenue reached $200 million, with AEBITDA up 6% to $74 million

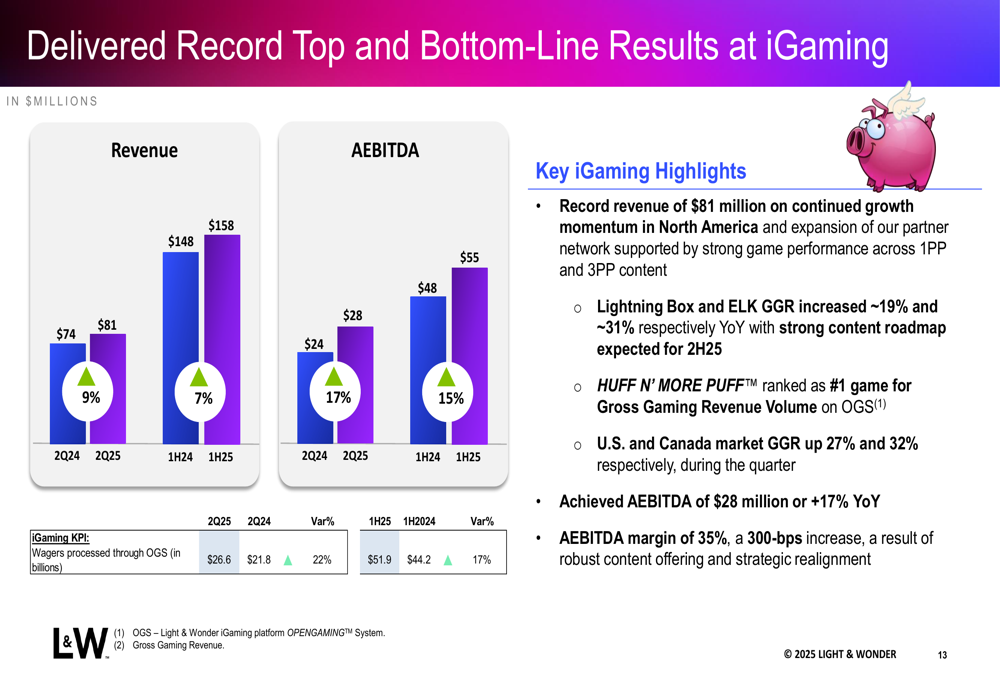

- iGaming: Achieved record revenue of $81 million (up 9%) and AEBITDA growth of 17% to $28 million

The following chart details the Gaming segment’s performance, showing the impact of the Grover acquisition and the shift in revenue mix:

SciPlay continued to outpace the broader social casino market, with strong monetization metrics including a 4% increase in Average Revenue Per Daily Active User (ARPDAU) to $1.08 and a 10% increase in Average Monthly Revenue Per Paying User (AMRPPU) to $128.96. The segment’s Direct-to-Consumer platform generated $35 million, representing 18% of total SciPlay revenue.

As illustrated in the following detailed SciPlay performance metrics:

The iGaming segment delivered record top and bottom-line results, with wagers processed through OGS increasing 22% to $26.6 billion. AEBITDA margin expanded 300 basis points to 35%.

The following chart highlights iGaming’s strong performance:

Strategic Initiatives

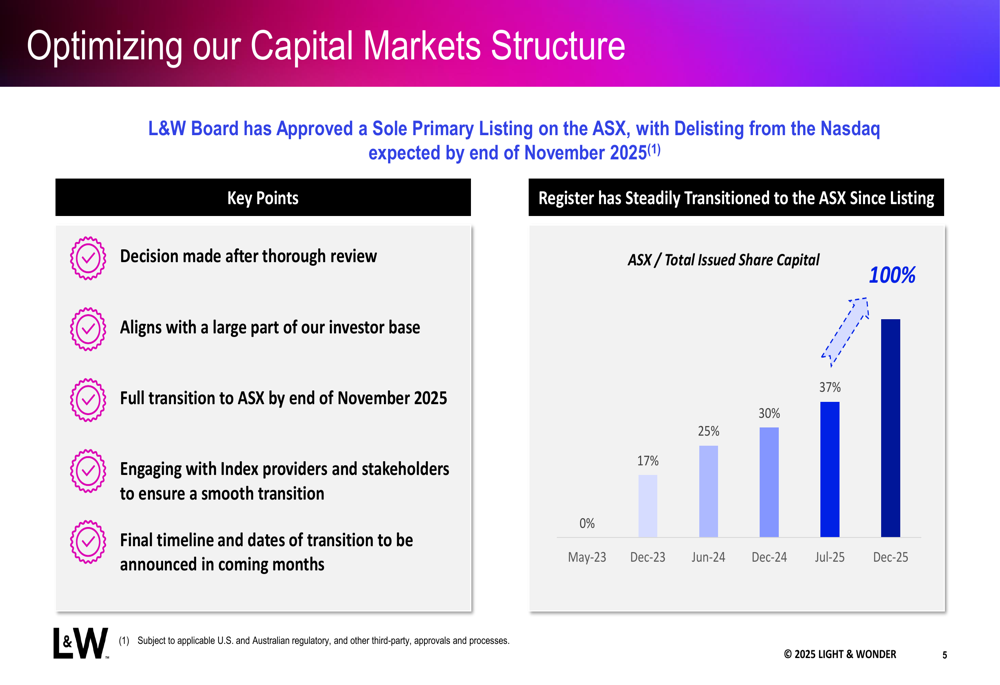

Light & Wonder announced a significant strategic shift, approving a sole primary listing on the Australian Securities Exchange (ASX) with plans to delist from Nasdaq by the end of November 2025. This decision follows a steady transition of the company’s investor register to the ASX, which has grown from 17% in May 2023 to 37% by December 2024.

The following chart illustrates this transition:

The company completed the acquisition of Grover Gaming in May 2025, expanding its charitable gaming footprint across North Dakota, Ohio, New Hampshire, Kentucky, Virginia, and Indiana. The integration is progressing with the addition of over 600 units since the February announcement.

Light & Wonder is also advancing its Direct-to-Consumer (DTC) platform within SciPlay, which now represents 18% of revenue, up 500 basis points from Q4 2024. This strategic initiative offers higher-value players a differentiated level of engagement and is driving margin uplift for the business.

Detailed Financial Analysis

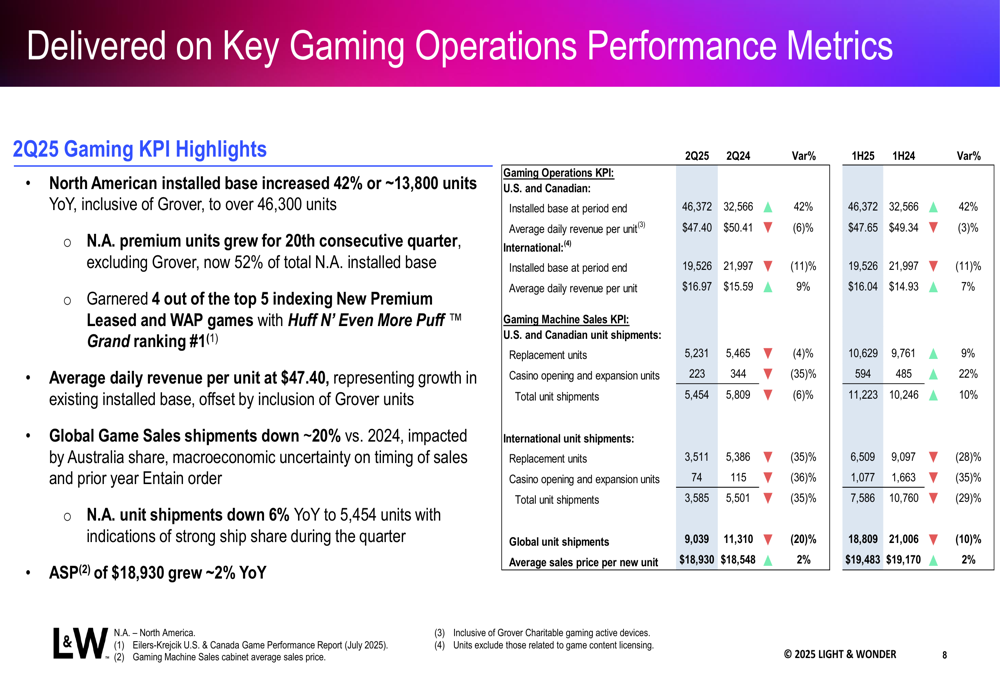

The Gaming segment’s revenue decline was primarily due to lower gaming machine sales and systems revenue, partially offset by 19% growth in gaming operations. North American installed base increased 42% year-over-year to over 46,300 units, with premium units growing for the 20th consecutive quarter to now represent 52% of the total North American installed base.

The following detailed gaming operations metrics highlight these trends:

Light & Wonder maintained a disciplined approach to capital allocation, ending Q2 with a net debt leverage ratio of 3.7x (or combined net debt leverage ratio of 3.4x), remaining within its targeted range of 2.5x to 3.5x. The company returned $100 million to shareholders through share repurchases in Q2, bringing the total capital returned in the first half of 2025 to $266 million.

The company has now completed 55% of its share repurchase program and announced an increase in the program from $1 billion to $1.5 billion, demonstrating confidence in its financial position and future prospects.

Forward-Looking Statements

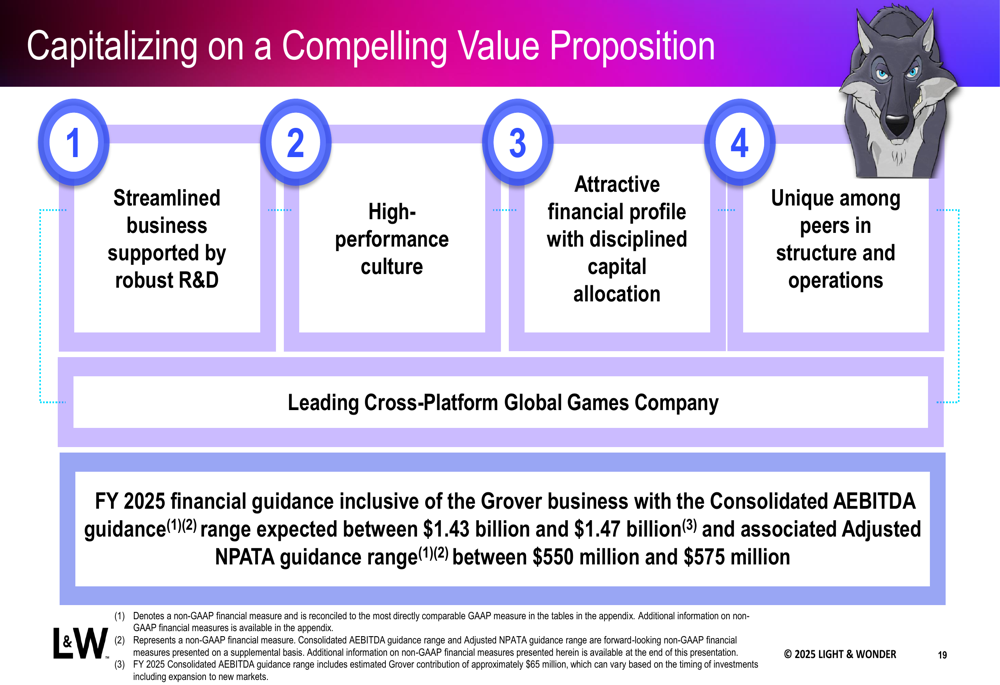

Light & Wonder provided FY 2025 financial guidance inclusive of the Grover business, with consolidated AEBITDA expected between $1.43 billion and $1.47 billion, and Adjusted NPATA projected between $550 million and $575 million.

The company’s value proposition, as summarized in the following slide, emphasizes its streamlined business supported by robust R&D, high-performance culture, attractive financial profile, and unique position among peers:

Management highlighted the continued earnings growth underpinned by game performance and disciplined investment. The company’s hardware and content roadmap features new titles across its COSMIC, KASCADA, LIGHTWAVE, and LANDMARK platforms, positioning it for future growth in the gaming market.

Light & Wonder’s Q2 2025 results demonstrate its ability to drive profitability growth through operational efficiency and strategic initiatives, even in a challenging revenue environment. The planned transition to a sole ASX listing represents a significant strategic shift that aligns with the company’s evolving investor base and could potentially unlock additional value for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.