Two 59%+ winners, four above 25% in Aug – How this AI model keeps picking winners

Introduction & Market Context

LKQ Corporation (NASDAQ:LKQ) released its first quarter 2025 earnings presentation on April 24, showing a 6.5% year-over-year revenue decline but improved margins and diluted EPS growth. The auto parts distributor reported total revenue of $3.46 billion, down from $3.70 billion in Q1 2024, while maintaining its full-year guidance despite early challenges.

The company’s shares were down 5.01% in premarket trading following the release, reflecting investor concerns about the revenue decline and negative cash flow for the quarter.

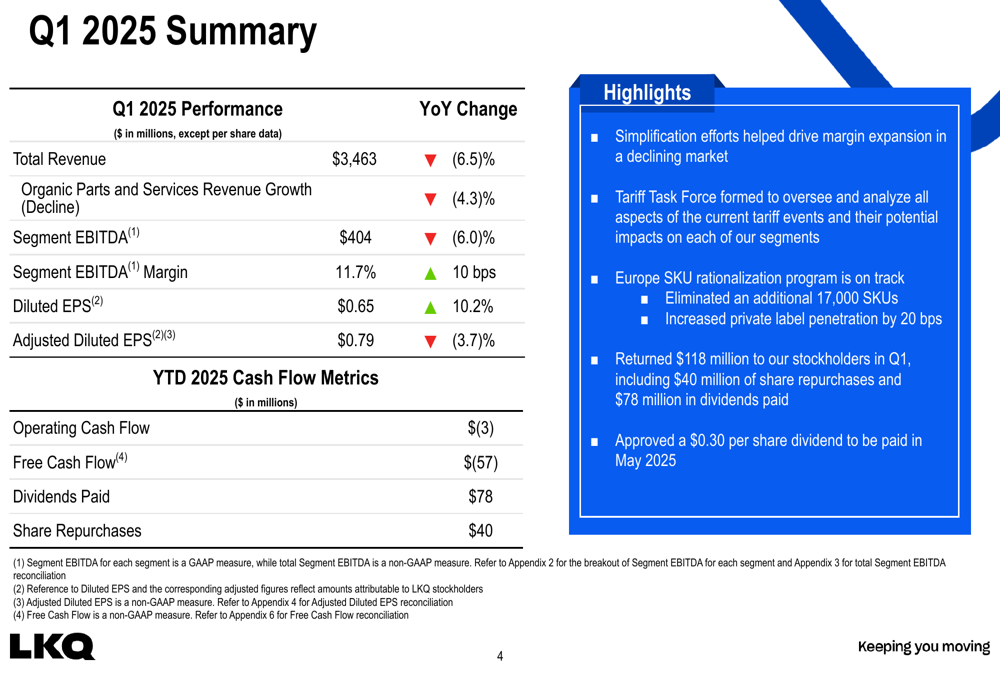

As shown in the following summary of Q1 performance:

Quarterly Performance Highlights

LKQ reported organic parts and services revenue declined 4.3% year-over-year, while segment EBITDA fell 6.0% to $404 million. Despite these challenges, the company managed to improve its segment EBITDA margin by 10 basis points to 11.7% and increase diluted EPS by 10.2% to $0.65.

"Our simplification efforts helped drive margin expansion despite revenue headwinds," said Justin Jude, President and CEO of LKQ Corporation. "We’ve also formed a Tariff Task Force to address potential impacts and continued our European SKU rationalization program, eliminating an additional 17,000 SKUs."

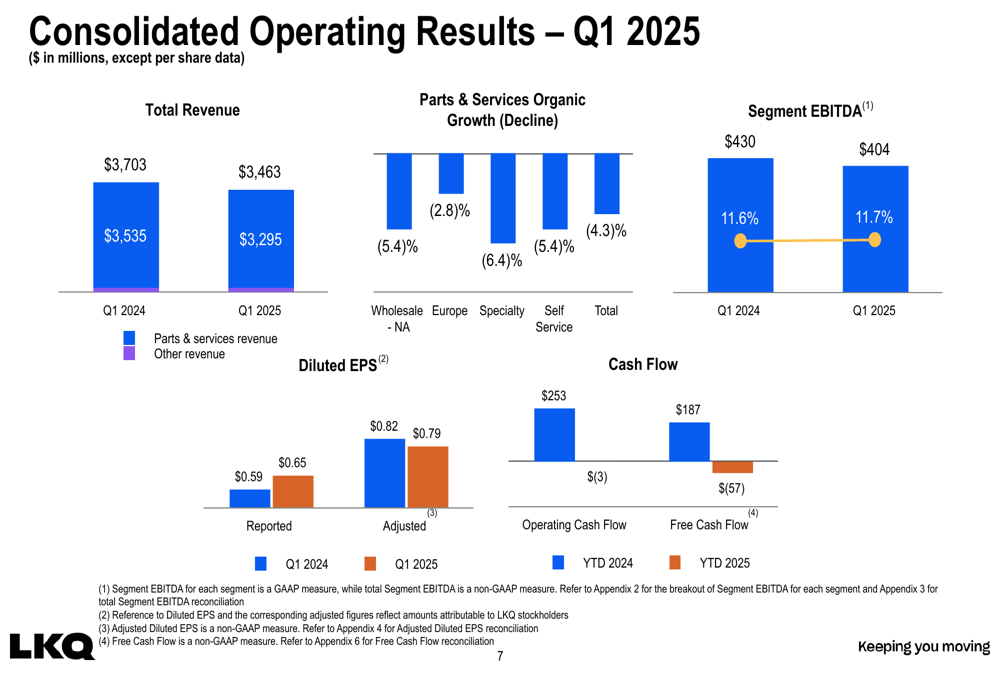

The consolidated results show pressure across most business segments:

Cash flow metrics were particularly challenging, with operating cash flow at negative $3 million and free cash flow at negative $57 million for the quarter. Despite this, LKQ returned $118 million to stockholders through $40 million in share repurchases and $78 million in dividends, and approved a $0.30 per share dividend to be paid in May 2025.

Tariff Mitigation Strategy

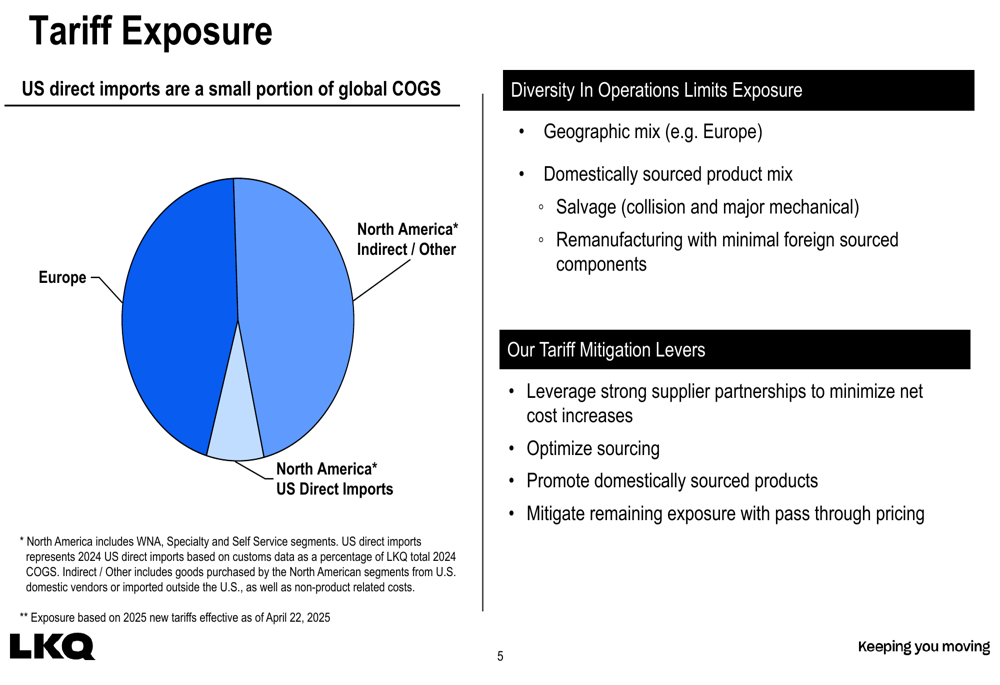

A significant focus of the presentation was LKQ’s approach to potential tariff impacts. The company emphasized that its diverse operational footprint limits exposure, with U.S. direct imports representing only a small portion of global cost of goods sold.

The company outlined several mitigation strategies, including leveraging strong supplier partnerships, optimizing sourcing, promoting domestically sourced products, and implementing pass-through pricing where necessary.

As illustrated in the following breakdown of the company’s tariff exposure:

Segment Analysis

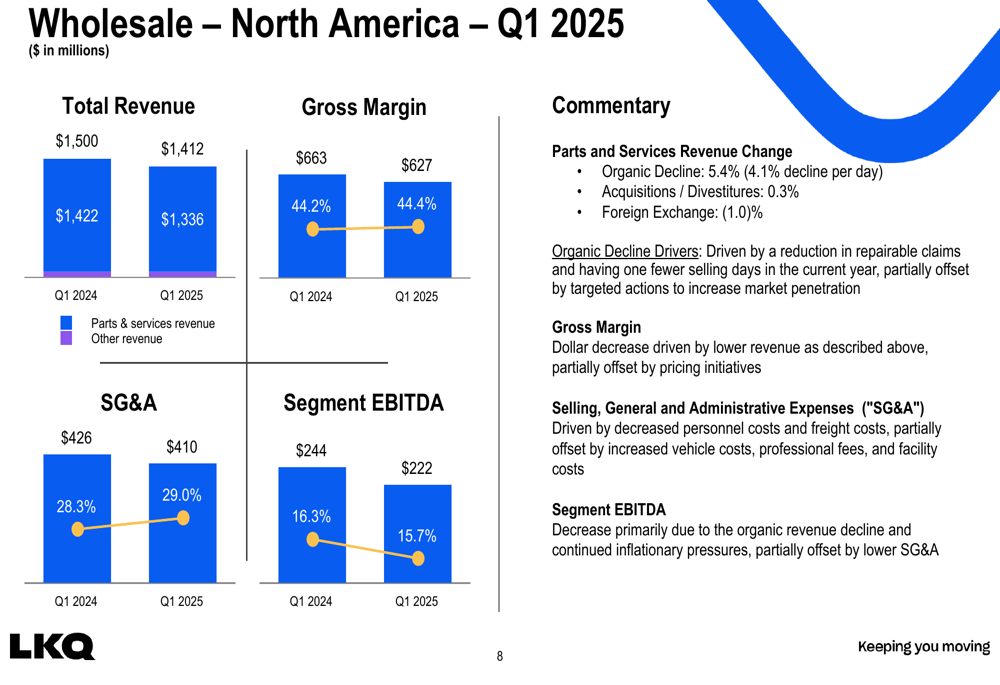

The Wholesale North America segment, LKQ’s largest, saw revenue decline 5.9% to $1.41 billion, with segment EBITDA falling from 16.3% to 15.7%. The company attributed this to "a reduction in repairable claims and having one fewer selling day in the current year," though noted it was "partially offset by targeted actions to increase market penetration."

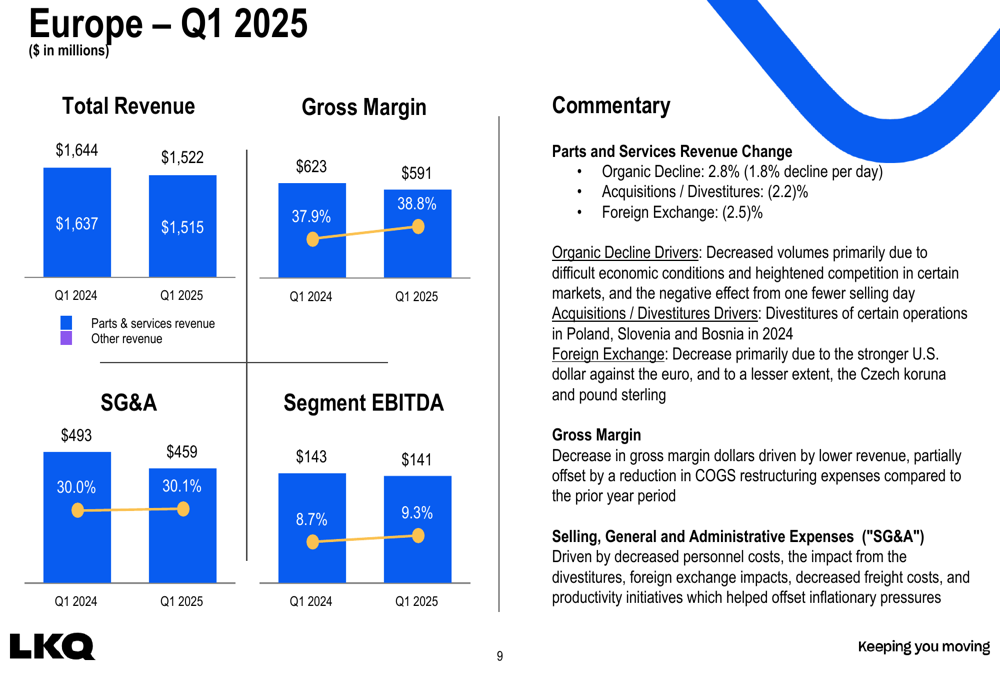

European operations faced similar challenges, with revenue declining 7.4% to $1.52 billion. However, segment EBITDA margin improved from 8.7% to 9.3% despite the revenue decline. Management cited "difficult economic conditions and heightened competition in certain markets" as primary factors for the organic decline of 2.8%.

The Self Service segment was a bright spot, with segment EBITDA increasing from 11.7% to 14.6% despite relatively flat revenue. This improvement helped offset some of the weakness in other segments.

Capital Allocation & Outlook

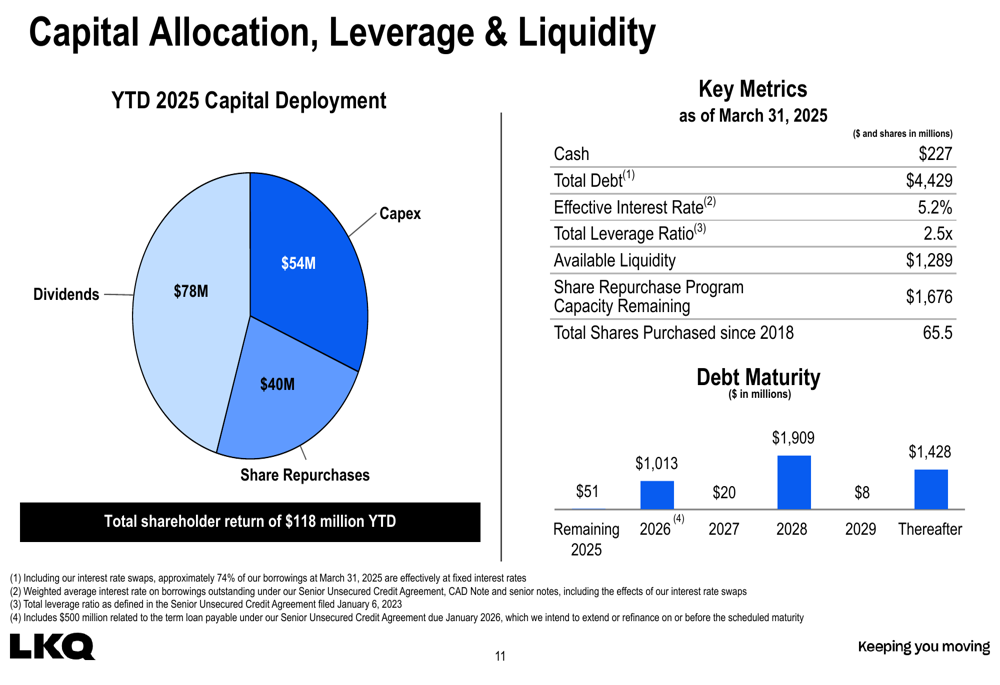

LKQ maintained a solid balance sheet with $227 million in cash and $1.29 billion in available liquidity as of March 31, 2025. The company’s total leverage ratio stood at 2.5x, with an effective interest rate of 5.2%.

The capital allocation strategy for the first quarter focused primarily on shareholder returns, with $78 million in dividends and $40 million in share repurchases, alongside $54 million in capital expenditures:

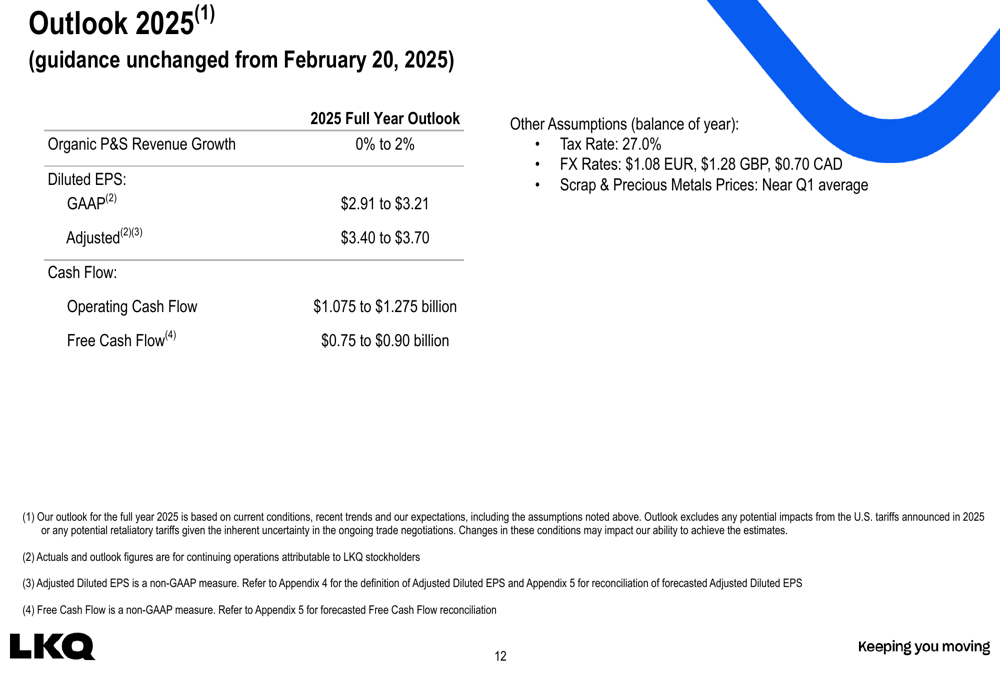

Despite the challenging first quarter, LKQ maintained its full-year 2025 guidance, projecting:

- Organic parts and services revenue growth of 0% to 2%

- Diluted EPS of $2.91 to $3.21 (GAAP) and $3.40 to $3.70 (adjusted)

- Operating cash flow of $1.075 to $1.275 billion

- Free cash flow of $0.75 to $0.90 billion

CFO Rick Galloway emphasized that the company expects improved performance in the coming quarters, stating, "We remain confident in our full-year outlook despite the slow start to 2025. Our operational efficiency initiatives and strategic focus on margin expansion will help offset the revenue challenges we faced in Q1."

The company’s ability to maintain its full-year guidance suggests management believes the first quarter challenges are temporary rather than indicative of a longer-term trend. Investors will be watching closely to see if the anticipated recovery materializes in subsequent quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.