Is this U.S.-China selloff a buy? A top Wall Street voice weighs in

Introduction & Market Context

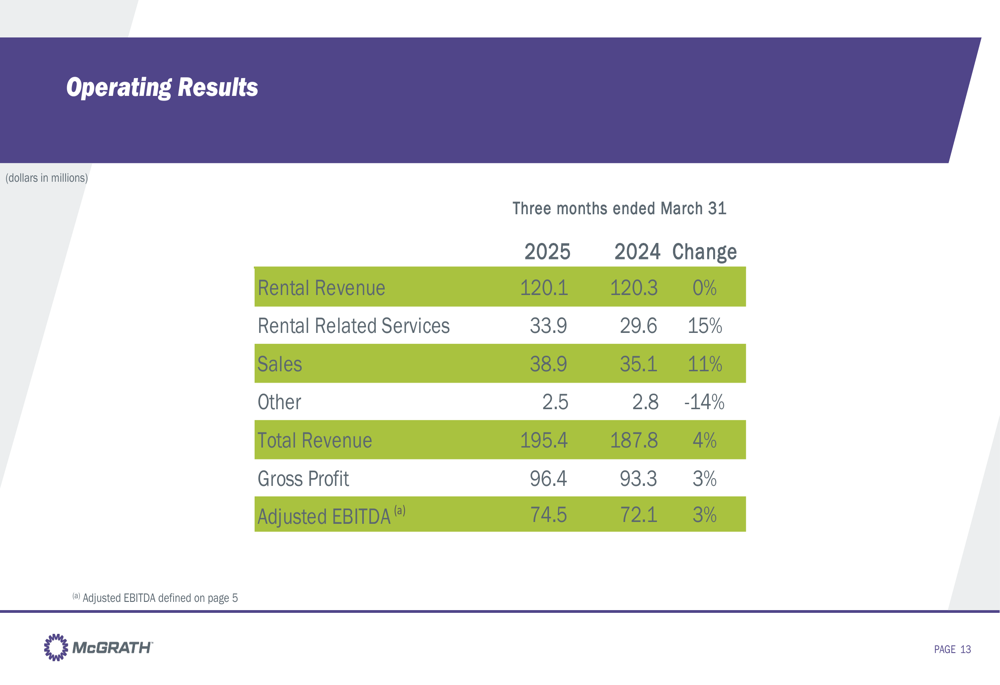

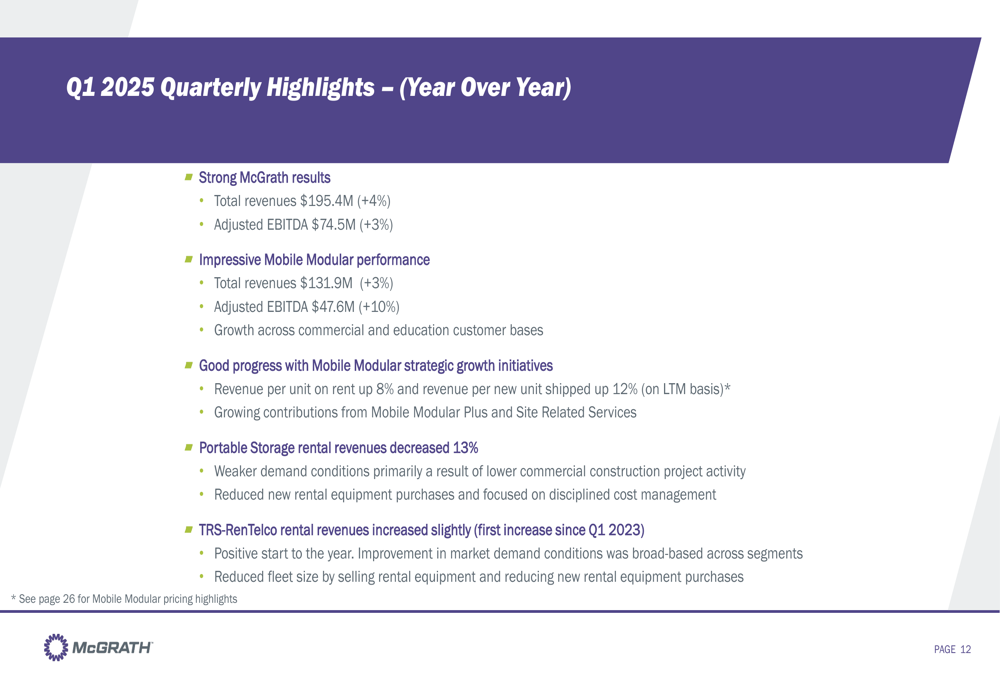

McGrath RentCorp (NASDAQ:MGRC) released its Q1 2025 investor presentation on April 24, 2025, highlighting a 4% year-over-year increase in total revenues to $195.4 million and a 3% rise in adjusted EBITDA to $74.5 million. The company’s stock closed at $102.42 on the day of the presentation and saw a modest 1.56% increase, reflecting cautious investor optimism despite mixed segment performance.

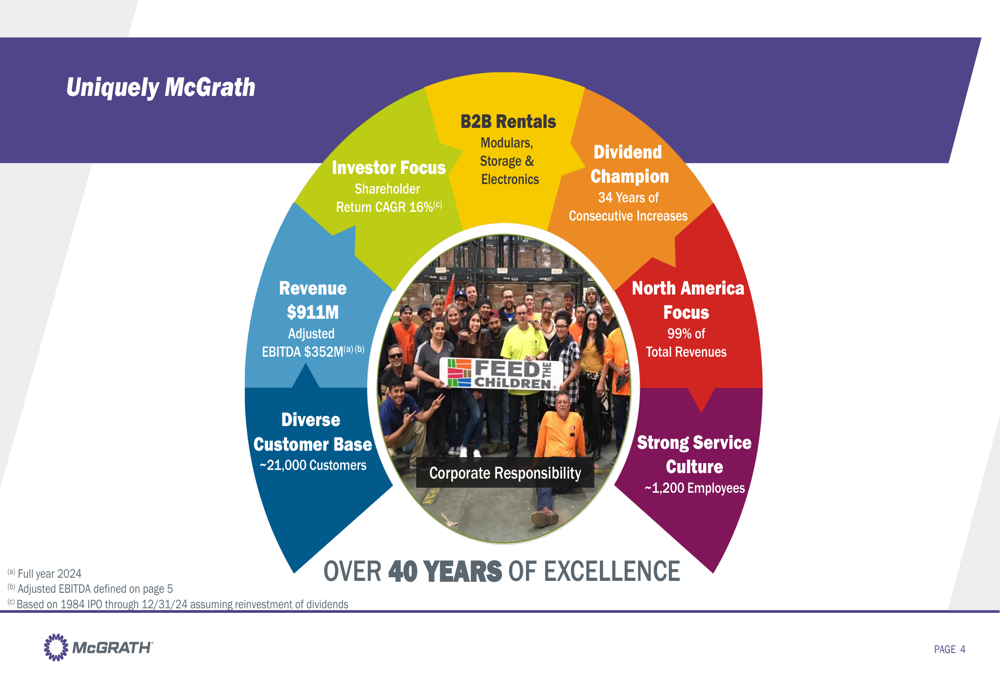

The B2B rental company, which focuses on modulars, storage, and electronics equipment, continues to leverage its strong North American presence, with 99% of revenues generated in this market. McGrath maintains a diverse customer base of approximately 21,000 clients and has positioned itself as a "Dividend Champion" with 34 consecutive years of dividend increases.

As shown in the following key highlights from the presentation:

Quarterly Performance Highlights

McGrath’s Q1 2025 results demonstrated resilience in a challenging economic environment, with total revenues increasing to $195.4 million (+4% YoY) and adjusted EBITDA rising to $74.5 million (+3% YoY). The company’s performance was primarily driven by the Mobile Modular segment, which offset weakness in the Portable Storage business.

The detailed financial comparison between Q1 2025 and Q1 2024 shows improvements across most revenue categories, with particularly strong growth in rental related services (+15%) and sales (+11%):

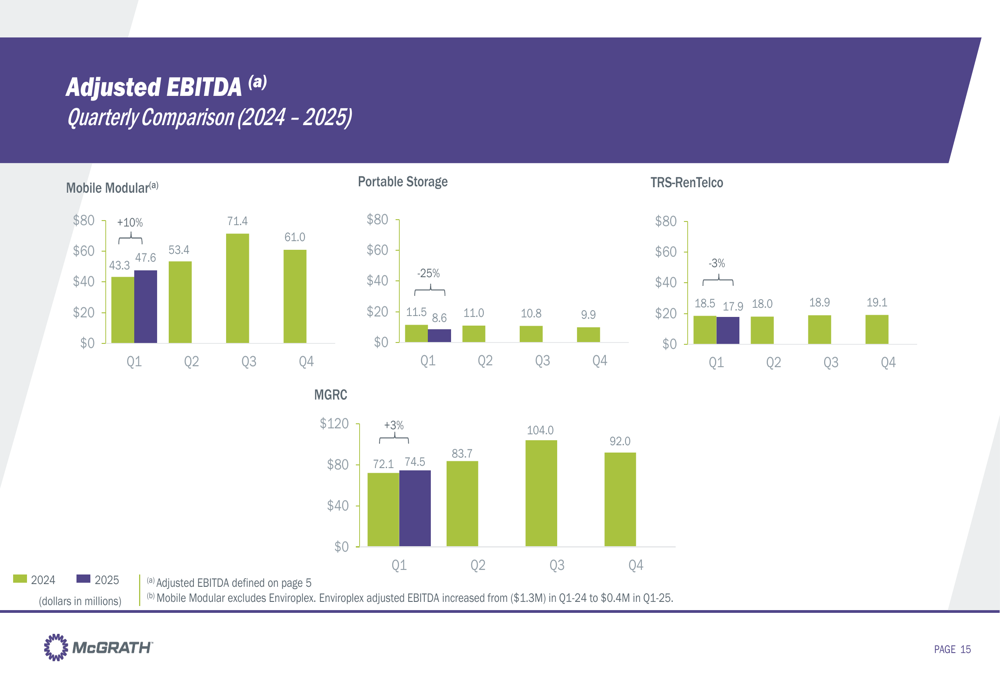

Breaking down the quarterly performance by segment reveals divergent trends. Mobile Modular showed solid growth with revenues increasing by 3% to $131.9 million and adjusted EBITDA rising by 10% to $47.6 million. This segment benefited from growth across both commercial and education customer bases. Additionally, revenue per unit on rent increased by 8% and revenue per new unit shipped rose by 12% on a last-twelve-months basis.

In contrast, the Portable Storage segment experienced a 13% decrease in rental revenues, primarily due to weaker demand conditions resulting from lower commercial construction project activity. In response, the company reduced new rental equipment purchases and focused on disciplined cost management for this segment.

The TRS-RenTelco segment showed signs of recovery with a slight increase in rental revenues, marking its first increase since Q1 2023. The company noted that improvement in market demand conditions was broad-based across segments, though it continued to reduce fleet size by selling rental equipment and limiting new purchases.

The quarterly rental revenue comparison across segments illustrates these trends:

Similarly, the adjusted EBITDA comparison highlights the strong performance of Mobile Modular against the challenges faced by other segments:

Segment Analysis

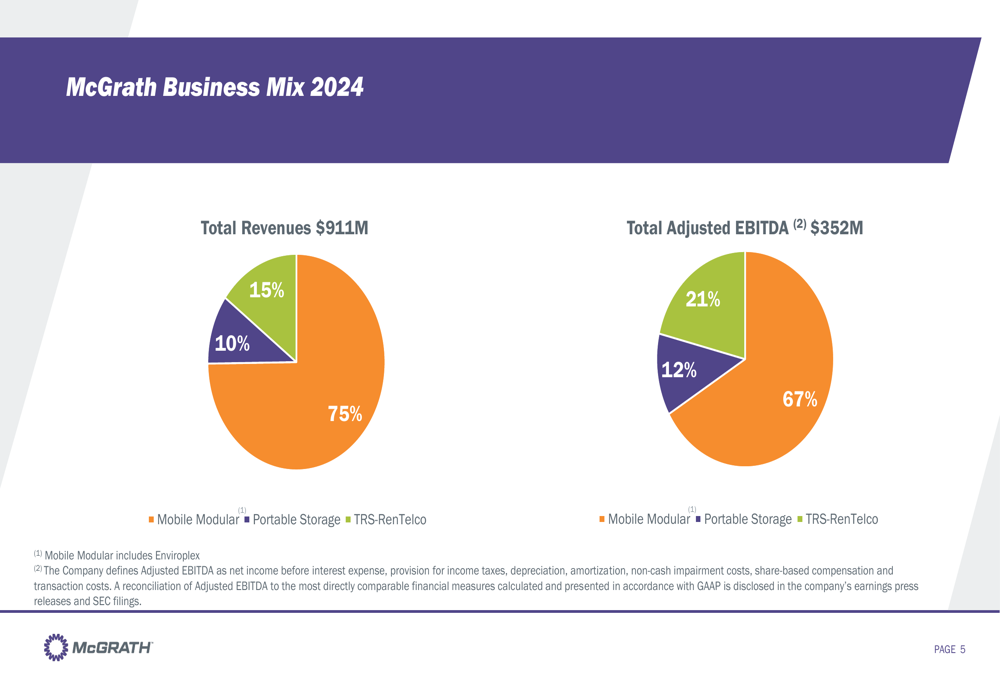

McGrath’s business mix remains heavily weighted toward Mobile Modular, which accounted for 75% of total revenues ($911 million) and 67% of total adjusted EBITDA ($352 million) in 2024. Portable Storage contributed 15% of revenues and 21% of adjusted EBITDA, while TRS-RenTelco represented 10% of revenues and 12% of adjusted EBITDA.

The Mobile Modular segment, which includes Enviroplex, reported Q1 2025 quarterly revenues of $132 million with a rental fleet of approximately 43,000 units valued at $1.415 billion (original acquisition cost). This segment continues to be the primary growth driver for McGrath, benefiting from increasing geographic coverage and wider service solutions to customers, including Mobile Modular Plus, Site Related Services, and Custom Modular Solutions.

Portable Storage, despite its current challenges, maintains a substantial rental fleet of approximately 42,000 units valued at $240 million, generating quarterly revenues of $21 million in Q1 2025. The segment’s weakness primarily stems from reduced commercial construction activity, which has prompted the company to adopt a more conservative approach to fleet expansion.

TRS-RenTelco, which specializes in electronic test equipment rentals, reported quarterly revenues of $35 million in Q1 2025, with a rental fleet of approximately 22,000 units valued at $334 million. The segment’s slight revenue increase represents a positive turn after several quarters of decline.

Strategic Initiatives

McGrath’s presentation emphasized three key strategic priorities: strategic growth, disciplined capital allocation, and shareholder value focus. The company is centering its growth strategy on the Mobile Modular segment, which represents its largest and highest-growth business. This includes expanding geographic coverage and developing wider service solutions for customers.

The company maintains a strong balance sheet and cash flow generation, which supports both organic investments and strategic acquisitions. McGrath’s commitment to shareholder value is evidenced by its 34-year track record of consecutive dividend increases and its share repurchase program, with 2 million shares authorized for repurchase as of September 18, 2024.

McGrath also highlighted its corporate social responsibility initiatives, noting that sustainability and responsible business practices remain "at the forefront in everything we do," according to President and CEO Joe Hanna. The company maintains a dedicated corporate responsibility site with additional information on environmental sustainability, social responsibility, and governance practices.

Financial Outlook

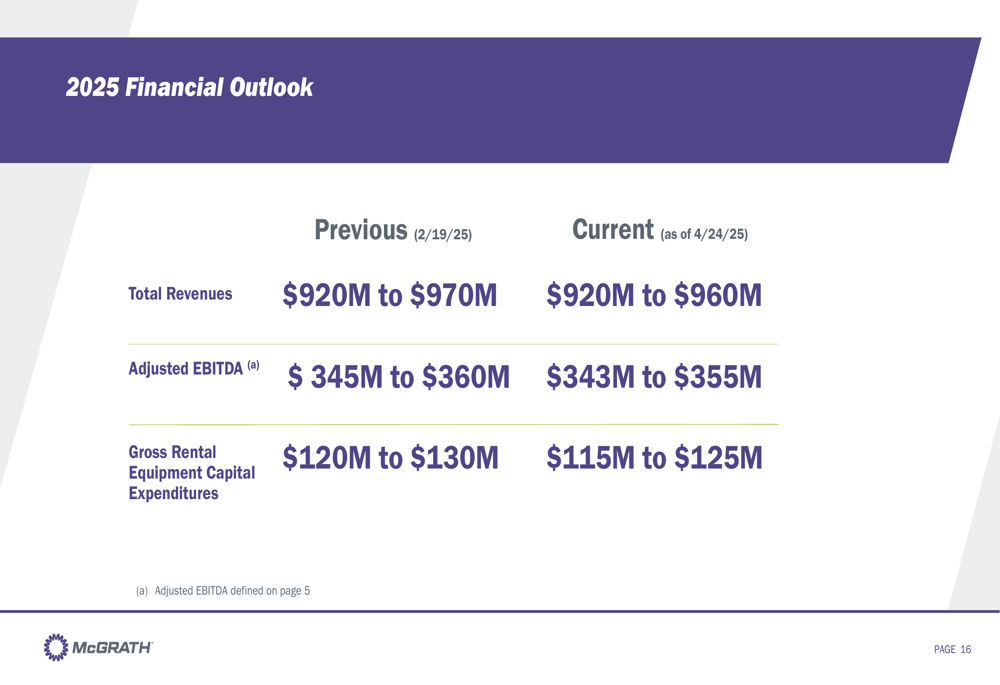

McGrath slightly adjusted its 2025 financial outlook compared to previous projections shared in February. The company now expects total revenues between $920 million and $960 million (down from $920-$970 million) and adjusted EBITDA between $343 million and $355 million (down from $345-$360 million). Gross rental equipment capital expenditures are projected to be $115-$125 million, reduced from the previous estimate of $120-$130 million.

These modest downward revisions reflect a cautious approach amid economic uncertainties, particularly in the commercial construction market that affects the Portable Storage segment. Despite these adjustments, McGrath maintains a positive long-term outlook, emphasizing its 40-year track record of navigating various economic challenges.

The company’s financial strategy continues to focus on disciplined capital allocation, with investments prioritized toward the high-performing Mobile Modular segment while maintaining cost discipline in more challenging areas. This balanced approach, combined with McGrath’s strong dividend history and share repurchase program, underscores management’s commitment to delivering long-term shareholder value despite near-term market fluctuations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.