Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

Defense giant Lockheed Martin Corporation (NYSE:LMT) reported solid first-quarter 2025 results on April 22, showing continued momentum in its growth strategy. The company’s shares were up 2.99% in premarket trading to $472.02, reflecting positive investor sentiment following the earnings release. This performance builds on Lockheed’s previous quarter, where the company had taken steps to de-risk classified programs that had impacted Q4 2024 results.

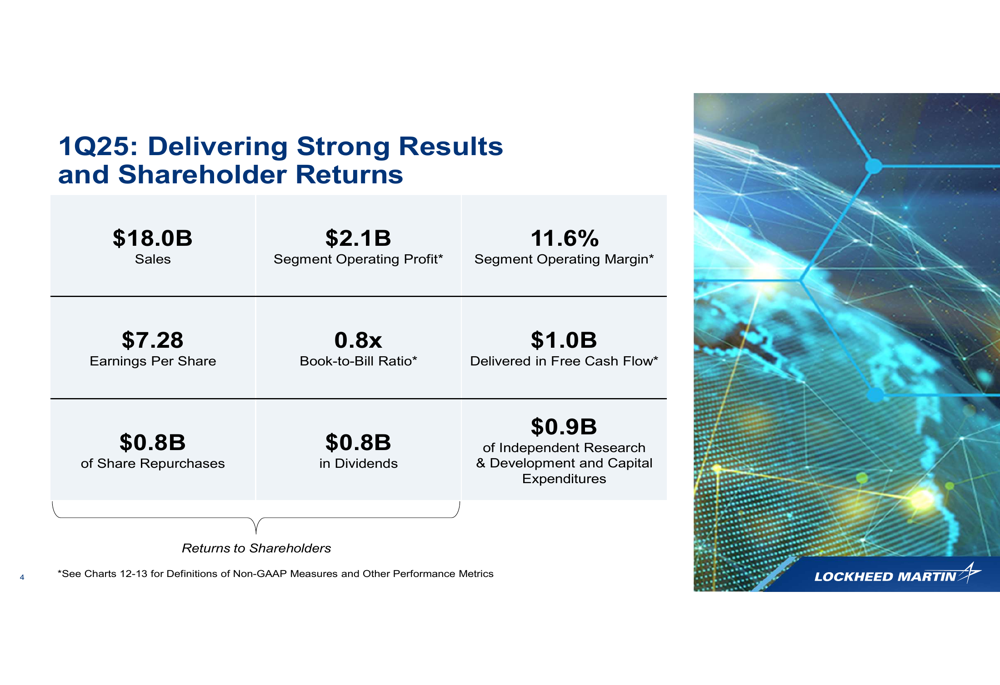

As shown in the following overview slide, Lockheed Martin emphasized building momentum in Q1 with solid financial results while remaining committed to its strategic vision:

Quarterly Performance Highlights

Lockheed Martin reported Q1 2025 sales of $18.0 billion, representing a 4% year-over-year increase. The company achieved segment operating profit of $2.1 billion with an 11.6% operating margin, demonstrating strong operational execution. Earnings per share came in at $7.28, while free cash flow reached $1.0 billion for the quarter.

The company’s book-to-bill ratio was 0.8x, indicating that while new orders were slightly below sales for the quarter, Lockheed continues to maintain a robust backlog. The company returned significant value to shareholders through $0.8 billion in share repurchases and $0.8 billion in dividends, while also investing $0.9 billion in research and development and capital expenditures.

The following slide details these key financial metrics for Q1 2025:

Segment Analysis

Lockheed Martin’s four business segments showed varying performance, with three reporting sales growth and all four delivering improved operating profits and margins.

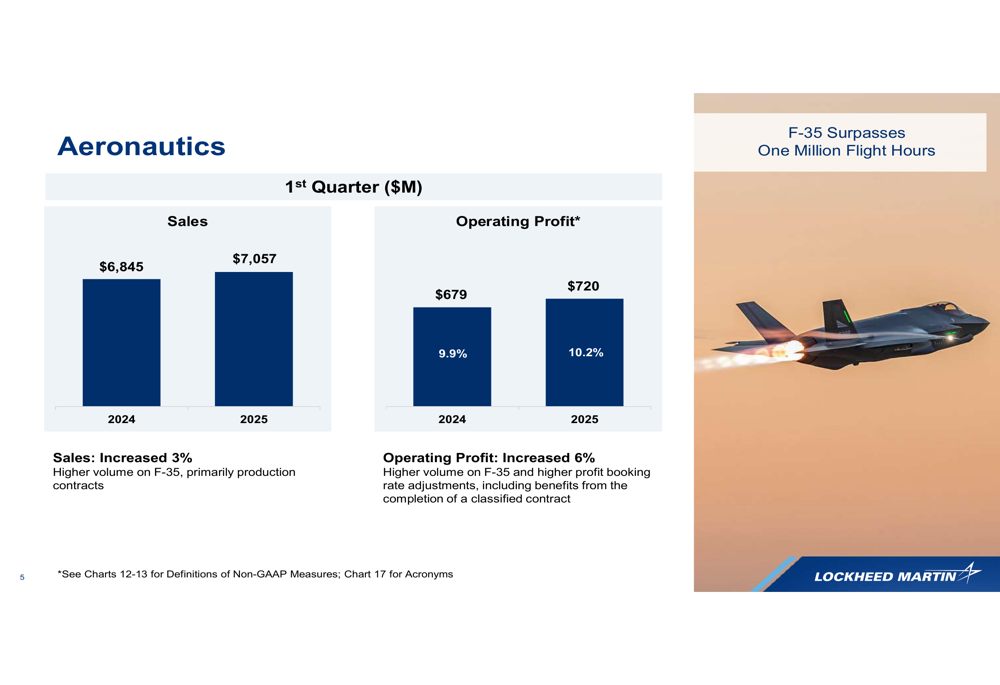

The Aeronautics segment, which includes the F-35 fighter jet program, reported sales of $7.06 billion, up 3% from Q1 2024. Operating profit increased 6% to $720 million, with margins improving from 9.9% to 10.2%. The growth was primarily driven by higher volume on F-35 production contracts.

As shown in the following chart detailing Aeronautics performance:

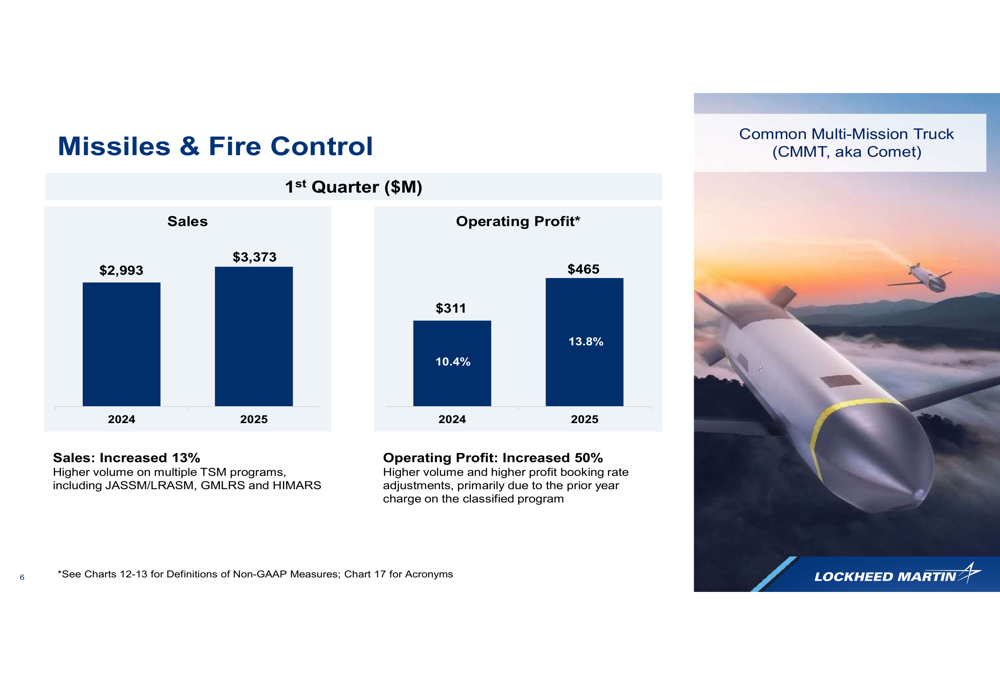

The Missiles & Fire Control (MFC) segment was the standout performer, with sales increasing 13% to $3.37 billion. This growth was driven by higher volumes across multiple Tactical Strike Missile programs, including JASSM/LRASM, GMLRS, and HIMARS. Operating profit surged 50% to $465 million, with margins expanding significantly from 10.4% to 13.8%. The substantial profit improvement was attributed to higher volume and favorable profit booking rate adjustments, following a prior year charge on a classified program.

The following slide illustrates MFC’s impressive performance:

Rotary & Mission Systems (RMS) delivered a strong quarter with sales of $4.33 billion, up 6% year-over-year. The growth was driven by higher volumes on Combat System Computer and Radar programs, as well as increased Blackhawk helicopter production at Sikorsky. Operating profit rose 21% to $521 million, with margins improving from 10.5% to 12.0%. This improvement was attributed to higher volume, favorable profit booking rate adjustments, and a benefit related to an intellectual property license arrangement.

The Space segment was the only business area to report a sales decline, with revenue decreasing 2% to $3.21 billion due to lower volume in National Security Space, primarily related to the Overhead Persistent Infrared (OPIR) program. However, operating profit increased 17% to $379 million, with margins expanding from 9.9% to 11.8%. The profit improvement was driven by higher profit booking rate adjustments, primarily related to a contract completion event, partially offset by lower equity earnings from United Launch Alliance (ULA).

Strategic Initiatives

Lockheed Martin emphasized its commitment to its "21st Century Strategic Vision," focusing on investments and partnerships to accelerate technology roadmaps. The company highlighted its operational transformation initiatives, including 1LMX (One Lockheed Martin Experience) and Accelerating Performance Excellence (APEX), which aim to improve efficiency and drive innovation across the enterprise.

These strategic initiatives align with comments made by CEO Jim Taiclet during the Q4 2024 earnings call, where he noted that the company’s "return to growth strategy that we implemented 3 years ago is well on its way and remains on a strong trajectory." The Q1 2025 results appear to validate this strategy, with solid growth across most segments and improved operational performance.

Forward-Looking Statements

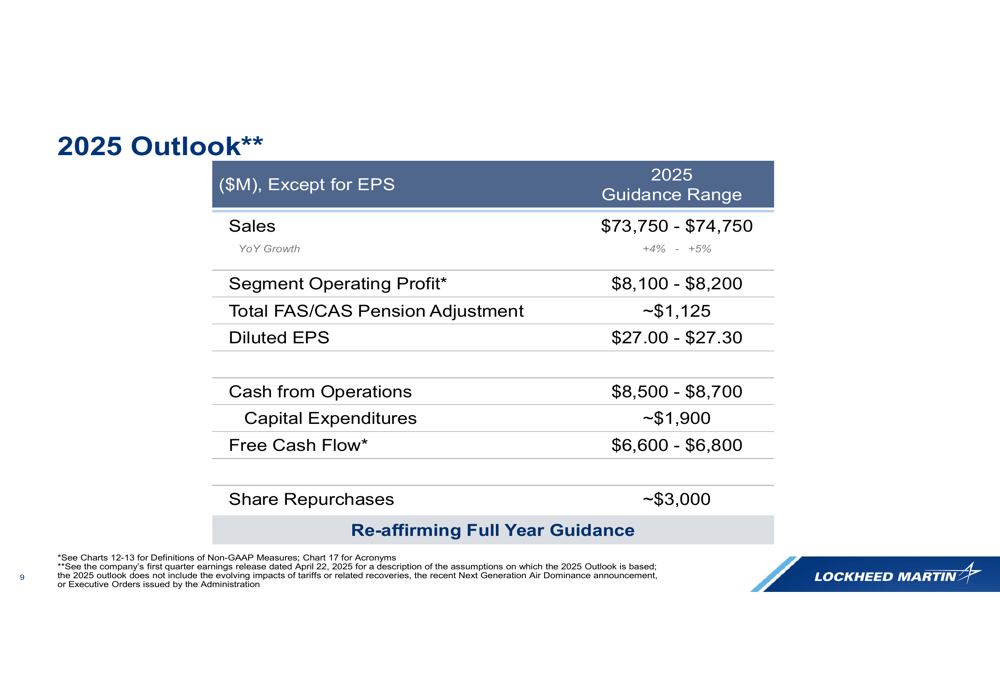

Lockheed Martin provided a positive outlook for 2025, projecting sales of $73.75-74.75 billion, representing 4-5% year-over-year growth. The company expects segment operating profit of $8.1-8.2 billion and diluted EPS of $27.00-27.30. Free cash flow is projected at $6.6-6.8 billion, with planned share repurchases of approximately $3 billion.

The following slide details the company’s full-year 2025 outlook:

The outlook aligns with statements made during the Q4 2024 earnings call, where management indicated expectations for "mid single digit growth in sales, segment operating margins returning to 11% and double digit growth in free cash flow per share" for 2025.

Lockheed Martin summarized its Q1 2025 performance and forward outlook with four key points: solid financial results to start the year, prioritizing resources to execute backlog and deliver commitments, building momentum to deliver on the 2025 financial outlook, and focusing on creating long-term value for customers and shareholders.

Conclusion

Lockheed Martin’s Q1 2025 results demonstrate the company’s continued execution of its growth strategy, with solid performance across most business segments. The Missiles & Fire Control segment’s outstanding results highlight the ongoing demand for advanced defense systems amid global security concerns.

With a positive outlook for the remainder of 2025, Lockheed Martin appears well-positioned to capitalize on its strong backlog and deliver value to shareholders through continued growth, margin improvement, and capital returns. The company’s focus on strategic investments in research and development, along with operational transformation initiatives, should help maintain its competitive edge in the defense industry.

Investors will likely continue to monitor the company’s execution on major programs, particularly the F-35, as well as its ability to convert its substantial backlog into revenue growth while maintaining strong margins across all business segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.