Piper Sandler lowers Arbor Realty Trust stock price target on credit issues

Introduction & Market Context

Malibu Boats Inc. (NASDAQ:MBUU) presented its first quarter fiscal 2026 earnings results on October 30, 2025, revealing solid performance despite ongoing challenges in the recreational boating market. The premium boat manufacturer reported significant year-over-year revenue growth while continuing to focus on dealer inventory health and strategic initiatives.

The company’s stock price reacted positively to the earnings beat, with pre-market trading showing a 1.32% increase to $32.57. However, the stock has since fallen 5.45% during the regular trading session, reflecting broader market concerns about the recreational boating industry’s outlook.

As shown in the following slide highlighting key takeaways, Malibu emphasized its ability to generate growth despite retail softness:

Quarterly Performance Highlights

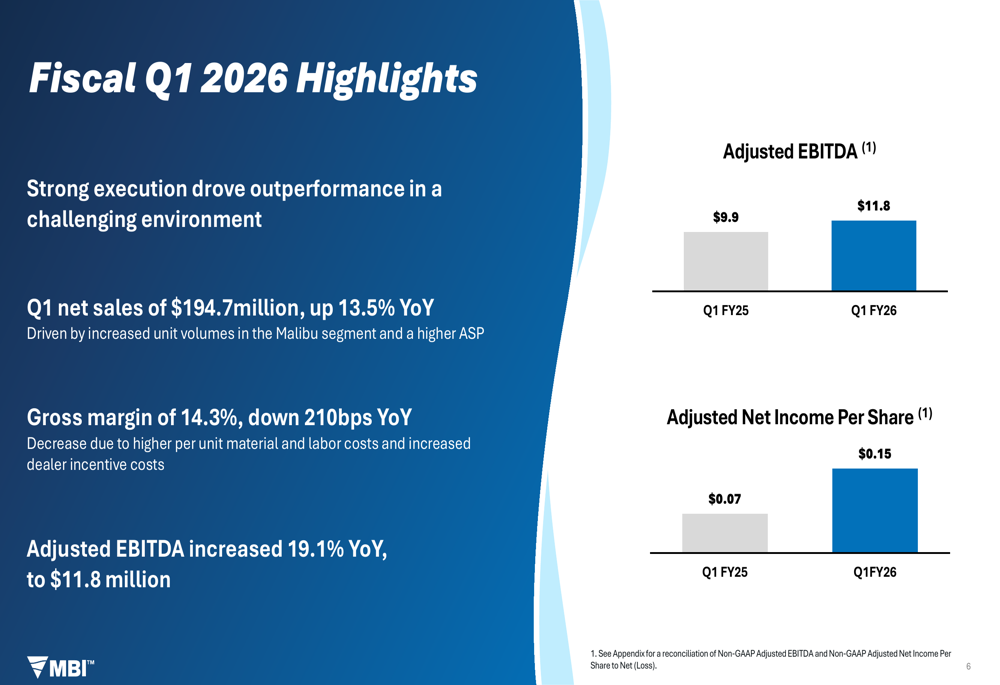

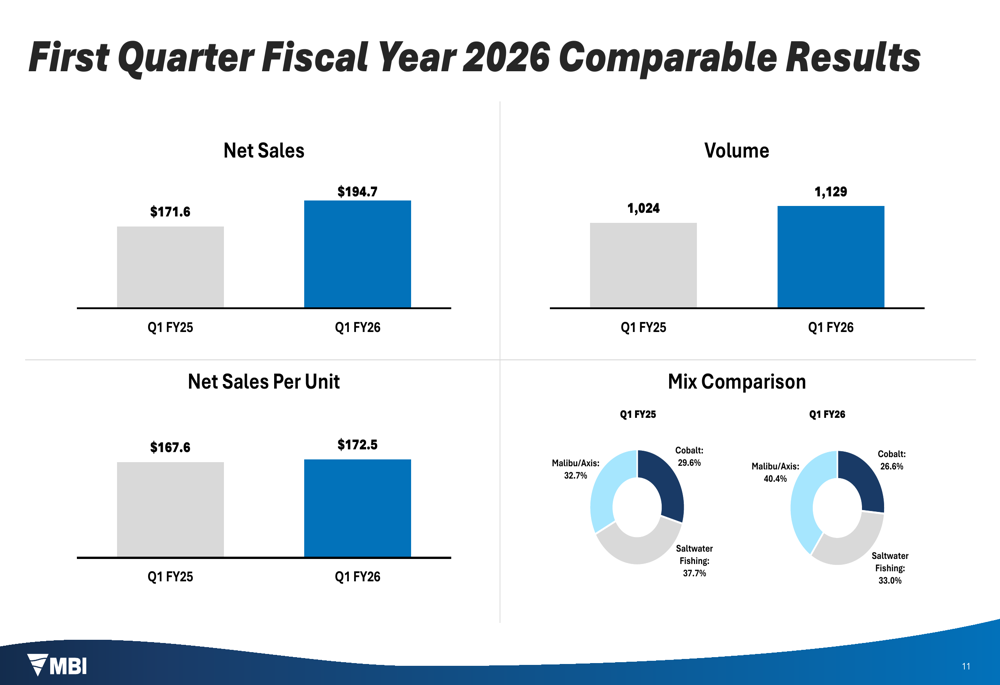

Malibu Boats reported net sales of $194.7 million for Q1 FY2026, representing a 13.5% increase compared to $171.6 million in the same period last year. This growth was primarily driven by higher unit volumes in the Malibu segment and increased average selling prices (ASP).

Unit volumes rose to 1,129, up 10.3% from 1,024 units in Q1 FY2025, while net sales per unit increased from $167.6 to $172.5. These metrics demonstrate the company’s ability to maintain pricing power despite challenging market conditions.

The following slide details the company’s first quarter financial performance, showing significant improvements in Adjusted EBITDA and Adjusted Net Income Per Share:

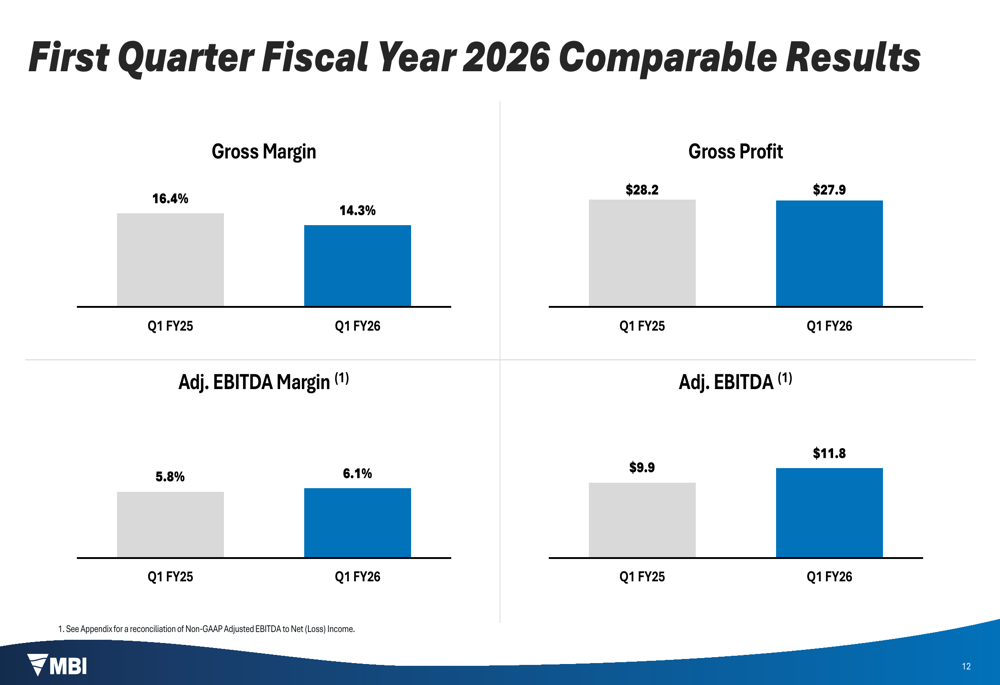

Despite the revenue growth, Malibu’s gross margin declined by 210 basis points year-over-year to 14.3%, compared to 16.4% in Q1 FY2025. This decrease was attributed to higher per-unit material and labor costs, as well as increased dealer incentive expenses as the company worked to support its dealer network.

However, Adjusted EBITDA increased by 19.1% to $11.8 million, with Adjusted EBITDA margin improving slightly to 6.1% from 5.8% in the prior year. Adjusted net income per share doubled to $0.15 from $0.07 in Q1 FY2025.

The company’s detailed quarterly results for sales, volume, and profitability metrics are shown in these comparative slides:

Malibu also reported positive free cash flow of $2.5 million for the quarter, a significant improvement from the negative $16.8 million reported in Q1 FY2025. This cash generation demonstrates the resilience of the company’s business model even in challenging market conditions.

Strategic Initiatives

Malibu Boats is pursuing several strategic initiatives to drive long-term growth. The company introduced multiple new boat models for model year 2026, including the Malibu 22LSV, Axis T250, Pursuit S388, and several others across its brand portfolio.

The following slide showcases the company’s new product introductions:

Beyond product development, Malibu outlined its strategy to accelerate profitable growth through three key avenues: new market growth, share growth, and strategic M&A. The company is exploring geographic expansion, whitespace opportunities, and adjacent markets while continuing to innovate its product lineup.

Malibu is also building new capabilities to diversify revenue streams and enhance customer financing options. The company highlighted two specific initiatives: Marine Components, a vertically integrated supplier of premium marine components, and MBI Acceptance, an in-house financing partnership designed to drive sales conversion.

As illustrated in this slide, these initiatives aim to expand revenue beyond boat sales and provide competitive financing options for customers:

Forward-Looking Statements

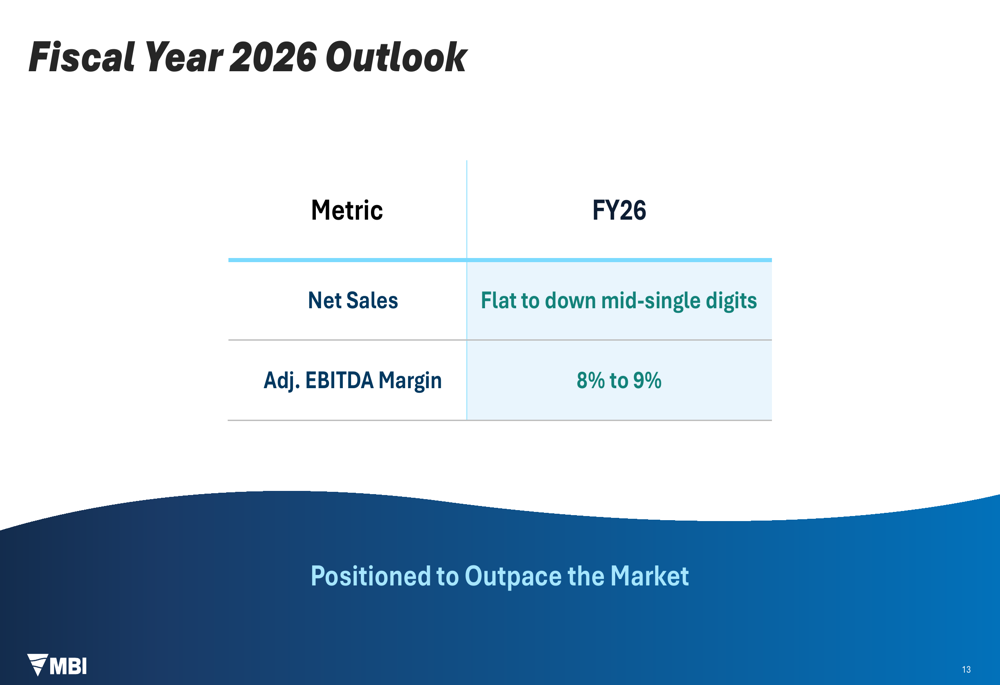

Despite the strong first quarter performance, Malibu Boats maintained a cautious outlook for fiscal year 2026. The company expects net sales to be flat to down mid-single digits compared to FY2025, with Adjusted EBITDA margin projected between 8% and 9%.

This guidance reflects management’s assessment of ongoing market challenges, including retail softness and dealer inventory adjustments. However, the company remains confident in its ability to outperform the broader market.

Malibu also presented an illustrative market environment framework comparing a mid-cycle baseline scenario with a potential outperformance scenario. In the outperformance framework, the company projects it could achieve approximately $1.5 billion in net sales with a 20% Adjusted EBITDA margin at 75% capacity utilization, compared to $1.3 billion and 17.5% margin in the baseline scenario.

CEO Steve Menneto expressed confidence in the company’s positioning, stating, "We are maintaining our full year guidance and remain confident in our ability to outperform the market while continuing to build for the next up cycle." He also highlighted the positive reception of new products and retail tools by dealers.

As Malibu navigates through market challenges, the company’s focus on dealer health, product innovation, and strategic initiatives positions it to weather the current environment while building capabilities for future growth. Investors will be watching closely to see if the company can continue to outpace the market as projected while maintaining profitability in a challenging recreational boating landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.