Bank of America just raised its EUR/USD forecast

Lumentum Holdings Inc (NASDAQ:LITE) reported strong third-quarter fiscal 2025 results on May 6, exceeding guidance on both revenue and earnings per share, driven primarily by robust demand from cloud customers. The optical and photonic products manufacturer continues to benefit from the growing AI infrastructure buildout.

Quarterly Performance Highlights

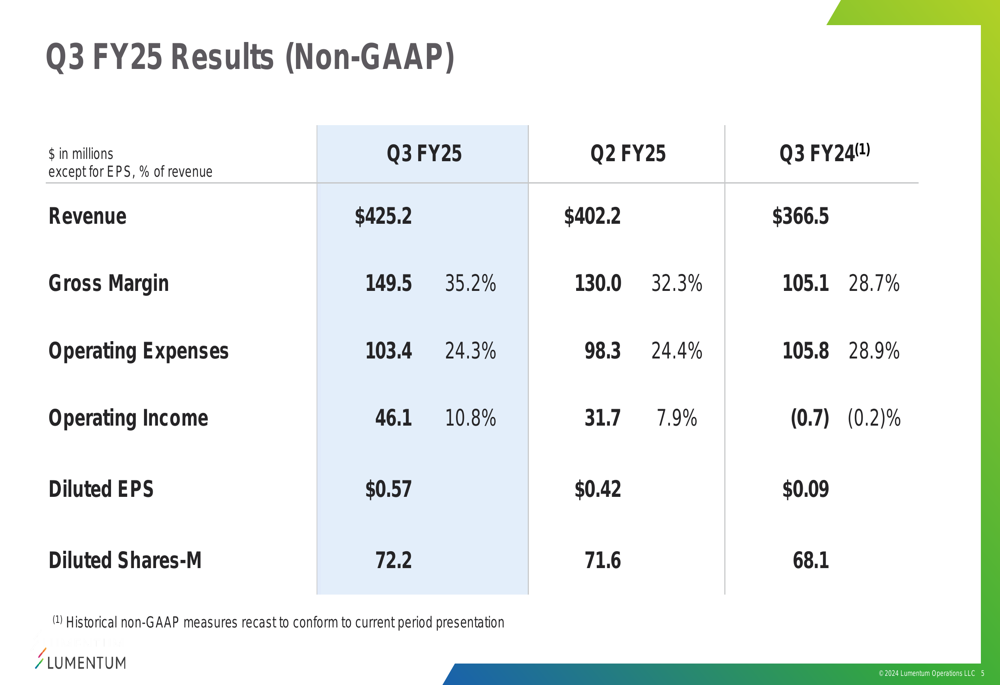

Lumentum reported Q3 FY25 revenue of $425.2 million, representing a 5.7% increase quarter-over-quarter and a 16% rise year-over-year. The company’s non-GAAP earnings per share reached $0.57, significantly higher than the $0.42 reported in the previous quarter and the $0.09 recorded in the same period last year.

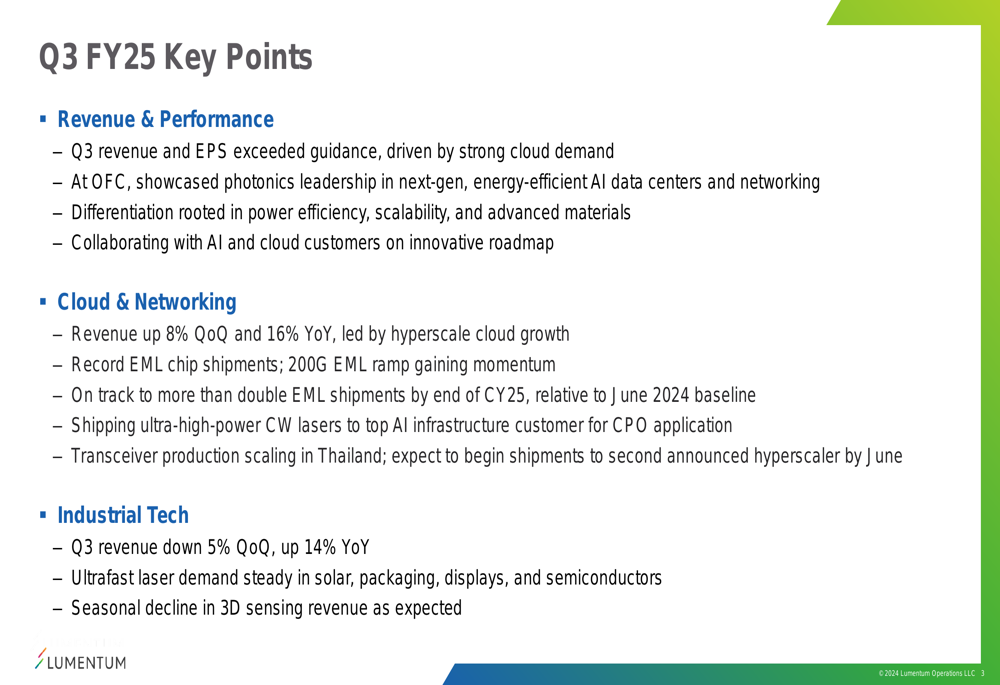

"Q3 revenue and EPS exceeded guidance, driven by strong cloud demand," the company noted in its presentation, highlighting its showcase of photonics leadership in next-generation, energy-efficient AI data centers and networking at the recent OFC conference.

As shown in the following slide summarizing key points from the quarter:

The company emphasized that its differentiation is rooted in power efficiency, scalability, and advanced materials, with ongoing collaboration with AI and cloud customers on innovative roadmaps.

Detailed Financial Analysis

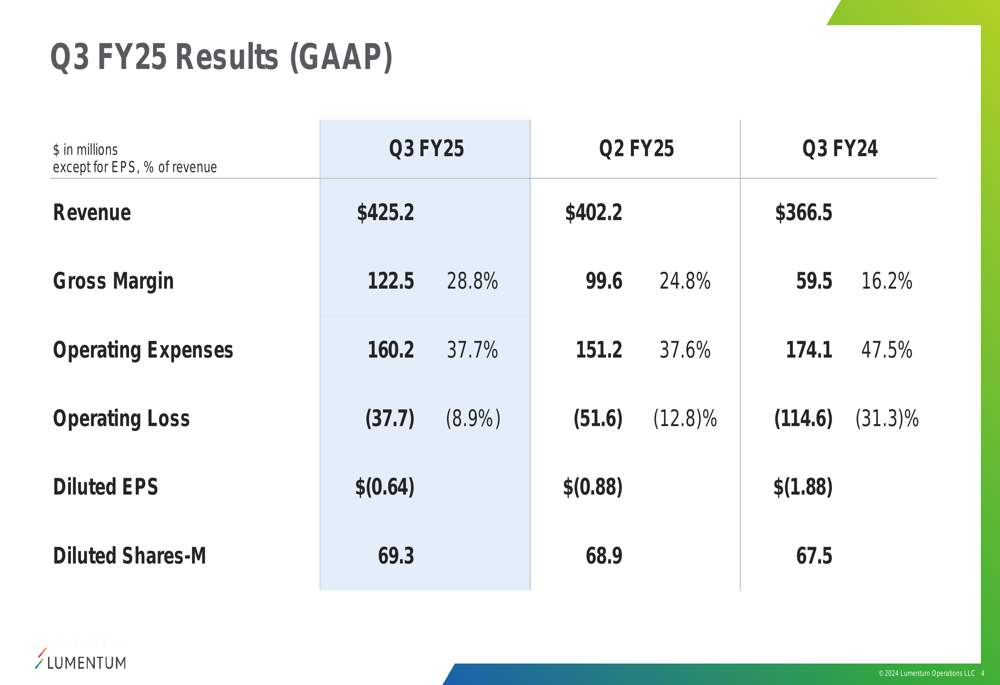

Lumentum’s financial performance showed substantial improvement across key metrics. On a GAAP basis, the company reported a reduced operating loss of $37.7 million (8.9% of revenue) compared to a $51.6 million loss in Q2 and a $114.6 million loss in the year-ago quarter.

The following slide details the GAAP financial results:

More importantly, on a non-GAAP basis, Lumentum achieved an operating income of $46.1 million, representing a 10.8% operating margin. This marks a significant improvement from the 7.9% operating margin in the previous quarter and a dramatic turnaround from the slight operating loss reported in Q3 FY24.

The non-GAAP results demonstrate the company’s improving profitability trajectory:

Gross margin improvement was particularly notable, with non-GAAP gross margin reaching 35.2% in Q3 FY25, up from 32.3% in Q2 and 28.7% in the year-ago period. This expansion reflects improved product mix and operational efficiencies.

Segment Performance

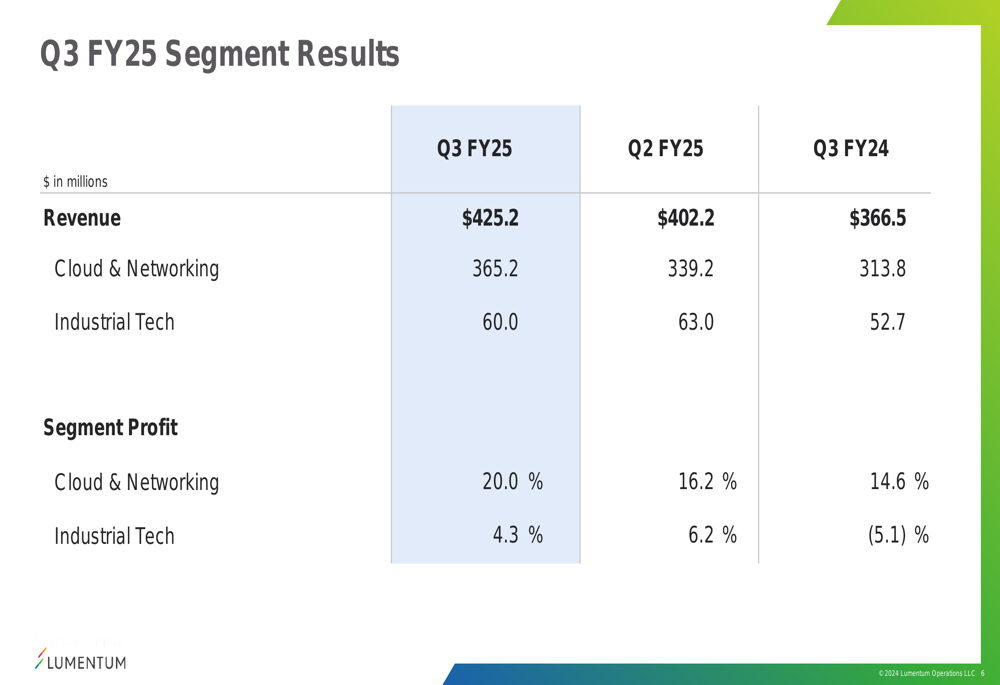

Lumentum’s business is divided into two main segments: Cloud & Networking and Industrial Tech. The Cloud & Networking segment, which represents approximately 86% of total revenue, continued its strong growth trajectory with revenue of $365.2 million, up 8% sequentially and 16% year-over-year.

The segment’s profit margin also improved significantly to 20.0%, compared to 16.2% in the previous quarter and 14.6% in the same period last year. This improvement reflects the company’s successful execution in high-growth cloud and AI markets.

The following slide provides a detailed breakdown of segment performance:

The Industrial Tech segment, while smaller at $60.0 million in revenue, saw a 5% sequential decline but a 14% year-over-year increase. The company noted that ultrafast laser demand remained steady across solar, packaging, displays, and semiconductor applications, while 3D sensing revenue experienced a seasonal decline as expected.

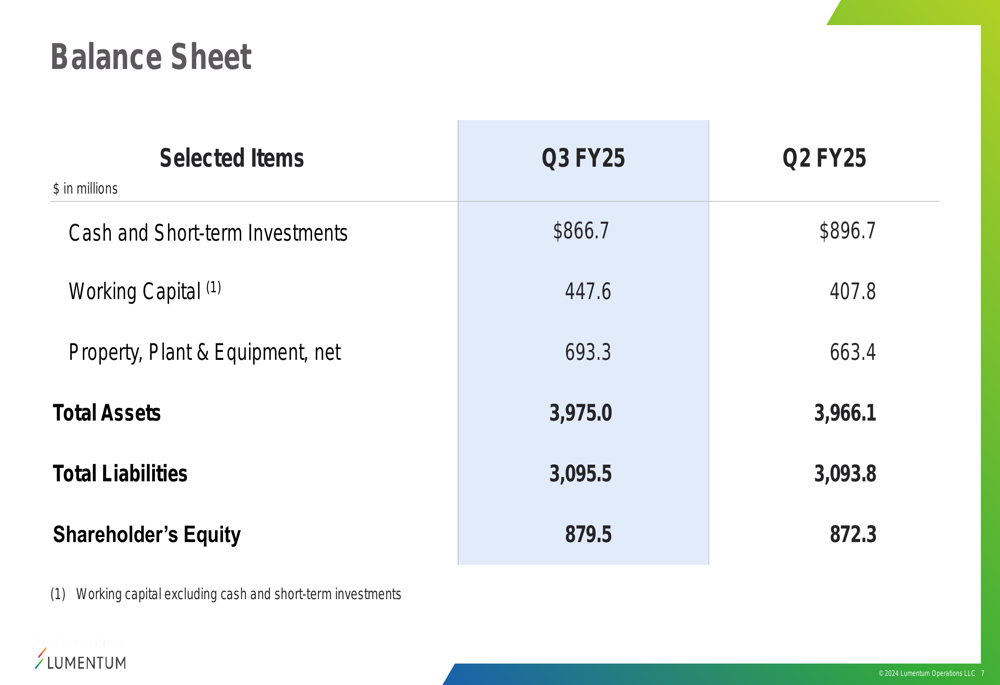

Balance Sheet and Liquidity

Lumentum maintained a strong financial position with $866.7 million in cash and short-term investments at the end of Q3, slightly down from $896.7 million in the previous quarter. Working capital increased to $447.6 million from $407.8 million, while property, plant, and equipment grew to $693.3 million, reflecting ongoing investments in production capacity.

The company’s balance sheet remains solid with total assets of $3,975.0 million and shareholders’ equity of $879.5 million, providing a strong foundation for continued growth and investment.

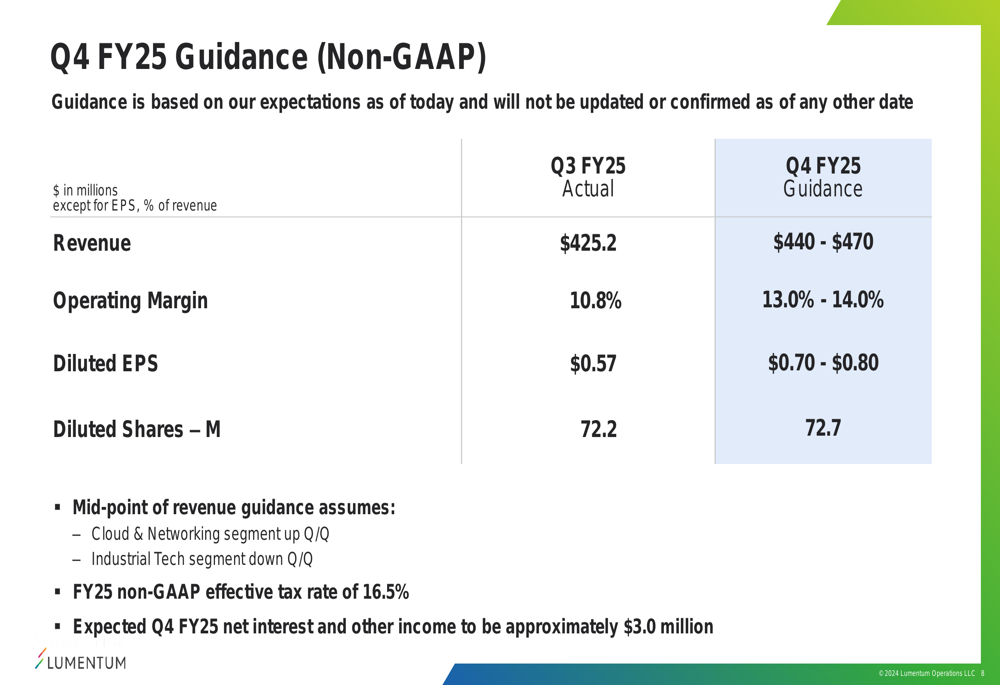

Forward Guidance

Looking ahead to Q4 FY25, Lumentum provided an optimistic outlook, projecting revenue between $440 million and $470 million, representing a sequential increase at the midpoint. The company also expects further margin expansion, with operating margin guidance of 13.0% to 14.0% and diluted EPS of $0.70 to $0.80.

This guidance assumes continued growth in the Cloud & Networking segment, partially offset by a sequential decline in the Industrial Tech segment. The company maintains a non-GAAP effective tax rate projection of 16.5% for fiscal 2025.

The following slide details the company’s Q4 FY25 guidance:

Strategic Initiatives

Lumentum highlighted several strategic initiatives and achievements during the quarter. The company reported record EML (Electro-absorption Modulated Laser) chip shipments, with the 200G EML ramp gaining momentum. Management confirmed they are on track to more than double EML shipments by the end of calendar year 2025, relative to the June 2024 baseline.

The company is also shipping ultra-high-power CW lasers to a top AI infrastructure customer for CPO (Co-Packaged Optics) applications, demonstrating its penetration into cutting-edge AI technologies.

Production scaling in Thailand continues to progress, with Lumentum expecting to begin shipments to a second announced hyperscale customer by June. This expansion of manufacturing capacity outside China aligns with the company’s strategy to enhance supply chain resilience and meet growing demand.

In after-hours trading following the earnings release, Lumentum shares rose 5.56% to $68.00, reflecting positive investor reaction to the results and outlook. The stock has shown significant momentum, trading well above its 52-week low of $38.28, though still below its 52-week high of $104.00.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.