ReElement Technologies stock soars after securing $1.4B government deal

Introduction & Market Context

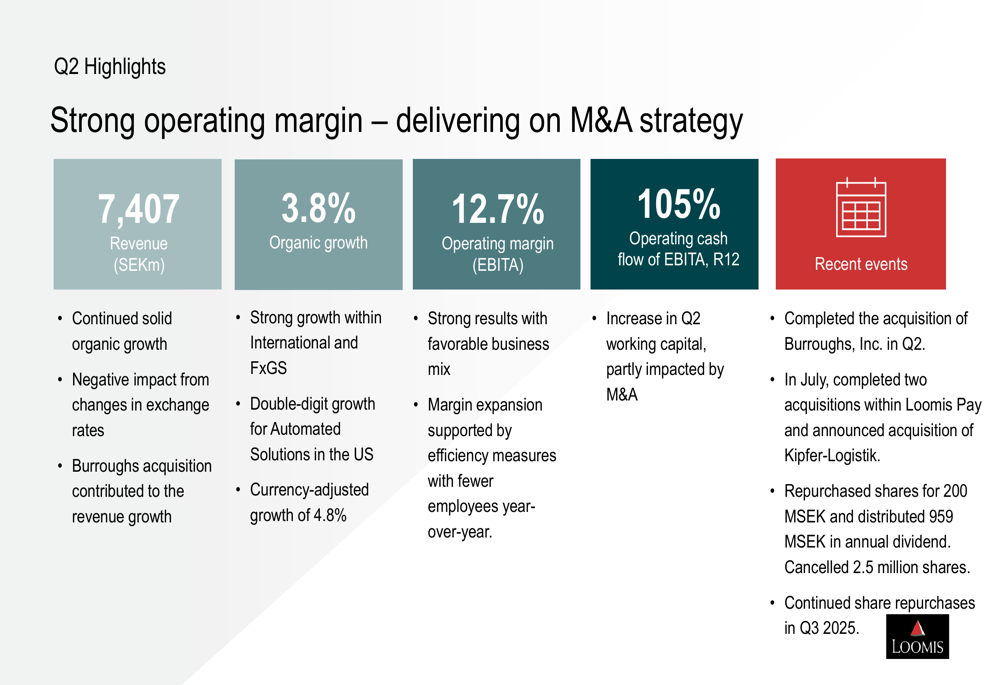

Loomis AB (STO:LOOMIS) presented its second quarter 2025 results on July 25, 2025, highlighting solid organic growth and improved profitability across its business segments. The company reported a 3.8% organic growth with revenue reaching SEK 7,407 million, while its operating margin (EBITA) expanded to 12.7%, up from 11.6% in the same period last year.

The cash management and logistics company continues to execute its growth strategy through strategic acquisitions while maintaining financial discipline, with a net debt to EBITDA ratio of 1.75. Loomis shares have performed well in 2025, with a year-to-date return of 20.26% according to market data, and the stock closed at SEK 390.4 in recent trading.

Quarterly Performance Highlights

Loomis delivered strong second quarter results, with operating income (EBITA) reaching SEK 944 million compared to SEK 887 million in Q2 2024. Basic earnings per share increased significantly to SEK 7.01 from SEK 5.65 in the prior year period, representing a 24% improvement.

As shown in the following quarterly highlights:

The company’s performance was driven by continued solid organic growth, particularly strong growth in the International and FXGS business lines, a favorable business mix, and efficiency measures. The operating cash flow remained robust at 105% of EBITA on a rolling 12-month basis.

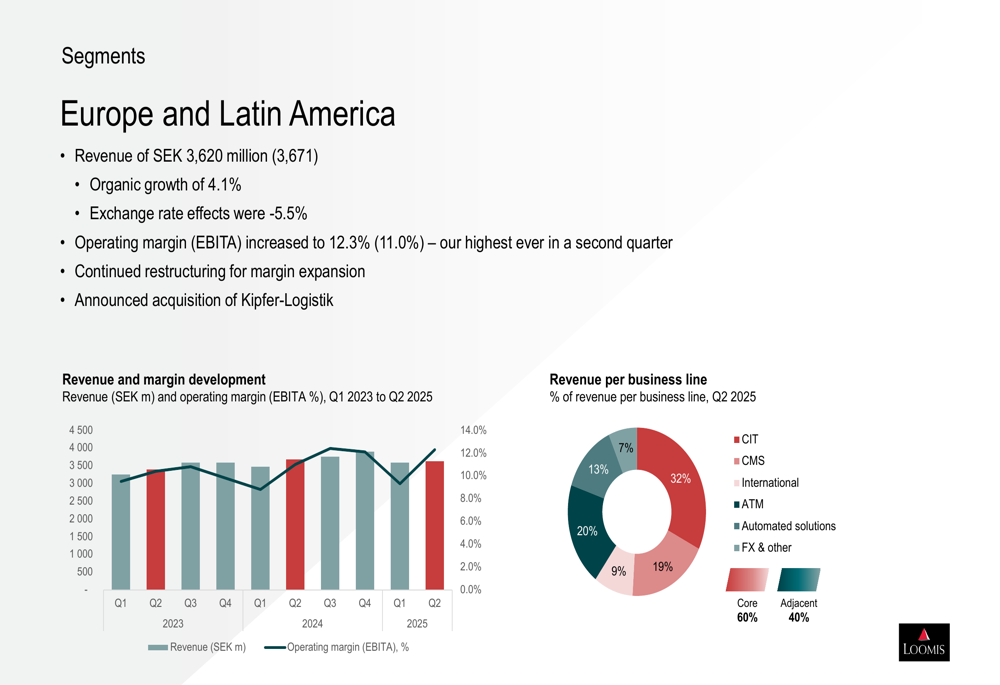

In the Europe and Latin America segment, Loomis achieved revenue of SEK 3,620 million with organic growth of 4.1%. The segment posted its highest-ever second-quarter operating margin of 12.3%, benefiting from continued restructuring efforts aimed at margin expansion.

The segment breakdown shows diversification across business lines:

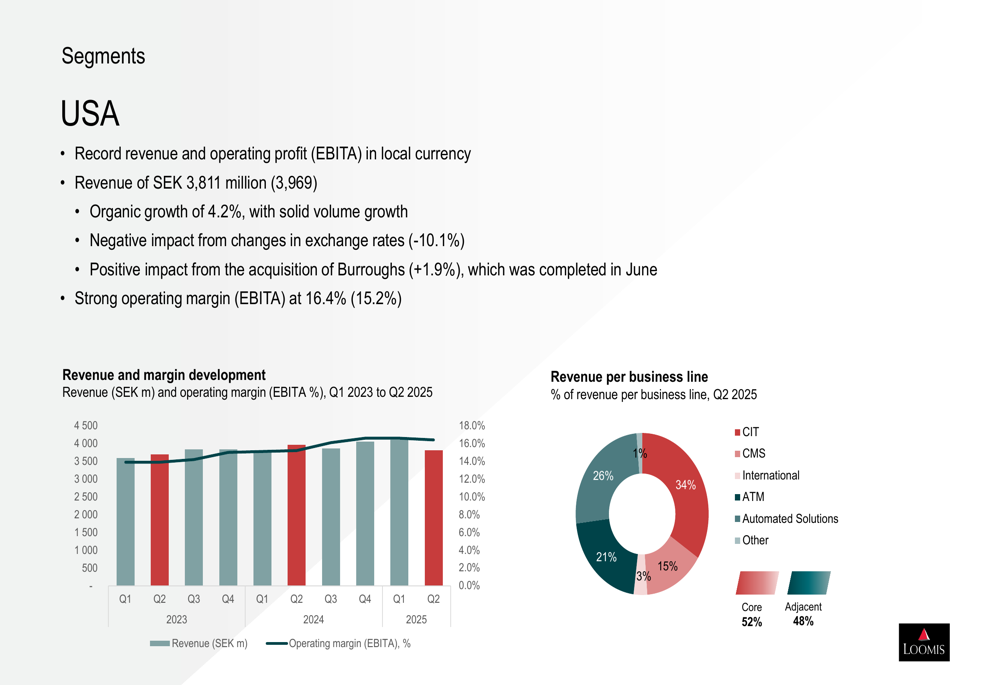

The USA segment delivered record revenue and operating profit in local currency, with reported revenue of SEK 3,811 million and organic growth of 4.2%. Despite negative impact from exchange rates (-10.1%), the segment maintained a strong operating margin of 16.4%. The acquisition of Burroughs, completed in June, contributed positively with a 1.9% impact on revenue.

The USA segment’s business mix is illustrated below:

The newly formed SME/Pay segment, established in 2025, reported revenue of SEK 43 million. While still in early phases, the operating income improved to SEK -41 million. Loomis strengthened this segment by acquiring two POS companies in Spain in July 2025: Central Cash and Sighore-ICS.

Detailed Financial Analysis

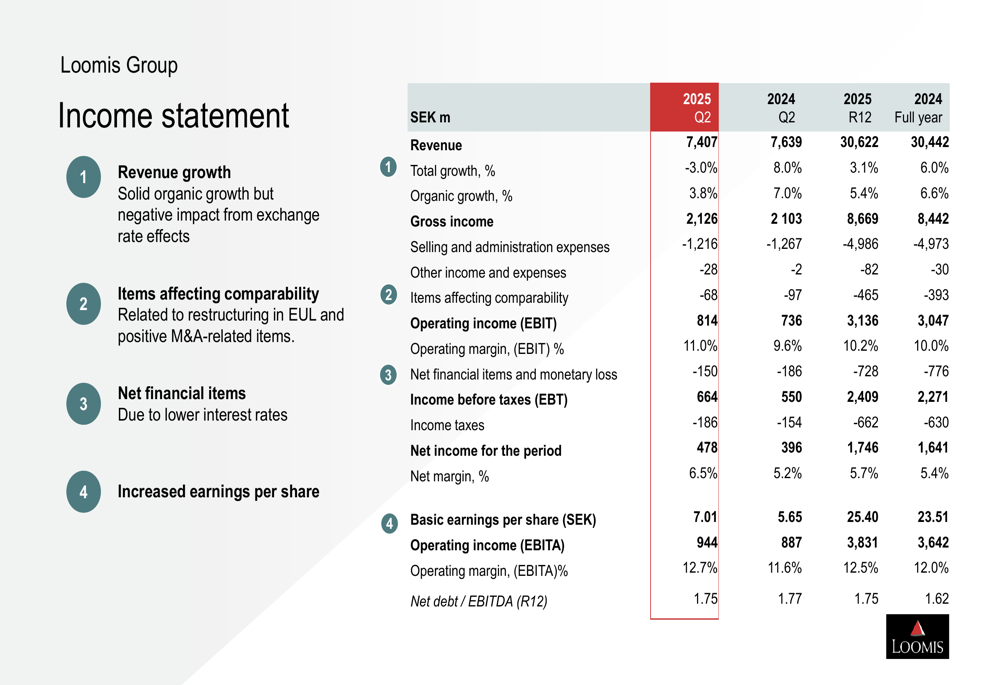

Loomis’ comprehensive income statement reveals solid performance across key financial metrics. The company maintained strong profitability with a net margin of 6.5% in Q2 2025, up from 5.2% in the same period last year.

The detailed income statement provides a clear picture of the company’s financial performance:

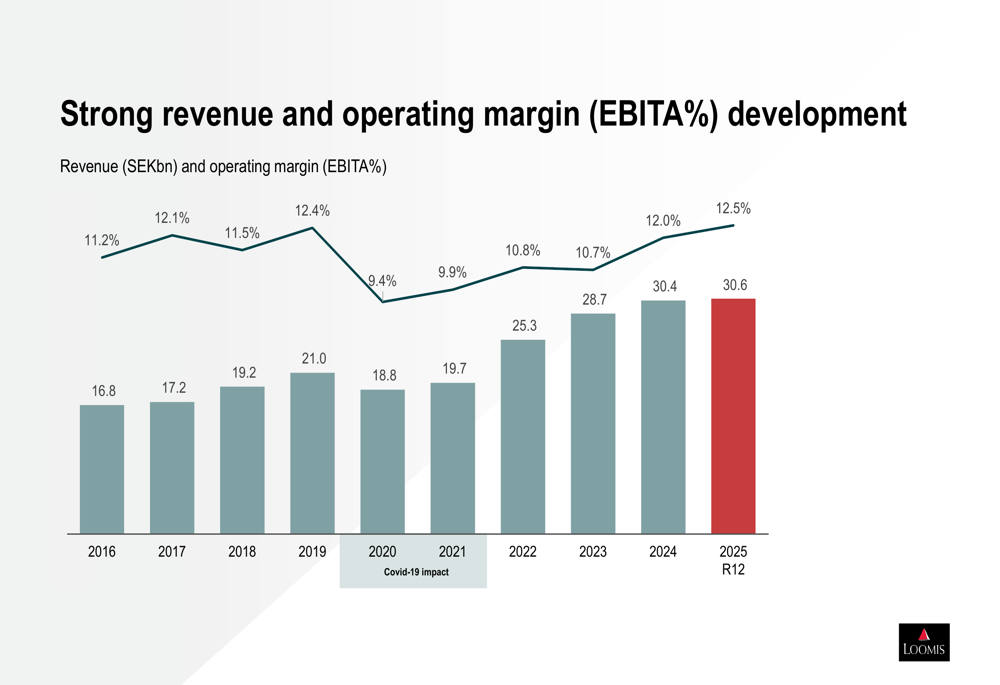

Looking at long-term trends, Loomis has demonstrated consistent revenue growth and margin improvement since 2016, with only a temporary setback during the pandemic years. The company’s revenue has grown from SEK 16.8 billion in 2016 to SEK 30.6 billion on a rolling 12-month basis in 2025, while operating margins have expanded from 11.2% to 12.5% over the same period.

This long-term performance trend is illustrated in the following chart:

Strategic Initiatives

Loomis continues to execute its growth strategy through strategic acquisitions. During the quarter, the company completed the acquisition of Burroughs, which contributed positively to the USA segment’s performance. Additionally, Loomis announced the acquisition of Kipfer-Logistik, further strengthening its European operations.

In July 2025, Loomis acquired two POS companies in Spain—Central Cash and Sighore-ICS—to bolster its SME/Pay segment. These acquisitions align with the company’s stated strategy of prioritizing value-creating acquisitions while maintaining financial discipline.

According to CEO Aritz Larrea, "We have a stable and resilient business model that has proven itself over time. We will continue to add to our growth by prioritizing value-creating acquisitions and taking a structured approach to gain further operational efficiencies."

Sustainability Efforts

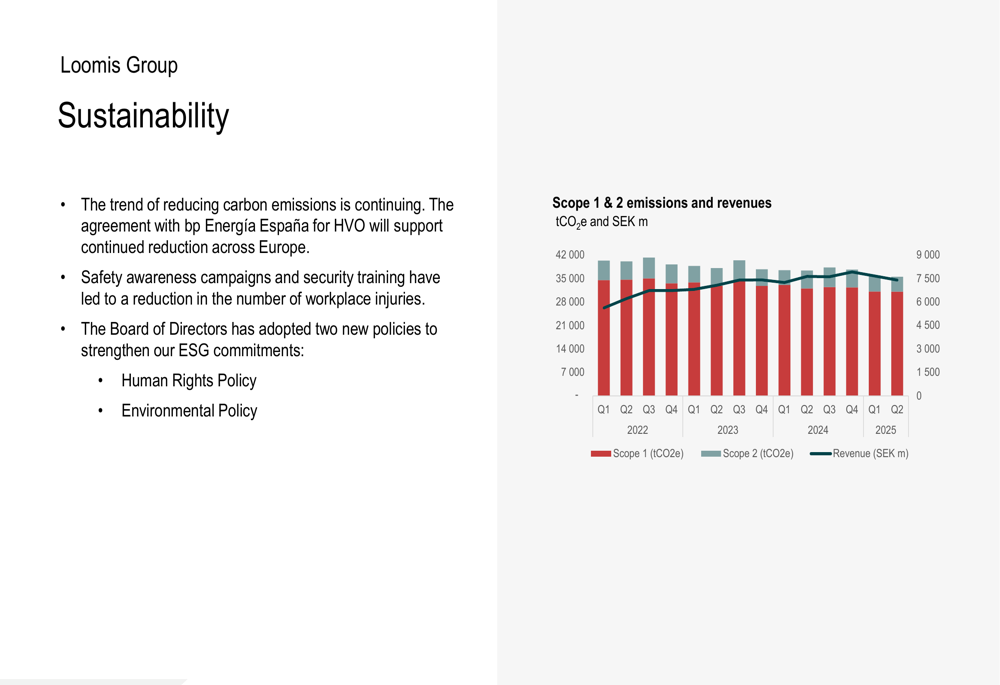

Loomis continues to make progress on its sustainability initiatives, with a focus on reducing carbon emissions. The company has entered into an agreement with bp Energía España for HVO (Hydrotreated Vegetable Oil) to support its emission reduction efforts.

Safety remains a priority, with awareness campaigns and security training contributing to a reduction in workplace injuries. The Board of Directors has adopted two new policies to strengthen ESG commitments: a Human Rights Policy and an Environmental Policy.

The company’s progress in reducing carbon emissions while growing revenue is illustrated below:

Forward-Looking Statements

Loomis remains committed to its growth strategy, focusing on value-creating acquisitions and operational efficiencies. The company is targeting over 90% cash conversion and expects continued benefits from its restructuring initiatives.

Future projections include an EPS forecast of 0.94 USD for Q4 2025 and 0.90 USD for Q1 2026, with revenue forecasts of 835.75 USD million and 853.26 USD million, respectively.

Key challenges ahead include economic fluctuations impacting currency-adjusted growth, integration risks associated with recent acquisitions, potential regulatory changes in key markets, competitive pressures in the pharmaceutical logistics sector, and successful execution of restructuring initiatives.

With strong cash flow generation, evidenced by a 13% free cash flow yield, and a history of maintaining dividend payments for 17 consecutive years, Loomis demonstrates robust financial fundamentals that position it well for continued growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.