TSX higher on employment data

Introduction & Market Context

Mattel Inc . (NASDAQ:MAT) released its first quarter 2025 earnings presentation on May 5, showcasing modest growth amid challenging macroeconomic conditions. The toy manufacturer reported net sales growth of 2% as reported and 4% in constant currency, outperforming analyst expectations despite ongoing concerns about tariffs and consumer spending.

The company’s stock saw a slight decline of 0.56% in after-hours trading to $16.11, following a 1.1% drop during regular trading hours. This reaction came despite Mattel beating earnings expectations, suggesting investors remain cautious about the company’s outlook given the uncertain tariff situation.

Quarterly Performance Highlights

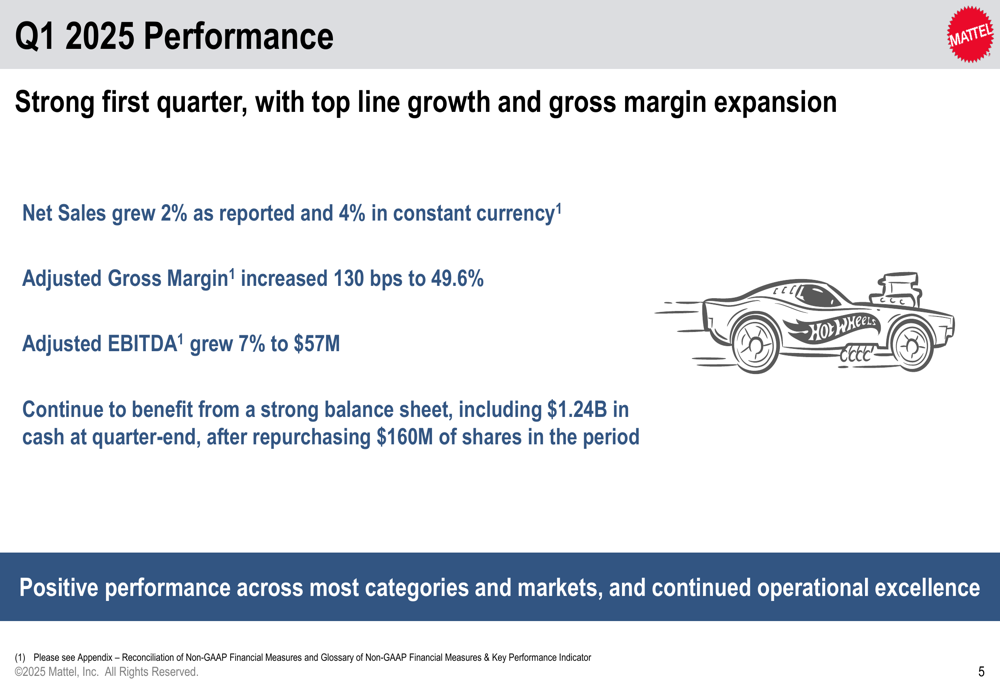

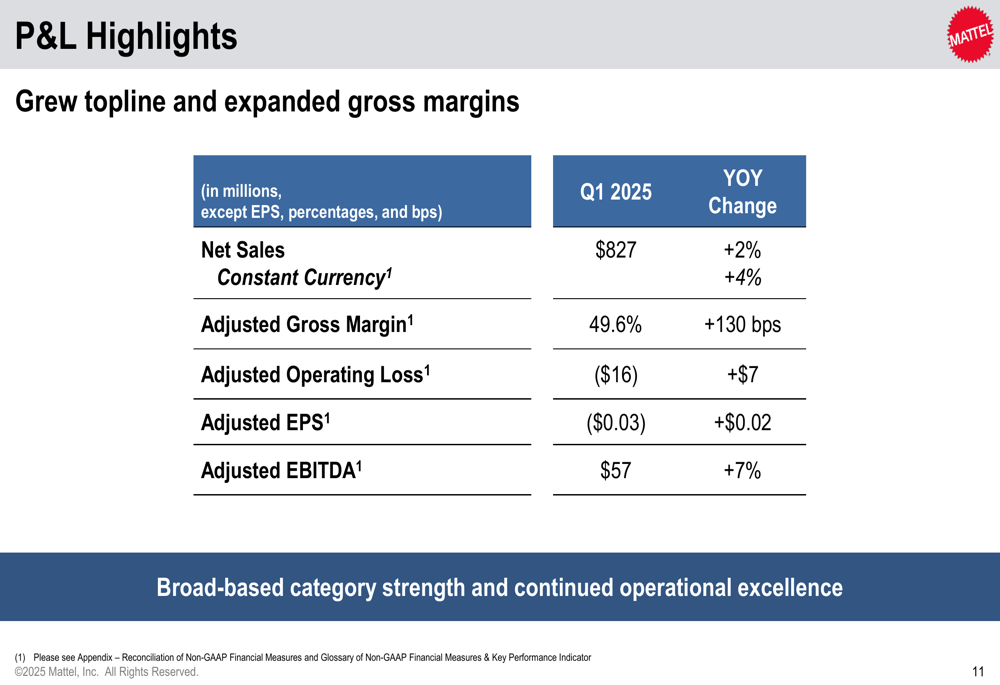

Mattel delivered a strong first quarter, with improvements across key financial metrics. The company reported net sales of $827 million, representing a 2% increase year-over-year. Adjusted gross margin expanded by 130 basis points to 49.6%, while adjusted EBITDA grew 7% to $57 million.

As shown in the following performance highlights slide, Mattel maintained a strong balance sheet with $1.24 billion in cash at quarter-end, after repurchasing $160 million of shares during the period:

The company’s adjusted operating loss improved by $7 million to ($16) million, and adjusted earnings per share improved by $0.02 to ($0.03). These results reflect Mattel’s continued operational excellence and effective cost management strategies.

A detailed breakdown of the profit and loss statement shows the company’s topline and gross margin growth:

Tariff Mitigation Strategy

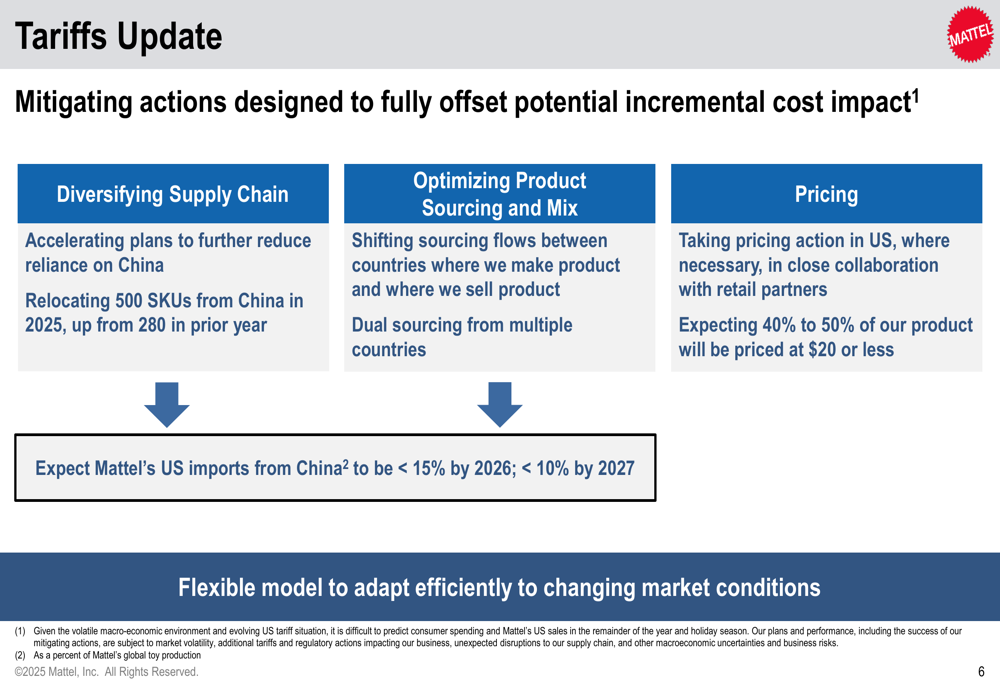

A significant focus of Mattel’s presentation was its comprehensive strategy to mitigate potential tariff impacts. The company is implementing several key actions to offset the potential incremental cost impact from tariffs, which could affect its U.S. business starting in Q3 2025.

The following slide outlines Mattel’s three-pronged approach to tariff mitigation:

Mattel is accelerating plans to diversify its supply chain and reduce reliance on China, relocating 500 SKUs from China in 2025, up from 280 in the prior year. The company expects U.S. imports from China to decrease to less than 15% by 2026 and less than 10% by 2027.

Additionally, Mattel is optimizing product sourcing and mix by shifting sourcing flows between countries and implementing dual sourcing from multiple countries. The company is also taking pricing action in the U.S. where necessary, while maintaining that 40% to 50% of its products will be priced at $20 or less.

Category and Regional Performance

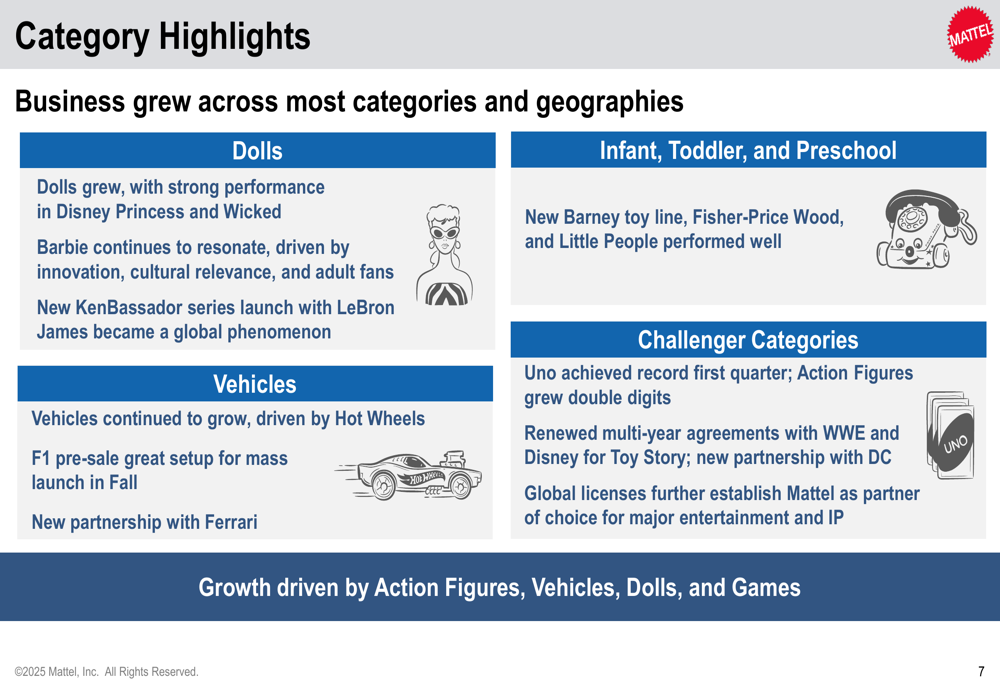

Mattel reported growth across most product categories and geographical regions in Q1 2025. The company’s diverse portfolio of brands continues to resonate with consumers globally, with particularly strong performance in its Dolls and Vehicles segments.

The following slide highlights key category performances:

The Dolls category grew with strong performance from Disney (NYSE:DIS) Princess and Wicked lines. Barbie continues to maintain cultural relevance, bolstered by the launch of the KenBassador series featuring LeBron James, which became a global phenomenon.

Vehicles continued to grow, driven by Hot Wheels, with a successful F1 pre-sale setting up for a mass launch in Fall. The company also announced a new partnership with Ferrari (BIT:RACE).

In the Challenger Categories, Uno achieved a record first quarter, while Action (WA:ACT) Figures grew double digits. Mattel renewed multi-year agreements with WWE and Disney for Toy Story and established a new partnership with DC.

The only category showing decline was Infant, Toddler, and Preschool, which fell 5% in constant currency, though the company noted strong performance from the new Barney toy line, Fisher-Price Wood, and Little People.

Entertainment and IP Expansion

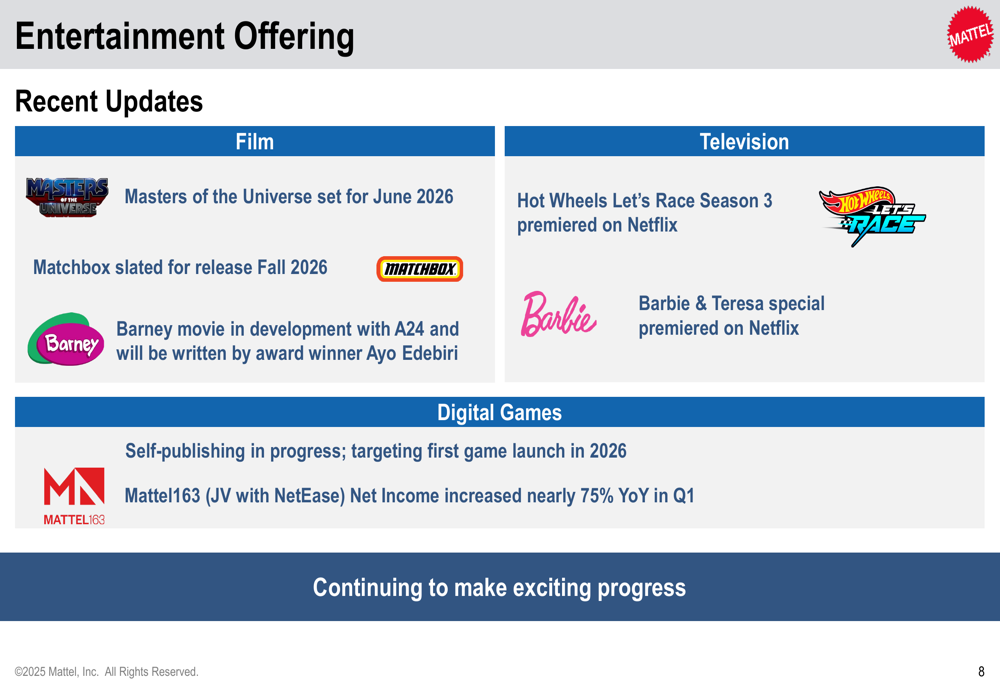

A key component of Mattel’s long-term strategy is expanding its entertainment offerings to capture the full value of its intellectual property. The company provided updates on various film, television, and digital gaming initiatives.

The following slide details Mattel’s progress in entertainment:

In film, Masters of the Universe is set for release in June 2026, with Matchbox slated for Fall 2026. A Barney movie is in development with A24, to be written by award-winner Ayo Edebiri.

On the television front, Hot Wheels Let’s Race Season 3 and a Barbie & Teresa special both premiered on Netflix (NASDAQ:NFLX) during the quarter.

Digital gaming initiatives are progressing, with Mattel targeting its first self-published game launch in 2026. Meanwhile, Mattel163, the company’s joint venture with NetEase (NASDAQ:NTES), saw its net income increase nearly 75% year-over-year in Q1.

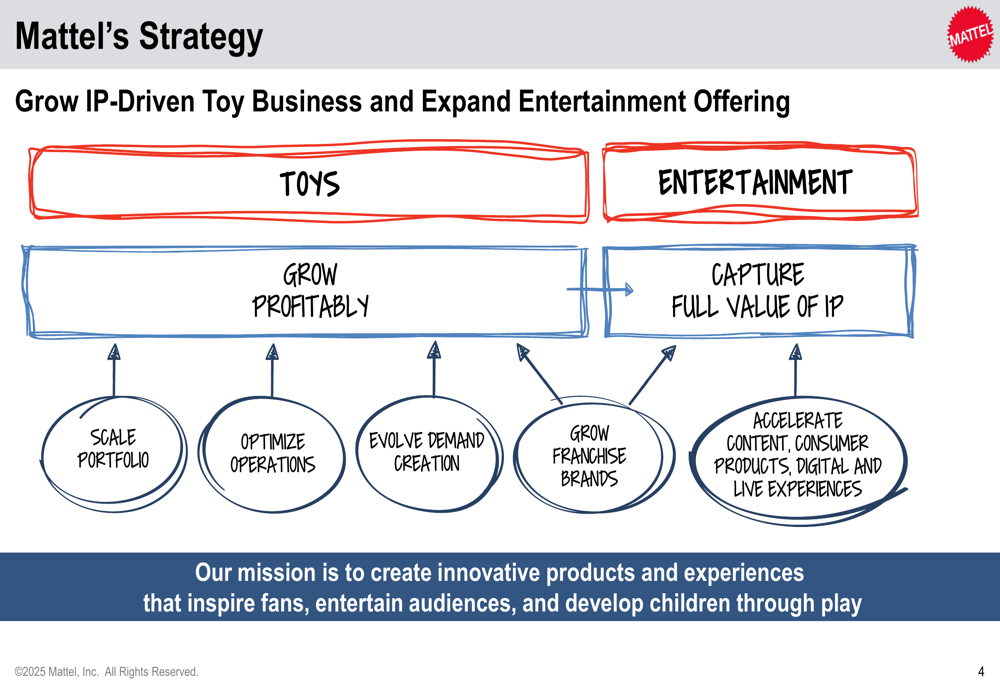

This entertainment strategy aligns with Mattel’s overall business approach, which focuses on growing its IP-driven toy business while expanding entertainment offerings:

Cost Optimization Progress

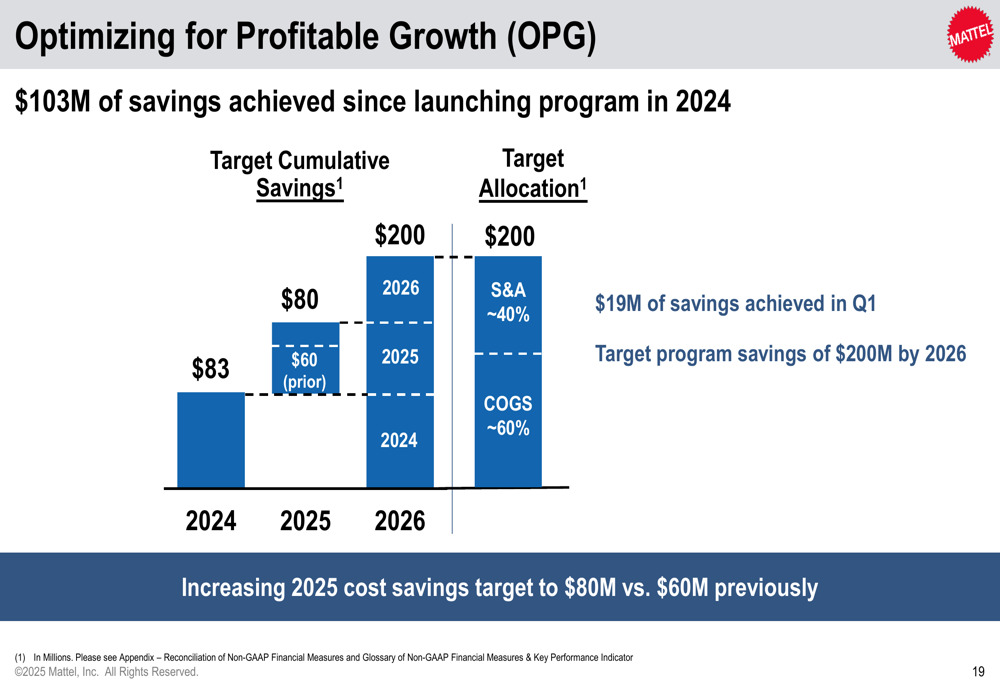

Mattel continues to make significant progress with its Optimizing for Profitable Growth (OPG) program, which is designed to improve operational efficiency and reduce costs.

The following slide shows the company’s achievements and targets for this initiative:

Since launching the program in 2024, Mattel has achieved $103 million in savings. The company has increased its 2025 cost savings target to $80 million, up from the previously announced $60 million, and maintains its overall program target of $200 million in savings by 2026.

These cost savings are allocated 40% to selling and administrative expenses and 60% to cost of goods sold, providing a balanced approach to margin improvement.

Forward-Looking Statements

Given the volatile macroeconomic environment and evolving U.S. tariff situation, Mattel has paused its full-year 2025 guidance until it has sufficient visibility into consumer spending and U.S. sales for the remainder of the year.

Despite this pause in guidance, the company maintained its $600 million share repurchase target for 2025, signaling confidence in its long-term strategy and financial position. Mattel also noted that its international business is not expected to be materially impacted by tariffs.

Point of sale (POS) data is off to a strong start in Q2, up double digits quarter-to-date both in the U.S. and internationally. The company expects Q2 to benefit from Jurassic World and Minecraft innovative products, as well as continued Hot Wheels momentum.

Ynon Kreiz, Chairman and CEO of Mattel, expressed confidence in the company’s strategy: "This was a strong quarter for Mattel, with positive performance and continued operational excellence. Our brands are thriving, our products and experiences stand out in the marketplace, and our balance sheet gives us resilience and flexibility to execute our strategy. As we navigate the current period of macro-economic volatility, we are adapting with speed, agility, and discipline. We expect not only to manage through this period but strengthen our competitive position."

While challenges remain, particularly related to tariffs and uncertain consumer spending, Mattel’s diversified manufacturing footprint and flexible business model position the company to navigate the current environment while continuing to execute its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.