Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

Introduction & Market Context

MasTec Inc . (NYSE:MTZ) released its second quarter 2025 earnings presentation on August 1, 2025, revealing strong financial performance that exceeded guidance expectations. Despite reporting 20% year-over-year revenue growth and raising full-year guidance, the infrastructure construction company’s stock tumbled 13.78% in premarket trading, closing at $162.74, down from the previous close of $189.21.

The company’s presentation highlighted record revenue and backlog figures, but investors appeared concerned about cash flow generation and segment-specific challenges, particularly in the Power Delivery business. MasTec’s results come amid broader market volatility and increasing scrutiny of infrastructure companies’ ability to maintain growth trajectories.

Quarterly Performance Highlights

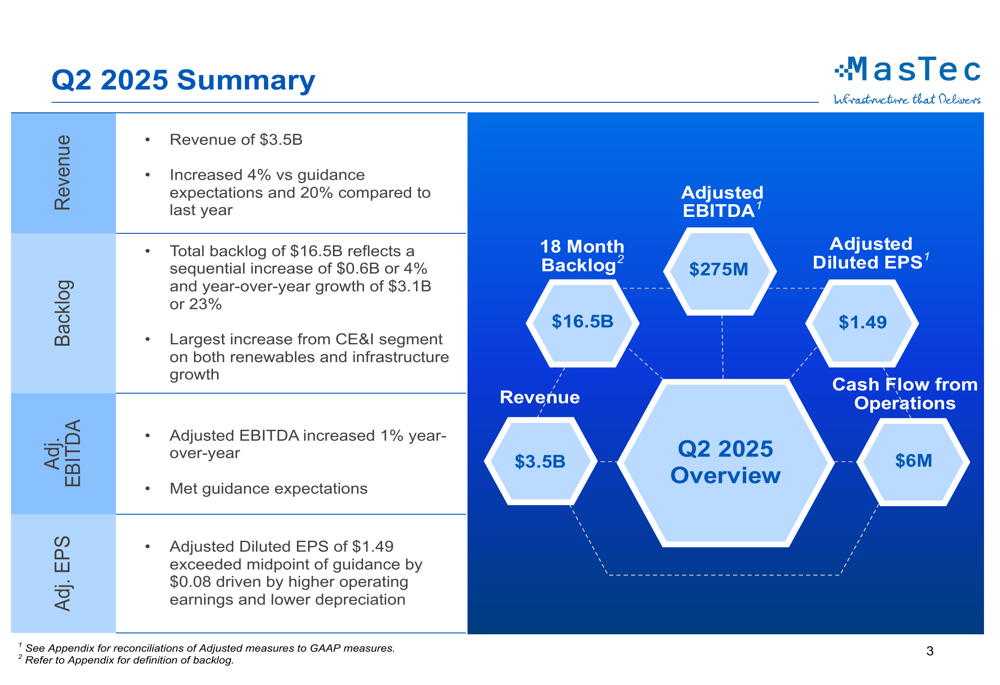

MasTec reported Q2 2025 revenue of $3.5 billion, representing a 20% increase compared to the same period last year and exceeding guidance expectations by 4%. Adjusted EBITDA reached $275 million, up 1% year-over-year and in line with guidance. The company delivered adjusted diluted earnings per share of $1.49, surpassing the midpoint of guidance by $0.08.

As shown in the following summary of key Q2 2025 metrics:

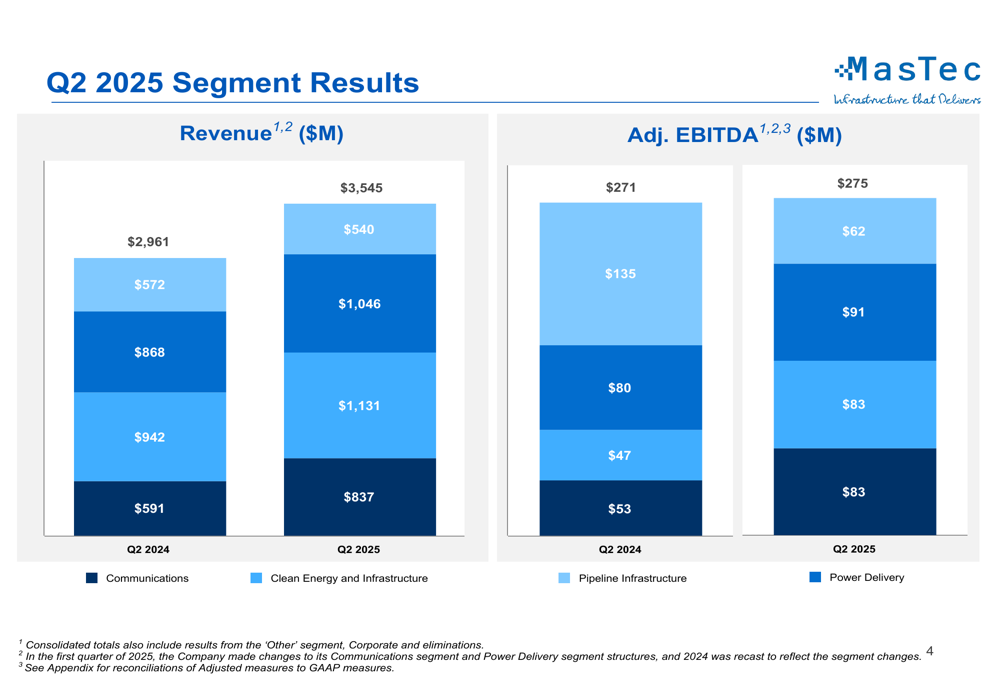

Segment performance varied significantly across the company’s business units. The Communications segment showed the strongest growth, with revenue increasing 42% year-over-year to $837 million. Clean Energy and Infrastructure revenue grew 20% to $1.13 billion, while Pipeline Infrastructure revenue rose 21% to $1.05 billion. However, Power Delivery revenue declined 6% to $540 million.

The segment-by-segment breakdown reveals significant profitability differences, with Communications and Clean Energy showing substantial EBITDA improvements while Power Delivery experienced a sharp decline:

Detailed Financial Analysis

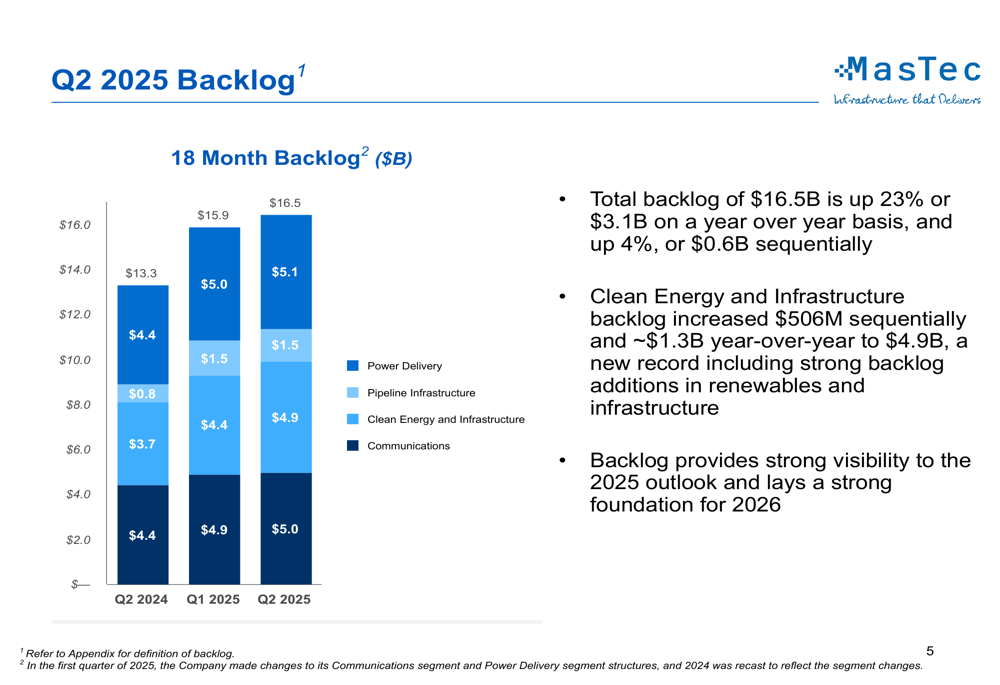

MasTec’s backlog, a key indicator of future revenue potential, reached $16.5 billion at the end of Q2 2025, representing a 23% year-over-year increase and a 4% sequential improvement from Q1. The Clean Energy and Infrastructure segment achieved a record backlog of $4.9 billion, up $506 million sequentially and approximately $1.3 billion year-over-year.

The following chart illustrates the company’s growing backlog across all segments:

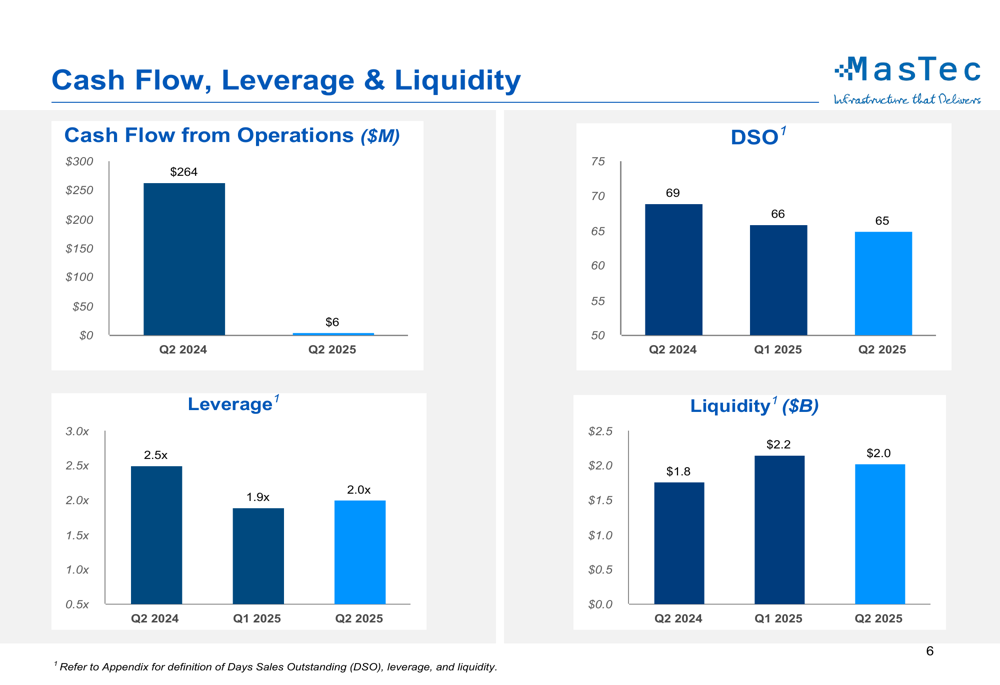

While revenue and backlog showed impressive growth, cash flow metrics presented a more challenging picture. Cash flow from operations dropped significantly to $6 million in Q2 2025 compared to $264 million in the same period last year. The company did make progress on working capital management, with Days Sales Outstanding (DSO) improving to 65 days from 69 days a year earlier.

The company’s leverage ratio stood at 2.0x at the end of Q2 2025, slightly up from 1.9x in Q1 but improved from 2.5x in Q2 2024. Liquidity remained strong at $2.0 billion, as shown in the following financial position summary:

Forward-Looking Statements

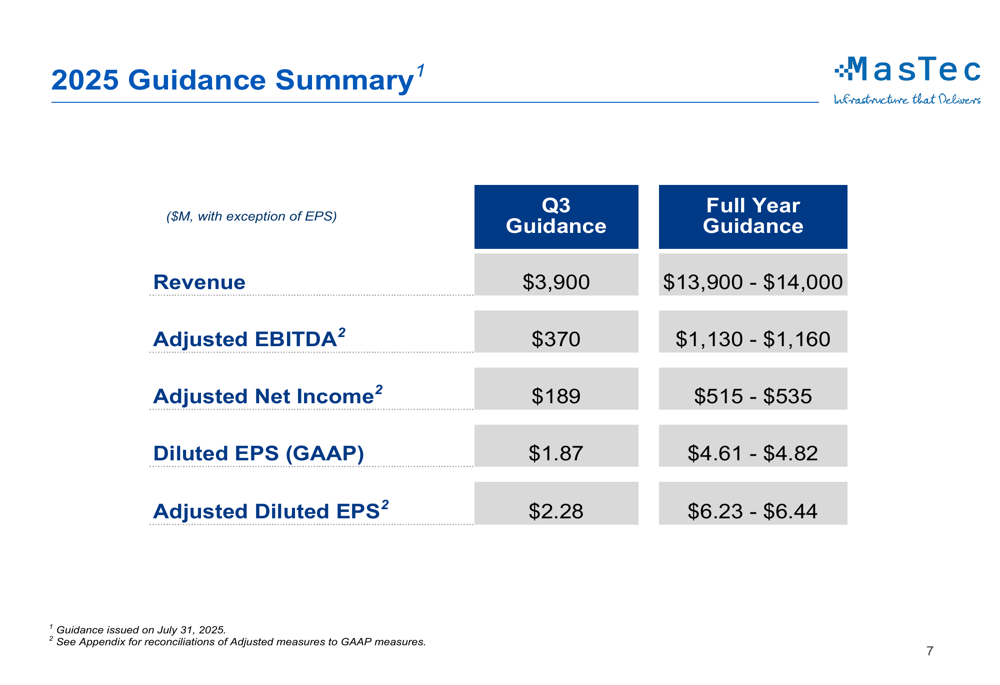

MasTec raised its full-year 2025 guidance, projecting revenue between $13.9 billion and $14.0 billion and adjusted EBITDA between $1.13 billion and $1.16 billion. For the third quarter of 2025, the company expects revenue of $3.9 billion and adjusted EBITDA of $370 million, with adjusted diluted EPS of $2.28.

The detailed guidance summary reveals management’s confidence in accelerating performance through the remainder of 2025:

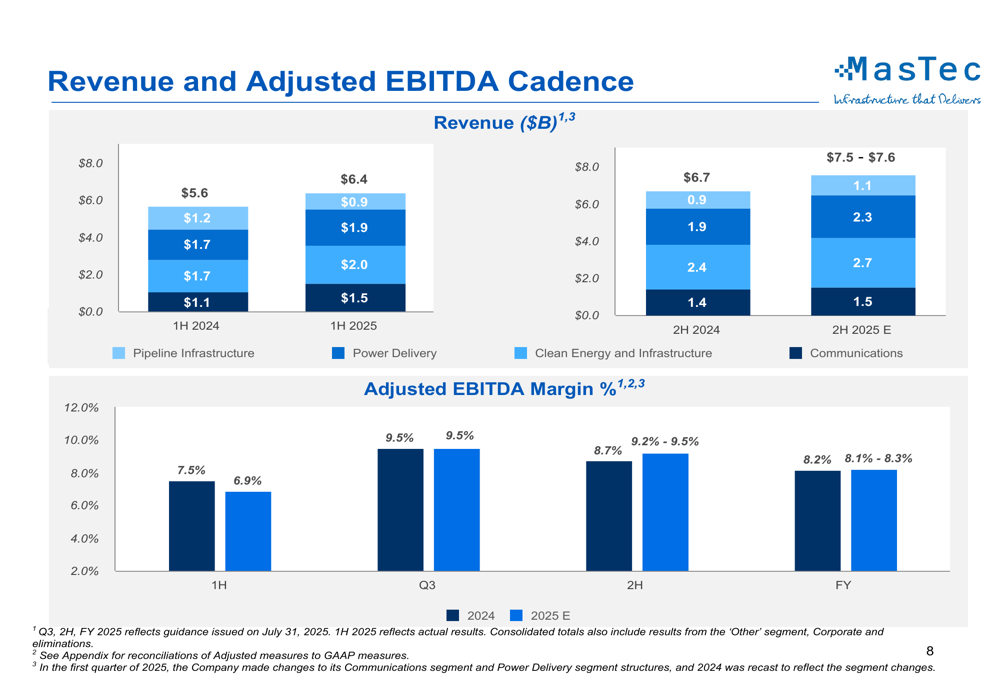

The company anticipates stronger second-half performance, particularly in the Clean Energy & Infrastructure and Power Delivery segments. Management projects improved adjusted EBITDA margins in the second half of 2025, reaching 9.2%-9.5% compared to 8.7% in the second half of 2024 and 6.9% in the first half of 2025.

The revenue and margin cadence expectations are illustrated in the following chart:

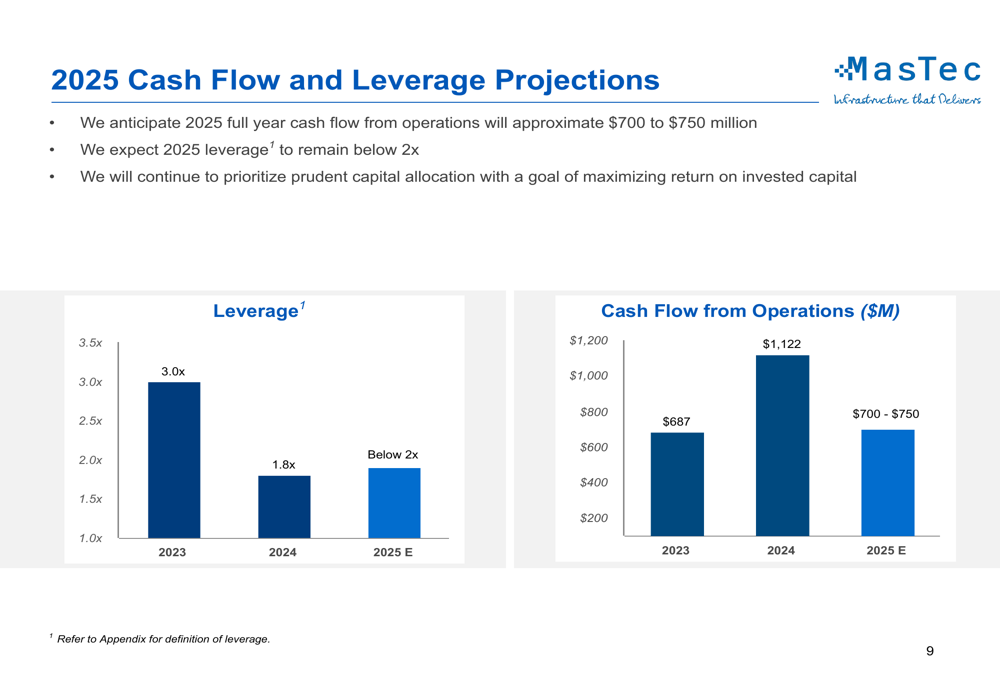

For full-year 2025, MasTec expects cash flow from operations to reach $700-$750 million, lower than the $1.12 billion generated in 2024 but in line with 2023 levels. The company projects leverage to remain below 2x throughout 2025, as shown in the following projections:

Market Reaction & Conclusion

Despite MasTec’s strong overall performance and raised guidance, investors responded negatively to the earnings presentation. The stock’s 13.78% decline in premarket trading suggests market concerns about several factors, including the significant year-over-year drop in cash flow from operations, the sharp decline in Power Delivery segment profitability, and potentially high valuation metrics.

According to available market data, MasTec’s stock had been trading near its 52-week high of $194 before the earnings release, with technical indicators suggesting overbought conditions. The company maintains a "GOOD" overall financial health score of 2.95 out of 5, with particularly strong momentum metrics.

Looking ahead, MasTec’s record backlog provides strong visibility for the remainder of 2025 and lays a foundation for continued growth in 2026. However, investors will likely focus on the company’s ability to convert its growing revenue into improved cash flow generation and address the profitability challenges in its Power Delivery segment. Management’s execution against its raised guidance will be crucial for restoring investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.