Swisscom profit drops 23% as Vodafone Italia costs weigh on results

Introduction & Market Context

LU-VE Group (BIT:LUVE) presented its H1 2025 financial results on September 9, 2025, showing a return to growth in the second quarter after a challenging start to the year. The company’s shares responded positively, rising 3.51% to €32.80 on the day of the presentation.

The heat exchanger and air-cooled equipment manufacturer highlighted its recovery trajectory, with Q2 2025 sales growth offsetting the decline experienced in Q1. The company also achieved record order backlog and EBITDA margins, signaling strengthening business fundamentals despite mixed performance across different product segments.

Executive Summary

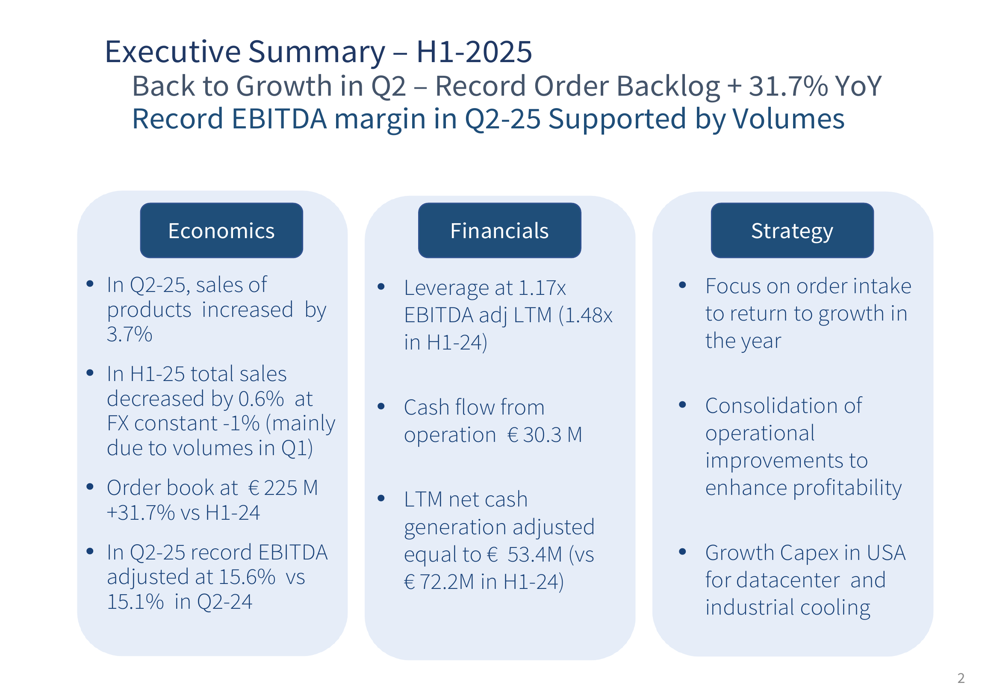

LU-VE Group’s H1 2025 results revealed a company in transition, with Q2 showing clear signs of recovery after a slower start to the year. Total sales decreased marginally by 0.6% year-over-year to €294.7 million, but Q2 sales increased by 3.2% compared to the same period last year.

As shown in the following executive summary slide, the company achieved a record order backlog of €225 million, representing a 31.7% increase compared to H1 2024:

The company’s profitability remained strong, with Q2 2025 delivering a record adjusted EBITDA margin of 15.6%, up from 15.1% in Q2 2024. This improvement was primarily driven by increased volumes and effective pricing strategies that more than offset rising operating costs.

Quarterly Performance Highlights

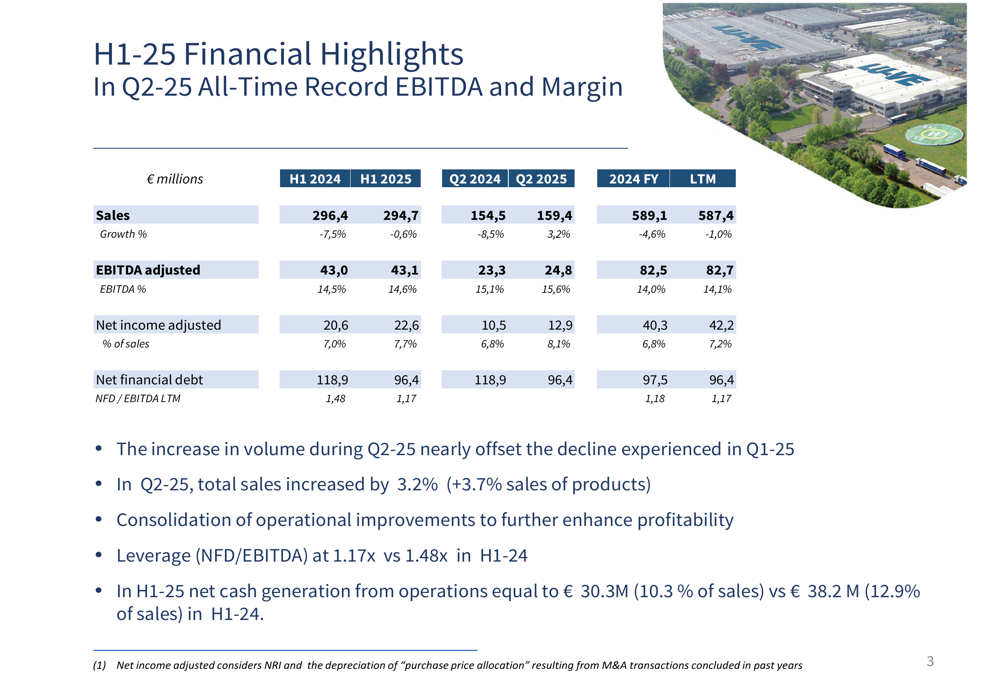

LU-VE Group’s financial performance in H1 2025 showed resilience despite challenging market conditions. The company maintained stable EBITDA at €43.1 million (adjusted) with a slight margin improvement to 14.6% compared to 14.5% in H1 2024.

The following table highlights key financial metrics, including the record EBITDA margin achieved in Q2 2025:

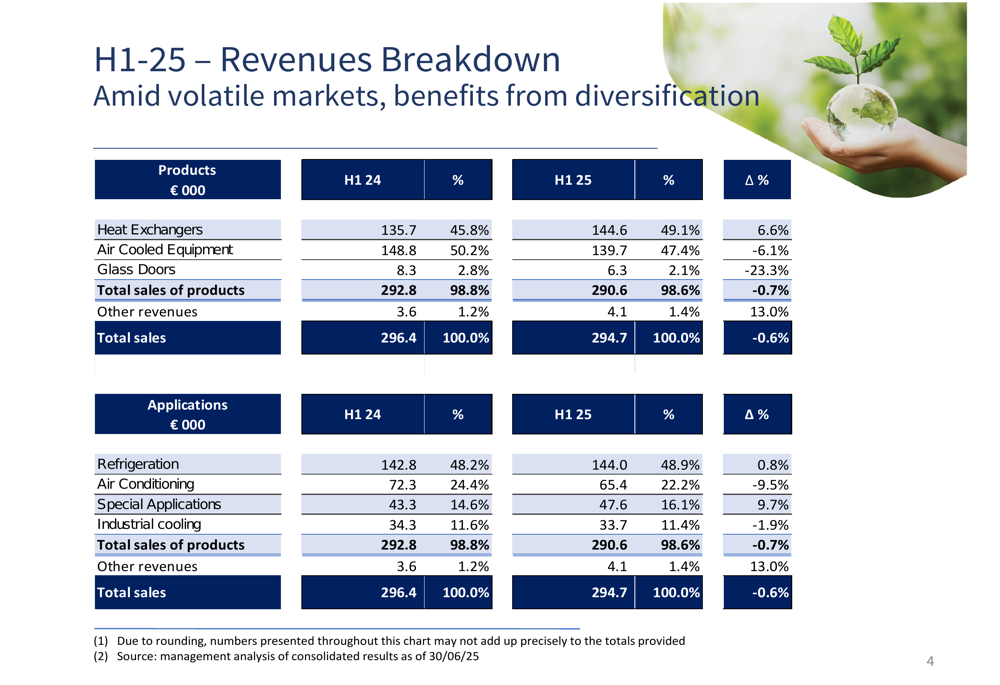

Revenue breakdown by product category revealed divergent performance across segments. Heat exchangers showed strong growth of 6.6% year-over-year, while air-cooled equipment declined by 6.1%. Special applications grew by 9.7%, offsetting a 9.5% decline in air conditioning.

The detailed revenue breakdown by product and application provides further insights into the company’s performance:

The company noted encouraging signs of recovery in heat pump heat exchangers, while air conditioning and mobile applications continued to face headwinds. The cooling systems business unit showed improvement in Q2 (-1.8%) compared to Q1 (-11.5%) and closed the quarter with its highest order book value in history.

Detailed Financial Analysis

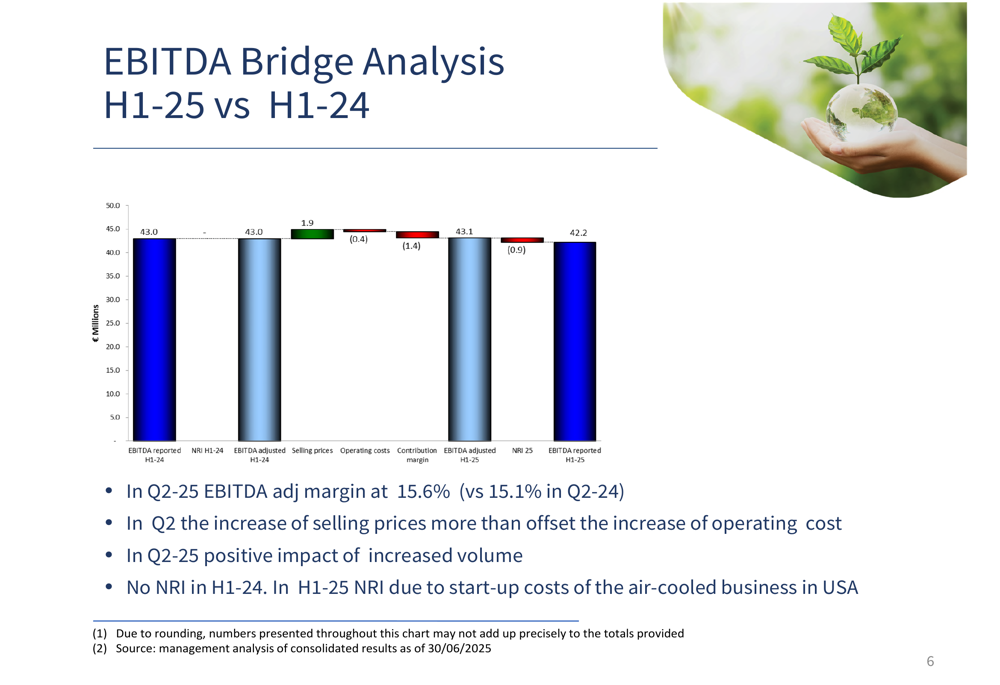

LU-VE Group’s EBITDA remained stable year-over-year despite slight revenue decline, demonstrating the company’s ability to maintain profitability through operational improvements and pricing strategies.

The following EBITDA bridge analysis illustrates how selling price increases of €1.9 million helped offset negative impacts from operating costs and contribution margin:

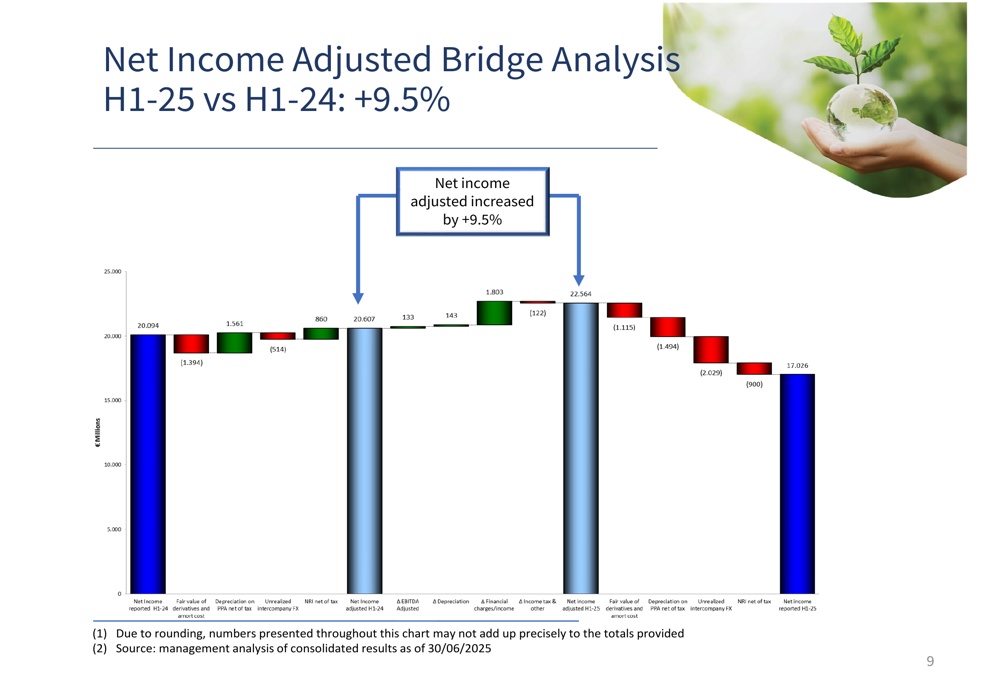

Net income adjusted increased by 9.5% to €22.6 million in H1 2025 from €20.6 million in H1 2024, representing 7.7% of sales compared to 7.0% in the previous year. This improvement was achieved despite challenges from unrealized foreign exchange losses and fair value adjustments on derivatives.

The bridge analysis below shows the progression from reported net income to adjusted net income, highlighting the impact of various adjustments:

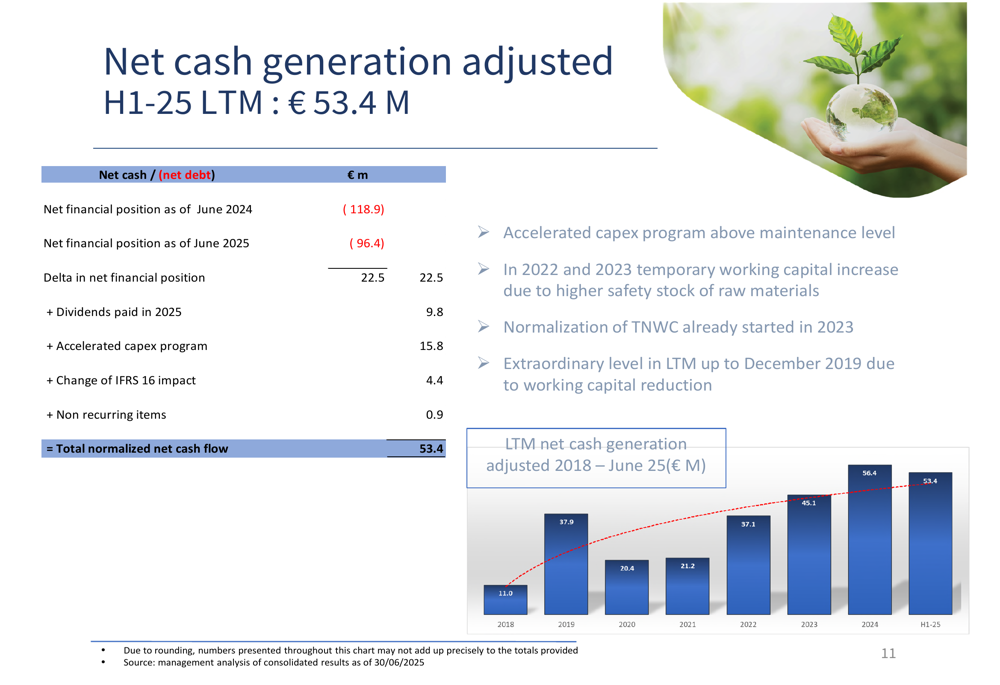

The company’s financial position continued to strengthen, with net financial debt decreasing to €96.4 million from €118.9 million a year earlier. This resulted in improved leverage with a net debt to EBITDA ratio of 1.17x, down from 1.48x in H1 2024.

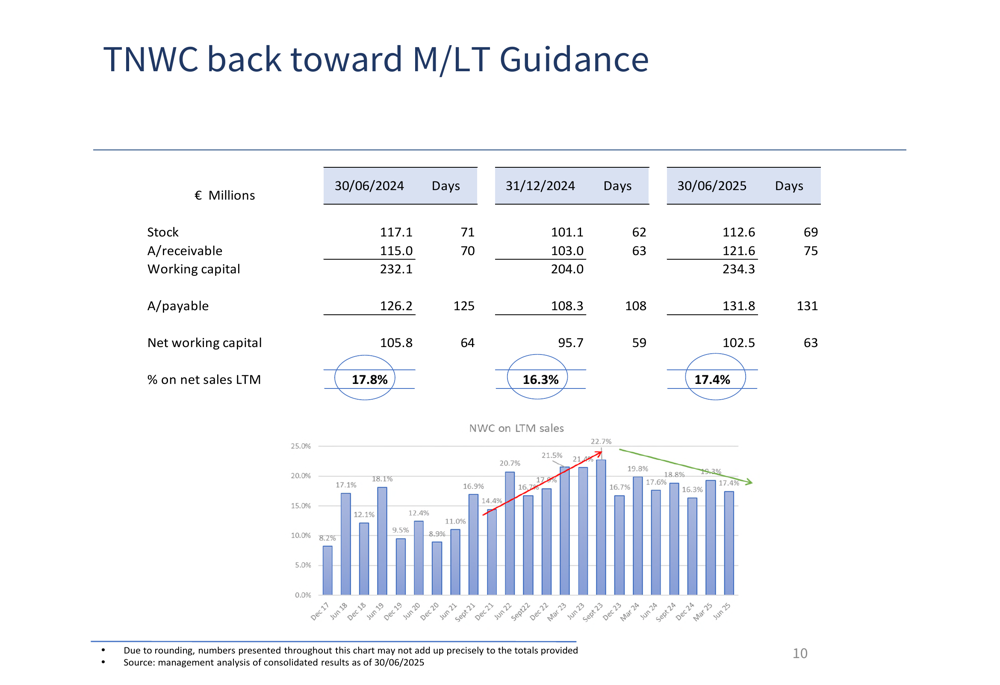

Total net working capital (TNWC) showed progress toward medium/long-term guidance, with days of working capital at 63 days as of June 30, 2025:

Strategic Initiatives

LU-VE Group continued to focus on strategic growth initiatives, particularly in the USA market for datacenter and industrial cooling applications. The company reported that the second stage of its plant expansion in the USA was in progress, with non-recurring costs in H1 2025 attributed to start-up costs for the air-cooled business in the USA.

The company generated strong cash flow from operations of €30.3 million in H1 2025, representing 10.3% of sales. While this was lower than the €38.2 million (12.9% of sales) generated in H1 2024, it still demonstrated solid cash conversion capabilities.

The following slide illustrates the company’s adjusted net cash generation of €53.4 million for the last twelve months:

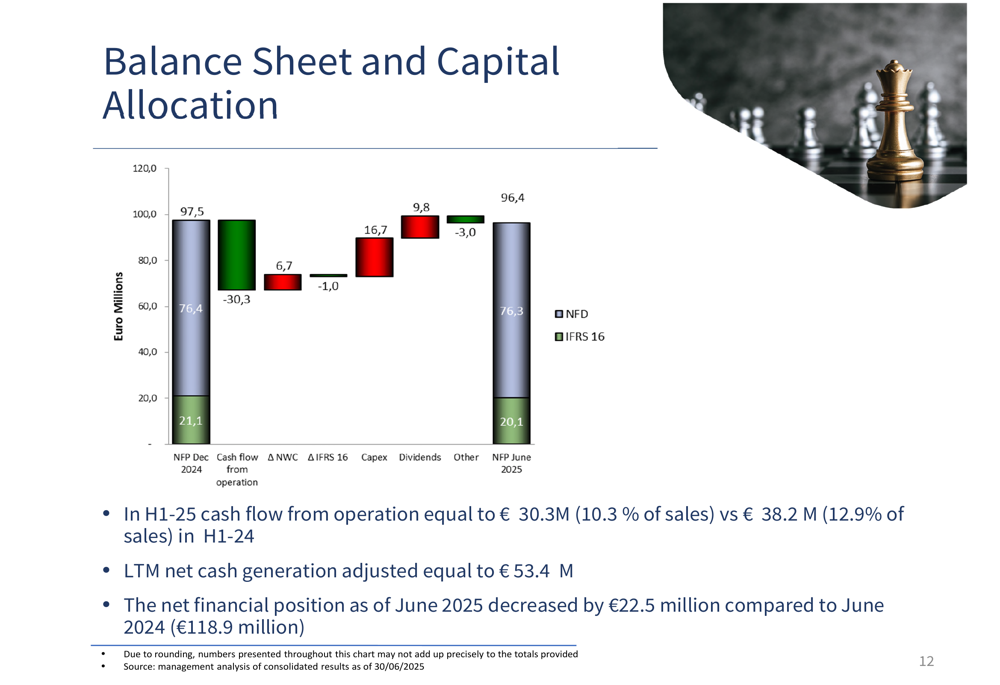

Capital allocation remained focused on growth investments, debt reduction, and shareholder returns. The company paid €9.8 million in dividends during the period while continuing to invest in its accelerated capital expenditure program.

The balance sheet and capital allocation strategy is summarized in the following slide:

Forward-Looking Statements

Looking ahead, LU-VE Group outlined several strategic priorities and market opportunities. The company expects continued growth in commercial refrigeration and noted that heat pump market recovery was better than expected. Nuclear applications are in progress, with sales impact expected to begin in H2 2025.

Strategic focus areas include datacenter and industrial projects, automation, process optimization, and cost reduction. The company also highlighted its continuous search for M&A opportunities with strong strategic rationale.

On the financial front, LU-VE Group emphasized its focus on cost efficiency, margin expansion, deleveraging, and net cash generation. The company’s strong order book and project pipeline suggest that year-end sales targets remain achievable despite some project delays, particularly in air conditioning and industrial cooling segments.

With its diversified customer base (largest customer representing only 3.9% of sales), improving financial metrics, and strategic focus on growth markets, LU-VE Group appears well-positioned to capitalize on medium to long-term secular growth trends in its core markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.