Fed Governor Adriana Kugler to resign

Introduction & Market Context

Matador Resources Company (NYSE:MTDR) released its first quarter 2025 earnings presentation on April 23, highlighting substantial production growth, strategic capital allocation, and operational efficiencies. The company’s stock closed at $40.84 on the day of the release, with premarket trading showing a 1.37% increase to $41.40.

The oil and gas producer has maintained its focus on the Delaware Basin, where it has expanded its acreage position significantly since its IPO in 2012. Matador’s presentation emphasized its strong financial position and operational performance in a challenging commodity price environment.

Quarterly Performance Highlights

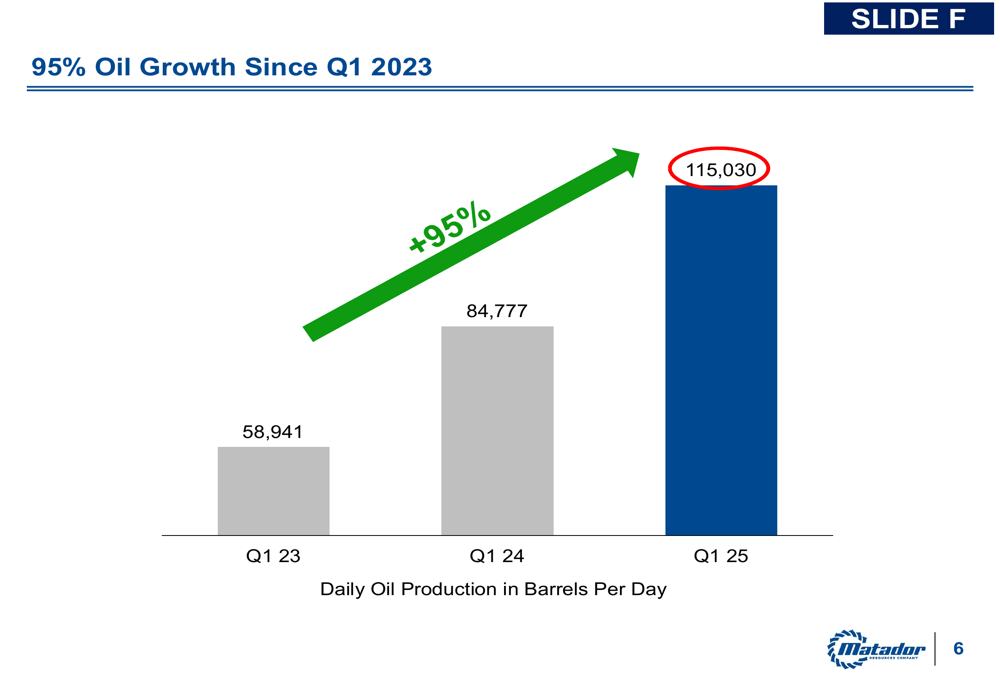

Matador reported impressive production growth, with Q1 2025 oil production reaching 115,030 barrels per day, representing a 95% increase compared to Q1 2023. Total (EPA:TTEF) production for the quarter was 198,631 BOE per day, exceeding the company’s guidance range of 195,000 to 197,000 BOE per day.

As shown in the following chart, Matador’s oil production has grown substantially over the past two years:

The company’s financial performance remained strong, with Q1 2025 Adjusted EBITDA of $644.2 million and adjusted free cash flow of $141.9 million. Matador’s leverage ratio stood at less than 1.0x as of March 31, 2025, reflecting the company’s commitment to maintaining a strong balance sheet.

Strategic Capital Allocation

Matador outlined several strategic capital allocation initiatives in its presentation. The company repaid $190 million in RBL debt during Q1 2025 and completed approximately $440 million in non-core asset sales, including the sale of its 19% ownership interest in Piñon Midstream for approximately $115 million.

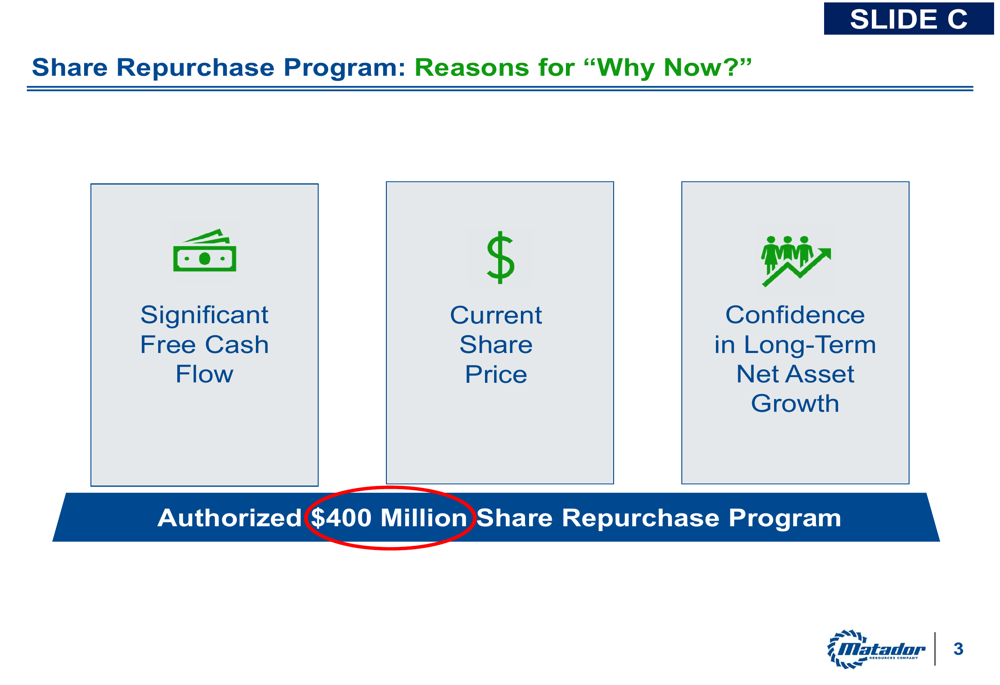

The company also authorized a $400 million share repurchase program, citing significant free cash flow, current share price, and confidence in long-term net asset growth as key factors in the decision:

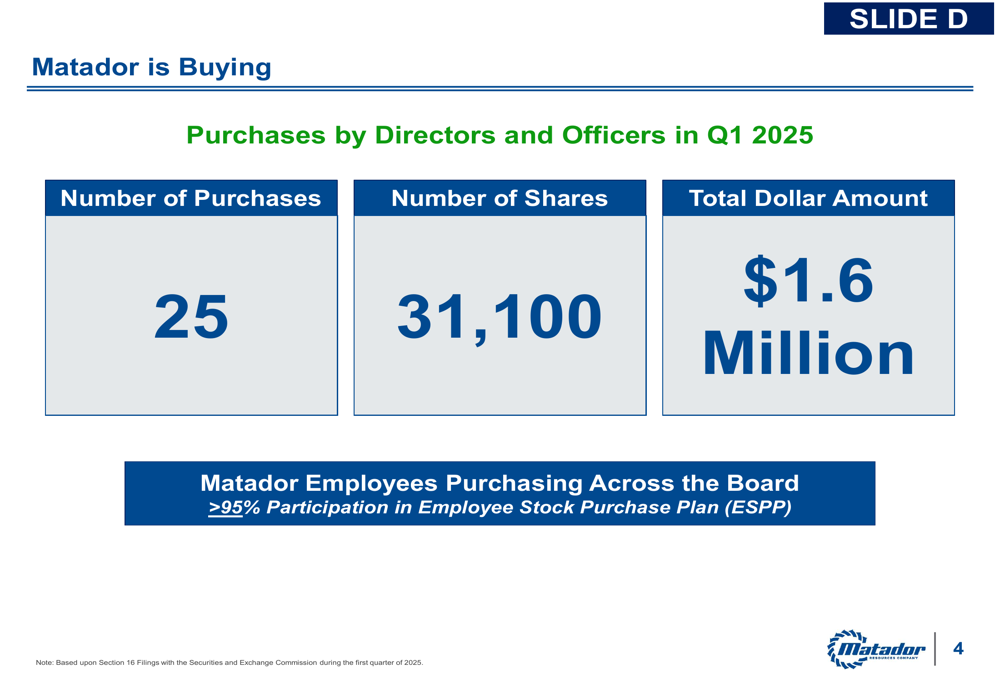

Management’s confidence in the company is further demonstrated by significant insider buying activity in Q1 2025, with 25 purchases totaling 31,100 shares worth $1.6 million. The company also noted strong employee participation in its stock purchase plan:

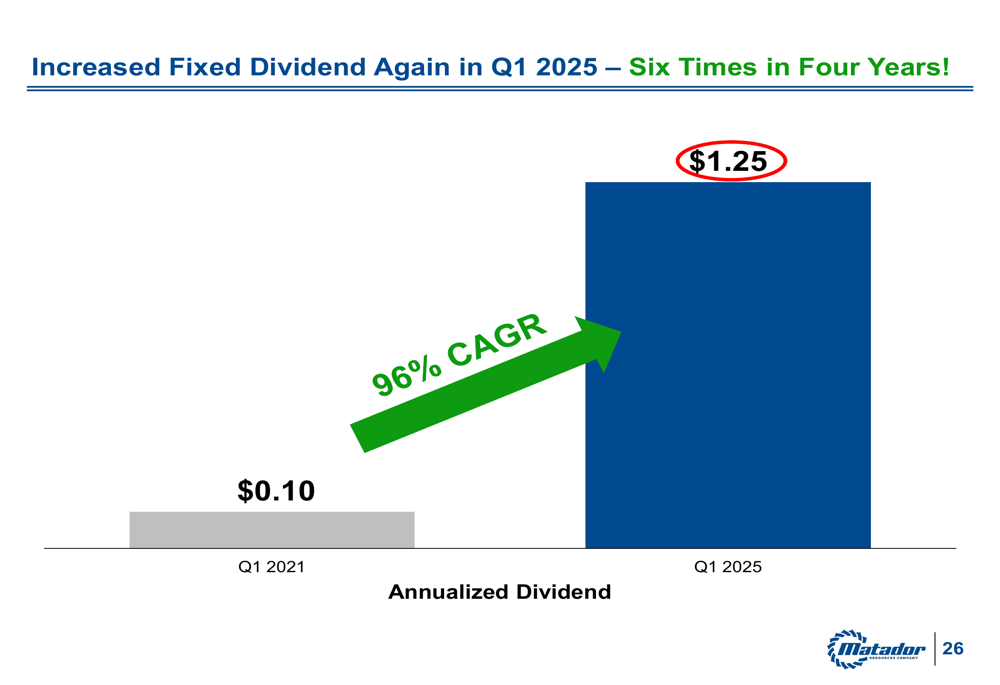

Matador has also continued to increase its dividend, which has grown from $0.10 per share in Q1 2021 to $1.25 per share in Q1 2025, representing a compound annual growth rate of 96%. The current dividend yield stands at approximately 3.0%.

Operational Efficiencies

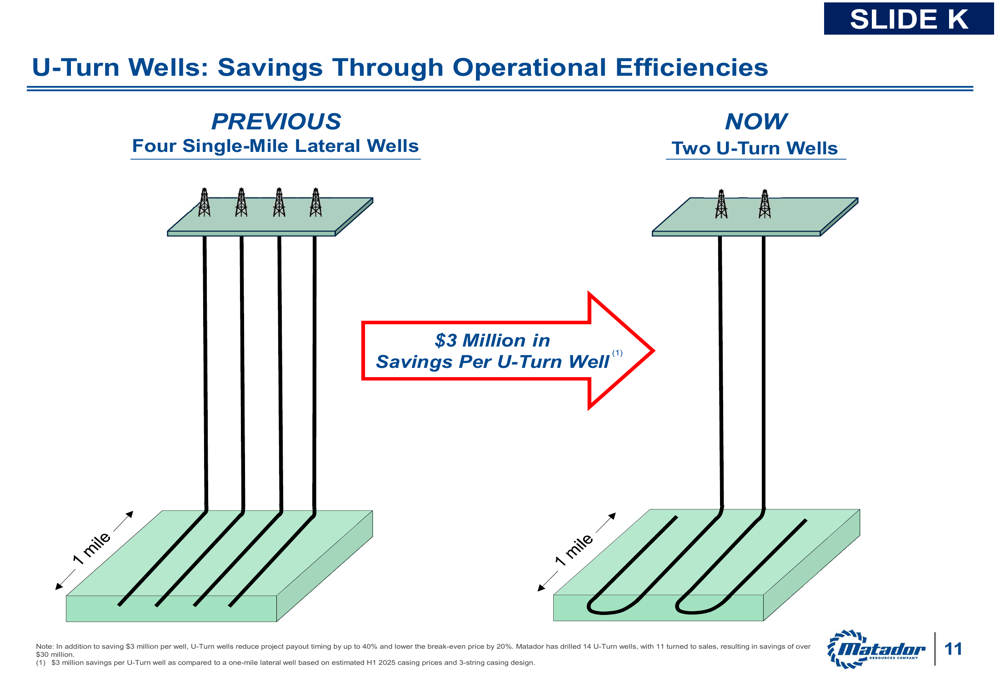

The presentation highlighted several operational efficiencies that have contributed to Matador’s strong performance. One notable innovation is the company’s U-Turn wells, which provide approximately $3 million in savings per well compared to traditional single-mile lateral wells:

These U-Turn wells not only reduce costs but also improve project economics by reducing payout timing by up to 40% and lowering break-even prices by 20%. Matador has drilled 14 such wells to date, with 11 turned to sales, resulting in savings of over $30 million.

The company also expects drilling and completion costs to average $865 to $895 per foot in 2025, representing a 3% decrease compared to 2024. This continues a trend of cost improvements, with an 18% reduction in D&C costs since 2023.

Competitive Industry Position

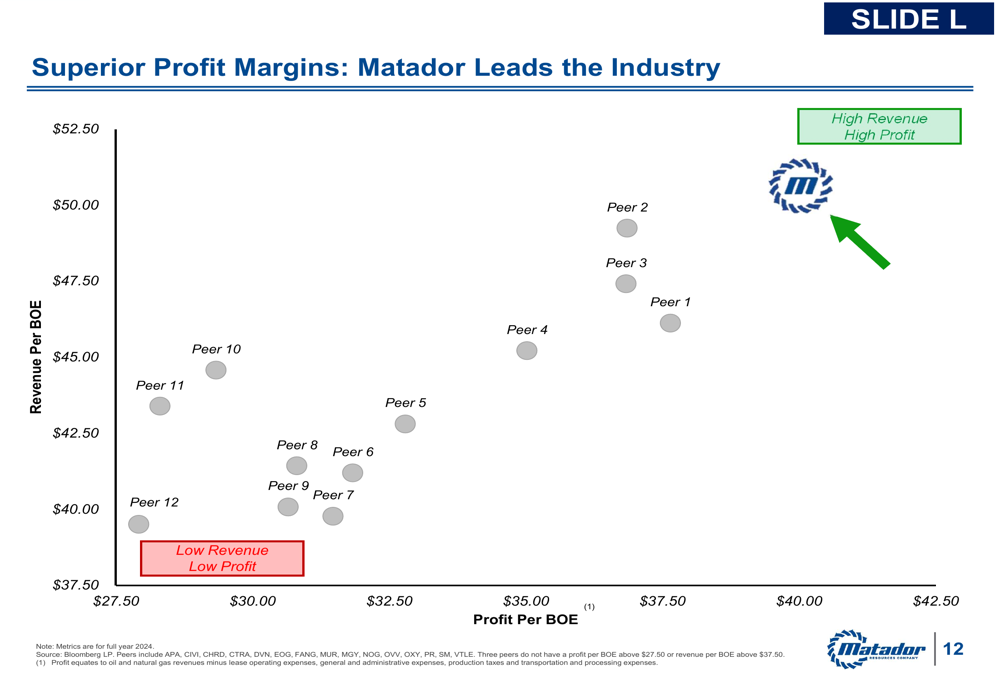

Matador emphasized its strong competitive position within the industry, highlighting its superior profit margins compared to peers:

The company also noted its industry-leading well productivity, with average oil EUR (Estimated Ultimate Recovery) exceeding that of its peer group. This productivity advantage, combined with Matador’s focus on operational efficiencies, has contributed to the company’s strong financial performance.

Asset Valuation and Investment Thesis

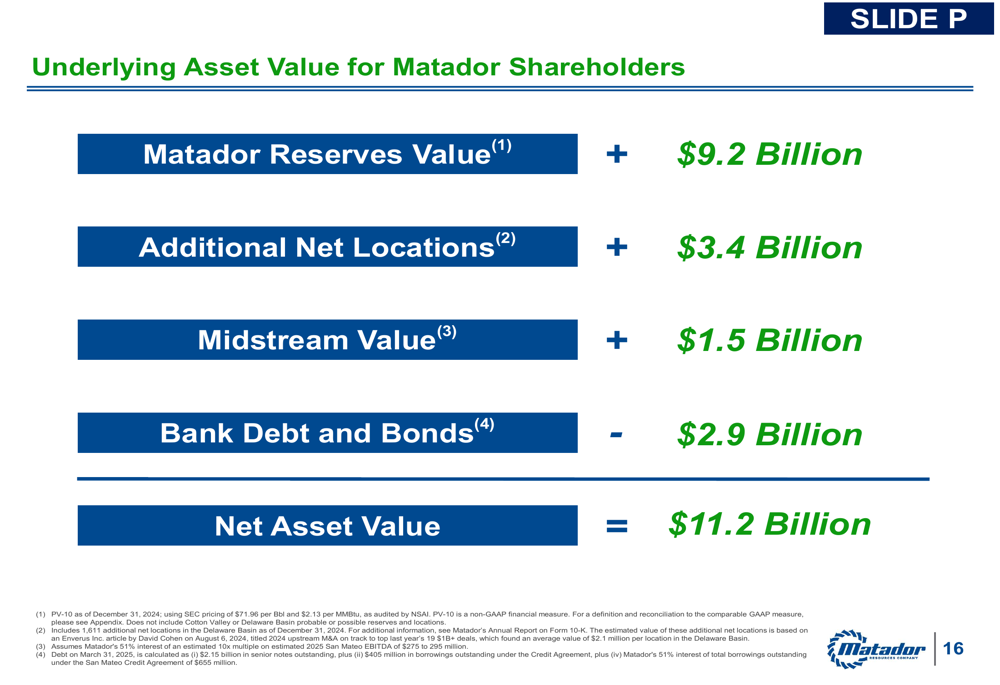

A key message in Matador’s presentation was the significant value of its assets compared to its market capitalization. The company estimated its net asset value at $11.2 billion, substantially higher than its market capitalization of approximately $4.95 billion as of the presentation date:

This valuation includes $9.2 billion for Matador’s reserves, $3.4 billion for additional net locations, and $1.5 billion for midstream assets, offset by $2.9 billion in bank debt and bonds.

The company summarized its investment thesis, highlighting its high margins, inventory depth, dividend growth, and strong balance sheet:

Forward-Looking Statements

Looking ahead, Matador maintained its 2025 oil production guidance of 114,000 to 115,000 barrels per day, despite already achieving 115,030 barrels per day in Q1. The company expects to adjust to an eight-rig Delaware Basin program in the middle of 2025, down from its current nine-rig program.

Capital expenditures for drilling, completion, and equipping (D/C/E) were $394.4 million in Q1 2025, slightly above the high end of the full-year guidance range of $340 to $400 million. Midstream capital expenditures were $46.4 million, below the full-year guidance range of $65 to $95 million.

The Marlan Plant, a key midstream asset, is expected to come online in Q2 2025 and was reported to be 90% complete as of March 31, 2025. This expansion will increase gas processing capacity from 520 MMcf per day to 720 MMcf per day.

Matador’s presentation reinforces the company’s position as a high-margin operator in the Delaware Basin with a strong balance sheet, growing production, and a commitment to returning capital to shareholders through dividends and share repurchases. The company’s focus on operational efficiencies and cost reductions should continue to support its competitive position in the industry.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.