Gold prices slip as stronger dollar, Fed rate uncertainty weigh

Introduction & Market Context

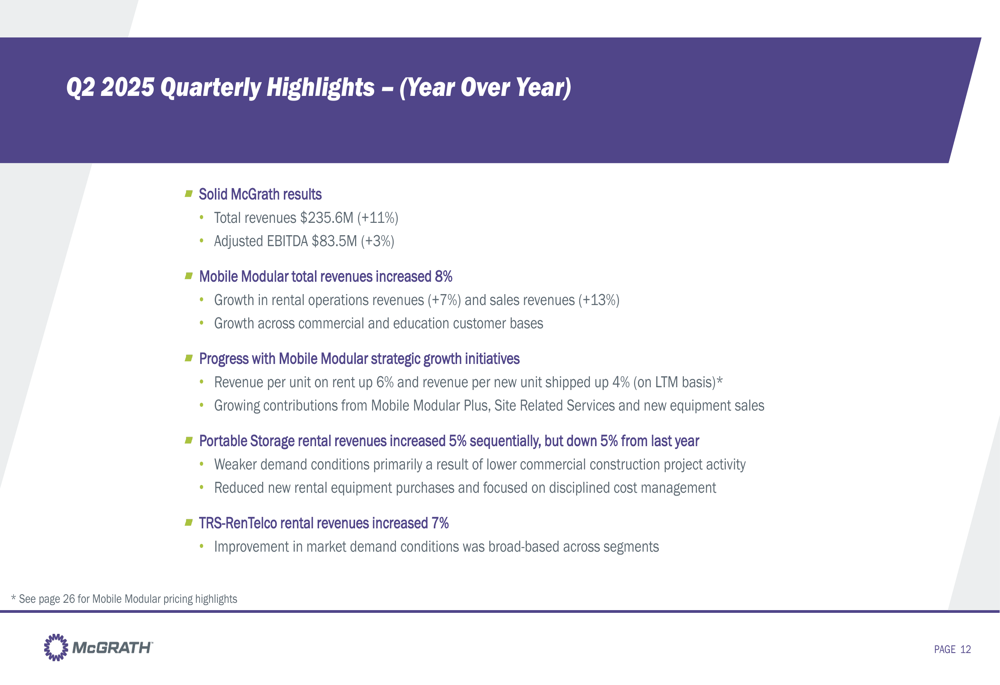

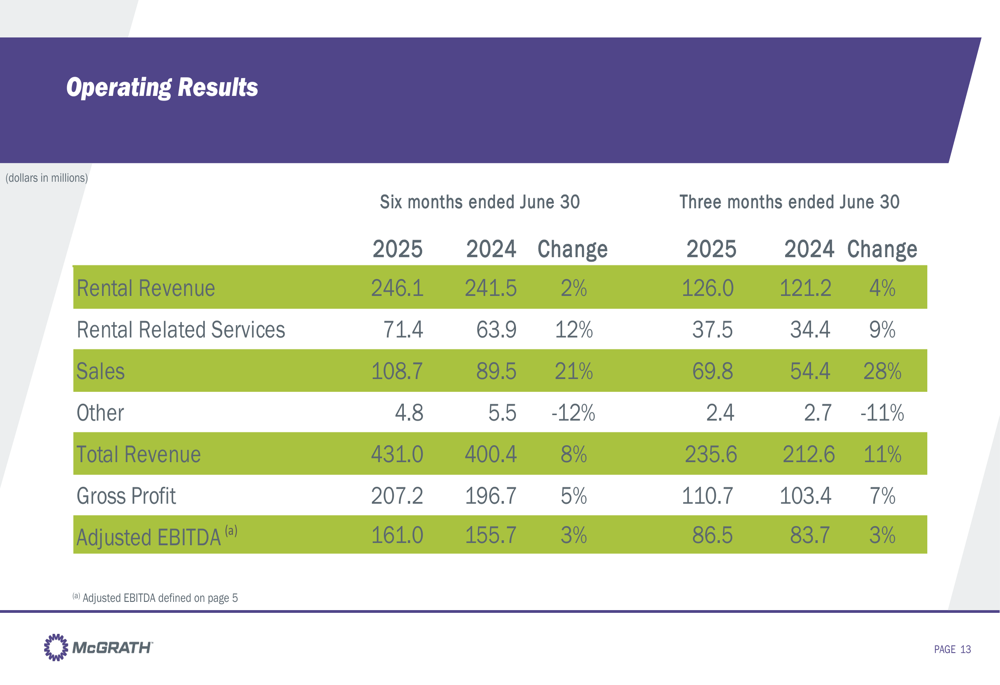

McGrath RentCorp (NASDAQ:MGRC), a leading provider of modular buildings, portable storage, and electronic test equipment, reported an 11% year-over-year increase in total revenues for Q2 2025, reaching $235.6 million. The company presented these results during its quarterly investor presentation on July 24, 2025, highlighting solid performance across most business segments despite a mixed economic environment.

Trading at $115.47 as of the most recent close, McGrath shares have shown resilience, maintaining a position well above their 52-week low of $97.81. The company, valued at approximately $2.87 billion, continues to demonstrate its ability to navigate economic uncertainties while delivering value to shareholders through its diversified business model.

Quarterly Performance Highlights

McGrath’s Q2 2025 results showed notable strength, with total revenues increasing 11% year-over-year to $235.6 million. Adjusted EBITDA grew 3% to $83.5 million, reflecting the company’s operational efficiency despite ongoing economic challenges.

The company’s performance for the first half of 2025 was equally impressive, with total revenues reaching $431.0 million, an 8% increase compared to the same period in 2024. This growth was driven by increases across all revenue streams: rental revenue (+2%), rental related services (+12%), and sales (+21%).

Rental revenue showed steady improvement throughout 2025, with McGrath achieving a 4% increase between Q1 and Q2. This growth was primarily driven by the Mobile Modular segment (+5%) and TRS-RenTelco (+7%), while Portable Storage experienced a 5% decline.

Segment Performance Analysis

Mobile Modular

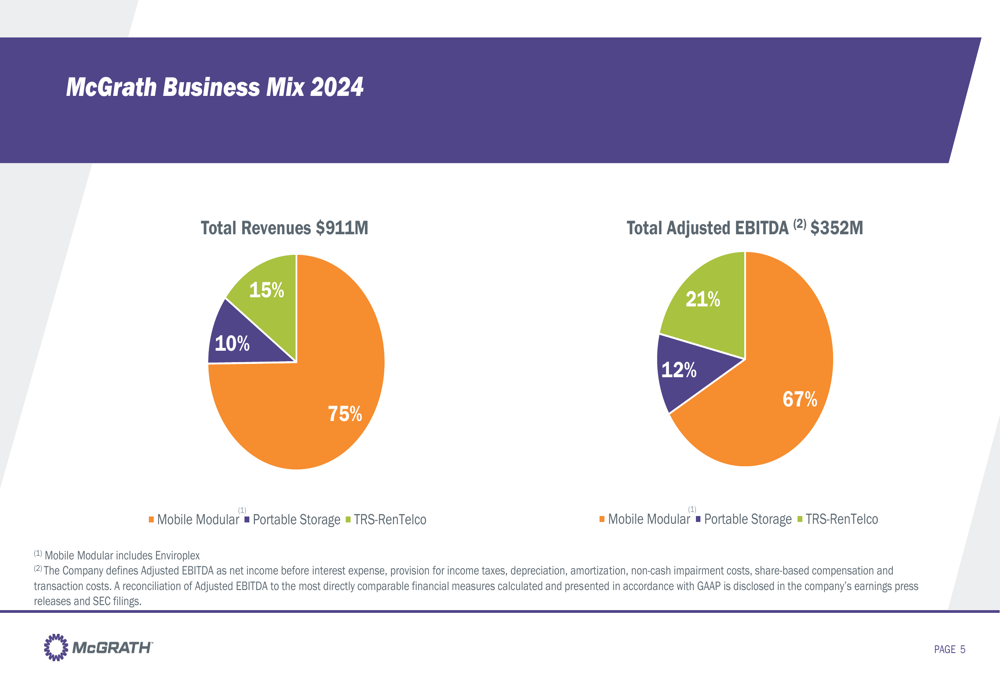

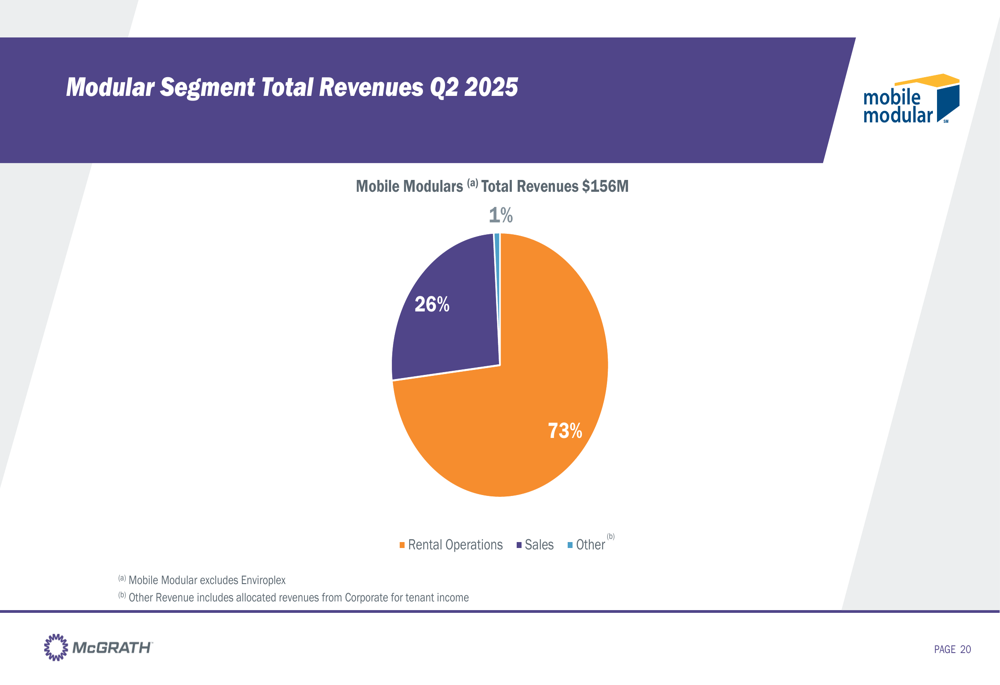

The Mobile Modular segment, which accounts for 75% of McGrath’s total revenue and 67% of adjusted EBITDA (based on 2024 figures), delivered an 8% increase in total revenues for Q2 2025, reaching $156 million. This growth was driven by a 7% increase in rental operations and a 13% rise in sales revenues.

The segment’s revenue mix for Q2 2025 shows that 73% came from rental operations, 26% from sales, and 1% from other sources. Despite the revenue growth, adjusted EBITDA for the segment decreased slightly by 1% year-over-year.

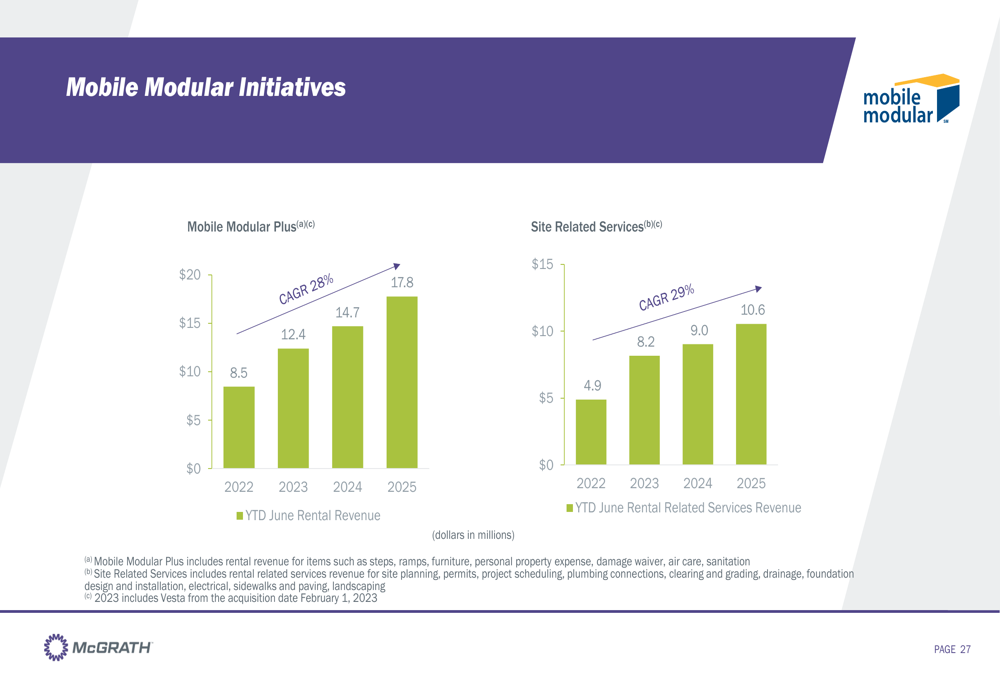

Mobile Modular’s strategic initiatives are showing positive results, with revenue per unit on rent increasing by 6% and revenue per new unit shipped up by 4%. The company has also seen growth in its value-added services, with Mobile Modular Plus and Site Related Services continuing to expand.

Portable Storage

The Portable Storage segment faced challenges in Q2 2025, with rental revenues declining 5% year-over-year. However, the company noted a 5% sequential improvement from Q1 2025, suggesting potential stabilization in this business line.

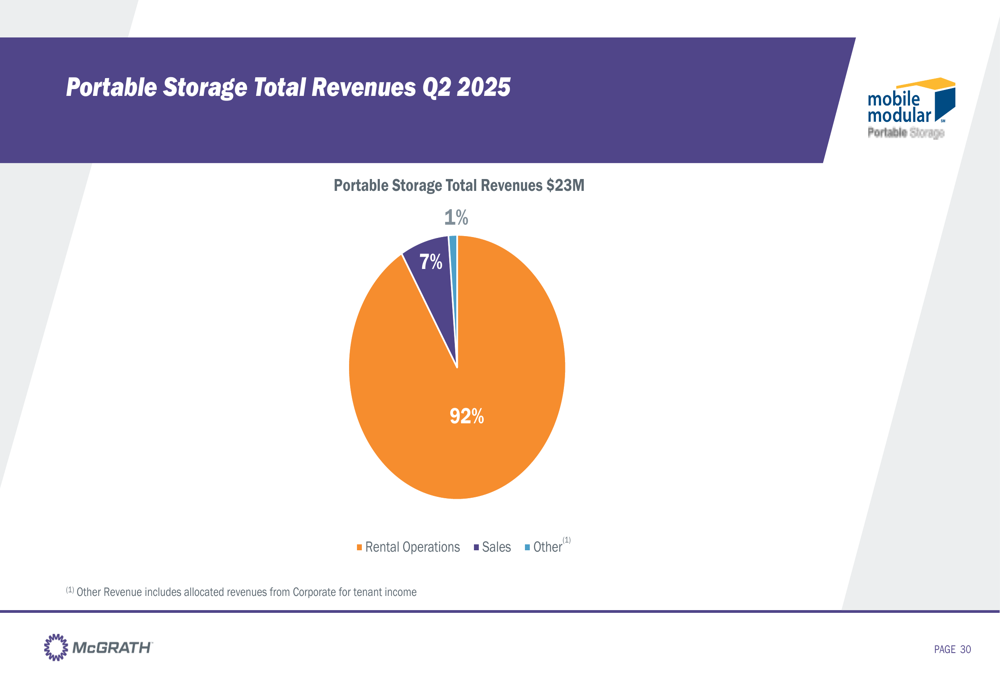

For Q2 2025, the segment generated $23 million in total revenues, with 92% coming from rental operations, 7% from sales, and 1% from other sources.

TRS-RenTelco

The TRS-RenTelco segment, which specializes in electronic test equipment rental, demonstrated solid performance with a 7% increase in rental revenues. This segment contributed $36 million to McGrath’s total revenues in Q2 2025.

The segment’s consistent performance reflects its position as a market leader with a highly diversified customer base and positive long-term demand drivers. TRS-RenTelco accounted for 15% of McGrath’s total revenues and 21% of adjusted EBITDA in 2024.

Strategic Initiatives & Growth Drivers

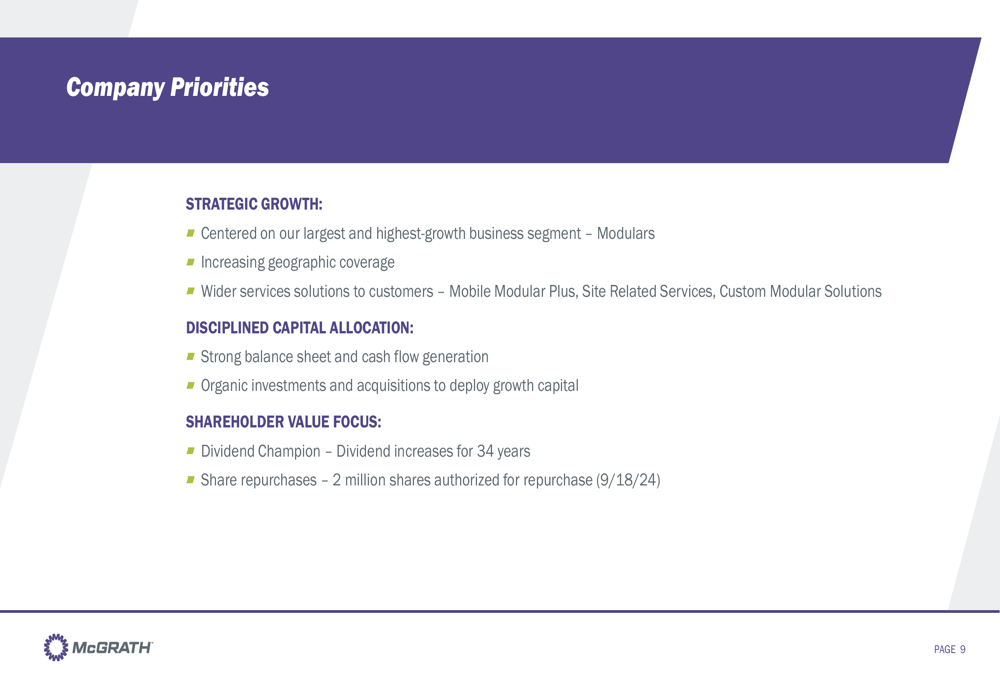

McGrath outlined several strategic priorities during the presentation, focusing on three key areas: strategic growth, disciplined capital allocation, and shareholder value creation.

The company’s strategic growth initiatives center around its modular business, with plans to increase geographic coverage and expand its solution offerings. McGrath currently services 35 states through its Mobile Modular division and 29 states through Portable Storage, indicating room for further expansion.

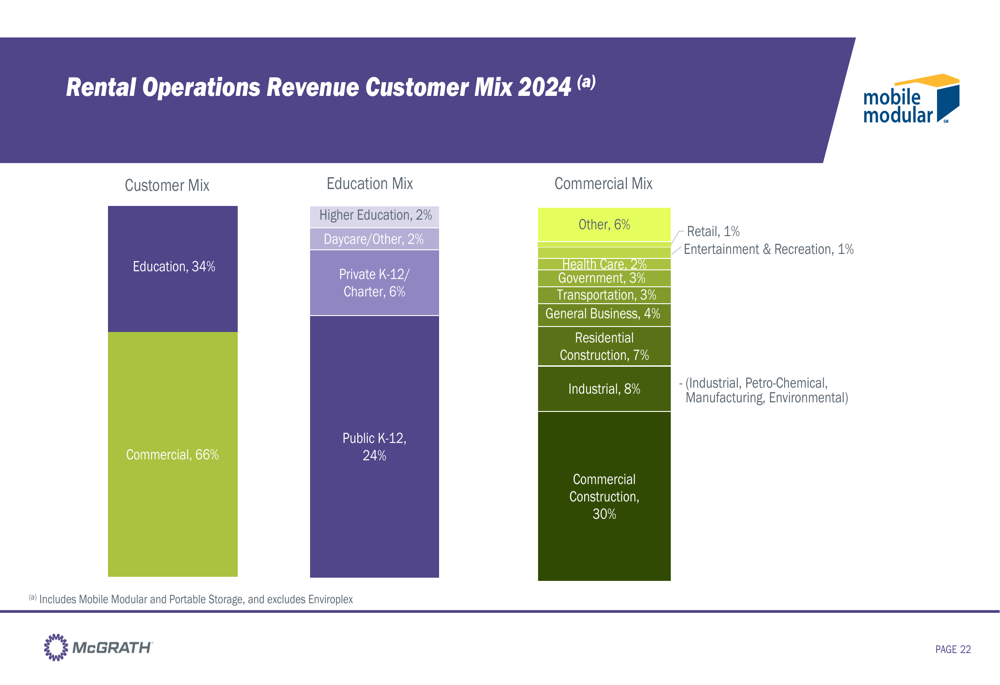

Customer diversification remains a strength for McGrath, with its rental operations revenue split between education (34%) and commercial (66%) sectors. This diversification helps insulate the company from downturns in specific markets.

Pricing improvements have been a key driver of growth, particularly in the Mobile Modular segment. The company reported that revenue per unit on rent increased from $793 to $840, while revenue for new shipments rose from $1,124 to $1,168 over the last twelve months.

Financial Outlook & Guidance

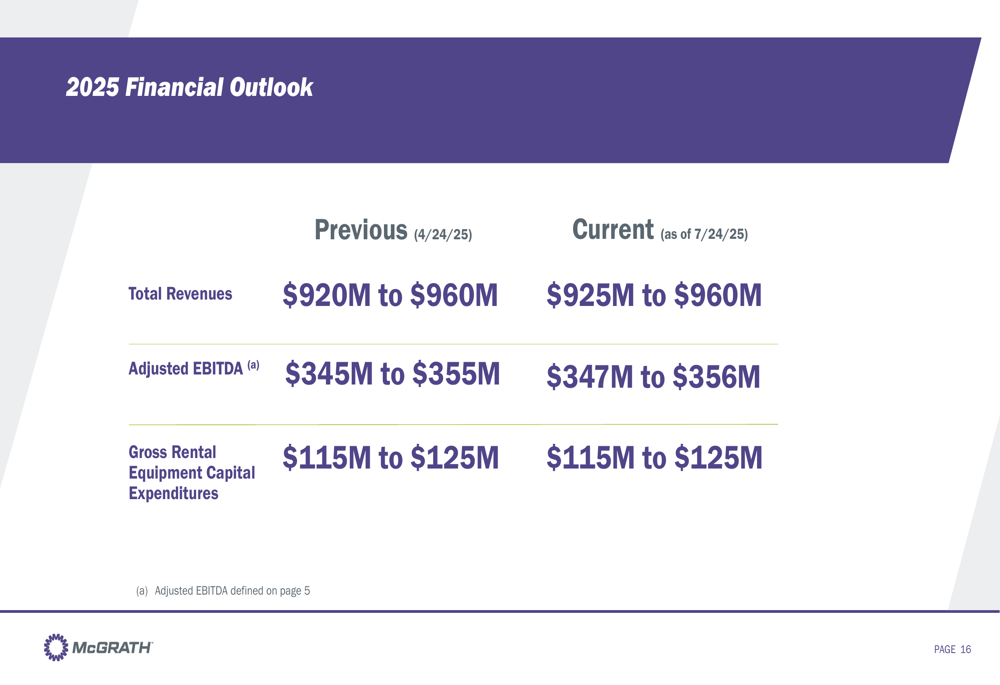

Based on its strong first-half performance, McGrath has raised its financial outlook for 2025. The company now expects total revenues to be between $925 million and $960 million, up from the previous guidance of $920 million to $960 million.

Similarly, adjusted EBITDA is now projected to be between $347 million and $356 million, an improvement from the previous range of $345 million to $355 million. Capital expenditures for rental equipment are expected to remain between $115 million and $125 million.

During the earnings call, management expressed cautious optimism about economic conditions improving in the coming quarters. CEO Joe Hanna noted that the company is "successfully navigating an uncertain economic environment" while continuing to deliver value to customers.

The company also highlighted potential benefits from anticipated federal tax legislation, which could add $10-$15 million in free cash flow benefits.

Conclusion

McGrath RentCorp’s Q2 2025 presentation demonstrates the company’s resilience and ability to generate growth despite economic uncertainties. The 11% increase in total revenues, driven primarily by the Mobile Modular and TRS-RenTelco segments, underscores the effectiveness of McGrath’s diversified business model.

The company’s decision to raise its financial outlook for 2025 signals confidence in continued momentum through the second half of the year. With a strong balance sheet, strategic growth initiatives, and a 34-year track record of dividend increases, McGrath appears well-positioned to navigate current market challenges while pursuing long-term growth opportunities.

Investors should note that while the overall trajectory remains positive, segment performance varies, with Portable Storage facing ongoing challenges despite sequential improvement. Management’s cautious optimism about economic conditions and active M&A pipeline suggest potential for further strategic developments in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.