German construction sector still in recession, civil engineering only bright spot

Introduction & Market Context

Matas Group presented its Q4 and full-year 2024/25 results on May 23, 2025, showcasing solid growth across its Nordic operations despite challenging market conditions. Despite reporting improved margins and announcing an enhanced capital distribution policy, shares of Matas (CPH:MATAS) fell 8.86% to DKK 142 following the presentation, as investors reacted to the company’s cautious outlook for the coming fiscal year.

The beauty and health retailer, which operates the Matas and KICKS brands across the Nordic region, delivered currency-neutral growth of 7.0% for the full year, driven by strong performance in both physical stores and e-commerce channels.

Quarterly Performance Highlights

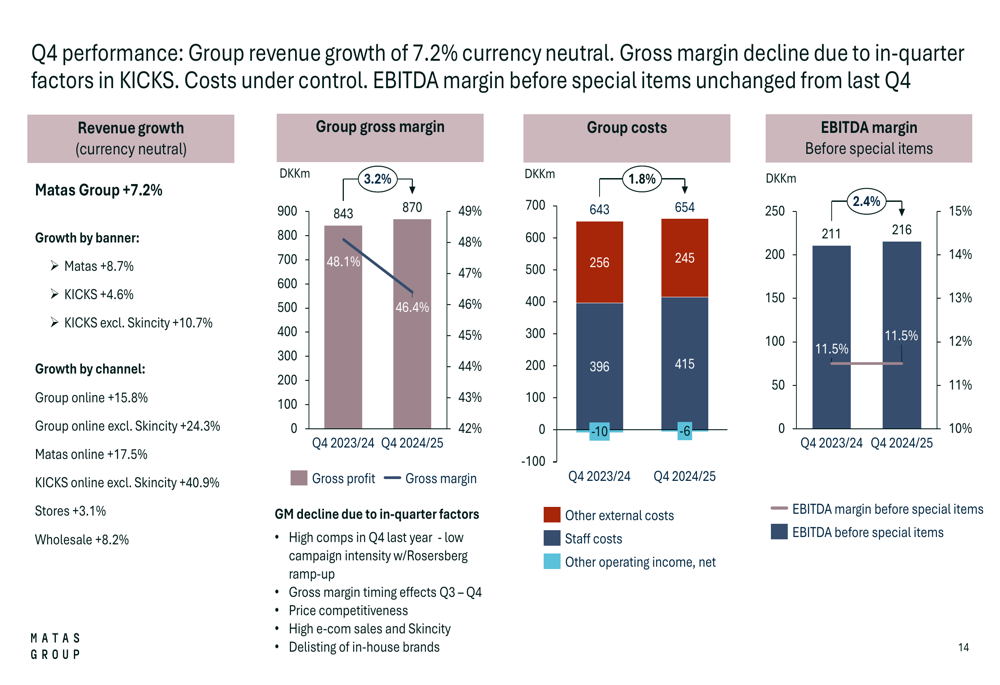

Matas Group reported currency-neutral growth of 7.2% year-over-year for Q4 2024/25, with the Matas banner growing 8.7% and KICKS increasing by 4.6% (10.7% excluding Skincity). Online sales were particularly strong, with group online growth of 15.8%, rising to 24.3% when excluding Skincity.

The company maintained its EBITDA margin before special items at 11.5% in Q4, matching the same period last year, despite some pressure on gross margins. Management attributed the gross margin decline to several factors, including high comparables from the previous year, timing effects between quarters, increased price competitiveness, and the delisting of in-house brands.

As shown in the following chart detailing Q4 performance metrics:

Detailed Financial Analysis

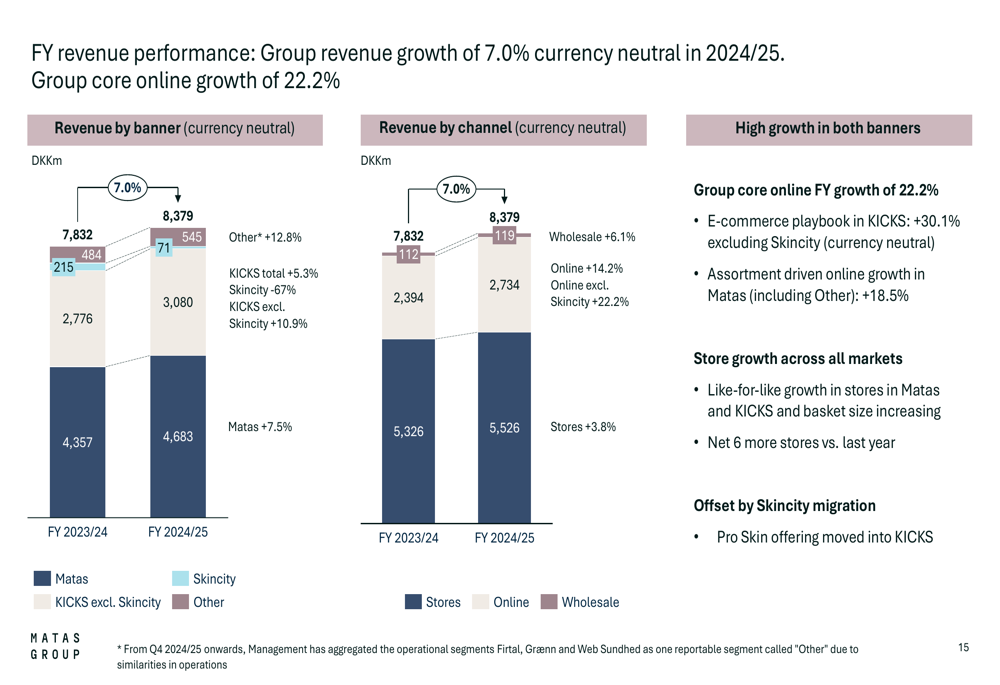

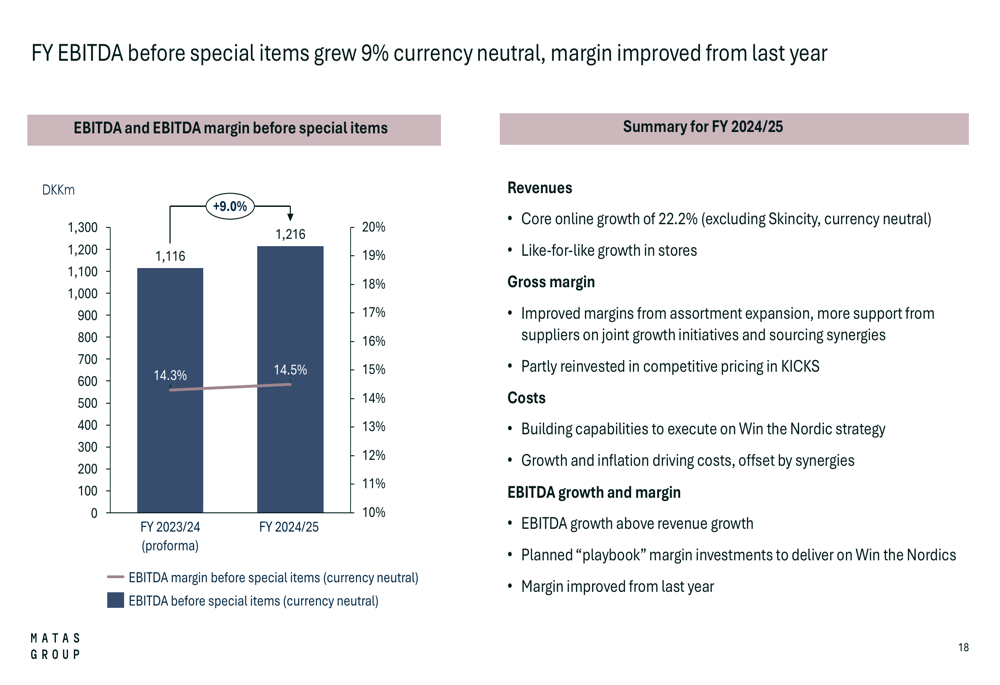

For the full fiscal year 2024/25, Matas Group achieved revenue of DKK 8,379 million, representing currency-neutral growth of 7.0% on a proforma basis. The EBITDA margin before special items improved to 14.5%, up from 14.3% in the previous year.

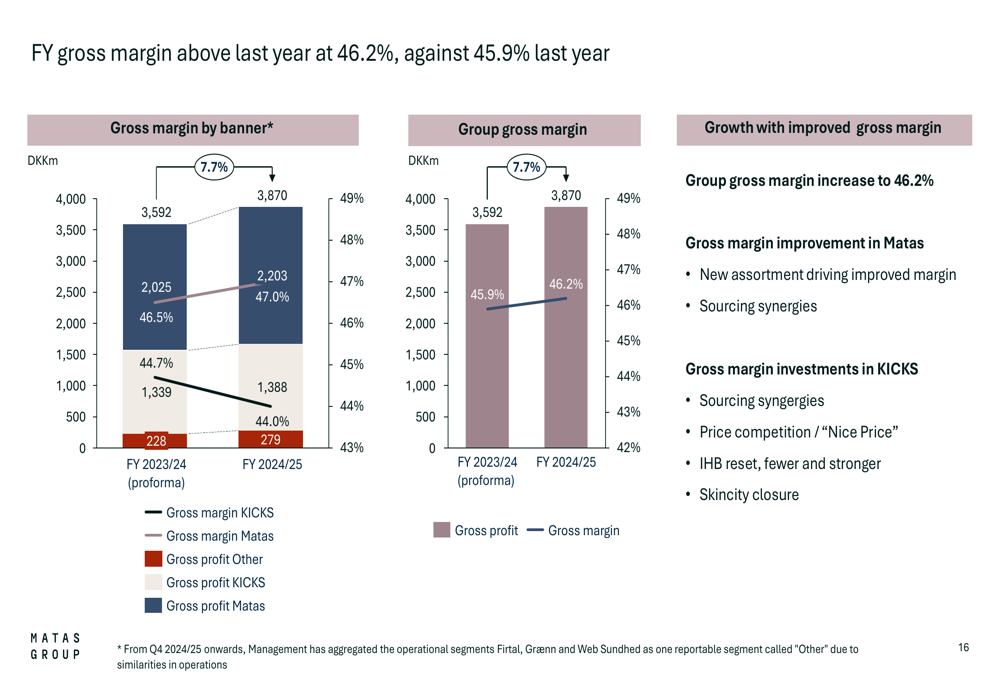

Breaking down performance by segment, Matas (including subsidiaries) generated revenue of DKK 5,228 million with stand-alone growth of 8.0% and an improved gross profit margin of 47.5% (compared to 46.5% in 2023/24). KICKS contributed DKK 3,151 million with currency-neutral growth of 5.3%, rising to 10.9% when excluding Skincity. However, KICKS’ gross profit margin declined slightly to 44.0% from 44.8% on a proforma basis.

The following chart illustrates the full-year revenue performance by banner and channel:

The group’s gross margin improved to 46.2% for the full year, compared to 45.9% in the previous year, reflecting the company’s focus on assortment optimization and operational efficiency. This margin improvement is particularly notable given the competitive market environment.

EBITDA before special items grew by 9% on a currency-neutral basis, with the margin improvement supported by strong online growth of 22.2% (excluding Skincity) and like-for-like growth in physical stores. The company’s cost control measures were effective, with costs growing at a slower rate than revenues.

Strategic Initiatives

Matas Group’s "Win the Nordics" strategy continues to drive growth across the region. The strategy focuses on three key pillars: "More for you," "All for you (Closer to you)," and "Stronger for you."

Key achievements in FY 2024/25 included the roll-out of a "one-stop" offering concept, launch of high-demand brands across both Matas and KICKS, and the expansion of in-house brands. The company launched approximately 260 new brands in Matas and 70 new brands in KICKS during the year, with 75 new brands introduced in Q4 alone.

The company’s Nordic membership program now exceeds 6 million members, with Matas having over 2 million members and KICKS approaching 4 million members, including more than 1 million in Norway. These loyalty programs continue to drive customer retention and increased basket sizes.

Operational improvements included the full activation of automated logistics centers in both Sweden and Denmark. The KICKS center in Rosersberg, outside Stockholm, and the Matas center in Lynge, outside Copenhagen, are now fully operational, supporting the company’s omni-channel strategy.

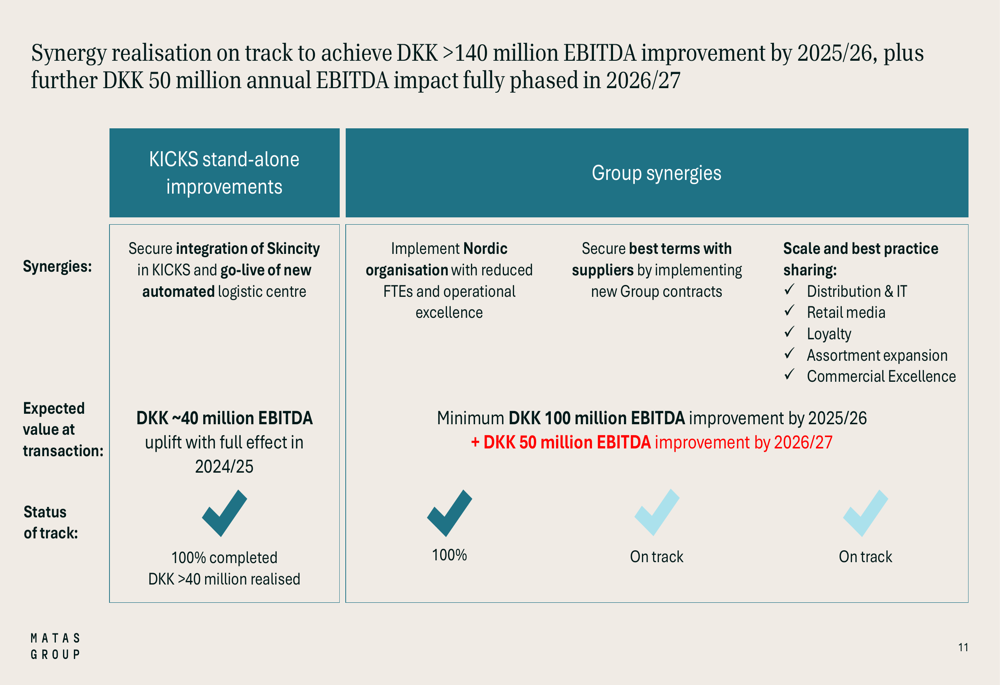

Synergy realization from the KICKS acquisition is on track to achieve DKK >140 million in EBITDA improvement by 2025/26, with an additional DKK 50 million annual EBITDA impact expected to be fully phased in by 2026/27. These synergies include the integration of Skincity into KICKS, organizational efficiencies, improved supplier terms, and shared distribution and IT infrastructure.

Forward-Looking Statements

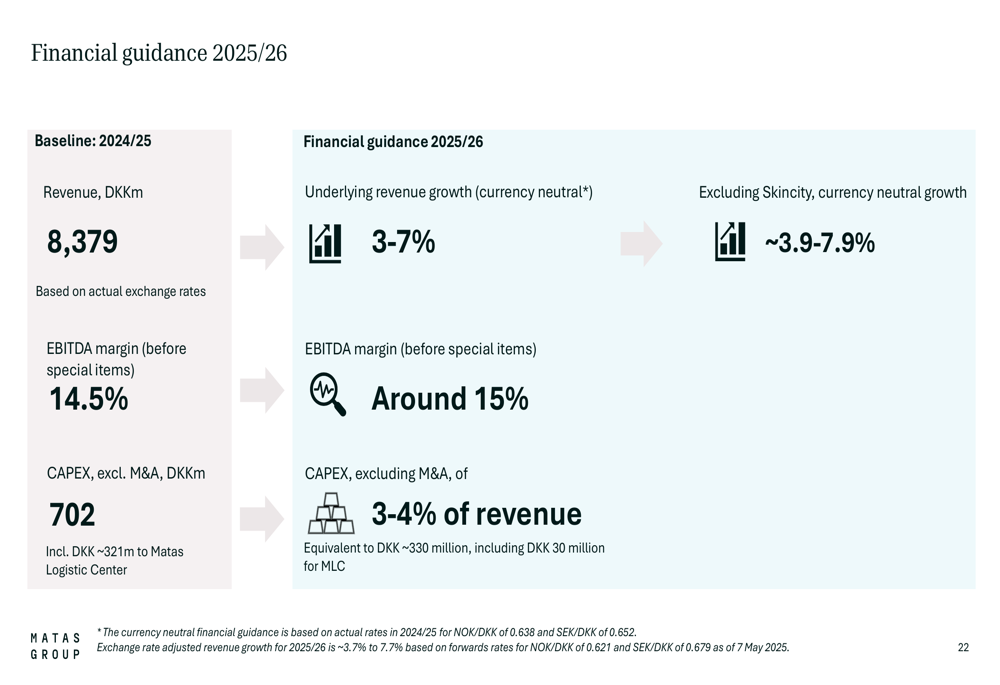

Looking ahead to FY 2025/26, Matas Group provided more cautious guidance, projecting revenue growth of 3% to 7% (3.9% to 7.9% excluding Skincity). This reflects increased uncertainty in the macroeconomic environment, particularly in Sweden where the company noted signs of a potential slowdown. Denmark and Finland show no impact from economic uncertainty, while Norway shows limited effects.

The company expects an EBITDA margin before special items of around 15% for 2025/26, with capital expenditure projected at 3-4% of revenue (approximately DKK 330 million, including DKK 30 million for Matas’ Logistics Center).

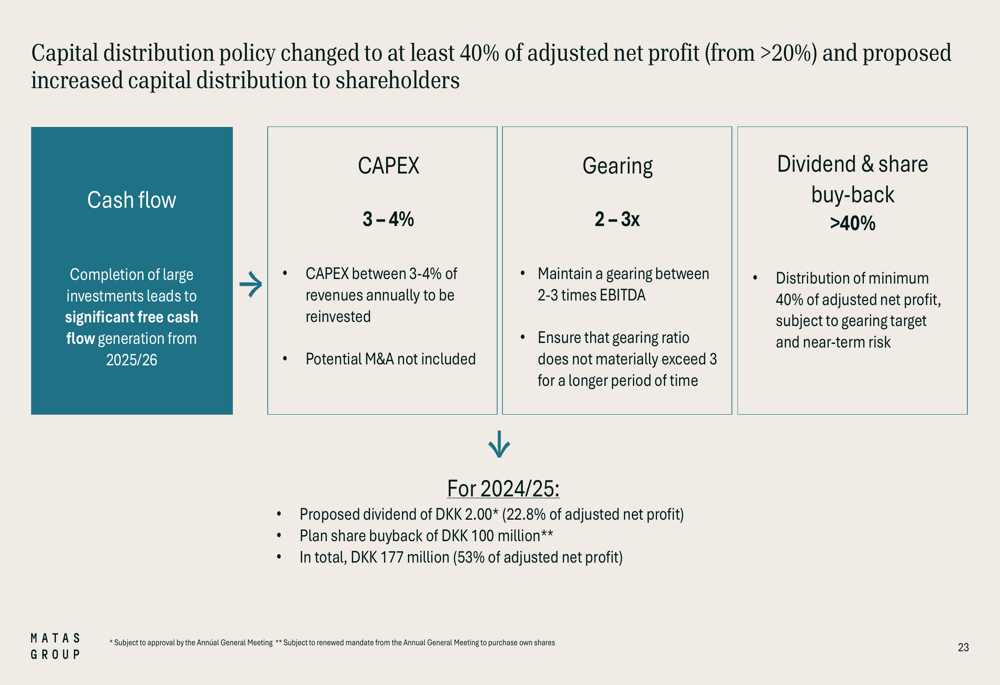

In a significant move for shareholders, Matas Group announced a change to its capital distribution policy, increasing the minimum distribution from 20% to 40% of adjusted net profit. The company proposed a dividend of DKK 2.00 per share and plans a share buyback program of DKK 100 million.

Despite the solid performance in FY 2024/25, the market reaction suggests investors were focused on the more cautious outlook for the coming year, particularly given signs of potential consumer spending slowdown in Sweden. However, management emphasized that the company’s omni-channel strategy, strong membership base, and operational efficiencies position it well to navigate potential headwinds in the Nordic beauty and health retail market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.