Gold prices hold sharp gains as soft US jobs data fuels Fed rate cut bets

Introduction & Market Context

Magna International Inc (TSX:MG) presented its second quarter 2025 results on August 1, highlighting improved profitability metrics despite a slight decline in sales. The automotive parts supplier saw its stock close at $56.82 on July 31, up 0.64% ahead of the earnings release, with shares trading well above their 52-week low of $43.25 but still below their high of $66.42.

The company’s performance shows a significant improvement from its first quarter results, when Magna missed EPS expectations but exceeded revenue forecasts. The Q2 presentation demonstrates the company’s continued focus on operational excellence and cost discipline while navigating industry challenges including tariffs and production fluctuations.

Quarterly Performance Highlights

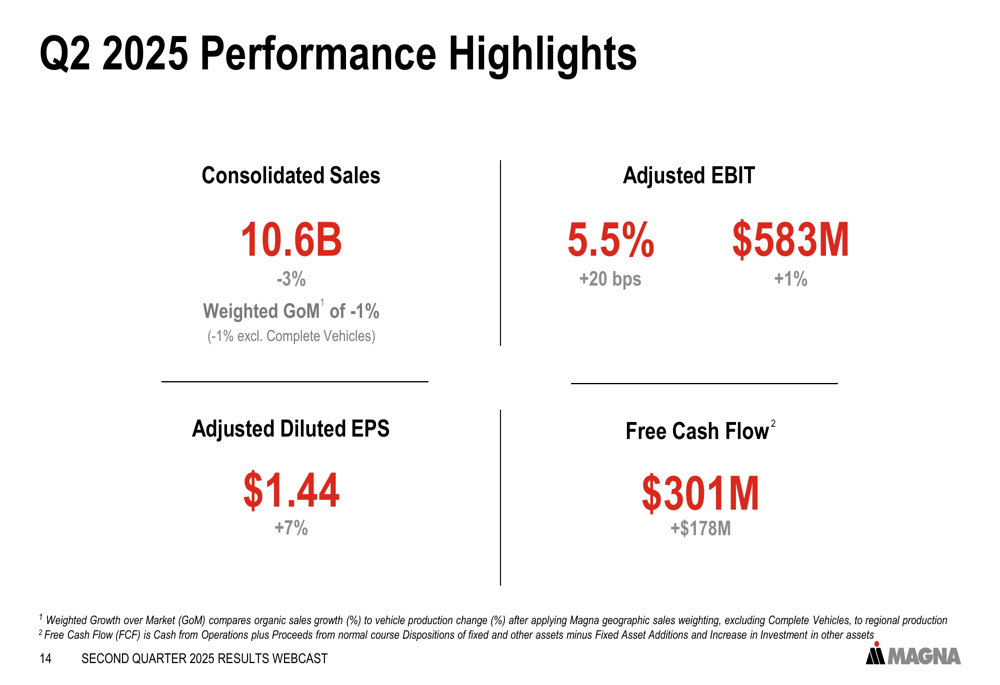

Magna reported consolidated sales of $10.6 billion for Q2 2025, down 3% year-over-year, but delivered stronger profitability metrics across the board. The company achieved adjusted EBIT of $583 million (up 1%), with margins expanding by 20 basis points to 5.5%. Adjusted diluted EPS rose 7% to $1.44, while free cash flow saw a substantial increase of $178 million to reach $301 million.

As shown in the following performance highlights:

The company’s weighted sales growth over market (GoM) was -1%, indicating that Magna’s sales performance was relatively in line with the overall market trends. This metric excludes complete vehicles and accounts for Magna’s geographic sales weighting.

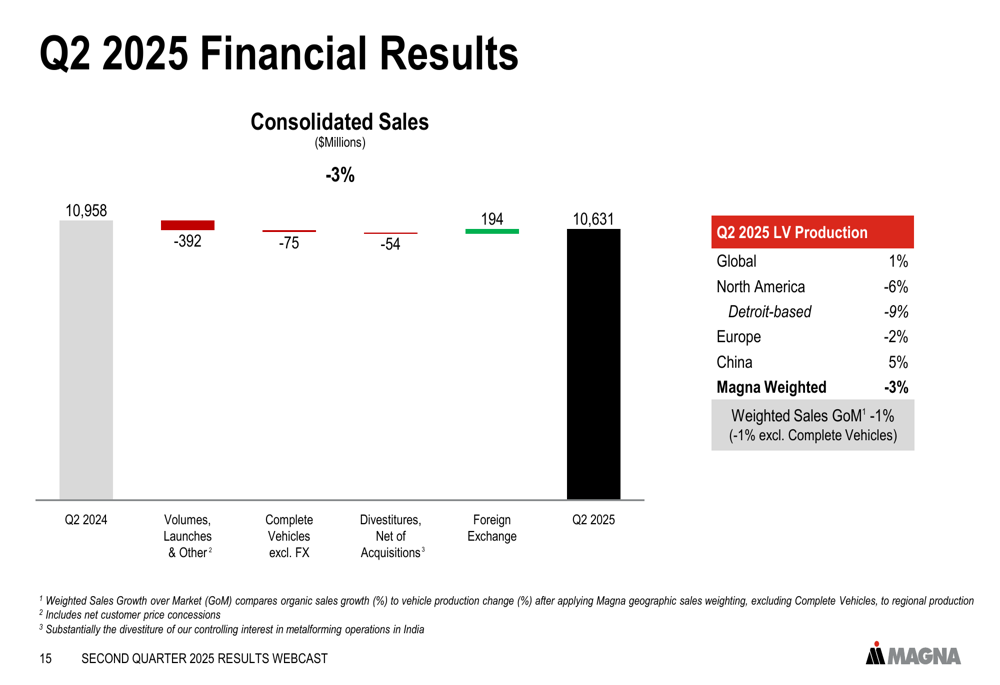

A detailed breakdown of the consolidated sales bridge reveals the key factors behind the 3% year-over-year decline:

While volumes, launches, and other factors reduced sales by $392 million, and complete vehicles excluding FX contributed a $75 million decrease, these were partially offset by a positive $194 million foreign exchange impact. The slide also highlights the regional production trends, with North America down 6%, Europe down 2%, and China up 5%.

Margin Improvement and Cost Management

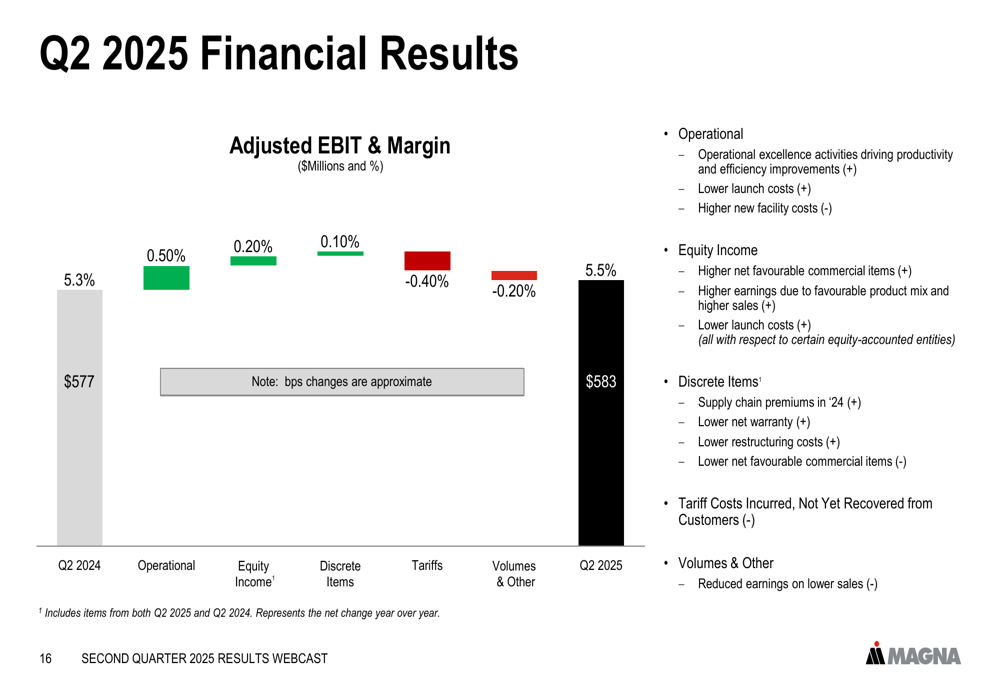

Despite the sales decline, Magna successfully expanded its adjusted EBIT margin by 20 basis points to 5.5%. This improvement was primarily driven by operational excellence initiatives, which contributed a 0.5% increase to the margin.

The following bridge analysis illustrates the factors affecting the margin performance:

Notably, operational excellence added 0.5% to the margin, while equity income and discrete items contributed 0.2% and 0.1% respectively. These gains were partially offset by a 0.4% negative impact from tariffs and a 0.2% decrease from volumes and other factors.

The company’s focus on cost management and operational efficiency has been a consistent theme since Q1, when CEO Swamy Kotagiri emphasized "cost and capital discipline" as key priorities. This disciplined approach appears to be yielding results, as evidenced by the margin expansion despite lower sales volumes.

Updated 2025 Outlook

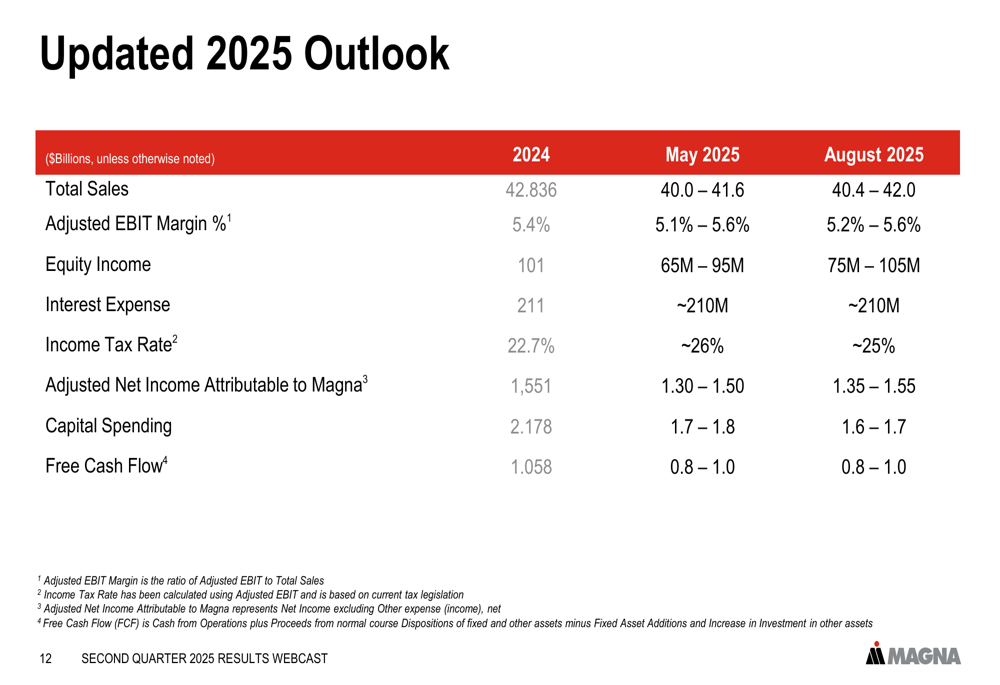

Based on its strong Q2 performance, Magna has raised its full-year 2025 outlook. The company now expects total sales of $40.4-42.0 billion, up from its previous forecast of $40.0-41.6 billion in May. Additionally, Magna increased the low end of its adjusted EBIT margin range to 5.2% (from 5.1%), maintaining the high end at 5.6%.

The updated outlook reflects both improved operational performance and changes to key assumptions:

The revised guidance also includes adjusted net income attributable to Magna of $1.35-1.55 billion and free cash flow of $0.8-1.0 billion. Capital spending is projected at $1.6-1.7 billion, slightly lower than the $1.7-1.8 billion mentioned in the Q1 earnings call, suggesting increased capital efficiency.

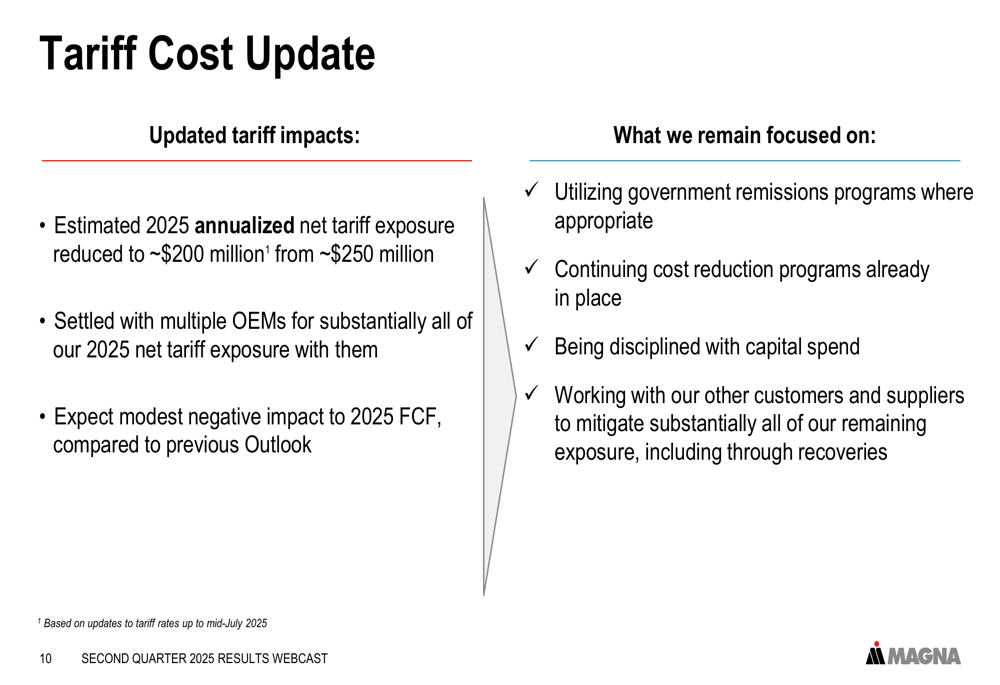

Tariff Mitigation Progress

A significant focus of Magna’s presentation was its progress in mitigating tariff impacts. The company has reduced its estimated 2025 annualized net tariff exposure to approximately $200 million, down from $250 million reported in Q1. Furthermore, Magna has settled with multiple OEMs for substantially all of its 2025 net tariff exposure.

The following slide details the company’s tariff mitigation efforts:

Management indicated that they expect only a modest negative impact to 2025 free cash flow compared to their previous outlook. The company continues to focus on utilizing government remissions programs, implementing cost reduction initiatives, maintaining disciplined capital spending, and working with customers and suppliers to address the remaining exposure.

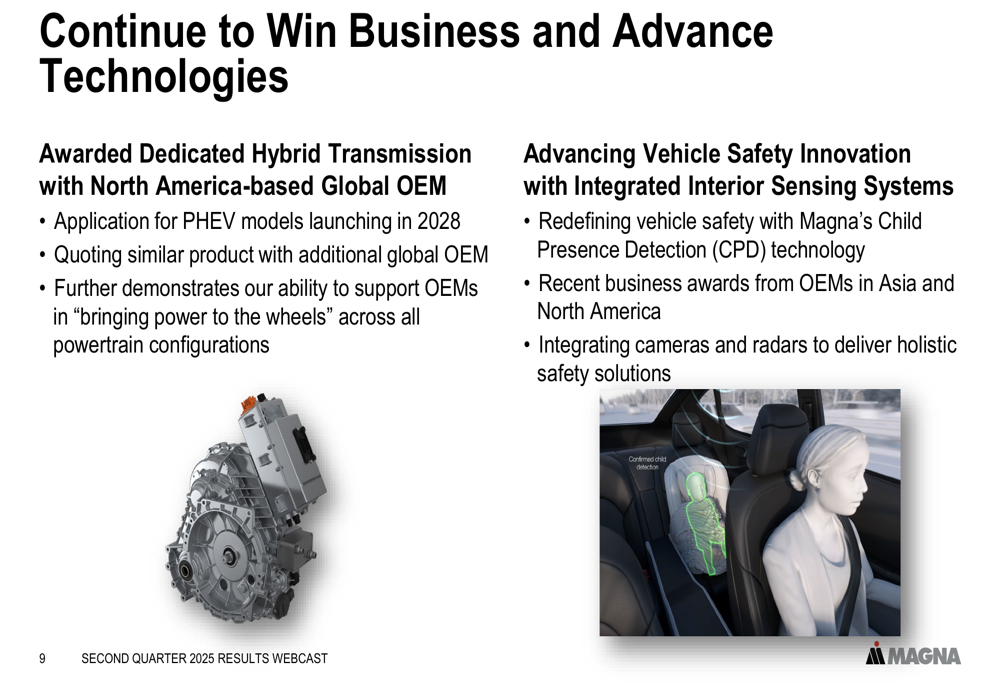

Strategic Wins and Innovation

Magna highlighted several recent business wins and technological advancements that position the company for future growth. These include a dedicated hybrid transmission contract with a North America-based global OEM for PHEV models launching in 2028, and advancements in vehicle safety innovation with integrated interior sensing systems.

The company’s innovation efforts are illustrated in the following slide:

Magna also received recognition for its quality and innovation, winning the J.D. Power Platinum Plant Quality Award for its Complete Vehicle Assembly Operation in Graz, Austria, and the Volkswagen (ETR:VOWG_p) Group Award 2025 in the Product category for its innovative battery cover on the VW MEB platform.

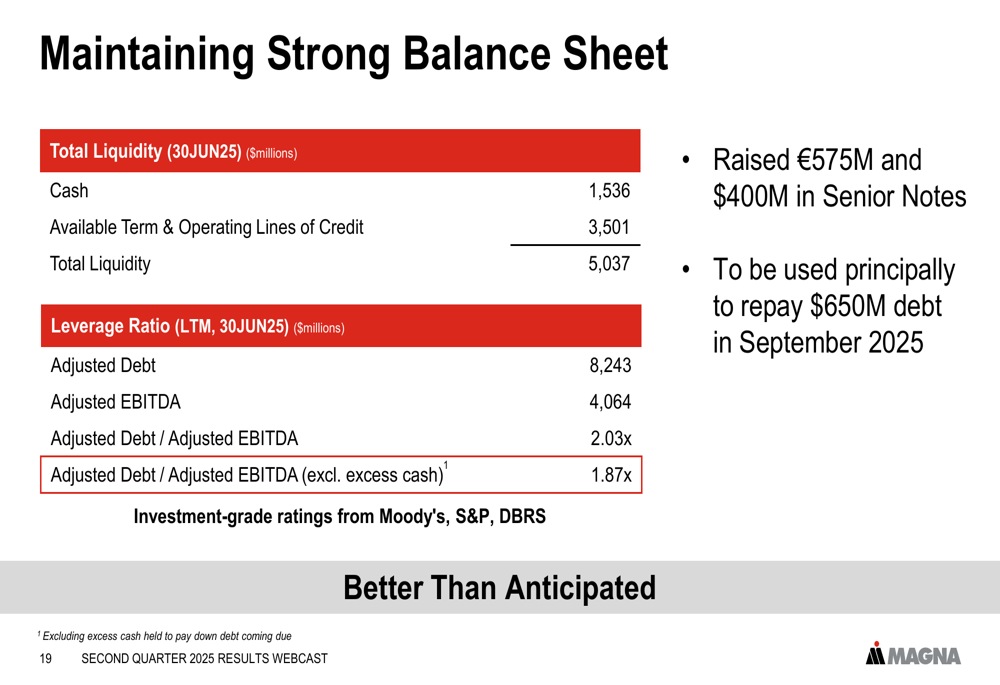

Balance Sheet and Shareholder Returns

The company maintained a strong financial position with total liquidity of $5.037 billion as of June 30, 2025, consisting of $1.536 billion in cash and $3.501 billion in available lines of credit. Magna’s leverage ratios remain healthy, with an adjusted debt to adjusted EBITDA ratio of 2.03x (1.87x excluding excess cash).

The following slide details the company’s balance sheet strength:

In terms of shareholder returns, Magna distributed $137 million in dividends during Q2 2025, bringing the year-to-date return of capital to $324 million. Unlike the previous quarter, when the company had paused share buybacks due to market uncertainty, the Q2 presentation focused primarily on dividend payments as the main vehicle for returning capital to shareholders.

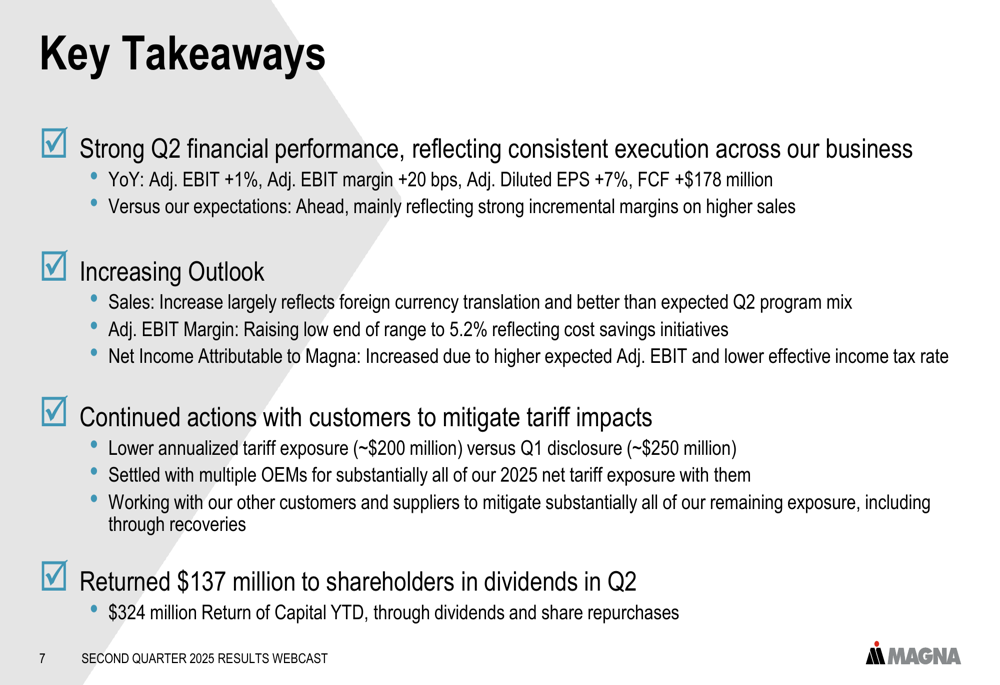

Forward-Looking Statements

Looking ahead, Magna’s management expressed confidence in the company’s ability to continue improving margins through operational excellence initiatives while effectively managing tariff-related challenges. The updated outlook reflects this optimism, particularly with the raised lower end of the adjusted EBIT margin range.

The company’s summary slide captures the key takeaways from the presentation:

With a consistent focus on operational execution, cost management, and strategic innovation, Magna appears well-positioned to navigate the evolving automotive landscape while delivering improved financial performance through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.