Street Calls of the Week

Introduction & Market Context

M/I Homes (NYSE:MHO) delivered a mixed performance in the second quarter of 2025, achieving record revenue while facing margin pressure in a challenging housing market environment. The homebuilder, ranked 13th on the BUILDER 100 list, continues to expand its community count and geographic presence while navigating fluctuating interest rates and affordability concerns.

The company’s stock responded positively to the earnings report, with a pre-market increase of 1.77% and closing up 2.04% at $120.19 on August 1, 2025. This investor confidence comes despite some challenging metrics, reflecting the market’s appreciation for MHO’s strategic positioning and financial strength.

Quarterly Performance Highlights

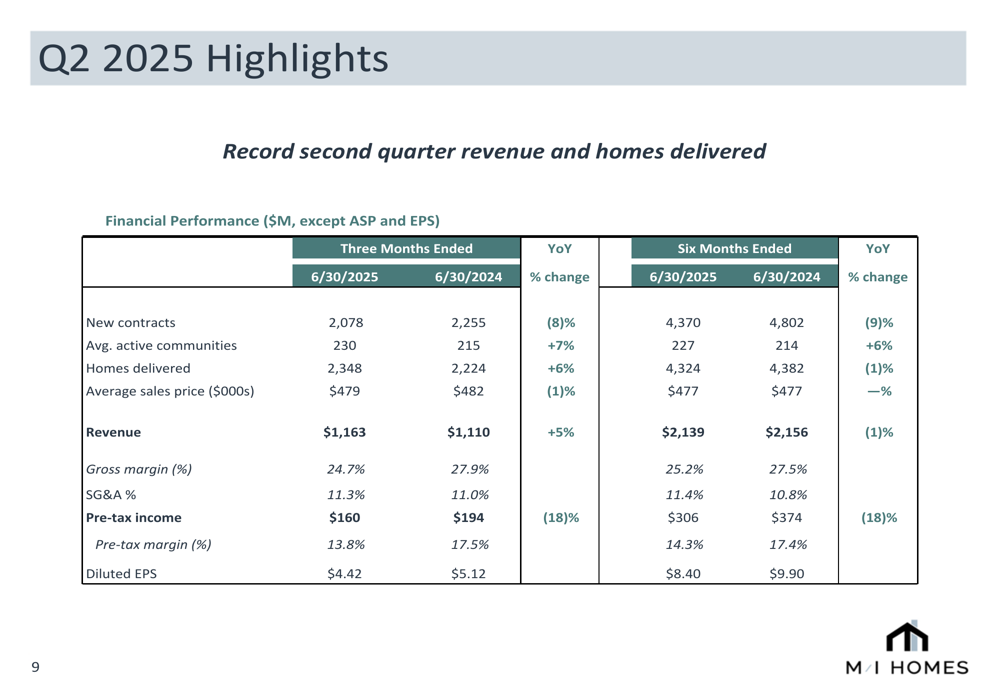

M/I Homes achieved record second quarter revenue of $1.16 billion, representing a 5% increase year-over-year and exceeding analyst expectations by 7.14%. The company delivered 2,348 homes during the quarter, a 6% increase compared to Q2 2024, while maintaining a relatively stable average sales price of $479,000 (down 1% year-over-year).

As shown in the following comprehensive financial results table from the company’s presentation:

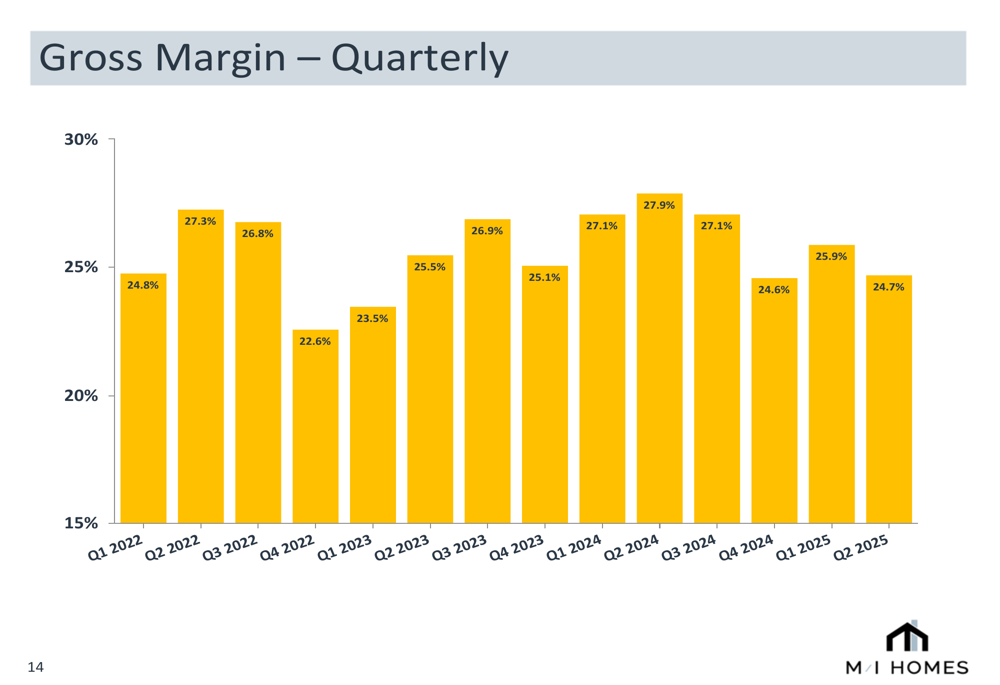

Despite the revenue growth, M/I Homes faced margin pressure during the quarter. Gross margin declined to 24.7% from 27.9% in the prior year period, while SG&A expenses as a percentage of revenue increased slightly to 11.3% from 11.0%. These factors contributed to an 18% decrease in pre-tax income to $160 million and a decline in diluted EPS to $4.42 from $5.12 in Q2 2024.

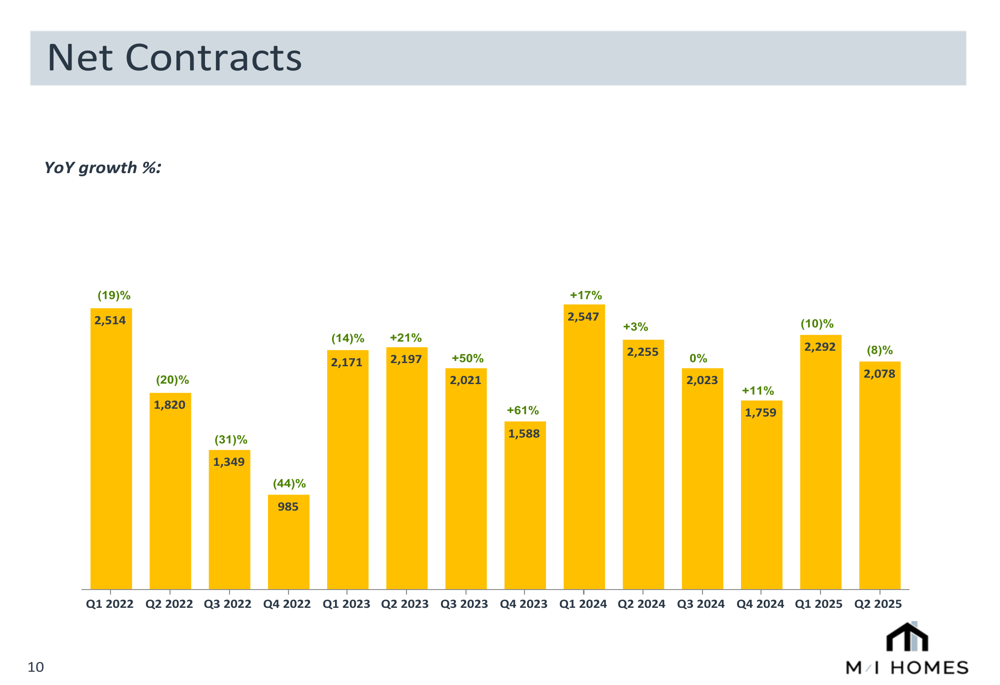

New contracts decreased by 8% year-over-year to 2,078 homes, though this was partially offset by a 7% increase in average active communities to 230. The following chart illustrates the trend in net contracts over recent quarters:

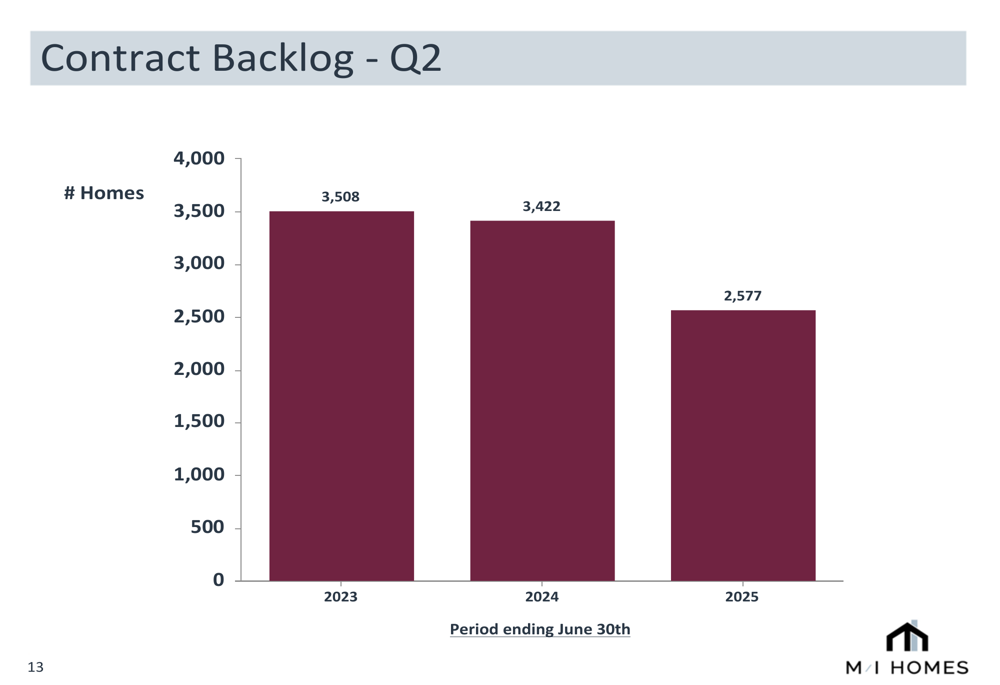

The company’s backlog position has declined compared to previous years, reflecting both the challenging market conditions and the company’s focus on converting existing orders to closings:

Strategic Initiatives and Market Position

M/I Homes continues to emphasize its "Smart Series" homes, which focus on affordability and represented 52% of Q2 2025 sales with an average selling price of $400,000. This strategic emphasis on more affordable homes positions the company well in a market where affordability remains a key concern for buyers.

The company maintains a strong presence across its operating regions, with top 5 positions in 8 markets and top 10 positions in 13 markets. This geographic diversification helps mitigate regional market fluctuations.

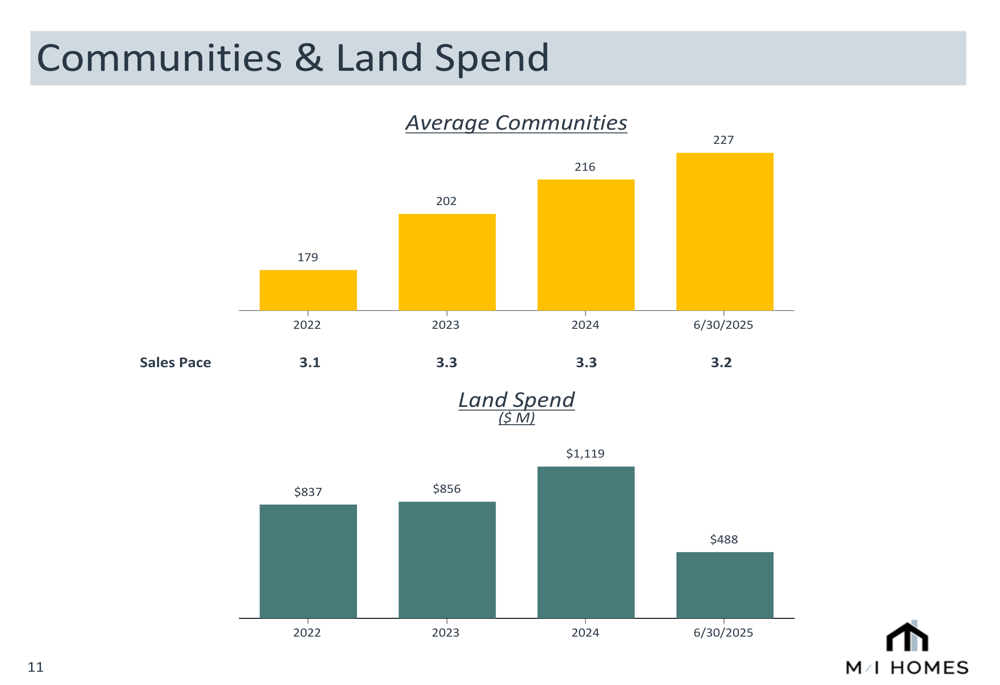

M/I Homes has been steadily growing its community count while maintaining a consistent sales pace, as illustrated in the following chart:

The company’s mortgage and title services continue to be a competitive advantage, with a 92% capture rate in Q2 2025. M/I Financial Services generated $14 million in pre-tax income on $31 million in revenue during the quarter, serving a strong buyer profile with an average credit score of 746 and an average down payment of 17%.

Financial Position and Outlook

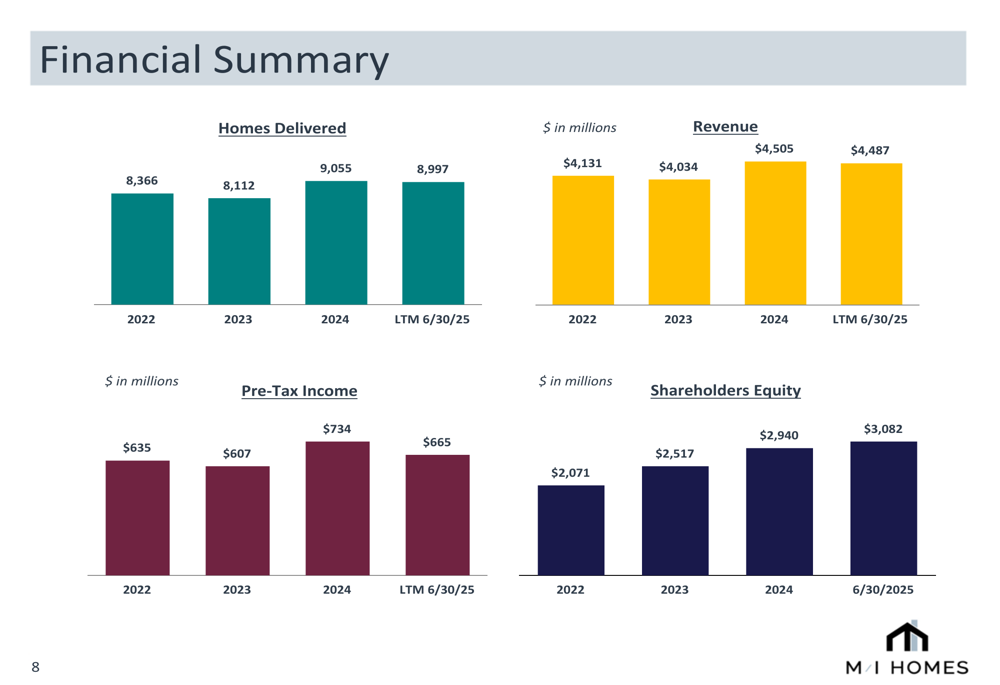

M/I Homes maintains a robust financial position with $800 million in cash and equivalents as of June 30, 2025, and a negative net homebuilding debt to capitalization ratio of -3%, indicating more cash than debt. The company’s shareholders’ equity has grown to $3.08 billion, reflecting continued profitability and reinvestment.

The following chart illustrates the company’s financial performance over recent years:

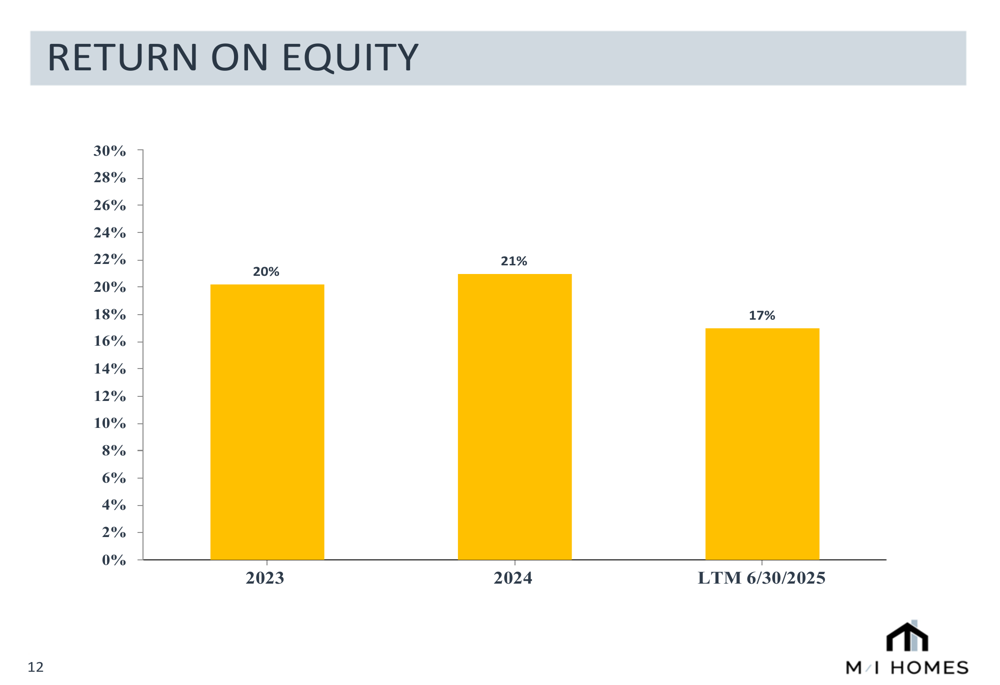

The company’s return on equity has moderated from its peak but remains solid at 17% for the last twelve months ending June 30, 2025:

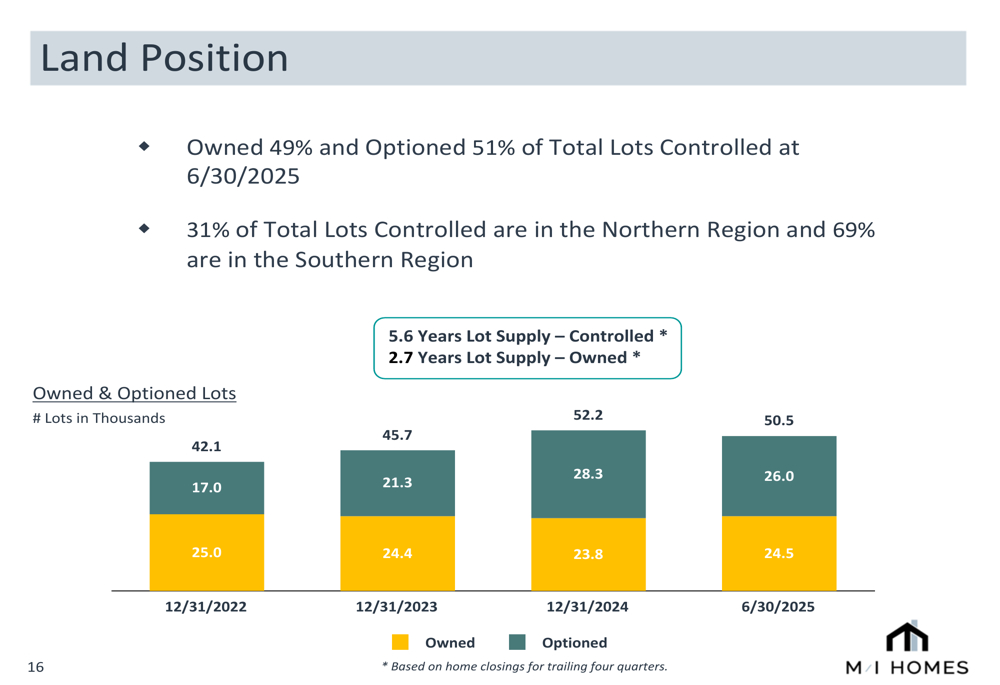

M/I Homes continues to execute a balanced land strategy, with 49% owned lots and 51% optioned lots as of June 30, 2025. This approach provides flexibility while maintaining sufficient inventory for future growth. The company controls 50,500 lots, representing 5.6 years of supply based on trailing four quarters of closings.

As shown in the following land position chart:

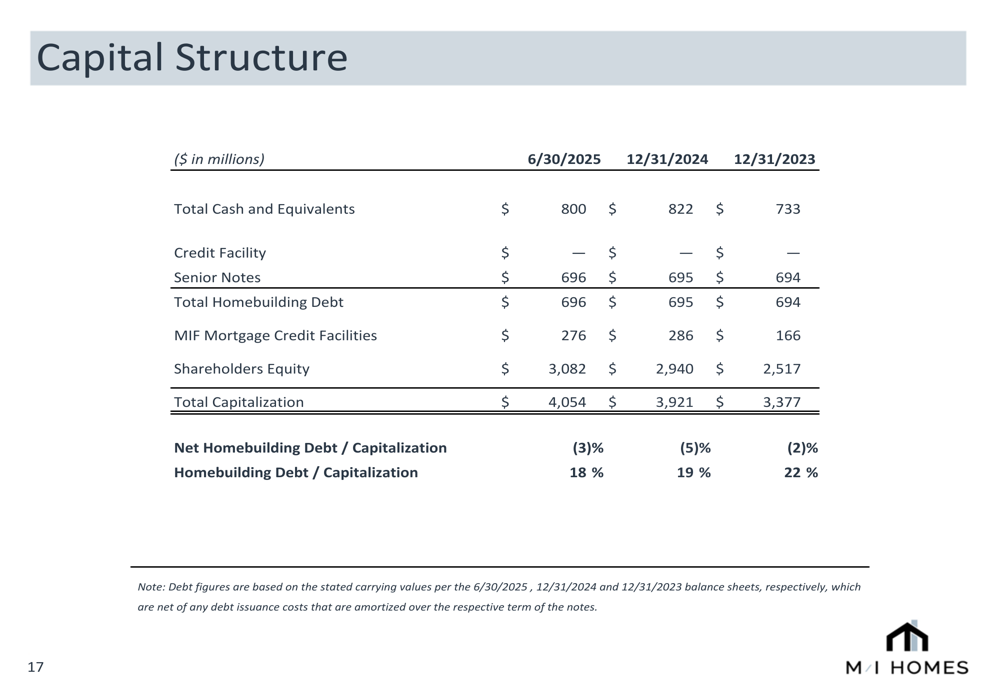

The company’s capital structure remains conservative, with total homebuilding debt of $696 million and a homebuilding debt to capitalization ratio of 18% as of June 30, 2025:

Challenges and Forward-Looking Statements

Despite the record revenue achievement, M/I Homes faces several challenges, including declining gross margins, decreased new contracts, and a reduced backlog. The company’s gross margin has fluctuated in recent quarters, as illustrated below:

Looking ahead, M/I Homes has outlined several strategic priorities:

- Maintaining a strong balance sheet

- Focusing on profitability and returns

- Emphasizing affordability

- Increasing community count

- Growing market share

- Continuing focus on core values including customer service, quality, and building better homes

CEO Bob Schottenstein highlighted the company’s resilience during the earnings call, stating, "The fact that we can post 14% income in this environment, I think is extraordinary." CFO Phil Creek emphasized a strategic focus on growth, noting, "We’re not trying to force volume like certain other builders are."

While the company anticipates a 5% growth in community count for 2025, with plans to deliver 12,000 to 14,000 homes across 17 markets, management acknowledges potential margin stabilization or slight decreases as market conditions evolve. The ongoing volatility in interest rates remains a key risk factor for homebuyer affordability and market demand.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.