Fed’s Powell opens door to potential rate cuts at Jackson Hole

MetLife, Inc. (NYSE:MET) reported first-quarter 2025 adjusted earnings of $1.35 billion, or $1.96 per share, representing a 7% year-over-year increase in adjusted EPS despite mixed segment performance. The insurer also announced a significant $10 billion variable annuity risk transfer agreement with Talcott Resolution Life Insurance (NSE:LIFI) Company, marking a strategic milestone in its risk management approach.

Quarterly Performance Highlights

MetLife’s Q1 2025 adjusted earnings of $1.35 billion showed modest growth of 1% compared to Q1 2024, while adjusted earnings per share increased 7% to $1.96. On a constant currency basis, adjusted earnings grew 5% and adjusted EPS increased 11%, reflecting the impact of ongoing share repurchases.

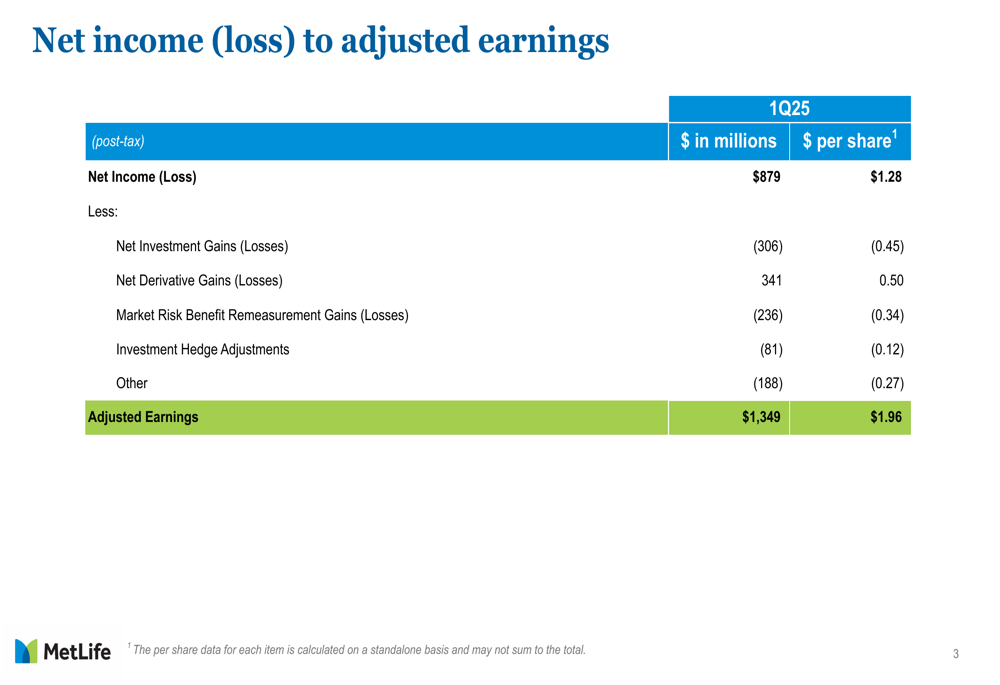

The company’s net income for the quarter was $879 million, or $1.28 per share, with the difference between net income and adjusted earnings primarily due to net derivative gains of $341 million offset by net investment losses of $306 million and market risk benefit remeasurement losses of $236 million.

As shown in the following reconciliation table, MetLife’s adjusted earnings exclude several non-recurring items to provide a clearer picture of underlying business performance:

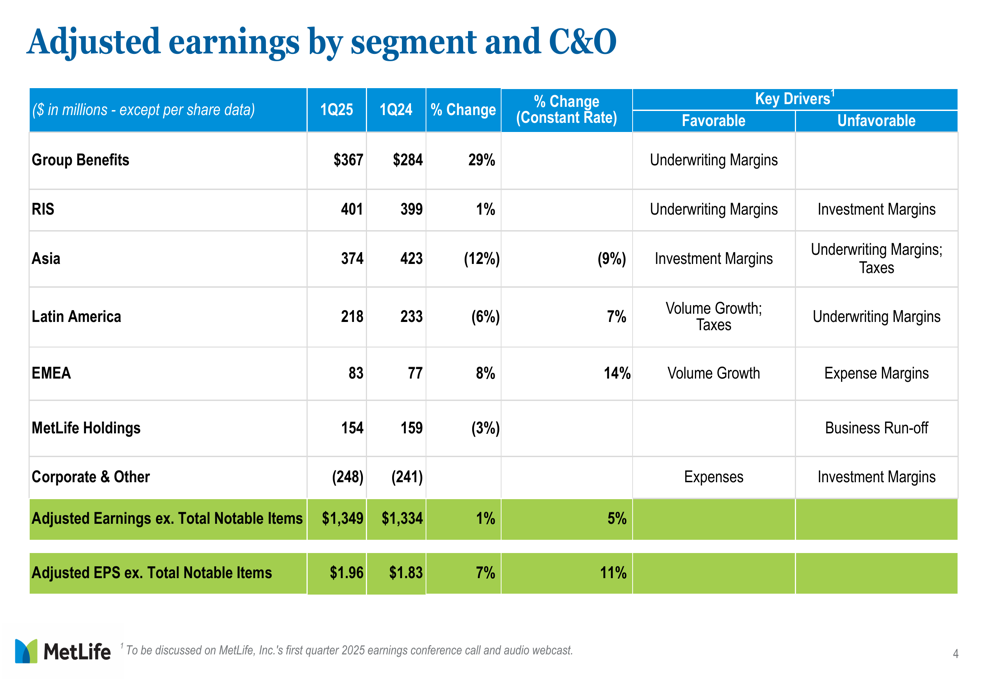

Segment performance varied significantly, with Group Benefits showing particularly strong results while international operations faced headwinds. The Group Benefits segment reported adjusted earnings of $367 million, a 29% increase from the prior year, driven by improved underwriting margins. Retirement & Income Solutions (RIS) delivered $401 million in adjusted earnings, up 1% year-over-year, benefiting from underwriting margins but offset by weaker investment margins.

The following table details the performance across all business segments:

Detailed Financial Analysis

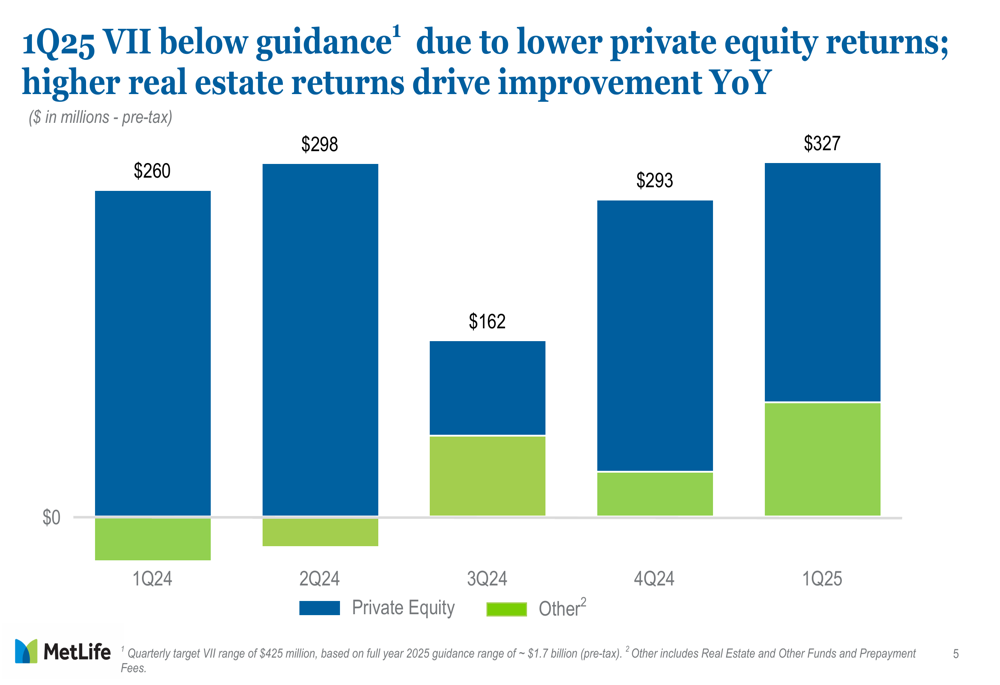

Variable Investment Income (VII) reached $327 million pre-tax in Q1 2025, up from $260 million in Q1 2024, but remained below the quarterly target of $425 million. The improvement was driven by higher real estate returns, which offset lower private equity performance.

As illustrated in the chart below, VII has shown volatility over the past five quarters, with the latest quarter showing the strongest performance in this period:

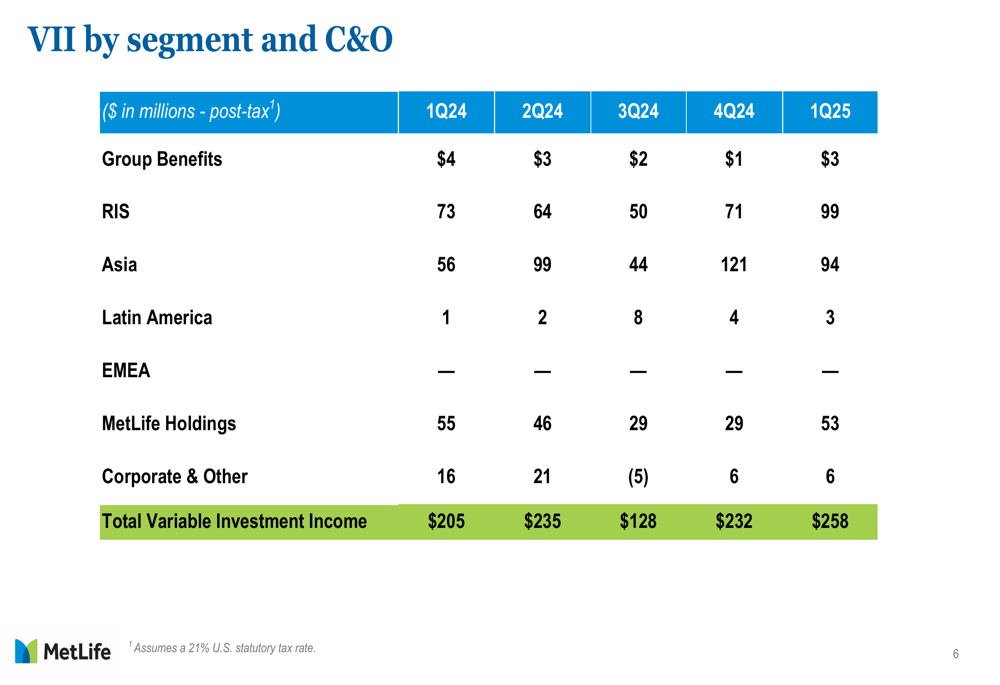

The distribution of VII across business segments reveals that RIS and Asia were the largest contributors, with post-tax VII of $99 million and $94 million respectively. MetLife Holdings also contributed significantly with $53 million.

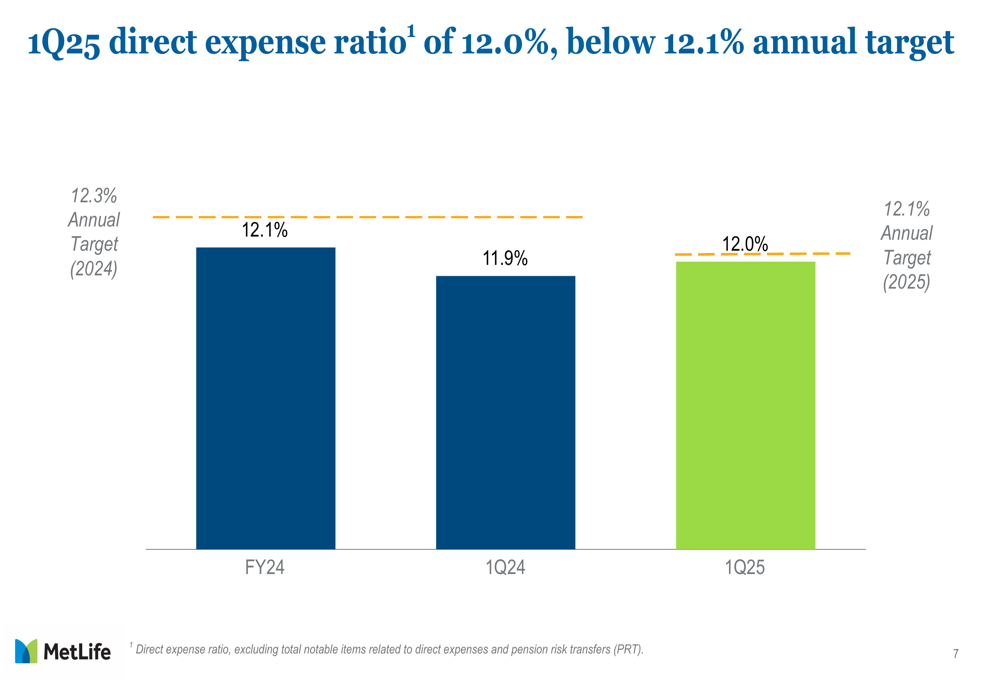

MetLife maintained strong expense discipline, with a direct expense ratio of 12.0% in Q1 2025, slightly up from 11.9% in Q1 2024 but still below the annual target of 12.1%. This demonstrates the company’s continued focus on operational efficiency.

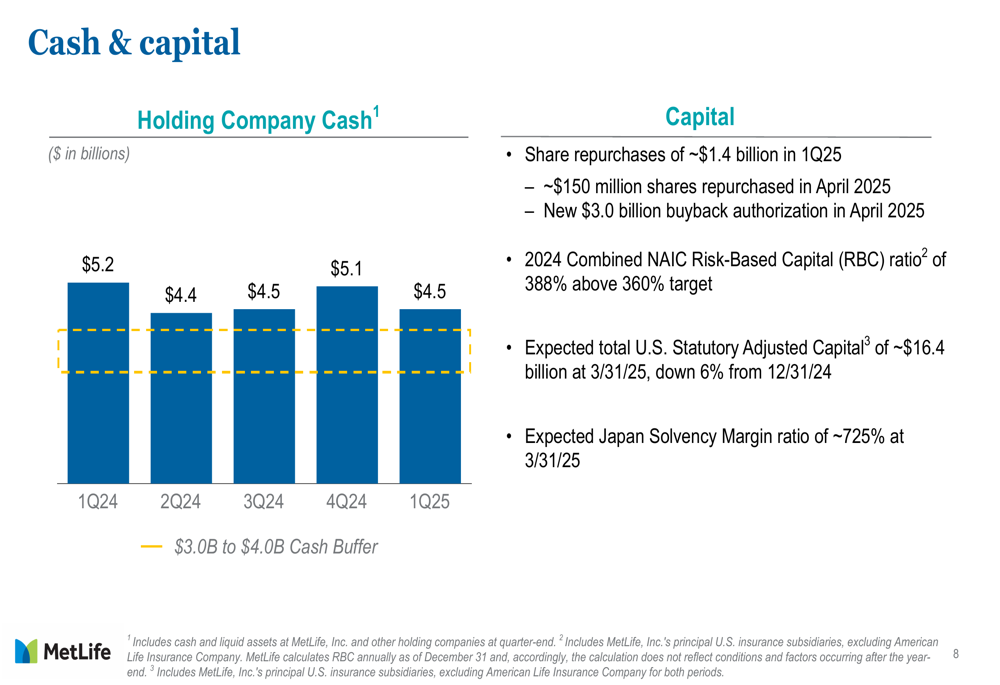

From a capital perspective, MetLife ended Q1 2025 with $4.5 billion in holding company cash, down from $5.1 billion at year-end 2024 but well above the company’s $3.0-$4.0 billion target buffer. The company repurchased approximately $1.4 billion of shares during the quarter, with an additional $150 million in April 2025, and announced a new $3.0 billion share repurchase authorization.

Strategic Initiatives

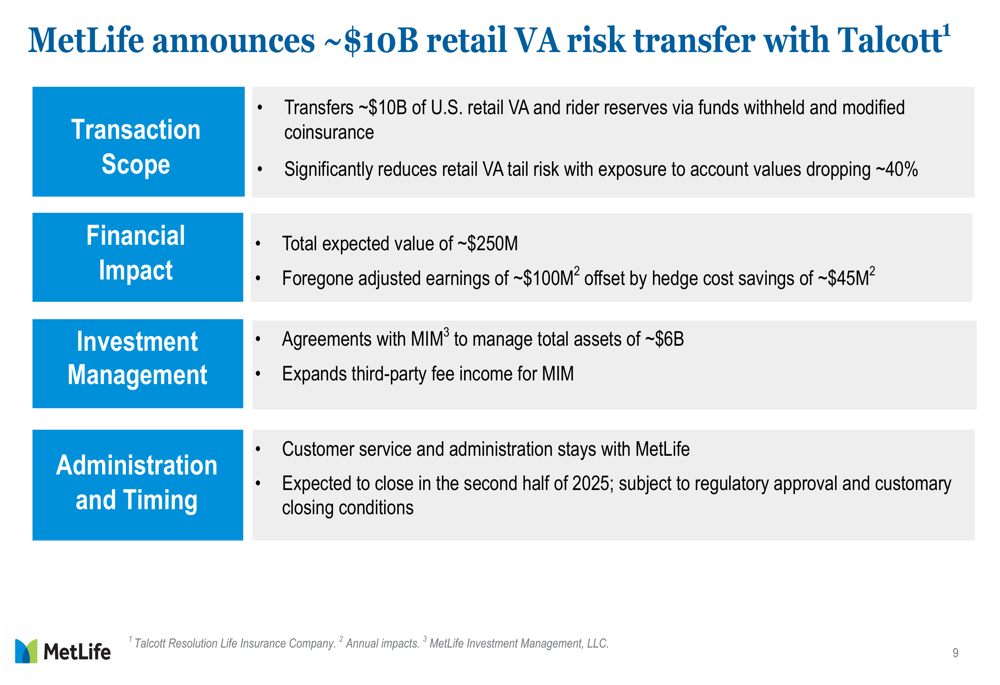

The most significant strategic announcement was MetLife’s approximately $10 billion retail variable annuity risk transfer agreement with Talcott Resolution Life Insurance Company. This transaction will reduce MetLife’s retail VA tail risk by transferring about 40% of its account value exposure through funds withheld and modified coinsurance arrangements.

The following slide details the key aspects of this transaction:

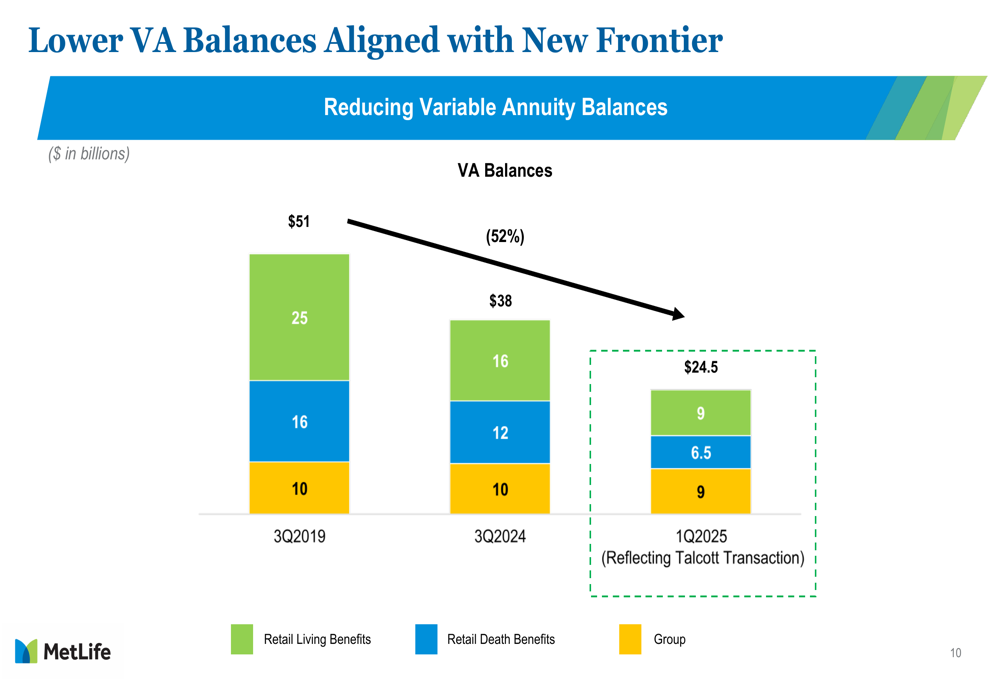

This transaction aligns with MetLife’s "New Frontier" strategy, which was unveiled in December 2024 and aims to optimize the company’s business mix and risk profile. The VA risk transfer represents a significant step in reducing MetLife’s exposure to market-sensitive businesses.

As shown in the following chart, MetLife has been systematically reducing its variable annuity balances from $51 billion in Q3 2019 to $38 billion in Q3 2024, with a further reduction to $24.5 billion expected after the Talcott transaction:

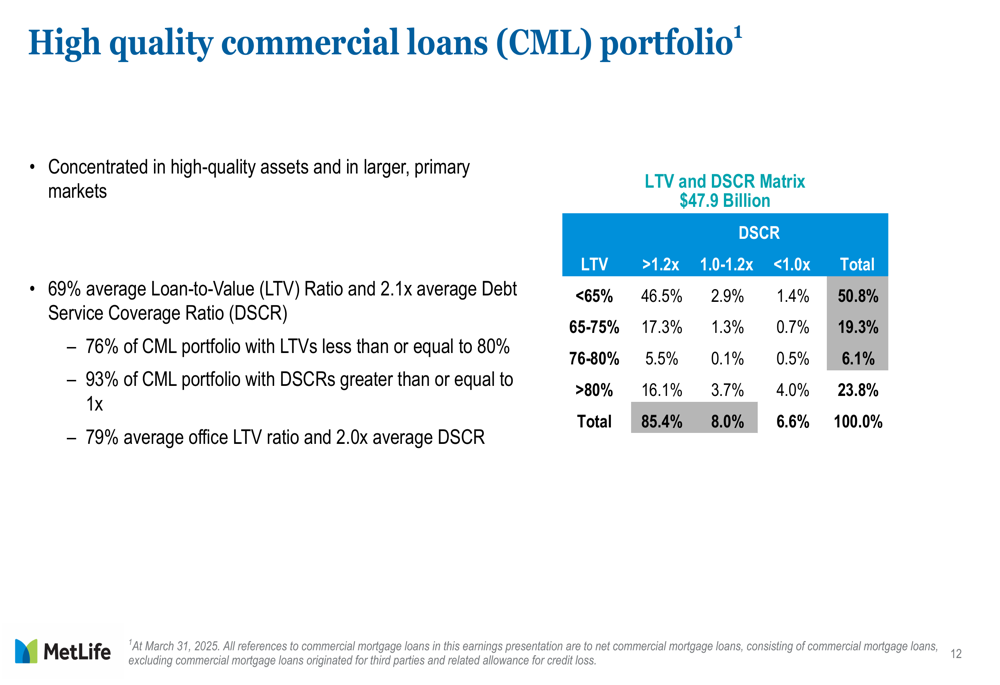

MetLife’s commercial mortgage loan portfolio remains high quality, with a 69% average loan-to-value ratio and 2.1x average debt service coverage ratio. Approximately 76% of the portfolio has loan-to-value ratios less than or equal to 80%, and 93% has debt service coverage ratios greater than or equal to 1x.

The following matrix provides a detailed breakdown of the $47.9 billion commercial mortgage loan portfolio:

Forward-Looking Statements

MetLife expects the Talcott transaction to close in the second half of 2025, subject to regulatory approval and customary closing conditions. The company anticipates a total economic value of approximately $250 million from the transaction, with foregone adjusted earnings of approximately $100 million annually offset by hedge cost savings of around $45 million annually.

The company’s investment management arm, MetLife Investment Management (MIM), will continue to manage approximately $6 billion in assets related to the transaction, expanding its third-party fee income.

MetLife’s capital position remains strong, with a 2024 combined NAIC Risk-Based Capital ratio of 388%, above its 360% target. However, the company reported that its expected total U.S. Statutory Adjusted Capital of approximately $16.4 billion as of March 31, 2025, represents a 6% decrease from December 31, 2024.

The company’s stock closed at $75.37 on April 30, 2025, but was trading down 2.07% in pre-market activity following the earnings release, suggesting some investor concerns despite the generally positive results and strategic progress.

As MetLife continues to implement its New Frontier strategy, investors will be watching closely to see how the company balances growth initiatives with risk management and capital return priorities in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.