Gold prices rebound as risk-off mood grips markets; US payroll data awaited

Loblaw Companies Limited (TSX:L) presented its second-quarter 2025 results on July 24, showing strong performance across both its food and drug retail segments. The Canadian retail giant reported a 5.2% increase in consolidated revenue and an 11.6% jump in adjusted earnings per share, demonstrating resilience in a challenging retail environment.

Quarterly Performance Highlights

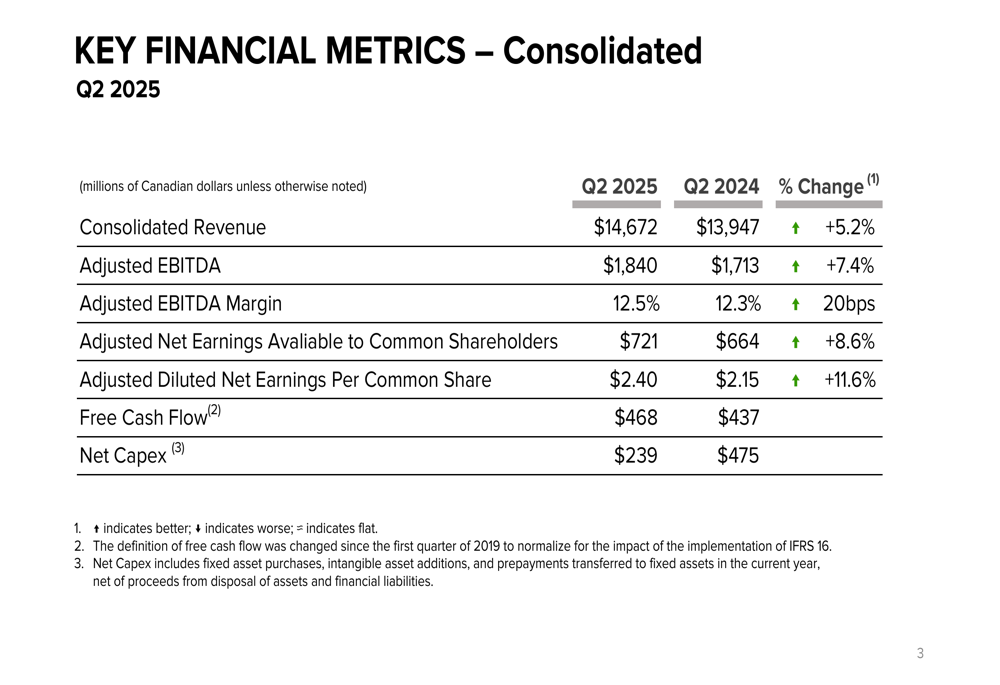

Loblaw’s Q2 2025 results showed robust growth across all key financial metrics. Consolidated revenue reached $14,672 million, a 5.2% increase compared to $13,947 million in the same quarter last year. Adjusted EBITDA grew by 7.4% to $1,840 million, with the adjusted EBITDA margin expanding by 20 basis points to 12.5%.

The company’s adjusted net earnings available to common shareholders increased by 8.6% to $721 million, while adjusted diluted earnings per share rose by 11.6% to $2.40, outpacing revenue growth and indicating improved operational efficiency.

As shown in the following consolidated financial metrics chart:

Free cash flow improved to $468 million compared to $437 million in Q2 2024, while net capital expenditure decreased significantly to $239 million from $475 million in the prior year, suggesting a more disciplined approach to capital allocation.

Detailed Financial Analysis

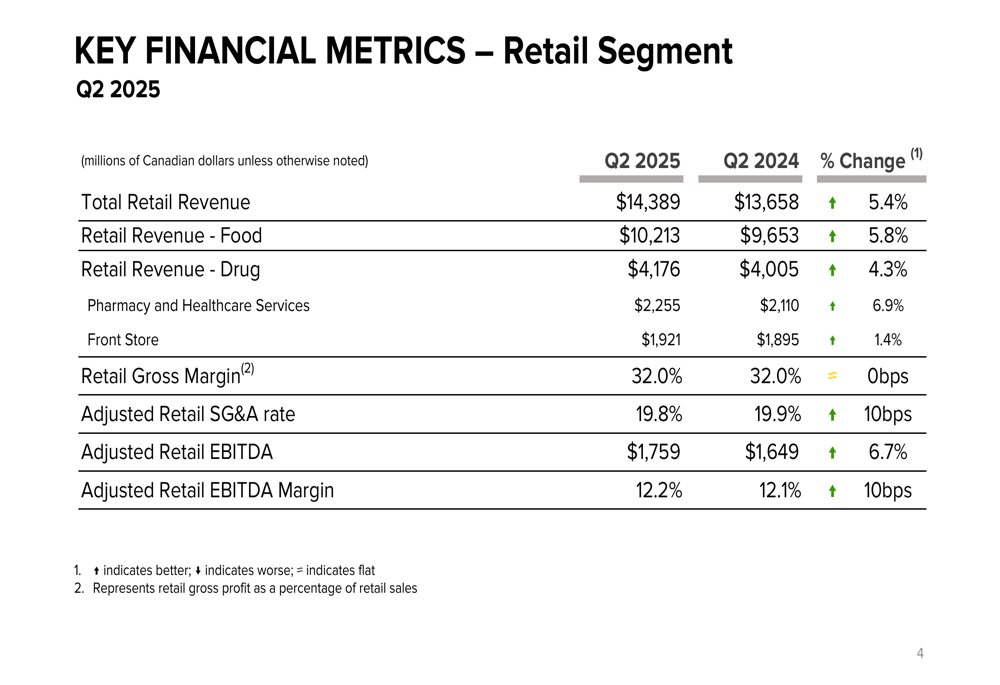

Loblaw’s retail segment, which accounts for the vast majority of the company’s business, posted a 5.4% increase in revenue to $14,389 million. The food retail division saw revenue growth of 5.8% to $10,213 million, while drug retail revenue increased by 4.3% to $4,176 million.

Within the drug retail segment, pharmacy and healthcare services performed particularly well, with revenue increasing by 6.9% to $2,255 million. Front store revenue in the drug retail segment grew by a more modest 1.4% to $1,921 million.

The following retail segment performance chart illustrates these results:

Retail gross margin remained stable at 32.0%, while the adjusted retail SG&A rate improved by 10 basis points to 19.8%, demonstrating the company’s ability to control costs despite inflationary pressures. Adjusted retail EBITDA increased by 6.7% to $1,759 million, with the margin expanding by 10 basis points to 12.2%.

Per Bank, CEO, emphasized the company’s commitment to delivering value and convenience during the earnings call, stating, "Our responsibility is to deliver value, quality, service, and convenience across every corner of our business." This focus appears to be resonating with customers, as evidenced by the operational metrics.

Operational Performance

Loblaw’s operational metrics showed positive momentum across both food and drug retail segments. Food retail same-store sales grew by 3.5%, with increases in both basket size and traffic. Drug retail same-store sales increased by 4.1%, driven by strong performance in pharmacy and healthcare services.

The following operational metrics chart provides a detailed breakdown:

Pharmacy and healthcare services saw same-store sales growth of 6.2%, supported by a 3.1% increase in prescription count and a 3.9% rise in average prescription value. Front store same-store sales in the drug retail segment grew by 1.7%.

These operational improvements align with Loblaw’s strategic initiatives, including the expansion of its store network. According to the earnings call, the company opened 20 new stores in the quarter and plans to open a total of 80 new locations by the end of 2025.

Strategic Initiatives & Outlook

Loblaw remains confident in its ability to meet its full-year outlook. The company’s strategic focus on digital innovation and AI-driven initiatives appears to be yielding positive results. Richard Dufresne, CFO, highlighted during the earnings call that "AI-driven initiatives are already yielding tangible improvements across key areas of our business."

The company also announced a 4-for-1 stock split effective August 18, 2025, signaling management’s optimism about future growth prospects. Additionally, Loblaw is exploring U.S. expansion with its T&T brand, which could provide a new avenue for growth beyond the Canadian market.

Despite these positive developments, Loblaw faces several challenges, including consumer price sensitivity, potential supply chain disruptions, and market saturation in Canada. However, the company’s focus on value offerings, particularly through its discount retail formats, positions it well to navigate these challenges.

Loblaw’s stock closed at CAD 55.19 following the earnings release, representing a 1% increase, which suggests positive investor reception of the Q2 results. Year-to-date, the stock has performed well, trading significantly above its 52-week low of CAD 43.32, though still below its 52-week high of CAD 59.70.

The company’s forward-looking statements, as outlined in its presentation, indicate continued focus on strategic objectives, financial performance, and operational efficiency, though these are subject to various risks and uncertainties as detailed in the company’s regulatory filings.

With strong Q2 2025 results across both food and drug retail segments, Loblaw appears well-positioned to maintain its market leadership in the Canadian retail landscape while pursuing new growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.