Microvast Holdings announces departure of chief financial officer

MGIC Investment Corporation (NYSE:MTG) has released its quarterly supplement for the first quarter of 2025, showcasing the mortgage insurer’s continued focus on maintaining strong credit quality and a robust capital position. The presentation, dated May 1, 2025, provides a comprehensive overview of the company’s risk portfolio, capital structure, and geographic distribution of insurance in force.

Portfolio Quality and Risk Metrics

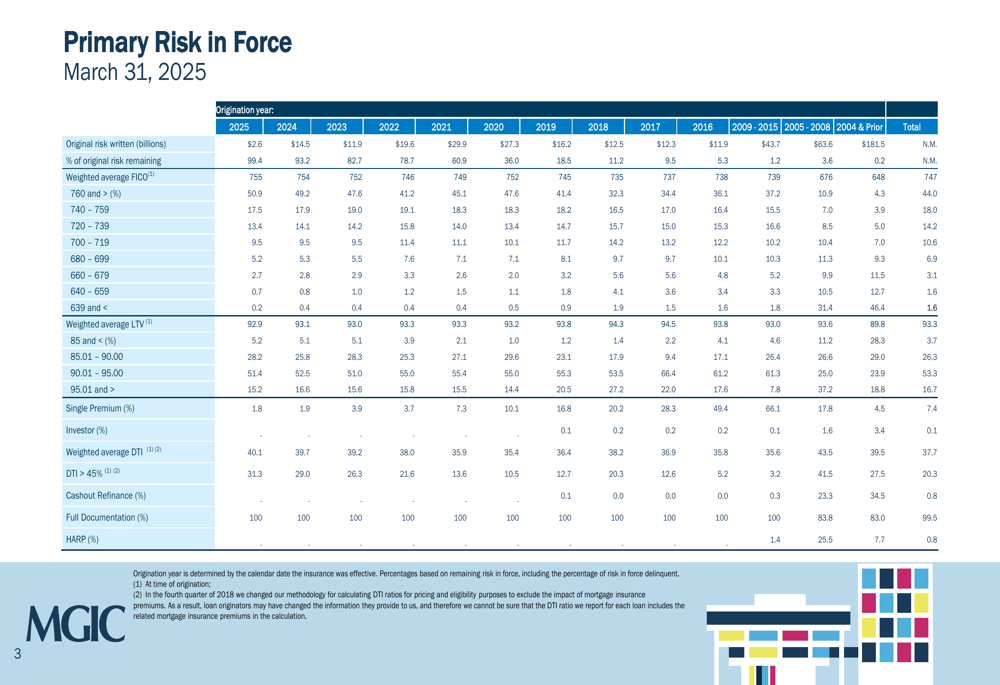

MGIC’s primary risk in force continues to demonstrate solid credit characteristics. The portfolio maintains a weighted average FICO score of 747 and a weighted average loan-to-value (LTV) ratio of 93.3%, indicating the company’s disciplined approach to underwriting. The weighted average debt-to-income (DTI) ratio stands at 37.7%, with 20.3% of the portfolio having DTI ratios exceeding 45%.

As shown in the following detailed breakdown of the company’s primary risk in force, MGIC has written $181.5 billion in original risk, with varying levels of risk remaining across different origination years:

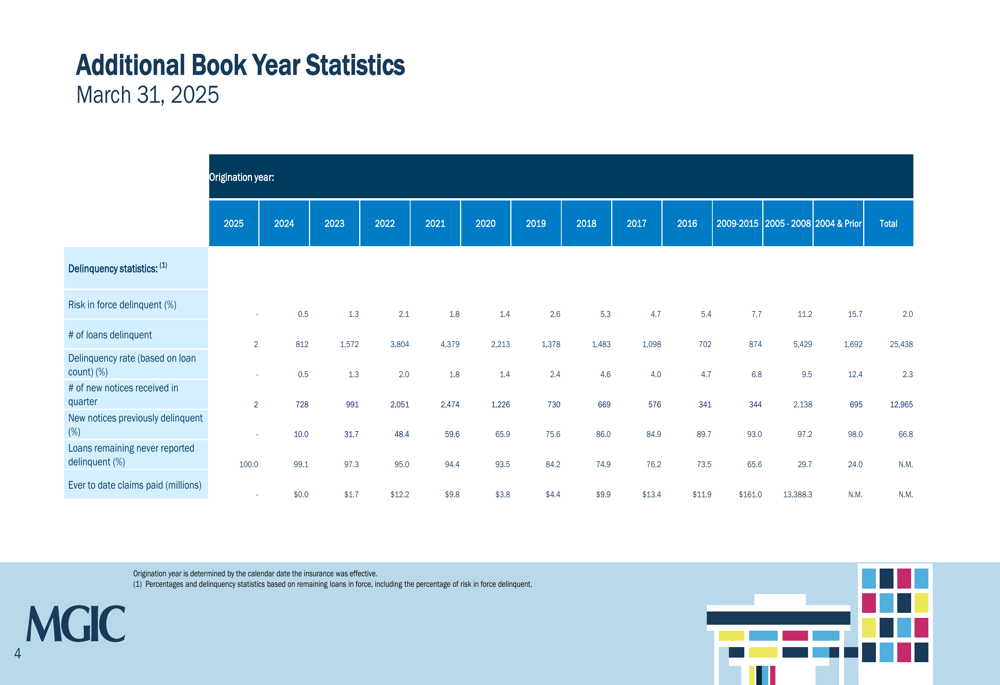

The credit performance of MGIC’s portfolio remains strong, with relatively low delinquency rates across most origination years. The company’s additional book year statistics reveal the percentage of risk in force delinquent, number of loans delinquent, and delinquency rates based on loan count.

This strong credit performance aligns with the company’s statements during its Q2 2024 earnings call, where CEO Tim Mattke noted, "We continue to be very pleased with the overall credit quality and performance of our portfolio. This credit performance continues to be a tailwind for our financial results."

Capital Position and Reinsurance Strategy

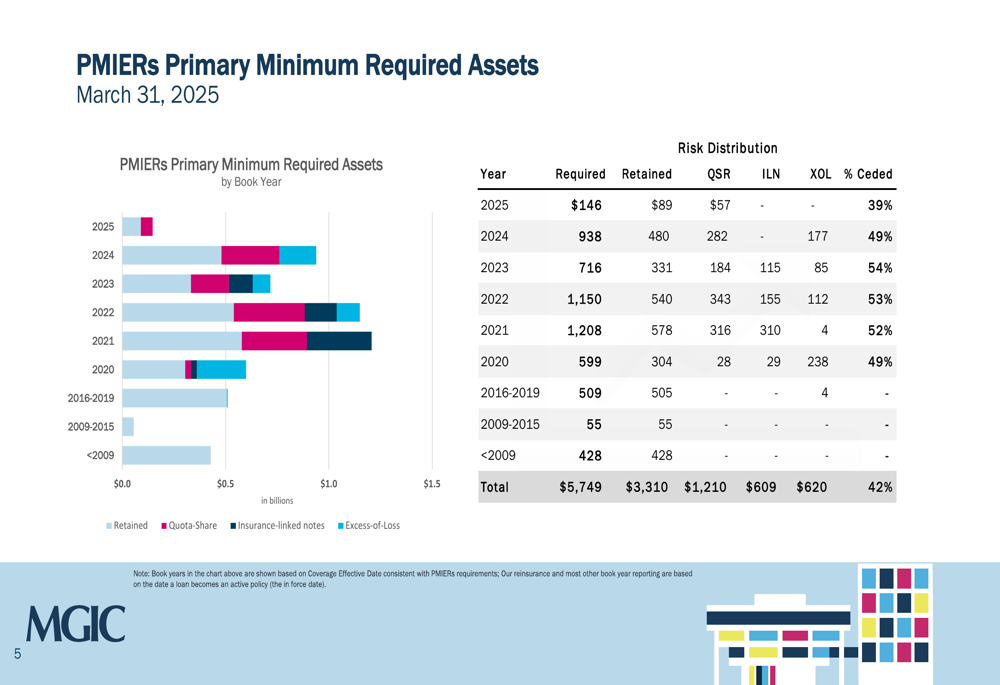

MGIC continues to maintain a robust capital position, with significant risk transfer through reinsurance arrangements. The company’s Primary Minimum Required Assets (PMIERS) as of March 31, 2025, stand at $5,749 million, with 42% of risk ceded through various reinsurance structures including Quota-Share, Insurance-linked notes, and Excess-of-Loss arrangements.

The following chart illustrates MGIC’s PMIERS capital requirements by book year and the distribution of risk retention versus transfer:

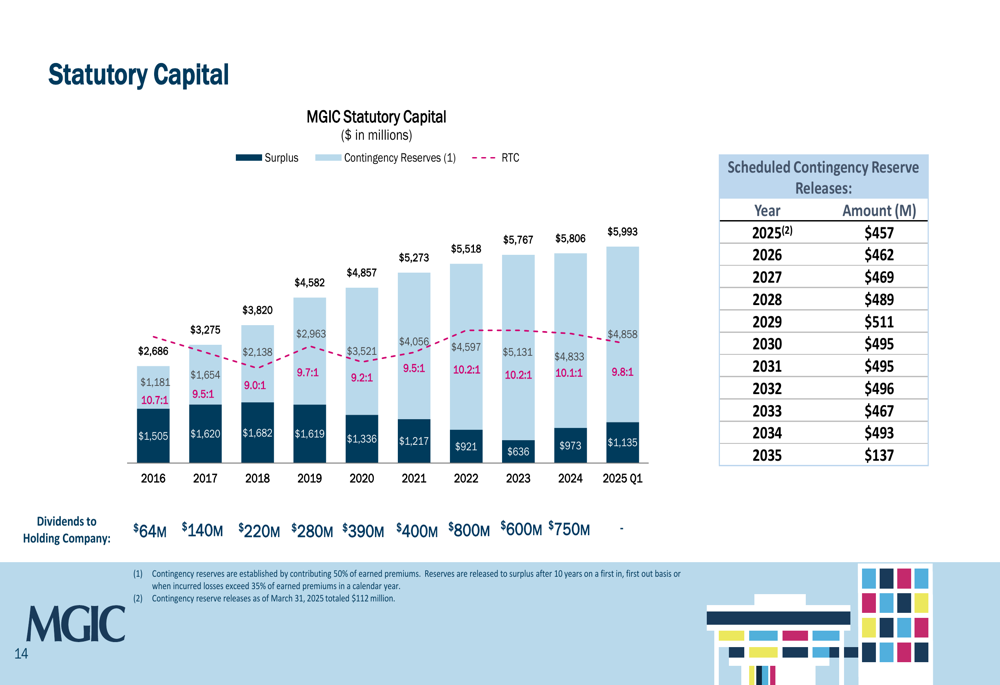

The company’s statutory capital position is further strengthened by scheduled contingency reserve releases, with $457 million expected to be released in 2025 and $462 million in 2026. These releases provide additional financial flexibility for MGIC in the coming years.

This capital management approach is consistent with the company’s strategy outlined in its Q2 2024 earnings call, where CFO Nathan Colson emphasized, "Maintaining financial strength and flexibility are the cornerstones of our approach to capital management."

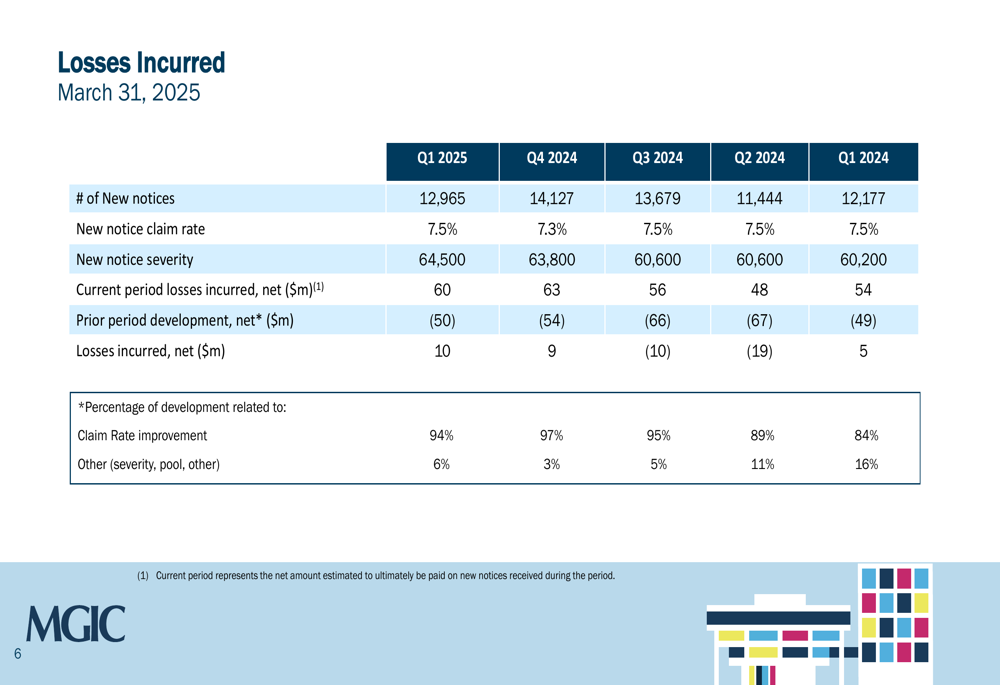

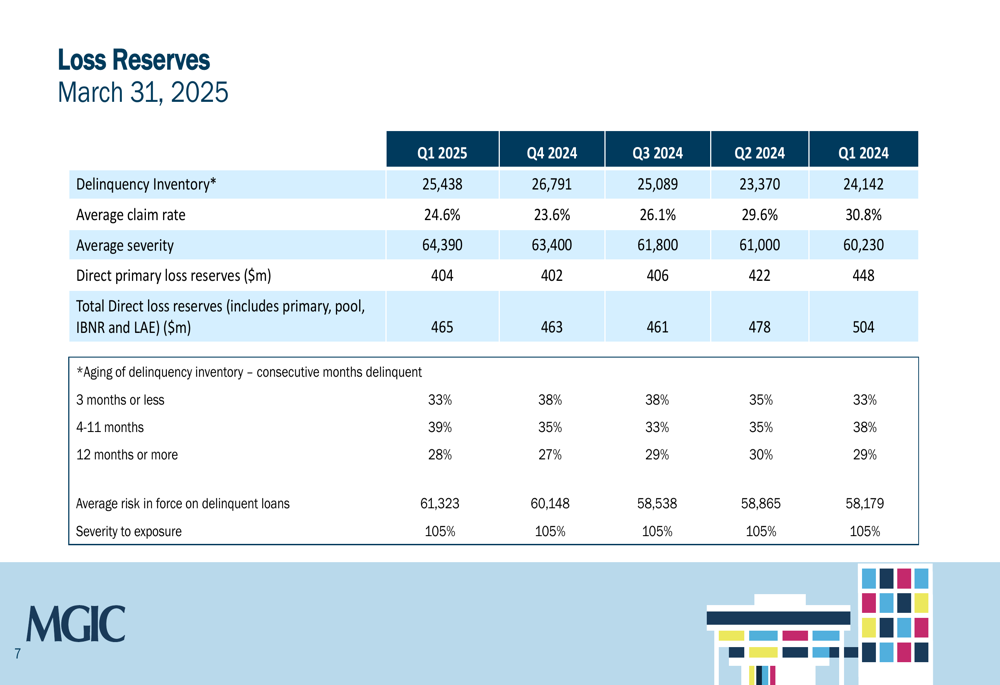

Loss Experience and Reserves

MGIC reported 12,965 new delinquency notices in Q1 2025, with a new notice claim rate of 7.5%. The company’s losses incurred for the quarter were $10 million net, reflecting the continued favorable credit environment.

The company’s loss reserves data shows the aging of delinquency inventory and the average risk in force on delinquent loans, providing insight into potential future claims.

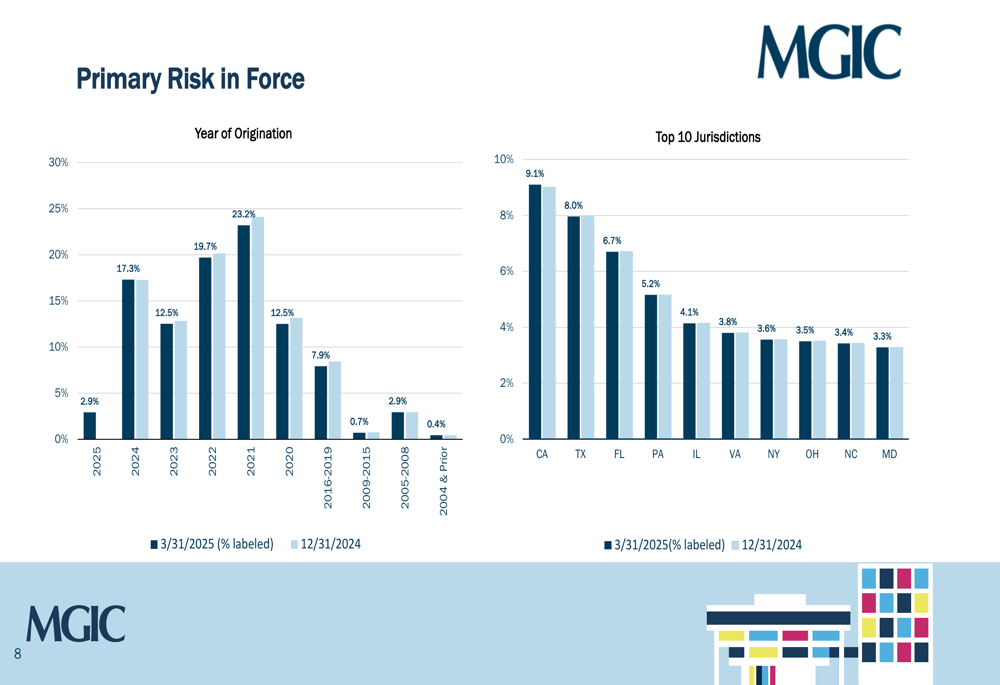

Geographic and Vintage Distribution

MGIC’s risk portfolio demonstrates geographic diversification, with the top jurisdictions including California, Texas, Florida, Pennsylvania, Illinois, Virginia, New York, Ohio, North Carolina, and Maryland. This diversification helps mitigate concentration risk in any single housing market.

The following chart shows the distribution of primary risk in force by origination year and jurisdiction:

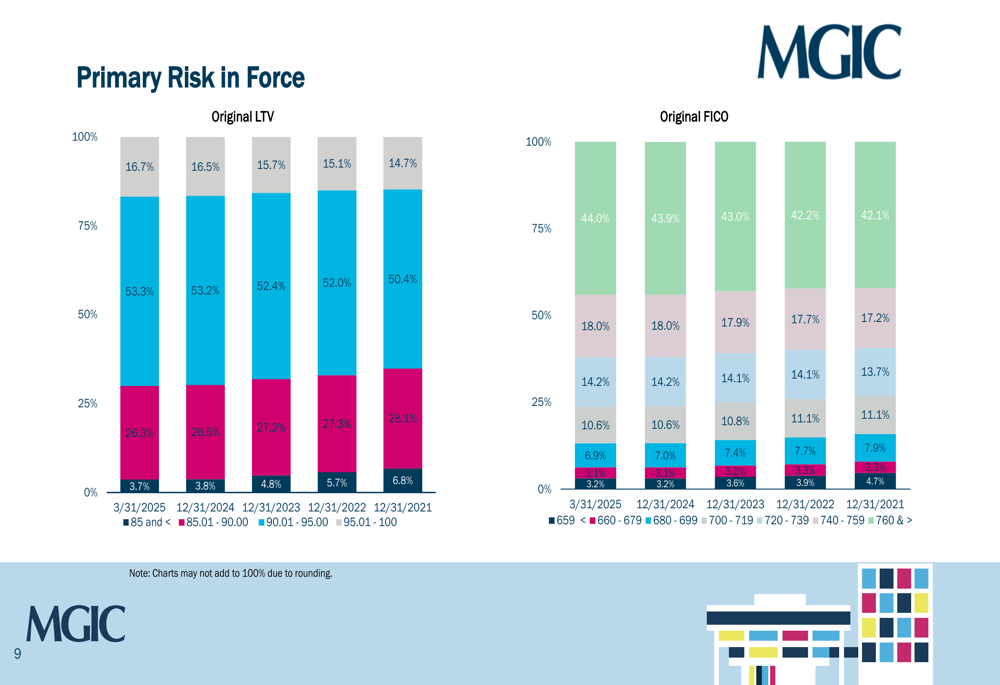

The company’s risk distribution by loan-to-value ratio and FICO score further illustrates the quality of the portfolio, with comparisons across multiple years:

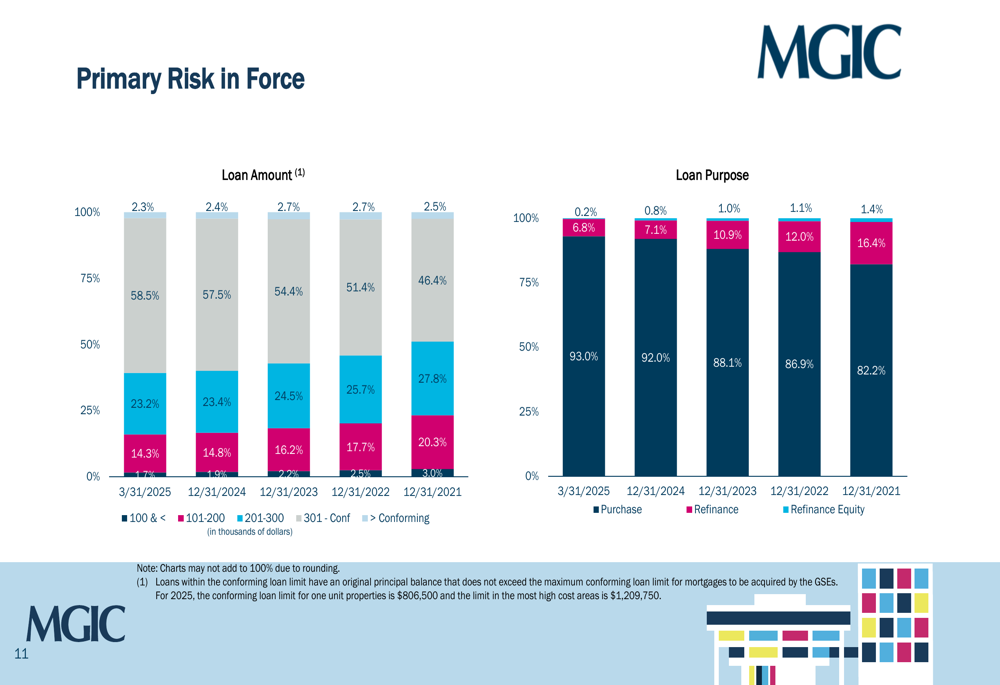

Additional portfolio characteristics include breakdowns by property type, occupancy status, loan amount, and loan purpose, providing a comprehensive view of MGIC’s risk exposure:

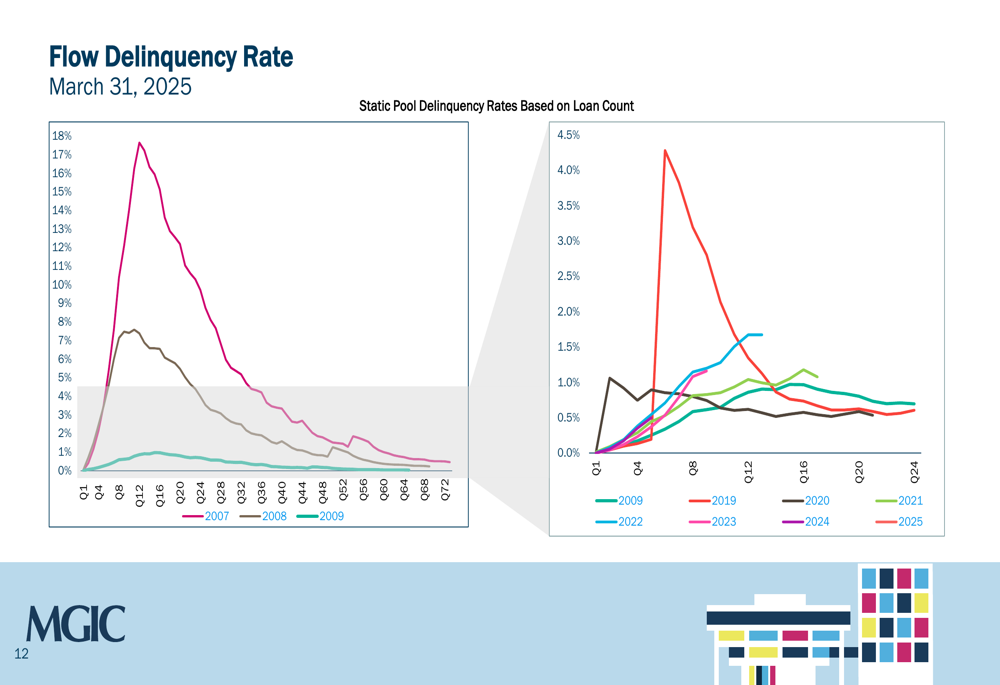

Delinquency Trends and Capital Requirements

The presentation includes static pool delinquency rates based on loan count, comparing the performance of different origination years. This analysis helps identify potential trends in credit performance across various vintages.

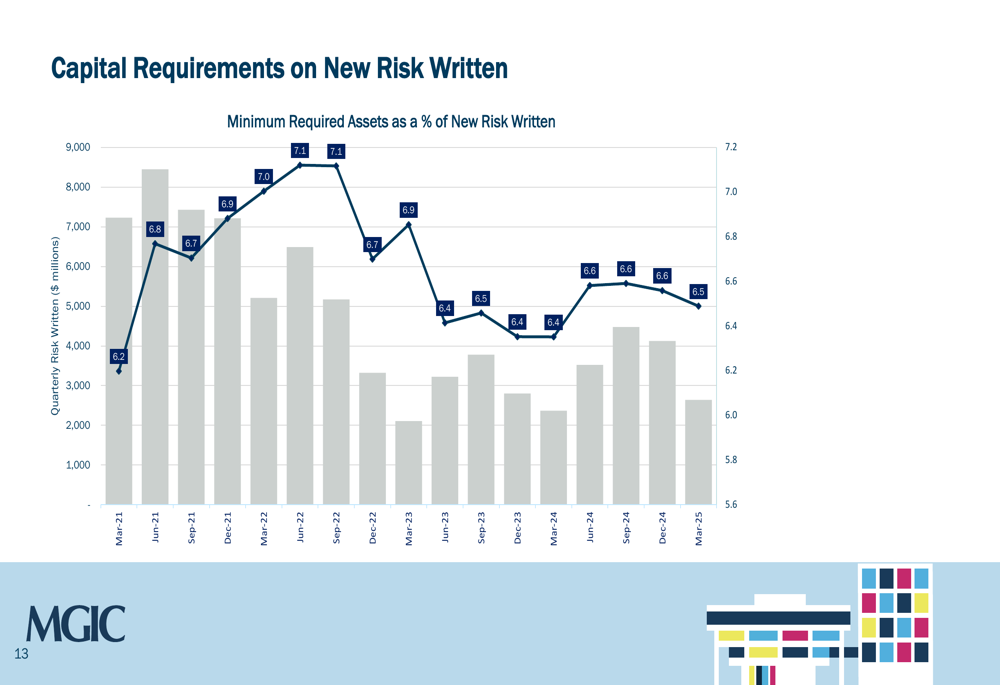

MGIC’s capital requirements on new risk written show the relationship between quarterly risk written and minimum required assets as a percentage of new risk written:

Forward-Looking Outlook

While the Q1 2025 presentation focuses primarily on current portfolio metrics rather than forward-looking statements, the company’s Q2 2024 earnings call provides context for its strategic direction. During that call, CEO Tim Mattke expressed confidence in the company’s market position and ability to execute on business strategies, noting, "I continue to be encouraged by positive credit trends we are experiencing in our existing insurance portfolio, the favorable employment trends and the resiliency of the housing market."

The mortgage origination industry continues to face challenges from higher interest rates and limited housing supply, but MGIC’s strong credit performance and capital position appear to position it well to navigate these headwinds.

In conclusion, MGIC’s Q1 2025 quarterly supplement demonstrates the company’s continued focus on maintaining strong credit quality, effective risk management, and a robust capital position. The diversification of its portfolio across geographies and vintages, combined with its reinsurance strategy, reflects a balanced approach to risk that has served the company well in previous cycles.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.