TSX runs higher on rate cut expectations

Introduction & Market Context

LXP Industrial Trust (NYSE:LXP) released its second quarter 2025 investor presentation, highlighting continued operational momentum with same-store NOI growth of 4.7% and strategic positioning in high-growth markets. The industrial REIT, which closed at $8.07 on July 29, 2025, with a 1.77% gain, continues to focus on capturing opportunities from manufacturing reshoring trends while maintaining a strong balance sheet.

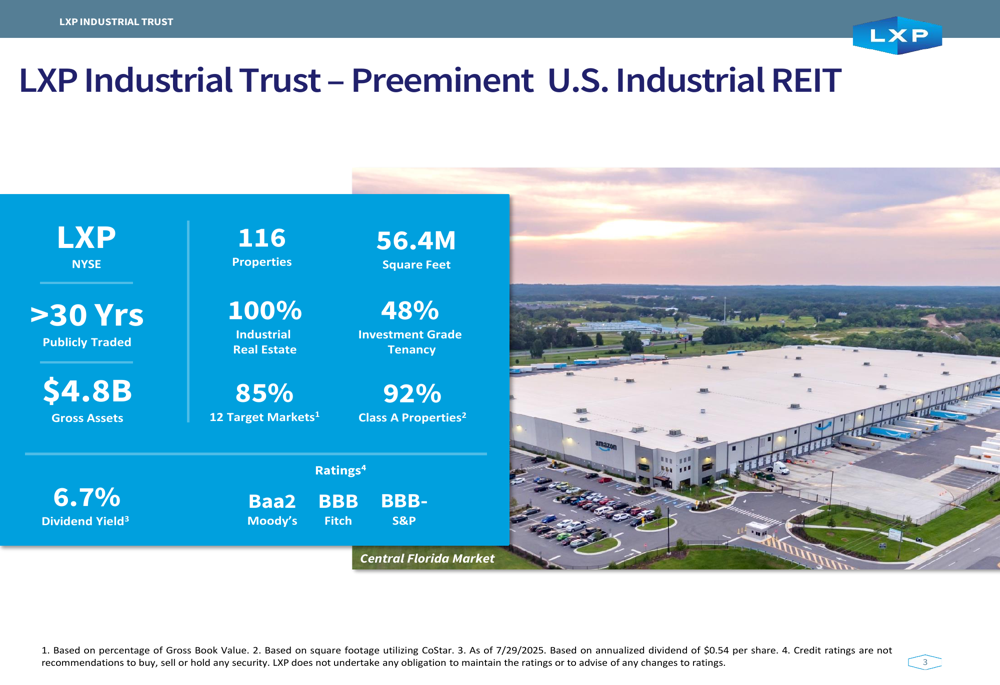

The company has established itself as a pure-play industrial REIT with 116 properties spanning 56.4 million square feet, concentrated primarily in the Sunbelt and lower Midwest regions. With investment-grade credit ratings from all three major agencies (Baa2 Moody’s, BBB Fitch, BBB- S&P), LXP maintains a portfolio that is 94.1% leased with a weighted average lease term of 5.1 years.

As shown in the following overview of LXP’s key metrics:

Quarterly Performance Highlights

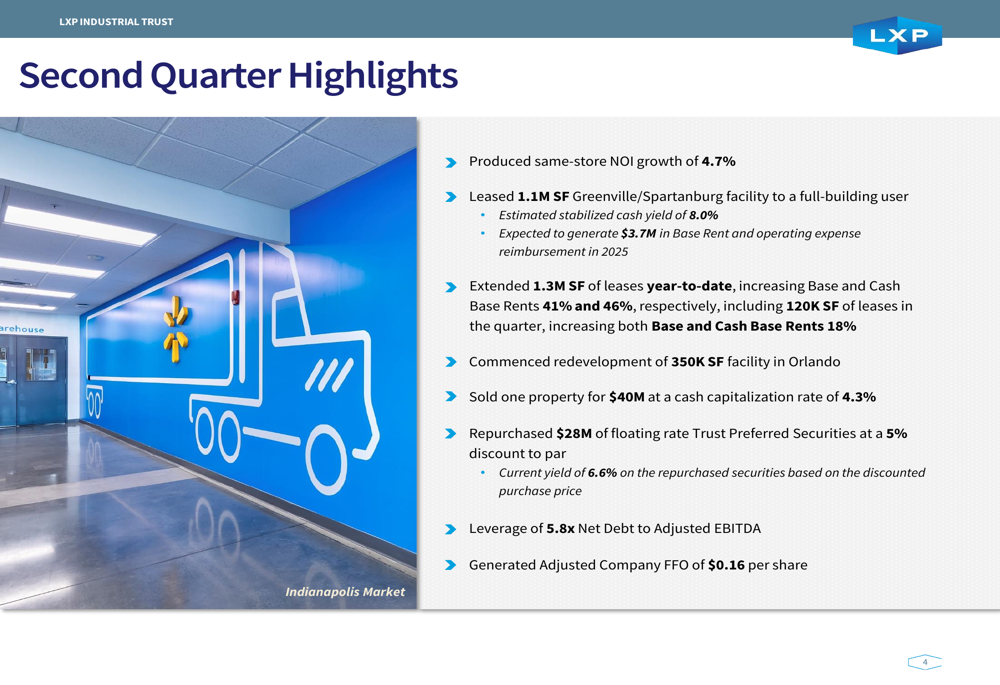

LXP delivered solid results in the second quarter, with same-store NOI growth of 4.7%, continuing the positive trend following 5.2% growth in Q1 2025. The company successfully leased a 1.1 million square foot facility in Greenville/Spartanburg with an estimated stabilized cash yield of 8.0%, expected to generate $3.7 million in base rent and operating expense reimbursement in 2025.

Leasing activity remained robust, with 1.3 million square feet of leases extended year-to-date, increasing base and cash base rents by 41% and 46% respectively. During the quarter, the company extended 120,000 square feet of leases with 18% increases in both base and cash base rents, demonstrating strong pricing power in its markets.

The company also made progress on its capital recycling strategy, selling one property for $40 million at a cash capitalization rate of 4.3% and repurchasing $28 million of Trust Preferred Securities at a 5% discount to par, yielding 6.6%. LXP reported Adjusted Company FFO of $0.16 per share for the quarter, with leverage at 5.8x Net Debt to Adjusted EBITDA.

The following slide details these quarterly achievements:

Strategic Initiatives

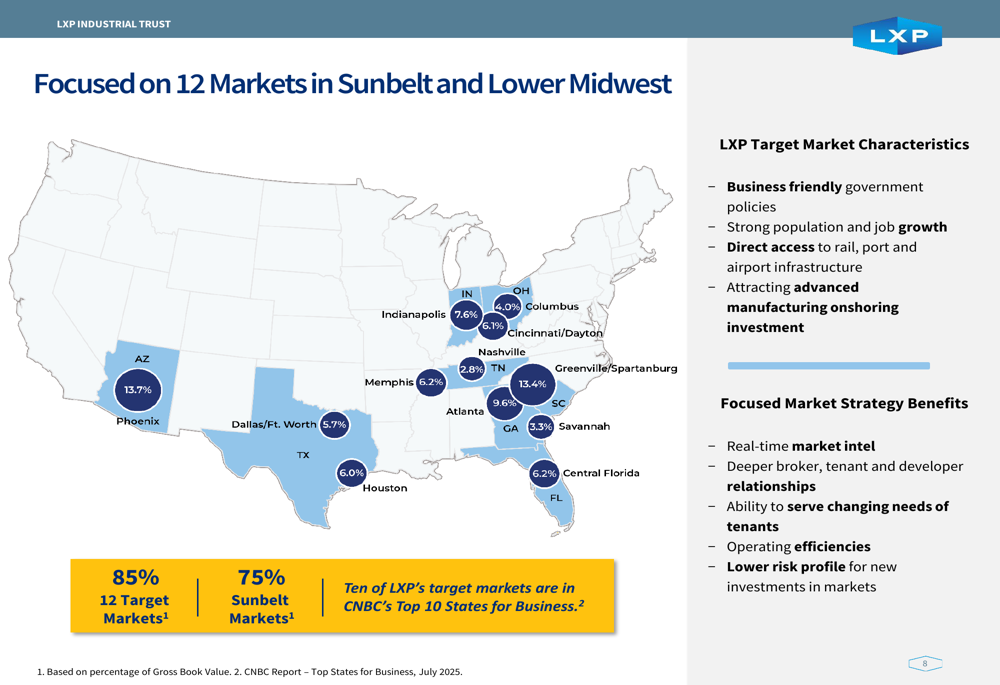

LXP’s strategic focus centers on 12 target markets in the Sunbelt and lower Midwest, regions experiencing population and job growth at 2.3x and 1.7x the national average, respectively. The company has positioned 85% of its portfolio in these markets, which are attracting significant manufacturing investment due to business-friendly policies, strong demographic trends, and robust infrastructure.

The presentation highlights $150 billion of planned advanced manufacturing investment announced in LXP’s target markets, positioning the company to benefit from the ongoing reshoring trend. This aligns with comments from CEO Will Eglin in the Q1 earnings call, who noted that while "the direction of tenant demand is uncertain in the near term," the company’s "portfolio footprint that aligns with onshoring initiatives positions us well."

The following map illustrates LXP’s strategic market concentration:

The company’s tenant base reflects high credit quality across diverse industries, with 47.8% of tenants holding investment grade ratings. Top tenants include Amazon (NASDAQ:AMZN) (6.7% of annualized base rent), Nissan (OTC:NSANY) (4.8%), and Black and Decker (3.4%). This diversification helps mitigate sector-specific risks while maintaining strong credit quality.

As shown in the following breakdown of LXP’s tenant composition:

Detailed Financial Analysis

LXP’s portfolio consists of 92% Class A properties with an average building age of just 9.3 years, positioning it well in the competitive industrial market. The company’s average rent per square foot stands at $5.14, with annualized NOI of $274 million as of Q2 2025.

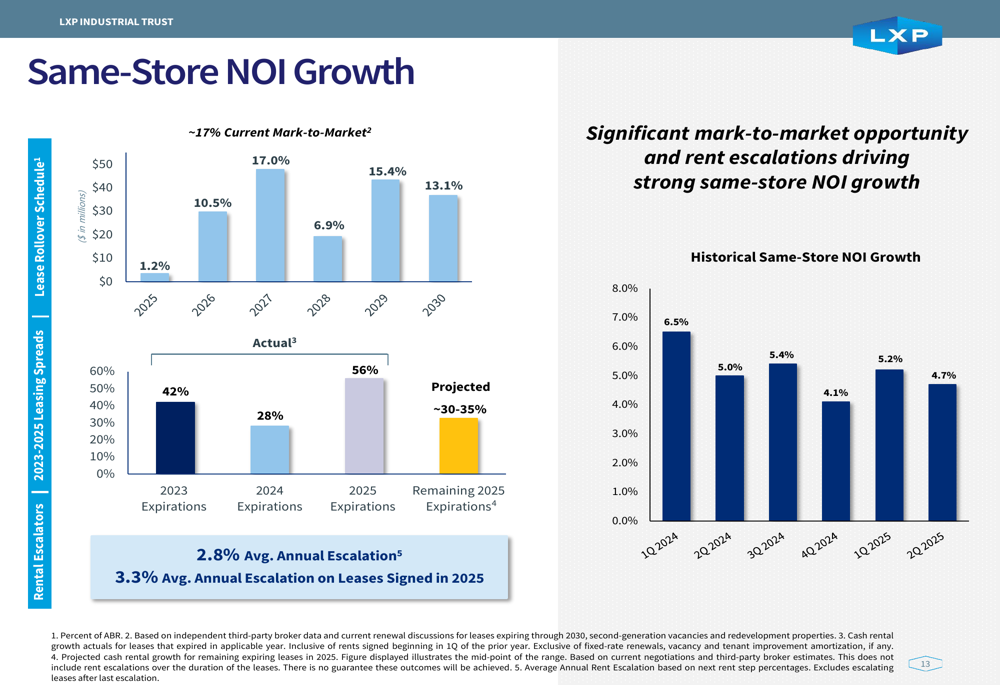

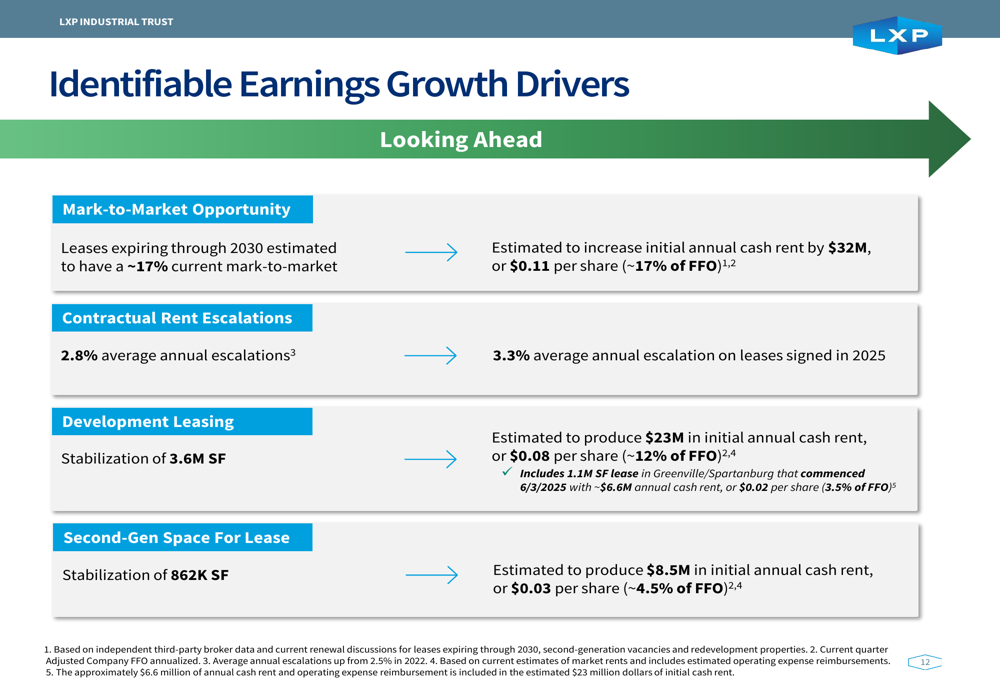

A significant mark-to-market opportunity of approximately 17% exists within the portfolio, providing a clear path to internal growth as leases expire and renew at market rates. This is complemented by average annual rental escalations of 2.8% across the portfolio, with leases signed in 2025 featuring even stronger 3.3% average annual escalations.

The following slide illustrates LXP’s same-store NOI growth trajectory:

The company’s development program has completed 9.1 million square feet of core and shell construction, with 74% of the program now leased. A notable achievement was the 1.1 million square foot lease at the Greenville/Spartanburg facility to a U.S. subsidiary of a global logistics company, which commenced on June 3, 2025, with initial rent of $5.50 per square foot and 3.25% annual rental escalations.

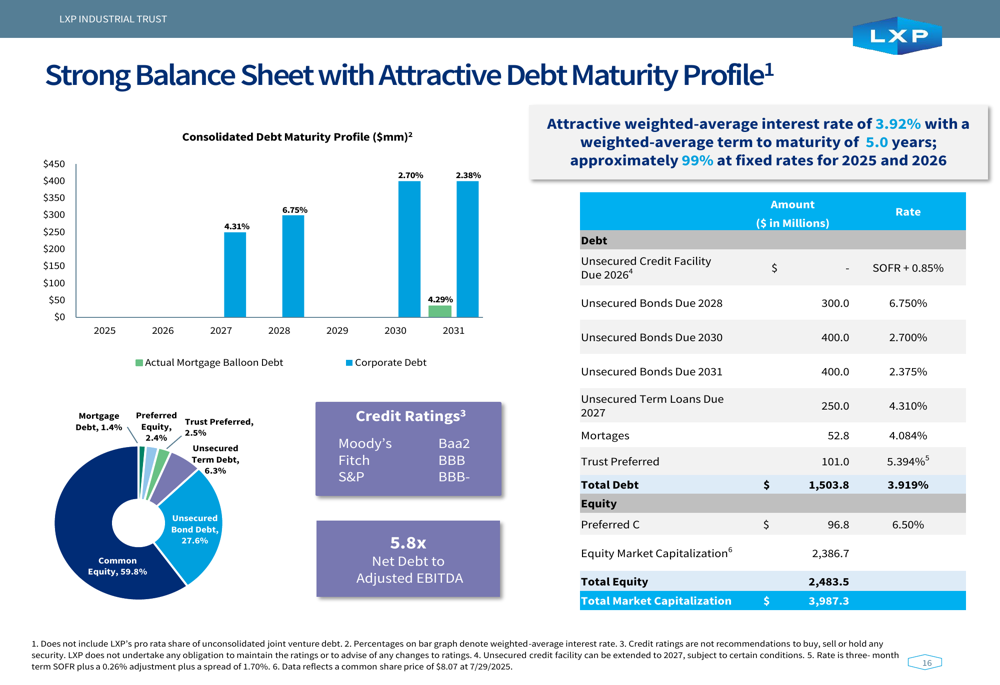

LXP maintains a strong balance sheet with an attractive debt maturity profile. The weighted-average interest rate on debt is 3.92% with a weighted-average term to maturity of 5.0 years. Approximately 99% of debt is at fixed rates for 2025 and 2026, providing stability in the current interest rate environment.

The following slide details LXP’s debt profile:

Forward-Looking Statements

LXP identified several earnings growth drivers that require limited incremental capital investment. These include the mark-to-market opportunity estimated to increase initial annual cash rent by $32 million ($0.11 per share), contractual rent escalations averaging 3.3% on leases signed in 2025, development leasing projected to produce $23 million in initial annual cash rent ($0.08 per share), and second-generation space for lease estimated to generate $8.5 million in initial annual cash rent ($0.03 per share).

The company’s lease expiration schedule shows limited near-term expirations (1.2% in 2025), with more significant rollovers in 2026 (10.5%) and 2027 (17.0%). This provides stability in the near term while offering opportunities to capture market rent growth in subsequent years.

As illustrated in the following growth drivers slide:

While LXP’s presentation maintains an optimistic outlook on reshoring opportunities, the Q1 earnings call noted some caution regarding "trade policy uncertainty" that "may affect tenant decision-making and demand." The company is navigating these uncertainties by maintaining high occupancy, focusing on tenant credit quality, and strategically positioning its portfolio in markets benefiting from manufacturing investment.

LXP’s 6.7% dividend yield (reported as 6.84% in recent earnings coverage) continues to attract income-focused investors, supported by the company’s stable cash flows and growth prospects. With a clear strategy focused on high-growth markets, modern facilities, and strong tenant relationships, LXP appears well-positioned to navigate the evolving industrial real estate landscape while delivering value to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.